How Do Car Loan Interest Work: A Simple Guide to Save Money

Understanding how car loan interest works can save you money. Let’s break it down simply.

When you take out a car loan, you borrow money from a lender. This lender charges you interest for using their money. The interest rate can vary based on your credit score, loan term, and lender policies. Knowing how these factors impact your loan can help you make better financial decisions.

In this blog, we will explain the basics of car loan interest. We’ll cover how interest rates are determined, how they affect your monthly payments, and tips to get the best rates. By the end, you’ll understand how to navigate car loans confidently. Let’s dive in!

Credit: www.youtube.com

Introduction To Car Loans

Car loans help people buy cars. You borrow money from a bank. Then, you pay it back over time. The bank charges you for borrowing money. This charge is called interest. Interest makes the total cost higher.

Understanding interest rates is crucial. Higher rates mean you pay more. Lower rates save you money. Always check the rate before agreeing. Compare different offers. Save money by choosing the best rate.

Credit: mytresl.com

Types Of Car Loan Interest Rates

Fixed interest rates stay the same. They do not change over time. This means your monthly payment will always be the same. Many people like this because it is predictable. You can plan your budget easily.

Variable interest rates can change. They go up and down with the market. Your monthly payment can be different each time. Sometimes it is lower. Other times it is higher. This type of rate can be risky. But it can also save you money.

How Interest Rates Are Determined

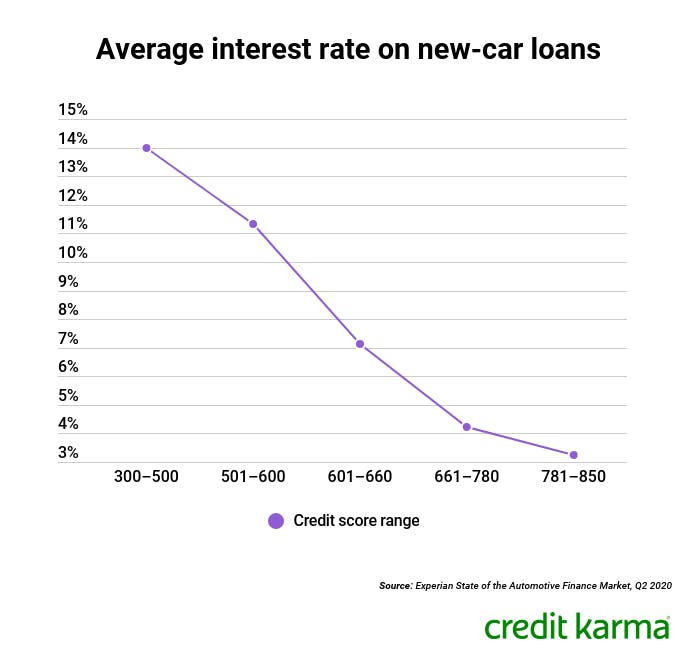

Your credit score plays a big role in interest rates. A high score means lower rates. A low score means higher rates. Lenders see a high score as low risk. They see a low score as high risk. Paying bills on time helps your score. Missing payments hurts your score. Always check your score before applying.

The loan term also affects interest rates. Short terms have higher monthly payments but lower rates. Long terms have lower monthly payments but higher rates. A short term means you pay off the loan faster. A long term means you pay more interest over time. Choose the term that fits your budget. Always consider the total interest paid.

Calculating Car Loan Interest

Simple interest is easy to calculate. Use the formula: Principal x Rate x Time. First, find out how much you borrowed. This is the principal. Next, know the interest rate. Then, decide the loan period in years. Multiply these three values. The result is the total interest. Divide it by the number of months. Now, you know the monthly interest.

Compound interest is a bit harder. Interest is added to the principal. Use the formula: Principal x (1 + Rate/number of times compounded)^(number of times compounded x Time). First, find the principal and rate. Next, determine how often interest is added. This can be yearly, monthly, or daily. Apply the formula. The answer gives you the future value. Subtract the principal to get the interest.

Ways To Lower Your Car Loan Interest

A higher credit score means lower interest rates. Pay bills on time. Reduce existing debt. Check your credit report. Fix any errors. Keep old accounts open. Use credit cards wisely.

A bigger down payment reduces loan amount. Lenders see less risk. This can lower your interest rate. Save more before buying. Trade in an old car. Ask for family help. Aim for at least 20% down.

Refinancing Your Car Loan

Refinancing can be a good idea if interest rates drop. A lower rate means lower monthly payments. Improved credit scores might also make refinancing beneficial. If your credit score is better now, you may get better terms. Refinancing is helpful if you need to change loan terms. Maybe you want to extend the loan period. This can reduce monthly payments too. But be aware, this means you’ll pay more in interest over time.

First, check your credit score. Better credit can get you lower rates. Then, gather your financial documents. This includes your current loan details. Shop around for the best offers. Compare rates from different lenders. Apply with the lender that offers the best terms. Once approved, review the new loan terms carefully. Make sure there are no hidden fees. If everything looks good, sign the new loan agreement. Finally, pay off the old loan with the new loan funds.

Common Mistakes To Avoid

Many people make a big mistake by ignoring loan terms. They only focus on the monthly payment. This can lead to higher costs in the long run. Always read the terms carefully. Check the interest rate, loan period, and total cost. A low monthly payment might mean a longer loan. This means you will pay more interest over time.

Another mistake is overlooking additional fees. These include processing fees, late payment charges, and early repayment penalties. These fees can add up. They can make your loan more expensive. Always ask about all fees before signing. Make sure you understand all costs involved.

Tips For Saving Money On Car Loans

Check offers from different banks. Compare interest rates. Look at loan terms and fees. Choose the lowest rate. Check for prepayment fees. These can add extra costs. Use online tools to compare. This makes it easier.

Ask lenders for lower rates. Show offers from other banks. This can help in negotiations. Ask about any hidden fees. Know all costs upfront. Try to shorten loan term. This can save money on interest. Make a larger down payment. This reduces loan amount and interest.

Credit: www.creditkarma.com

Frequently Asked Questions

What Is A Car Loan Interest Rate?

A car loan interest rate is the percentage charged by the lender on the borrowed amount. It determines the cost of the loan over time.

How Is Car Loan Interest Calculated?

Car loan interest is typically calculated using simple interest. The formula involves multiplying the principal amount, the interest rate, and the loan term.

Can I Reduce My Car Loan Interest Rate?

Yes, you can reduce your car loan interest rate by improving your credit score, making a larger down payment, or shopping around for better rates.

Does Loan Term Affect Car Loan Interest?

Yes, the loan term affects car loan interest. Longer terms usually result in more interest paid over the life of the loan.

Conclusion

Understanding car loan interest helps you make informed decisions. Lower interest rates save money. Always compare offers from different lenders. Consider loan terms and monthly payments. A good credit score can secure better rates. Budget wisely to avoid financial stress.

With this knowledge, you can navigate car loans confidently. Happy car shopping!