How Much Will Car Insurance Go Up After a Claim? Uncover Costs!

How Much Will Car Insurance Go Up After a Claim

Car insurance is a necessary expense for drivers, providing financial protection in the event of an accident or damage to their vehicle. However, many people are concerned about how much their car insurance premiums will increase after filing a claim. In this article, we will explore the factors that influence the increase in car insurance rates after a claim and provide some tips on how to minimize the impact on your premiums.

Factors that Determine the Increase in Car Insurance Rates After a Claim

1. At-Fault vs. Not-At-Fault Claims: One of the most significant factors that determine the increase in car insurance rates after a claim is whether the claim is deemed at-fault or not-at-fault. If you are found at-fault for an accident, your insurance rates are more likely to increase compared to a not-at-fault claim. Insurance companies consider at-fault accidents as an indication of higher risk, resulting in higher premiums.

2. Severity of the Claim: The severity of the claim also plays a role in determining the increase in car insurance rates. If the claim involves significant damage to your vehicle or other vehicles involved, the insurance company may consider you a higher risk and adjust your premiums accordingly. On the other hand, minor claims may have a smaller impact on your rates.

3. Previous Claims History: Insurance companies also take into account your claims history when determining the increase in car insurance rates. If you have a history of multiple claims, regardless of fault, your rates are more likely to increase compared to someone with a clean claims history. Insurance companies view multiple claims as a higher risk and adjust premiums accordingly.

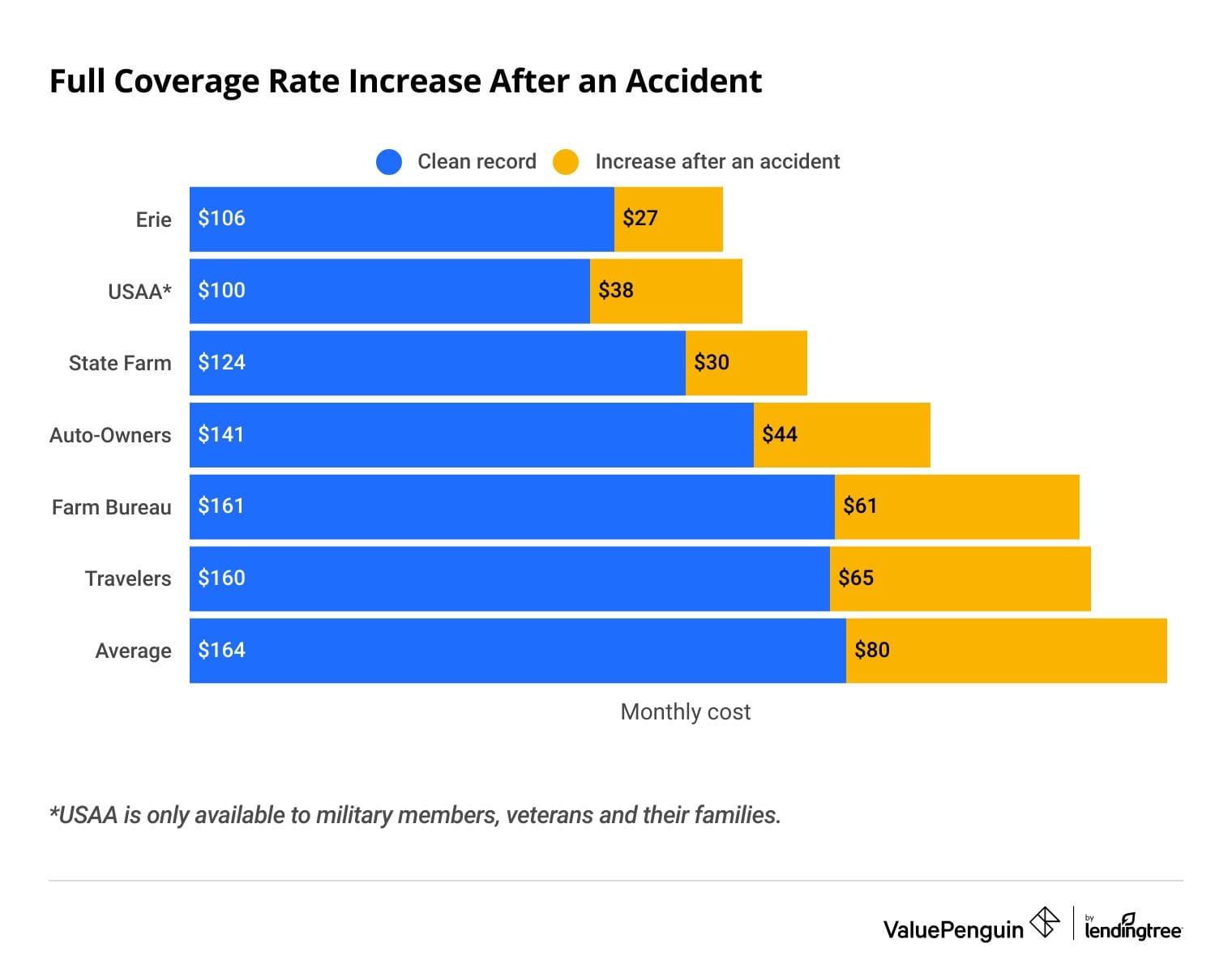

4. Insurance Provider: Different insurance providers have different policies and guidelines when it comes to rate increases after a claim. Some insurance companies may have stricter policies and increase rates more substantially compared to others. It’s essential to review your insurance provider’s policies regarding rate increases after a claim to understand how it may affect your premiums.

Tips to Minimize the Increase in Car Insurance Rates After a Claim

While it’s challenging to avoid an increase in car insurance rates after filing a claim, there are a few strategies you can employ to minimize the impact on your premiums:

1. Consider Your Deductible: Increasing your deductible can help offset the potential increase in premiums after a claim. By opting for a higher deductible, you are taking on more financial responsibility in the event of an accident, but it can result in lower premiums overall.

2. Safe Driving Discounts: Some insurance providers offer safe driving discounts or accident forgiveness programs. These programs reward drivers for maintaining a clean driving record and can help mitigate the increase in rates after a claim.

3. Shop Around for Insurance: It’s always a good idea to shop around for car insurance coverage, especially after filing a claim. Different insurance providers have varying policies when it comes to rate increases, so comparing quotes from multiple companies can help you find the best rates.

4. Consider a Telematics Device: Some insurance providers offer telematics devices that monitor your driving behavior. By installing these devices in your vehicle, you can demonstrate safe driving habits, which may result in lower premiums, even after filing a claim.

5. Defensive Driving Courses: Completing a defensive driving course can demonstrate to your insurance provider that you are committed to safe driving practices. Some insurance companies offer discounts for drivers who have completed these courses, which can help offset the increase in rates after a claim.

Conclusion

Filing a claim can result in an increase in car insurance rates, but the extent of the increase depends on various factors such as fault, severity of the claim, claims history, and the insurance provider’s policies. While it’s challenging to avoid an increase in rates entirely, implementing strategies like increasing your deductible, shopping around for insurance, and maintaining a clean driving record can help minimize the impact on your premiums. It’s essential to review your insurance policy and discuss any potential rate increases with your insurance provider to fully understand how your premiums may be affected after filing a claim.