Are Car Loan Rates Going Down? The Real Story

While overall car loan rates aren’t dropping dramatically yet, you have the power to lower your personal rate. By improving your credit score, getting pre-approved from multiple lenders, and choosing a shorter loan term, you can secure a much better deal. These smart moves can save you thousands, regardless of national trends.

Thinking about a new car? You might be wondering about loan rates. It can feel confusing when you hear different things on the news. Are car loan rates going down, or are they staying high? It’s a big question, and the answer can save you a lot of money.

You’re not alone in feeling this way. Many drivers worry about getting a good deal on a car loan. The good news is, you have more control than you think. We are going to walk through this together. This guide will show you simple, proven steps to get the best possible rate, no matter what the market is doing. Let’s get you ready to drive away with a great deal.

First, let’s talk about the big picture. For a while, interest rates for everything, including car loans, were on the rise. This was largely because the Federal Reserve was working to manage the economy. When their rates go up, the rates lenders offer you for a car loan also tend to go up. You can read more about how this works directly from the Federal Reserve.

So, are car loan rates going down right now? The answer is a bit mixed. We are not seeing a massive, widespread drop across the board. However, the period of rapid increases seems to be stabilizing. Some lenders are starting to offer more competitive rates to attract buyers. This means it’s a critical time to be a smart shopper.

The most important thing to remember is this: the national average rate is not the rate you have to accept. Your personal financial health, especially your credit score, plays the biggest role in the interest rate you are offered. That’s where your power lies. Even if national rates are high, you can take specific steps to secure a loan that’s much lower than the average.

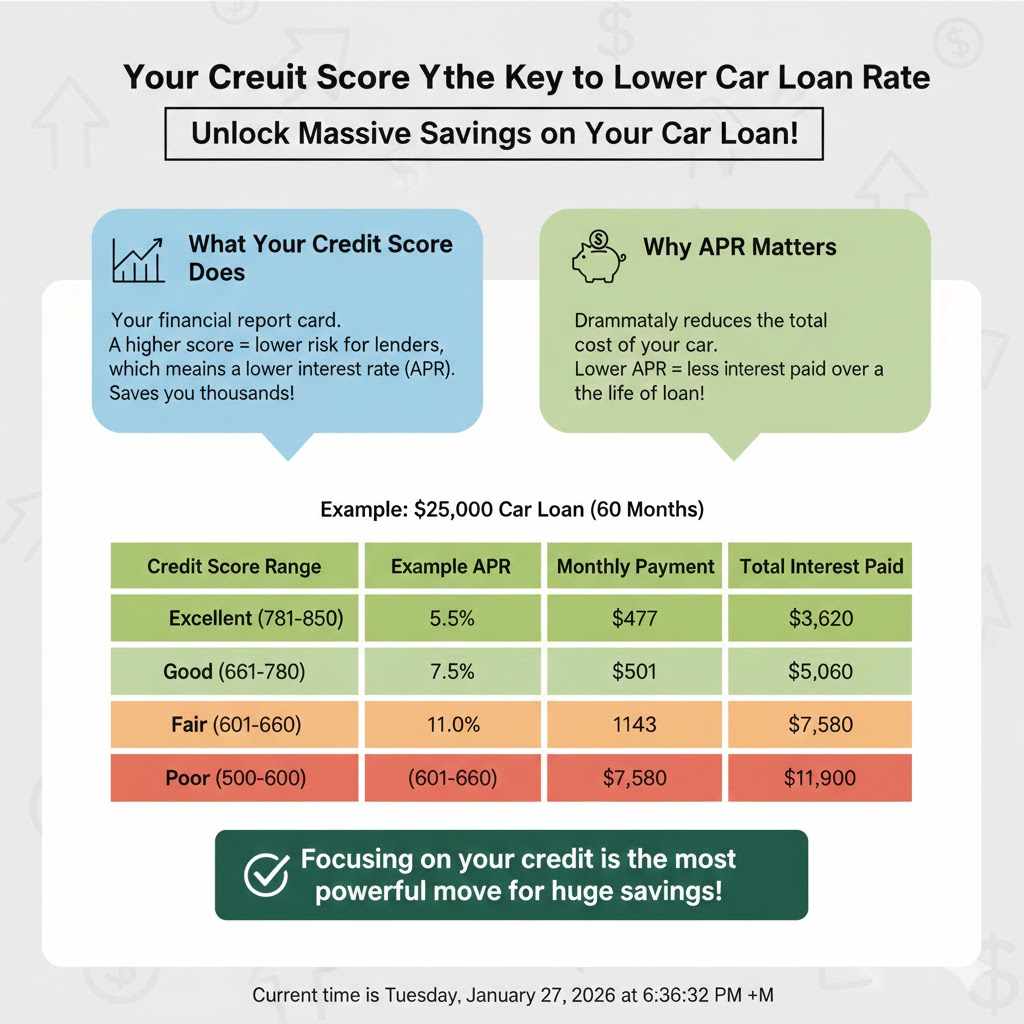

Your Credit Score: The Key to a Lower Car Loan Rate

Think of your credit score as your financial report card. Lenders look at it to decide how risky it is to lend you money. A higher score tells them you are very likely to pay back the loan on time. To reward you for being a reliable borrower, they offer you a lower interest rate, which is also called the Annual Percentage Rate (APR).

A lower APR can save you thousands of dollars over the life of your loan. It doesn’t just lower your monthly payment a little; it dramatically reduces the total amount of money you pay for your car.

Let’s look at an example. Imagine you are borrowing $25,000 for a car on a 60-month (5-year) loan. See how much a good credit score can save you.

| Credit Score Range | Example APR | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| Excellent (781-850) | 5.5% | $477 | $3,620 |

| Good (661-780) | 7.5% | $501 | $5,060 |

| Fair (601-660) | 11.0% | $543 | $7,580 |

| Poor (500-600) | 16.5% | $615 | $11,900 |

Look at the “Total Interest Paid” column. The driver with an excellent credit score pays over $8,000 less in interest than the driver with a poor score for the exact same car! This is why focusing on your credit is the most powerful move you can make.

Proven Smart Moves to Get the Best Rate Now

You don’t have to wait for national rates to drop to get a great deal. You can take action right now to lower the rate you are offered. Here are proven strategies that work.

Move 1: Give Your Credit Score a Quick Boost

Even small improvements to your credit score can unlock better loan offers. You don’t need to wait years to see a change. Here are some things you can do in just a few weeks or months:

- Check Your Credit Report for Free: You are entitled to a free credit report from each of the three major bureaus (Equifax, Experian, and TransUnion) every year. Get yours at AnnualCreditReport.com, the official government-mandated site. Look for errors, like accounts that aren’t yours or incorrect late payments. Disputing and fixing errors can raise your score quickly.

- Pay Down Credit Card Balances: One of the biggest factors in your score is your “credit utilization ratio.” This is the amount of credit you’re using compared to your total credit limit. Try to get your balances below 30% of your limit. For example, if you have a card with a $5,000 limit, aim to have a balance under $1,500. Paying down debt is a powerful way to boost your score.

- Make Every Payment On Time: Your payment history is the single most important factor. If you have any upcoming bills, make sure they are paid on time. Setting up automatic payments can help you avoid any accidental late payments.

Move 2: Get Pre-Approved Before You Step into a Dealership

Walking into a car dealership without a loan already lined up is like going to the grocery store without a wallet. You’re stuck with whatever they offer you. Getting pre-approved for a loan beforehand completely changes the game.

Pre-approval means a lender has reviewed your finances and has told you how much you can borrow and at what interest rate. It’s a firm offer.

Why Pre-Approval is a Smart Move:

- It Gives You Bargaining Power: When you have a pre-approval letter in your hand, you are a “cash buyer” in the eyes of the dealer. You can negotiate the price of the car without getting distracted by financing talk. If the dealership’s financing department offers you a loan, you can compare it to your pre-approval and choose the better deal. You might be surprised when they suddenly find a way to beat your offer!

- It Sets a Clear Budget: Your pre-approval tells you exactly how much car you can afford. This prevents you from falling in love with a vehicle that’s outside your budget and helps you shop with confidence.

- It Saves You Time and Stress: You can apply for pre-approval from the comfort of your home. It’s much less stressful than trying to negotiate a loan under pressure in a dealership finance office.

Don’t just get one pre-approval. Apply to two or three different lenders within a 14-day period. Credit scoring models usually count multiple auto loan inquiries in a short time as a single “hard pull,” minimizing the impact on your credit score. Try these places:

- Your Local Credit Union: Credit unions are non-profits and often offer some of the best interest rates and most customer-friendly terms.

- Your Bank: If you have a good relationship with your bank, they may offer you a competitive rate as a loyal customer.

- Online Lenders: There are many reputable online lenders that specialize in auto loans and can provide quick decisions and great rates.

Move 3: Choose a Shorter Loan Term

It can be tempting to choose a longer loan term, like 72 or even 84 months, because it gives you a lower monthly payment. However, this is usually a costly mistake. Lenders see longer loans as riskier, so they charge a higher interest rate for them. You also end up paying interest for many more years.

A shorter loan term (e.g., 48 or 60 months) almost always comes with a lower APR. While your monthly payment will be higher, you will pay off the car much faster and save a huge amount in total interest.

Let’s look at the same $25,000 loan and see how the term changes the total cost.

| Loan Term | Example APR | Monthly Payment | Total Interest Paid | Total Cost of Car |

|---|---|---|---|---|

| 48 Months (4 years) | 6.0% | $587 | $3,176 | $28,176 |

| 60 Months (5 years) | 6.5% | $489 | $4,340 | $29,340 |

| 72 Months (6 years) | 7.0% | $425 | $5,600 | $30,600 |

By choosing the 48-month loan instead of the 72-month one, you would save $2,424 in interest and own your car free and clear two years sooner. If the monthly payment for a shorter term feels too high, it might be a sign to look for a slightly less expensive car that fits comfortably within your budget.

Move 4: Make a Healthy Down Payment

A down payment is the cash you pay upfront when you buy a car. The more you put down, the less money you have to borrow. Lenders love to see a significant down payment for a few reasons:

- It Lowers Their Risk: When you have your own money invested in the car, you’re less likely to miss payments. This makes you a safer bet, and lenders may reward you with a lower interest rate.

- It Reduces Your Loan Amount: A smaller loan means smaller monthly payments and less total interest paid over time.

- It Protects You from Being “Upside Down”: Cars lose value (depreciate) the moment you drive them off the lot. If you borrow the full amount, you could soon owe more on the loan than the car is actually worth. This is called being “upside down” or having negative equity. A good down payment helps prevent this.

A common recommendation is to put down at least 20% of the car’s purchase price. For a $25,000 car, that would be a $5,000 down payment. If you can’t manage 20%, any amount you can put down will help your financial situation.

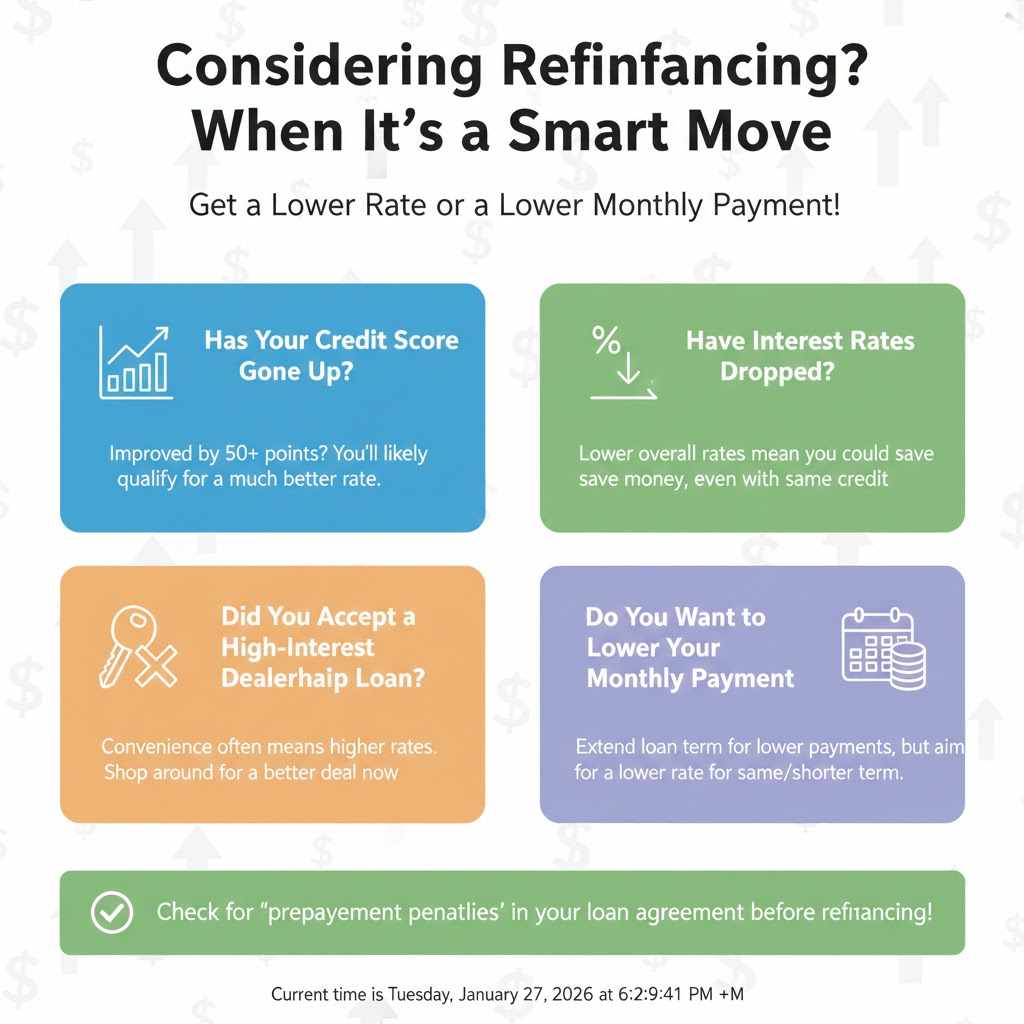

Considering Refinancing? When It’s a Smart Move

What if you already have a car loan with a high interest rate? You aren’t stuck with it. You might be able to refinance, which means replacing your current loan with a new one that has better terms.

Refinancing is a great option if your financial situation has improved since you first got your loan. According to the Consumer Financial Protection Bureau, it’s a way to get a lower interest rate or a lower monthly payment.

Checklist: Is Refinancing Right for You?

- Has your credit score gone up significantly? If you’ve improved your score by 50 points or more, you will likely qualify for a much better rate.

- Have interest rates dropped since you bought your car? Even if your credit is the same, if overall rates are lower now, you could save money.

- Did you accept a high-interest dealership loan? If you took the first loan offered to you at the dealership out of convenience, there’s a very good chance you can find a better rate elsewhere.

- Do you want to lower your monthly payment? Refinancing can sometimes extend your loan term to lower your payments, but be careful. Only do this if you truly need the monthly cash flow, as it could mean paying more interest over time. The best goal is to get a lower rate for the same or a shorter term.

Before you refinance, make sure your current loan doesn’t have a “prepayment penalty,” which is a fee for paying off the loan early. These are less common today but are still worth checking for in your loan agreement.

Frequently Asked Questions (FAQ)

What is a good APR for a car loan?

A “good” APR depends heavily on your credit score and the loan term. For a borrower with excellent credit (780+), anything under 6% is generally considered very good. For someone with average credit, an APR between 7% and 10% might be typical. The goal is to get the lowest rate you possibly can by following the smart moves in this guide.

How long does it take to get approved for a car loan?

It can be very fast! Applying for pre-approval online with a bank, credit union, or online lender can often get you a decision in minutes. The entire process, from application to having the funds ready, can sometimes be completed in the same day.

Can I get a car loan with bad credit?

Yes, it is possible to get a car loan with bad credit, but it will almost certainly come with a very high interest rate. If your credit is poor, it’s highly recommended to spend a few months working to improve your score before you apply. This could save you thousands of dollars. Also, making a larger down payment can increase your chances of approval.

Does checking my car loan rate hurt my credit score?

When you formally apply for a loan, the lender does a “hard inquiry” on your credit, which can cause your score to dip by a few points temporarily. However, credit scoring models like FICO and VantageScore understand that people shop around for the best rates. They will treat all auto loan inquiries made within a short period (usually 14 to 45 days) as a single event, minimizing the impact. This allows you to shop for the best deal without fear.

What’s the difference between a bank and a credit union for a car loan?

Banks are for-profit businesses owned by investors. Credit unions are non-profit financial cooperatives owned by their members (the people who bank there). Because credit unions don’t have to make a profit for shareholders, they often return their earnings to members in the form of lower interest rates on loans and higher rates on savings accounts. It’s always a good idea to check the rates at a local credit union.

When is the best time of year to buy a car?

Dealerships often have sales goals they need to meet, which can work in your favor. The end of the month, the end of the quarter (March, June, September, December), and the end of the year are often great times to negotiate a better price. Holiday sales events, like those around Memorial Day or Labor Day, can also feature special financing offers from manufacturers.

Your Roadmap to a Great Car Loan

So, are car loan rates going down? While we can’t control the national economy, the answer to that question doesn’t have to control your wallet. The most important rate is the one you personally qualify for, and you have a tremendous amount of influence over that number.

By taking charge of your financial health, you can put yourself in the driver’s seat. Remember the proven smart moves: clean up your credit report, pay down your balances, and get pre-approved from multiple lenders before you even think about visiting a dealership. Choose a shorter loan term that you can comfortably afford and make the largest down payment possible. These steps work together to make you the ideal customer in a lender’s eyes.

Don’t let the process intimidate you. You are now equipped with the knowledge to navigate car financing with confidence. By being a prepared and informed buyer, you can secure a great loan, save thousands of dollars, and enjoy your new car knowing you made a truly smart move.