Car Buying Why My Interest Rate Is Not The Same As My Tila Apr Carleton Inc

It’s a common point of confusion for car buyers. You see one number for the interest rate, and then another, often higher, number called the TILA APR. They sound like they should be the same, right?

Yet, they’re not. This difference can feel sneaky. It makes you wonder if you’re getting the best deal.

Let’s break down exactly why these two numbers often don’t match up. We’ll look at what goes into each. This way, you can feel more confident when you sign on the dotted line for your next car.

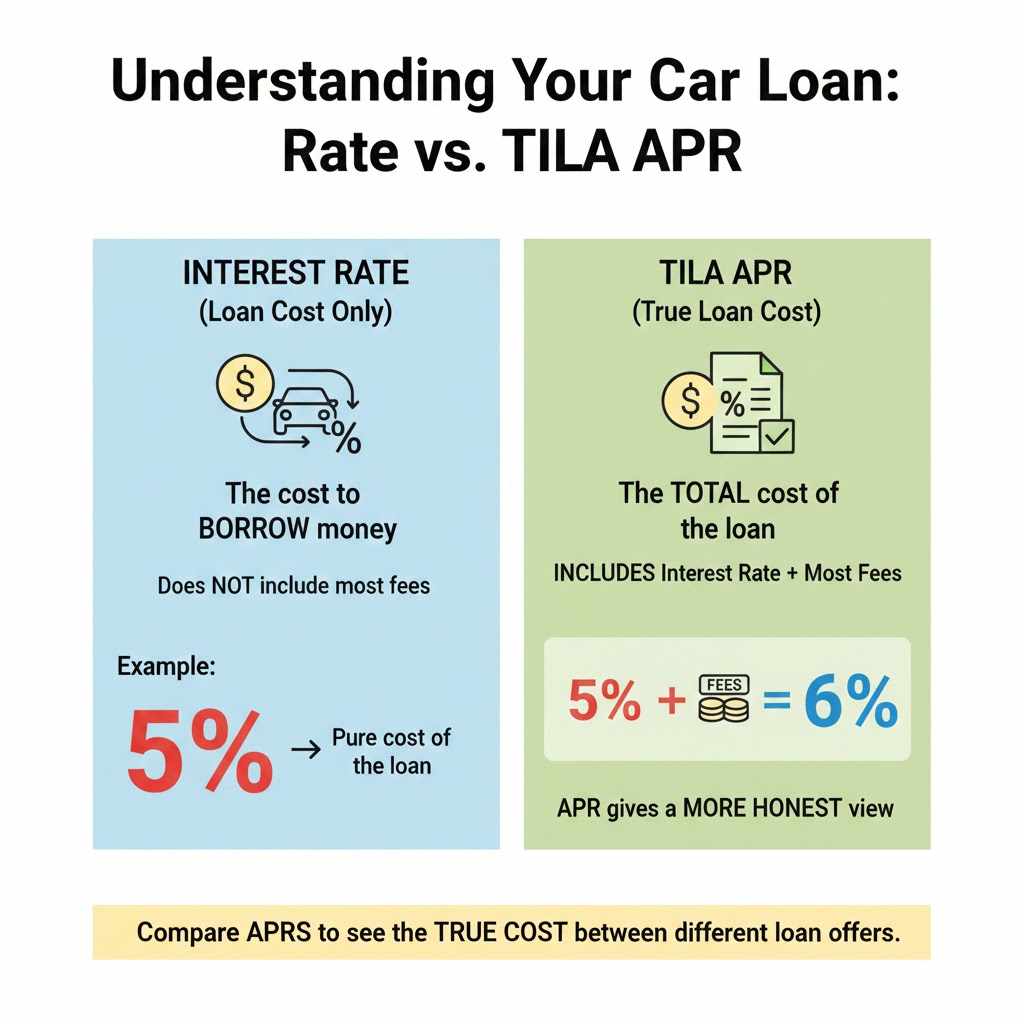

The key difference between your stated interest rate and the TILA APR on a car loan lies in what each number includes. The interest rate is just the cost of borrowing money. The TILA APR, however, is a broader measure. It includes the interest rate plus most of the fees associated with the loan. This gives you a more complete picture of your borrowing cost.

Understanding Your Car Loan Rate vs. TILA APR

When you shop for a car loan, you’ll often hear about two main numbers: the interest rate and the Annual Percentage Rate (APR). They are related but not identical. The interest rate is the percentage the lender charges you for borrowing money.

It’s the pure cost of the money itself. Think of it as the rent you pay for using the bank’s cash.

The TILA APR, on the other hand, is a much more comprehensive figure. TILA stands for the Truth in Lending Act. This law requires lenders to tell you the true cost of your loan.

So, the APR includes the interest rate. But it also adds in most of the fees you have to pay to get the loan. This is important because fees can add up.

They can significantly increase the total amount you pay over the life of the loan.

For example, imagine a loan with a 5% interest rate. If there are also several fees, the APR might be 6% or even higher. This shows you that the APR gives you a more honest view of your actual borrowing expense.

It’s designed to help you compare different loan offers more easily. You can see the true cost of one loan versus another.

Why the Numbers Aren’t Always the Same

The main reason your interest rate and the TILA APR differ is the inclusion of various fees in the APR calculation. Lenders have to disclose these fees under the Truth in Lending Act. They want you to know the full price tag.

Some common fees that get rolled into the APR include:

- Origination fees: These are fees charged for processing your loan application.

- Documentation fees: Fees for preparing the loan paperwork.

- Certain closing costs: Some costs associated with finalizing the loan.

- Discount points: If you choose to pay points to lower your interest rate.

It’s crucial to understand that not all fees are included in the APR. For instance, late payment fees or penalties for defaulting on the loan are generally not part of the APR calculation. These are costs you might incur if you don’t meet your loan obligations.

The APR focuses on the costs you pay upfront or that are standard for getting the loan.

The goal of the APR is to give shoppers a standardized way to compare loans. Without it, comparing offers could be very difficult. You might focus only on the interest rate and miss hidden fees that make one loan much more expensive than another.

The TILA APR helps level the playing field.

My Own Car Buying Frustration

I remember buying my first car after college. I was so proud to get approved for a loan with what I thought was a great interest rate. The salesman kept talking about how low the rate was.

I felt like I was getting a steal. I focused on that number and the monthly payment. I signed the papers without really digging into the details of the other numbers.

A few weeks later, I was reviewing my loan documents. I noticed the APR was a full percentage point higher than the interest rate I was so happy about. Panic set in.

I felt duped. Was I misled? I called the finance manager, feeling a bit embarrassed.

He patiently explained that the APR included fees like the “dealer prep fee” and “documentation charge.” These were standard, he said. They were just part of the loan package.

That experience taught me a valuable lesson. The interest rate is only part of the story. The APR tells the whole financial tale of the loan.

It’s easy to get caught up in the excitement of a new car. But it’s vital to slow down. Understand all the numbers.

Don’t just focus on the headline rate. Always ask questions about the APR and what it includes. It’s your money, and you deserve to know where it’s going.

Key Components of the TILA APR

What’s Included:

- Stated Interest Rate

- Loan Origination Fees

- Processing Fees

- Documentation Fees

- Certain Underwriting Fees

What’s Generally Excluded:

- Late Payment Fees

- Repossession Fees

- Non-Sufficient Funds (NSF) Fees

- Optional Products (like extended warranties, GAP insurance, credit life insurance) – unless they are required to get the loan.

The Role of Fees in Your Loan

Fees are a major reason why the interest rate and APR diverge. Lenders and dealerships often charge various fees. These fees can seem small individually.

But they can add up quickly. Some fees are legitimate costs for processing your loan. Others can be profit generators for the dealership.

Origination fees are a classic example. The lender charges this fee for setting up your loan. It covers their administrative costs.

Documentation fees are similar. They cover the paperwork involved. Dealerships often add their own set of fees.

These might include things like a “dealer service fee” or a “processing fee.” These fees are added to the total amount you finance. This means you end up paying interest on them too.

For instance, if you borrow $20,000 and there’s a $500 origination fee and a $300 documentation fee, that’s $800 in fees. If your interest rate is 5% over 60 months, that $800 in fees will increase your APR. It will also increase your total interest paid.

The APR calculation aims to capture this extra cost.

It’s important to note that some fees are not included in the APR. For example, fees for optional products like GAP insurance, extended warranties, or credit life insurance are typically not part of the APR. These are usually presented as separate add-ons.

However, if the lender requires you to purchase one of these products to get the loan, then its cost might be included in the APR. Always clarify this with your lender.

Dealer Markups and Your Interest Rate

This is where things can get a bit more complex, and sometimes, a little frustrating for buyers. The interest rate you are offered might not be the “base” rate that the bank gave the dealership. Dealerships often work with multiple lenders.

They can negotiate a “buy rate” with a lender.

Then, the dealership can add a “dealer markup” to that buy rate. This markup is essentially the profit the dealership makes on the financing itself. So, the bank might offer the loan at 4.5% to the dealership.

The dealership might then mark it up to 5.5% or even 6.5% for you, the customer. This markup is also factored into the TILA APR calculation.

This is why two people with similar credit scores can get different interest rates for the same car loan. The dealership’s profit margin on financing plays a big role. It’s why it’s so important to get pre-approved for a car loan from your bank or credit union before you even set foot on a car lot.

This gives you a solid benchmark for the interest rate you should be paying. It also helps you negotiate better with the dealership’s finance office.

When you receive a loan offer from a dealership, always ask them to show you the TILA APR. Then, compare it to the interest rate. If the difference is large, it could be due to significant fees or dealer markups.

You can then ask for an itemized breakdown of all fees and the base rate offered by the lender before the dealership added their margin.

Contrast Matrix: Interest Rate vs. TILA APR

Interest Rate

Focus: Cost of borrowing money itself.

Includes: Primarily just the percentage charged on the principal amount.

What it Tells You: How much “rent” you pay for the cash.

Limitation: Doesn’t show total loan cost with fees.

TILA APR

Focus: True annual cost of the loan.

Includes: Interest rate PLUS most fees (origination, documentation, etc.).

What it Tells You: The total expense of getting and repaying the loan.

Benefit: Better for comparing different loan offers.

When is a Large Difference Normal?

A small difference between the interest rate and the TILA APR is usually normal. This is because most car loans come with some standard fees. For example, a documentation fee of a few hundred dollars is common.

This will nudge the APR up a bit from the interest rate.

However, a significant gap can be a red flag. If your interest rate is 5%, but the TILA APR is 8% or higher, you should investigate. This large difference could be due to:

- High origination or administrative fees.

- Substantial dealer markups on the interest rate.

- The inclusion of optional products that you might not need.

In some states, certain fees are capped. For instance, there are limits on how much a dealership can charge for documentation fees. Also, some lenders might offer lower interest rates but charge higher fees.

The APR calculation accounts for this trade-off.

It’s also worth noting that some car loans might be structured with very low or even zero interest rates. In such cases, the APR might appear much higher. This is because the cost of the loan is being recovered through higher prices for the car itself or through significant fees.

Always look at the total price of the car and the total amount financed. This gives you a clearer picture.

Understanding Optional Products

Dealership finance departments often try to sell you additional products. These are sometimes called “add-ons” or “F&I products” (Finance & Insurance). These products are usually optional.

They are not required to get the loan itself. Examples include:

- Extended Warranties: Cover repairs after the manufacturer’s warranty expires.

- GAP Insurance: Covers the difference between what you owe on the loan and what your car is worth if it’s totaled.

- Tire and Wheel Protection: Covers damage to tires and wheels.

- Paint Protection and Fabric Protection: Treatments to preserve the car’s finish and interior.

- Key Replacement: Covers the cost of replacing lost keys.

- Credit Life Insurance: Pays off your loan if you die.

- Job Loss Insurance: Can defer payments if you lose your job.

Generally, the cost of these optional products is NOT included in the TILA APR. This is because you have the choice to buy them or not. They are not a mandatory part of obtaining the loan.

However, if a lender forces you to buy one of these products to get approved for the loan, then its cost should be included in the APR.

This is a crucial point. Sometimes, salespeople can be vague. They might bundle the cost of these products into the loan amount.

Then, they might not clearly state whether they are required or optional. If you are unsure, ask directly. “Is this product required for me to get this loan?” If the answer is no, you can choose to decline it.

Declining these products can lower your total loan amount and, consequently, your APR.

Quick-Scan Table: When Fees Impact APR

| Fee Type | Included in APR? | Reason |

|---|---|---|

| Loan Origination Fee | Yes | Direct cost of setting up the loan. |

| Documentation Fee | Yes | Cost of preparing loan paperwork. |

| Dealer Markup on Rate | Yes | Increases the lender’s profit margin. |

| Late Payment Fee | No | Penalty for missing payments, not a cost to get the loan. |

| Optional Extended Warranty | No (Usually) | Customer choice, not required for the loan. |

| Required Credit Life Insurance | Yes (If mandatory) | Cost imposed by lender to secure the loan. |

How Lenders Calculate the APR

The calculation of the TILA APR is actually quite complex. It’s not a simple formula you can easily do with a basic calculator. Lenders use specific financial formulas and software to determine the accurate APR.

The goal is to find the single annual interest rate that, when applied to the loan amount and accounting for all fees and the loan term, results in the total amount of interest paid.

Here’s a simplified idea of what happens:

- Total Loan Amount: This is the price of the car minus your down payment and trade-in value.

- Add Fees: Most of the fees you pay to get the loan are added to this amount. This increases the principal you are borrowing.

- Calculate Total Interest Paid: This is based on the loan term (how long you have to repay) and the stated interest rate.

- Total Repayment Amount: This is the principal amount plus the total interest.

- Find the APR: The APR is the annual rate that makes the present value of all the loan payments equal to the total amount financed (including fees).

Because this calculation is so precise and involves specific financial mathematics, it’s best to rely on the lender’s disclosure statement. The Truth in Lending Act mandates that lenders provide you with an official Loan Estimate or Closing Disclosure. This document clearly states the APR.

It also lists the fees that were used to calculate it.

If you are ever curious about how a specific fee impacts your APR, you can use online APR calculators. You can plug in your loan details and manually add or remove fees to see the effect. However, for official loan documents, the lender’s disclosed APR is the legally recognized figure.

When to Worry and When Not To

It’s normal for the TILA APR to be slightly higher than the stated interest rate. This is due to the inclusion of standard loan fees. Don’t panic if you see a small difference.

A difference of 0.25% to 0.5% is often just the result of common processing and documentation fees.

You should start to pay closer attention and ask more questions if the gap is substantial. If the APR is more than 1% or 2% higher than the interest rate, it warrants further investigation. This could indicate:

- Excessive dealer markups.

- Very high origination or administrative fees.

- The inclusion of optional products that you didn’t fully understand were required.

What to check:

- Ask for an itemized list of all fees. Make sure you understand what each fee is for.

- Inquire about the “buy rate” vs. your offered rate. Understand if the dealership added a markup.

- Review any optional products you agreed to. Were they truly necessary for the loan?

- Compare offers from multiple lenders. This helps you see if the fees and APR are competitive.

If you feel pressured or can’t get clear answers about the fees and the APR, it might be a sign to walk away. There are always other dealerships and other lenders. Your goal is to find a loan where the TILA APR accurately reflects the true cost of borrowing, and where you feel you are being treated fairly.

Tips for Car Buying Negotiation

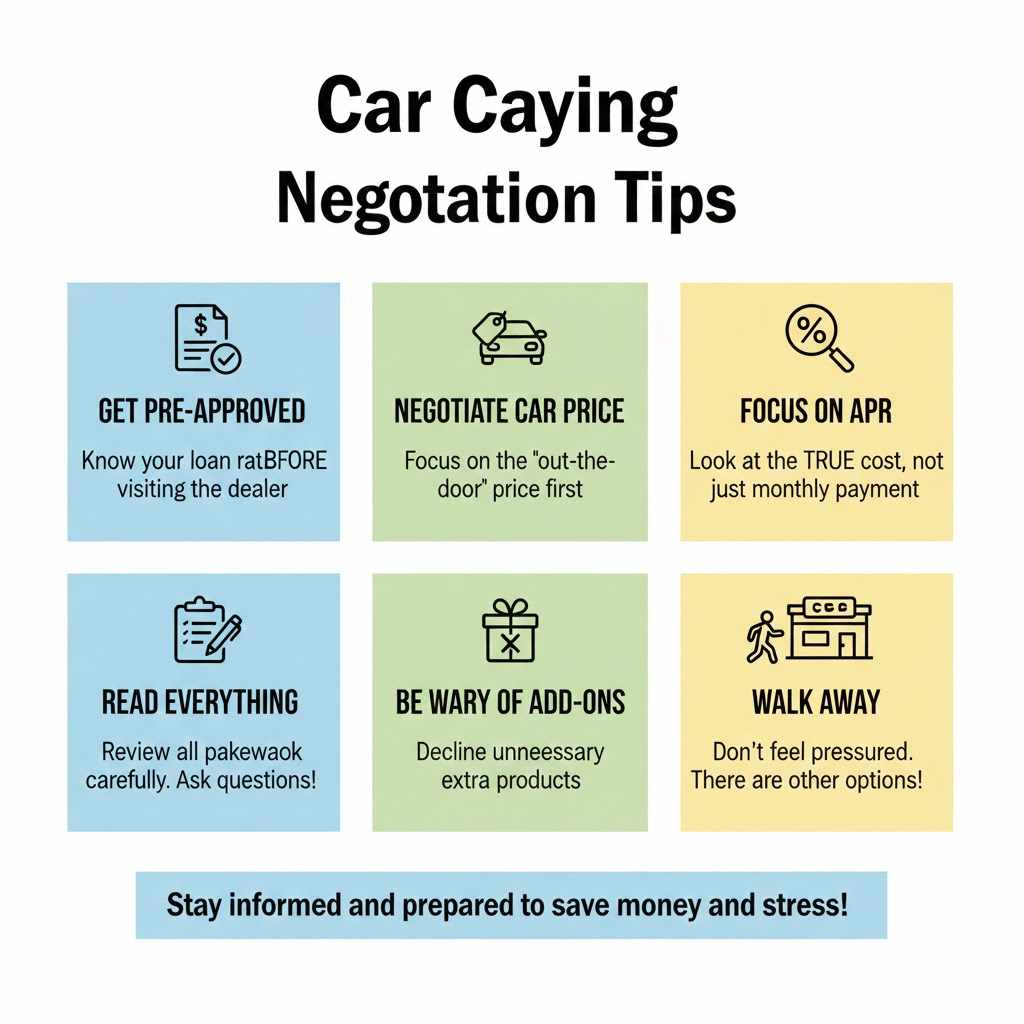

When you’re in the process of buying a car, your focus should be on a few key areas. Understanding the difference between interest rate and APR is one of them. Here are some tips to help you navigate the negotiation process:

- Get Pre-Approved First: Before visiting a dealership, get loan pre-approval from your bank or credit union. This gives you a clear understanding of what interest rate you qualify for. It also strengthens your negotiating position. You can compare the dealership’s offer to your pre-approval.

- Negotiate the Car Price First: Focus on the total “out-the-door” price of the car before discussing financing. This prevents dealerships from inflating the car price to compensate for a lower interest rate or to hide fees.

- Focus on the APR, Not Just the Monthly Payment: A low monthly payment can be achieved by extending the loan term. This means you’ll pay more interest over time. Always look at the APR to understand the true cost of borrowing.

- Read Everything Carefully: Don’t rush through the paperwork. Read every line item. Ask questions about anything you don’t understand. Make sure the numbers on the final contract match what you agreed upon.

- Be Wary of “Add-Ons”: Understand the purpose and cost of any optional products being offered. If you don’t need them, politely decline.

- Know Your State’s Laws: Some states have regulations on dealer fees. Familiarize yourself with any rules that might apply to your situation.

- Walk Away if Necessary: If you feel pressured, confused, or uncomfortable with the deal, it’s always okay to walk away. There are other cars and other lenders.

By staying informed and prepared, you can avoid common pitfalls. You can ensure you get a fair deal on your car loan. Remember, the TILA APR is your most accurate guide to the total cost of borrowing.

Frequently Asked Questions

What is the main difference between interest rate and APR?

The interest rate is the cost of borrowing money itself. The APR (Annual Percentage Rate) includes the interest rate plus most of the fees associated with getting the loan. The APR shows the true, overall cost of borrowing.

Why would a dealership add fees to my loan?

Dealerships add fees for several reasons. Some cover legitimate administrative costs, like processing and documentation. Others are part of their profit margin, such as dealer markups on the interest rate, or the sale of optional products.

Are all fees included in the TILA APR calculation?

No, not all fees are included. Generally, fees that are mandatory to get the loan are included. Fees for optional products, or penalties for late payments, are typically excluded.

Can I negotiate the fees on my car loan?

Yes, you can often negotiate fees, especially documentation fees and dealer markups. It’s best to discuss the car’s price and financing separately. Having pre-approval from your bank gives you leverage to negotiate better terms.

What happens if I see a large difference between my interest rate and the APR?

A large difference (more than 1-2%) suggests that the loan has significant fees or dealer markups. You should ask for a detailed breakdown of all fees and the lender’s base rate. It might be an opportunity to negotiate further or seek financing elsewhere.

Should I always focus on the APR over the interest rate?

Yes, when comparing loan offers, the APR is a more accurate tool. It gives you a clearer picture of the total cost of the loan. While the interest rate is important, the APR reflects the real expense after all mandatory fees are considered.

Conclusion

Understanding the difference between your car loan’s interest rate and its TILA APR is key to smart car buying. The APR provides a more honest look at your borrowing costs. It includes the interest plus most fees.

Don’t just focus on the advertised interest rate. Always examine the APR. It helps you compare loans fairly.

Knowing this can save you money and prevent unwelcome surprises down the road.