USAA Auto Loans Rebuilt Titles Guide

Getting a car loan when the vehicle has a rebuilt title can feel a little tricky, especially if this is your first time. Many lenders find these kinds of cars harder to finance. But don’t worry!

We’re here to make it simple. This guide will walk you through everything you need to know about USAA Auto Loans for Vehicles With Rebuilt Titles. We’ll break down the process step-by-step so you can get behind the wheel with confidence.

Let’s find out what USAA can do for you.

Understanding Rebuilt Titles

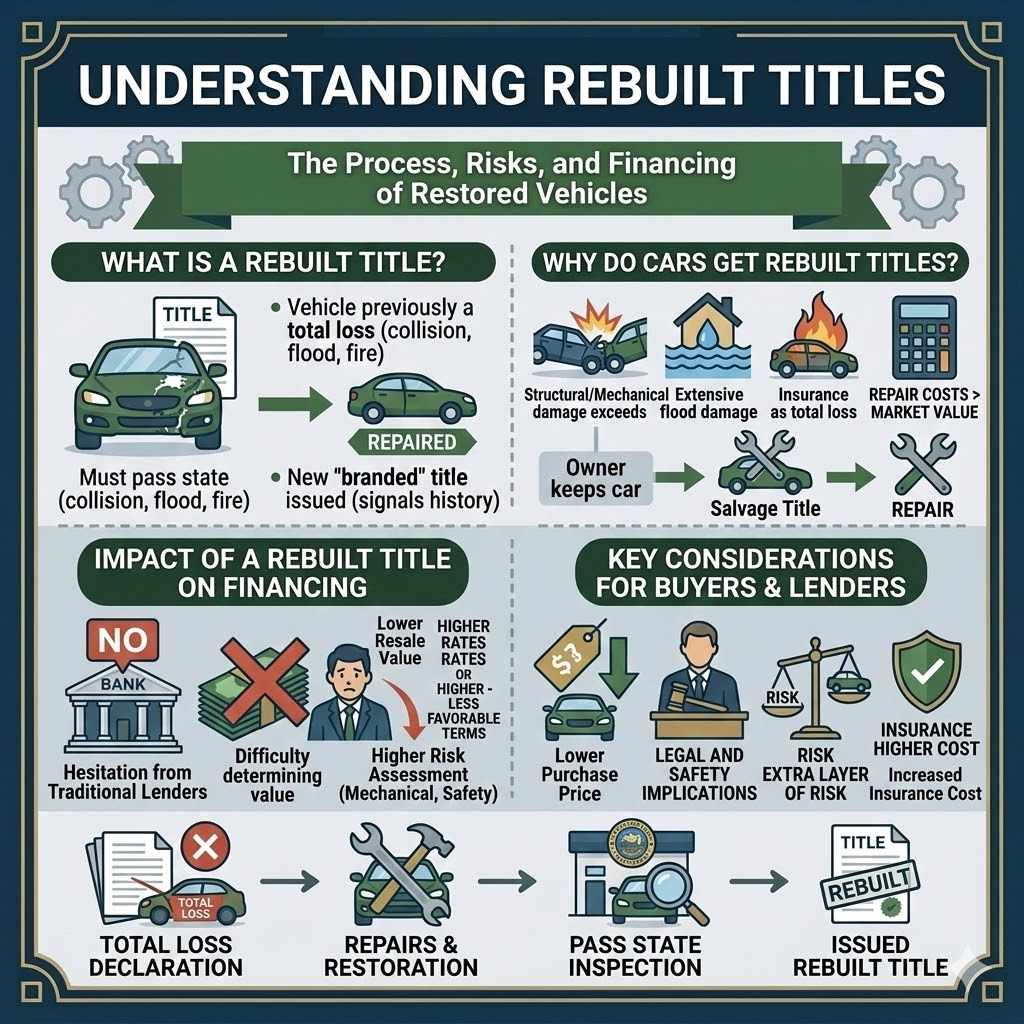

A rebuilt title means a vehicle was previously declared a total loss by an insurance company. This usually happens after it was damaged in an accident, flood, or fire. After repairs, it needs to pass a state inspection to be legally driven again.

This process often results in a new title being issued, but it’s marked as “rebuilt” or “salvage-rebuilt.” This designation signals to lenders and buyers that the car has a history of significant damage.

For car buyers, a rebuilt title can mean a lower purchase price. For lenders, it means a higher risk. The car’s past damage might affect its long-term reliability or safety.

Insurance companies also tend to charge more for vehicles with rebuilt titles. Because of these factors, finding financing can be more challenging.

What is a Rebuilt Title?

A rebuilt title is a legal designation for a vehicle that has sustained damage severe enough for an insurance company to consider it a total loss. This often happens after a major collision, extensive flood damage, or a fire. However, the vehicle can be repaired and restored to a drivable condition.

Once repaired, it must undergo a rigorous inspection process by the state’s Department of Motor Vehicles (DMV) or a similar agency.

If the vehicle passes this inspection, it is issued a new title. This new title will clearly state that it is a “rebuilt,” “salvage-rebuilt,” or similarly branded title. This branding is crucial because it alerts future buyers and lenders to the vehicle’s history.

It’s a way of saying the car has a past that involved serious damage.

Why Do Cars Get Rebuilt Titles?

Cars get rebuilt titles for a few main reasons. The most common is a major accident that causes structural damage. If the cost to repair the car exceeds a certain percentage of its market value, the insurance company may declare it a total loss.

Flood damage is another frequent cause. Water can damage the electrical system and other critical components, making repairs very expensive.

Fire damage can also lead to a total loss designation. Even if the visible damage seems minor, fire can compromise materials and systems in ways that are not immediately apparent. In these situations, the insurance company pays out the value of the car to the owner.

The owner then has the option to keep the car and receive a reduced payout (resulting in a salvage title initially) or let the insurance company take possession. If the owner keeps the car and repairs it, it can eventually be retitled as rebuilt after inspection.

The Impact of a Rebuilt Title on Financing

A rebuilt title significantly impacts a vehicle’s financing options. Many traditional lenders are hesitant to offer loans for cars with this type of title. This is because the vehicle’s value is harder to determine accurately.

The risk of future mechanical issues is also higher. Insurance coverage can also be more difficult to obtain or more expensive.

When a vehicle has a rebuilt title, its resale value is typically lower than a comparable car with a clean title. Lenders assess risk based on the car’s value and the borrower’s creditworthiness. A rebuilt title introduces an extra layer of risk for the lender.

This often means that even if financing is approved, the interest rates might be higher, or the loan terms less favorable.

USAA Auto Loans for Vehicles With Rebuilt Titles

Finding a lender that offers auto loans for vehicles with rebuilt titles can be tough. Many people assume their options are very limited. USAA, known for serving military members and their families, often provides more flexible solutions.

They understand that their members may be looking for affordable transportation options. This can include vehicles that have been repaired after previous damage.

Securing a loan for a rebuilt title vehicle with USAA involves a similar process to standard auto loans, but with a few extra checks. USAA will likely require a thorough inspection report. They may also want documentation proving the repairs were done correctly.

This ensures they are lending against a safe and roadworthy vehicle.

USAA’s Approach to Rebuilt Title Loans

USAA is generally considered more accommodating to members with unique situations. This can include offering auto loans for vehicles with rebuilt titles. They aim to help their members find reliable transportation.

Their focus on member service means they often look for ways to say “yes” when other lenders might say “no.”

When applying for a loan with USAA for a rebuilt title vehicle, be prepared to provide additional documentation. This might include a detailed repair history, receipts for parts and labor, and a report from a mechanic confirming the vehicle’s roadworthiness. USAA wants to ensure that the vehicle is safe and that its value, while potentially lower than a clean-title car, still supports the loan amount.

The Application Process with USAA

The application process for a USAA auto loan for a rebuilt title vehicle generally mirrors that of a standard auto loan, with a few key differences. You’ll start by gathering your personal financial information, including your income, employment history, and credit score. USAA will review your creditworthiness to determine your eligibility and the terms of the loan.

For rebuilt title vehicles, USAA will also require specific documentation about the car. This typically includes the vehicle’s history report (like CarFax or AutoCheck) which shows the rebuilt title status. You may also need to provide proof of repairs and a recent inspection certificate.

This extra information helps USAA assess the risk associated with the loan.

What to Expect During Approval

If your application for a USAA auto loan for a rebuilt title vehicle is approved, you’ll receive loan terms. These will include the interest rate, repayment period, and monthly payment amount. It’s important to understand that interest rates for rebuilt titles might be slightly higher than for vehicles with clean titles.

This is due to the increased risk for the lender.

USAA will also outline any specific requirements for the loan. This could include stipulations about the vehicle’s condition or the need for comprehensive insurance. Once you accept the terms, you’ll proceed to finalizing the loan agreement and purchasing the vehicle.

USAA’s goal is to ensure both you and the collateral (the car) are in a good position.

Steps to Secure Your USAA Loan for a Rebuilt Title Car

Getting a loan for a car with a rebuilt title from USAA involves a few specific steps. It’s important to be organized and have all your information ready. This will make the process smoother.

By following these steps, you can increase your chances of getting approved.

1. Check Your Eligibility and Credit Score

Before you even start looking at cars or applying for a loan, it’s wise to check your credit score. USAA, like most lenders, uses your credit score to assess your financial reliability. A higher credit score generally means better loan terms, including a lower interest rate.

If your score is lower, USAA might still approve you, but the terms could be less favorable.

You can get free copies of your credit report from the three major credit bureaus (Equifax, Experian, and TransUnion) once a year. Review these reports for any errors that might be dragging down your score. Addressing any inaccuracies can improve your credit standing.

Also, ensure you meet USAA’s general membership eligibility requirements.

2. Find a Suitable Vehicle

When looking for a car with a rebuilt title, it’s crucial to be thorough. Don’t just rely on the seller’s description. Always get a pre-purchase inspection from an independent, trusted mechanic.

Ask them to specifically check for any signs of past damage that might have been poorly repaired. They can identify structural issues, frame damage, or electrical problems that a typical buyer might miss.

Also, run a vehicle history report (e.g., CarFax, AutoCheck). This report will confirm the rebuilt title status and often details the nature of the damage the car sustained. Look for any inconsistencies or red flags.

Understanding the car’s history and condition is vital for both your safety and for USAA’s loan approval process.

3. Gather Necessary Documentation

To apply for a USAA auto loan for a rebuilt title vehicle, you’ll need to prepare specific documents. This includes standard personal financial documents like proof of income (pay stubs, tax returns), identification, and proof of residency. You’ll also need the vehicle’s specific paperwork.

For a rebuilt title car, this means having the vehicle’s history report, the rebuilt title itself, and any receipts or documentation related to its repairs. A detailed report from your mechanic confirming the vehicle’s safety and roadworthiness is highly recommended. The more thorough you are with documentation, the easier it will be for USAA to process your application.

4. Apply for the Loan Through USAA

Once you have your finances in order and have identified a suitable vehicle, you can apply for the USAA auto loan. You can typically start the application process online through USAA’s website. Fill out all the required sections accurately and completely.

Be sure to indicate that the vehicle has a rebuilt title.

USAA may ask for details about the seller and the vehicle beyond what’s on the history report. They will review your application, your credit history, and the provided documentation about the car. This is where all the preparation you’ve done will pay off.

USAA’s underwriters will assess the risk and make a decision.

5. Review and Accept the Loan Offer

If USAA approves your loan application, they will present you with a loan offer. This offer will detail the loan amount, interest rate, repayment term, and monthly payments. Carefully review all the terms and conditions.

Make sure you understand everything, especially any specific requirements related to the rebuilt title.

Compare the offer to any other financing options you might have, although finding other lenders for rebuilt titles can be difficult. If you’re satisfied with the USAA offer, you can accept it. This will lead to the final steps of signing the loan documents and arranging for the purchase of the vehicle.

Tips for Buying a Rebuilt Title Vehicle with USAA

Buying a car with a rebuilt title can be a smart financial move if done correctly. These vehicles often cost less than comparable cars with clean titles. This can save you a significant amount of money.

However, it’s essential to approach the purchase with caution and diligence.

USAA can be a valuable partner in this process. Their willingness to consider loans for rebuilt titles sets them apart. By following best practices, you can make sure you get a safe and reliable car at a good price, financed through a lender that supports your needs.

Be Prepared for Extra Scrutiny

When you tell USAA you’re looking to finance a vehicle with a rebuilt title, expect them to look closely. They need to be sure that the repairs were done correctly and that the car is safe to drive. This means you’ll likely need more paperwork than for a standard car loan.

This includes detailed repair invoices, mechanic inspection reports, and potentially photos or videos of the repairs. USAA’s goal is to mitigate their risk. By showing them you’ve been diligent and that the car is sound, you help them feel more comfortable approving your loan.

Get a Thorough Pre-Purchase Inspection

This step cannot be stressed enough. For any used car, a pre-purchase inspection (PPI) is vital. For a rebuilt title car, it’s absolutely essential.

Take the car to an independent mechanic you trust. Ask them to check every system, especially the frame, suspension, and electrical components.

A good mechanic can spot signs of poor repairs or underlying issues that could become costly problems later. This inspection is not just for your peace of mind; it can also be a critical piece of evidence when you apply for the loan. If the mechanic finds serious issues, it might be best to walk away from that particular vehicle.

Understand Insurance Requirements

Insuring a vehicle with a rebuilt title can sometimes be more challenging or expensive than insuring a car with a clean title. Many standard auto insurance policies might have limitations when it comes to covering rebuilt title vehicles. USAA is a major insurance provider, so they can likely help you with this.

When you discuss your loan with USAA, also inquire about their auto insurance options for vehicles with rebuilt titles. They can explain what coverage is available, what the premiums might be, and if there are any specific requirements they have for insuring these vehicles. This ensures you’re fully covered and compliant with your loan agreement.

Consider the Resale Value

Vehicles with rebuilt titles generally have a lower resale value compared to those with clean titles. This is an important factor to consider when you’re buying. While you might get a good deal upfront, you should be aware that you may not get as much back when you decide to sell it in the future.

This is one of the trade-offs for potentially paying less for the car initially. When you take out a loan, the loan amount should reflect the car’s current market value, even with the rebuilt title. USAA will likely factor this into their loan approval process.

Alternatives to USAA Auto Loans for Rebuilt Titles

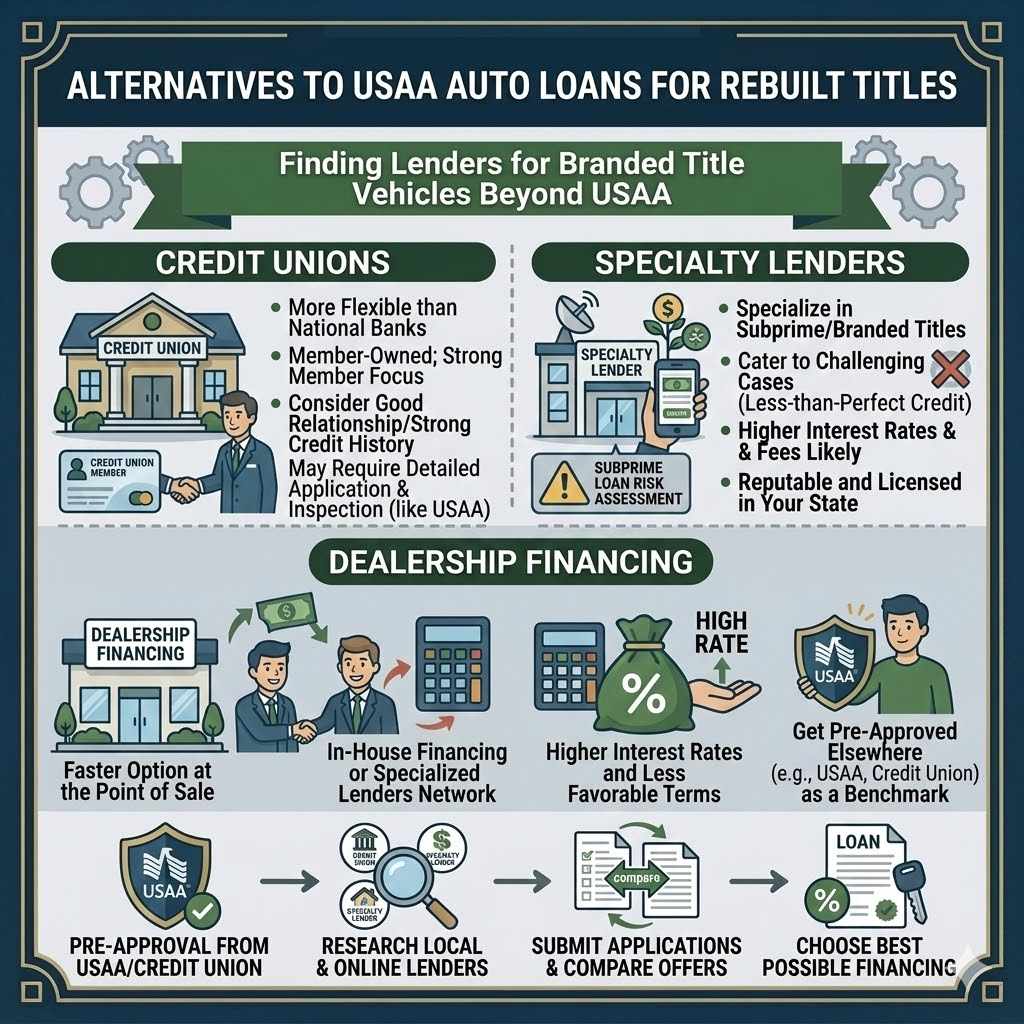

While USAA is a great option for many, it’s always good to know about alternatives. Finding lenders that offer loans for vehicles with rebuilt titles can be challenging, but they do exist. Exploring these options can help you secure the best possible financing.

Credit Unions

Local credit unions are often more flexible than large national banks. They are member-owned and may be willing to consider loans for rebuilt titles, especially if you have a good relationship with them or a strong credit history. They might offer competitive interest rates and terms.

Many credit unions have specific programs or staff members who handle these types of unique loan requests. It’s worth checking with credit unions in your area to see what they offer. They might require a more detailed application and vehicle inspection, similar to USAA.

Specialty Lenders

There are also online lenders and financial institutions that specialize in subprime auto loans or loans for vehicles with branded titles. These lenders often cater to borrowers with less-than-perfect credit or those looking for financing for vehicles that traditional lenders might avoid.

However, be cautious when exploring these options. Interest rates and fees can be significantly higher than those offered by mainstream lenders like USAA. Always read the fine print carefully and compare offers before committing.

Ensure the lender is reputable and licensed in your state.

Dealership Financing

Some car dealerships may offer in-house financing or work with a network of lenders that approve loans for rebuilt title vehicles. This can sometimes be a faster option. However, dealership financing can sometimes come with higher interest rates and less favorable terms.

If you consider dealership financing, always try to get pre-approved by USAA or a credit union first. This gives you a benchmark interest rate to compare against. It also strengthens your negotiation position.

Remember, the car dealership’s primary goal is to sell you a car, so ensure the loan terms are truly in your best interest.

Frequently Asked Questions

Question: Can USAA finance any vehicle with a rebuilt title?

Answer: USAA may finance vehicles with rebuilt titles, but they typically require a thorough inspection and documentation to ensure the vehicle is safe and roadworthy. Not all rebuilt title vehicles will qualify.

Question: What is the biggest challenge when getting a USAA loan for a rebuilt title car?

Answer: The biggest challenge is providing sufficient documentation and proof that the vehicle has been properly repaired and is safe, as lenders see a higher risk with rebuilt titles.

Question: How does a rebuilt title affect my car insurance with USAA?

Answer: A rebuilt title may affect your insurance rates or coverage options. USAA can explain their specific policies for insuring vehicles with rebuilt titles when you discuss your loan.

Question: Do I need a co-signer for a USAA loan with a rebuilt title?

Answer: While not always required, having a co-signer with good credit can improve your chances of approval or help you secure better loan terms, especially with a rebuilt title vehicle.

Question: What happens if USAA denies my loan for a rebuilt title car?

Answer: If USAA denies your loan, they will likely provide a reason. You can work on improving your credit score, gather more documentation on the vehicle’s repairs, or explore alternative lenders like credit unions.

Conclusion

Securing USAA Auto Loans for Vehicles With Rebuilt Titles is achievable with careful preparation. USAA often offers a path for members who need financing for these cars. By understanding the requirements and diligently gathering your documentation, you can make the process smoother.

Focus on finding a safe vehicle and presenting a strong case to USAA. This approach helps you get the car you need.