Can I Lease A Car For $100/Month? Essential Guide

Yes, it’s possible to lease a car for around $100 per month, but it’s extremely rare and usually involves specific niche vehicles, promotions, or very long lease terms with significant down payments. This guide will break down what makes such low payments possible and set realistic expectations.

Are you dreaming of a new set of wheels but worried about breaking the bank? The idea of leasing a car for just a hundred dollars a month sounds amazing, right? Many people wonder if this is even a real possibility. It can be frustrating when you see advertised low lease prices that seem too good to be true, and you’re not sure how to achieve them. Don’t worry, I’m here to help you understand the ins and outs of car leasing so you can make informed decisions. We’ll explore what it takes to get close to that $100/month payment and what you can realistically expect.

Understanding the Basics: How Car Leases Work

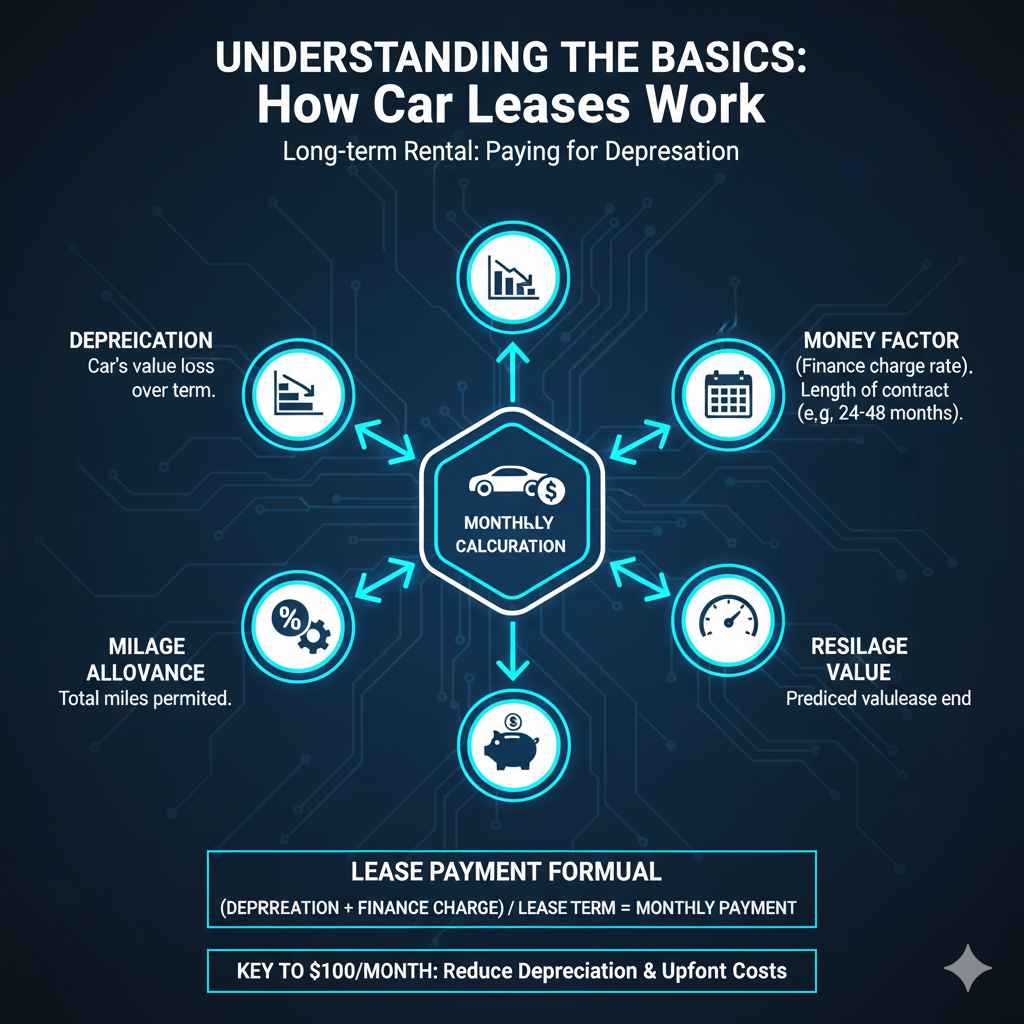

Before we dive into the possibility of a $100 monthly payment, let’s quickly go over how leasing fundamentally works. Think of a lease as a long-term rental agreement. You pay for the depreciation of the car (how much value it loses) over the lease term, rather than paying the full price of the car.

The monthly payment is calculated based on several key factors:

- Depreciation: The difference between the car’s starting value and its estimated value at the end of the lease.

- Money Factor (Interest Rate): This is like the interest rate on a loan, but expressed differently. A lower money factor means less interest paid.

- Lease Term: The length of the lease contract (e.g., 24, 36, or 48 months).

- Mileage Allowance: The total number of miles you’re allowed to drive during the lease.

- Capitalized Cost: The negotiated price of the car at the start of the lease.

- Residual Value: The predicted value of the car at the end of the lease term.

The formula for a basic lease payment looks something like this:

(Depreciation + Finance Charge) / Lease Term = Monthly Payment

To get a low monthly payment like $100, you need to significantly reduce the depreciation cost and/or pay a lot upfront. Let’s see if that’s achievable.

Can You Really Lease a Car for $100/Month? The Honest Truth

Let’s address the big question directly: Can I lease a car for $100 a month? In short, it’s highly unlikely for most mainstream new cars in typical conditions. While special promotions or niche situations might get you very close, a consistent $100 monthly payment on a new car is exceptionally rare.

Here’s why it’s so difficult:

- Car Prices: Even the cheapest new cars today often start with MSRPs (Manufacturer’s Suggested Retail Price) well over $20,000. A significant portion of that value is lost to depreciation over a typical 2-3 year lease.

- Depreciation is Key: To get a $100 payment, the car’s depreciation over the lease term would need to be incredibly low, around $2,400-$3,600 for a 24-36 month lease. This means the car would need to hold almost all of its value, which is rare for most vehicles.

- Fees and Taxes: Lease agreements include various fees, taxes, and the money factor (interest), all of which add to your monthly cost.

Factors That Can Lead to Ultra-Low Lease Payments

While a standard $100/month lease is a long shot, certain conditions can bring payments down significantly. Understanding these might help you find deals that get closer to your target, even if it isn’t exactly $100.

1. Manufacturer Incentives and Special Promotions

Automakers frequently run special lease deals to move inventory, especially on less popular models or during slow sales periods. These deals can include:

- Special Lease Cash: The manufacturer might offer thousands of dollars in incentives that reduce the capitalized cost of the vehicle, thereby lowering depreciation and your monthly payments.

- Low Money Factor: Sometimes, manufacturers offer sub-prime interest rates (money factors) to attract buyers.

- Deep Discounts: Dealerships might offer significant discounts below MSRP to meet sales targets.

These promotions are often limited in time and may apply only to specific trims or models. Keeping an eye on manufacturer websites and local dealership ads is crucial.

2. Very Long Lease Terms

Lease terms are typically 24, 36, or 48 months. Extending the lease term beyond 48 months can lower the monthly payment because you’re spreading the total depreciation cost over more months. However, this comes with significant downsides:

- Extended Warranty Issues: You might be driving a car out of its factory warranty, leading to higher repair costs.

- Higher Mileage: The car will accumulate more miles, increasing wear and tear.

- Value Decline: The car depreciates faster in later years, so you might be paying more than the car is worth towards the end of a very long lease.

Leasing for 60 or even 72 months is uncommon and often not financially sensible due to these risks.

3. High Residual Value Cars

Some vehicles hold their value better than others. Cars with historically high residual values (meaning they are predicted to be worth more at the end of the lease) will naturally have lower depreciation costs and, therefore, lower monthly payments.

Examples often include:

- Certain models from brands like Toyota, Honda, and Subaru.

- Vehicles with a strong reputation for reliability and demand.

You typically won’t find luxury or performance cars with high residual values that would make $100 payments feasible. For more details on residual values, you can check resources like fueleconomy.gov, which often lists depreciation estimates.

4. Very Small or Older Models

The cheapest new cars are usually small, entry-level models. Think compact sedans or hatchbacks. Leasing a car with an MSRP of $18,000-$20,000 is much more likely to result in a lower payment than leasing a $35,000 SUV.

Sometimes, very basic, older-generation models that are being phased out might be offered with aggressive lease deals. These cars might not have all the latest tech or features, but they can be economical for transportation.

5. Significant Down Payment or “Cap Cost Reduction”

This is one of the most common ways to achieve a lower monthly payment. By paying a large sum upfront (known as a “cap cost reduction” or down payment), you effectively reduce the capitalized cost of the vehicle. This directly lowers the total depreciation the leasing company needs to cover.

Example: Imagine a car has $12,000 in depreciation over a 36-month lease, leading to a $333 monthly payment ($12,000 / 36). If you pay $5,000 upfront as a cap cost reduction, you reduce the depreciation cost by $5,000. The new depreciation cost is $7,000, resulting in a monthly payment closer to $194 ($7,000 / 36). Paying even more upfront could theoretically bring it down further.

However, paying a huge amount upfront is generally not recommended for leases. If the car is totaled in an accident, you might not get your entire down payment back from insurance. It’s often better to keep your upfront costs low (like for the first month’s payment, fees, and taxes) and lease a car you can afford on its monthly payment alone.

6. Used Car Leases (Rare)

Leasing used cars is not as common as leasing new ones, but it does exist. Some manufacturers or leasing companies offer certified pre-owned (CPO) leases. Because the car has already undergone significant depreciation, a used car lease might offer lower monthly payments. However, the selection is limited, and the residual values might not be as favorable as for new cars.

The Reality of a $100/Month Lease Payment

Let’s put it in perspective. If a car has an MSRP of $22,000 and is expected to be worth $15,000 after 3 years (36 months), that’s $7,000 in depreciation. Divided by 36 months, that’s about $195 per month just for depreciation. Add in the money factor (interest), fees, and taxes, and you’re easily looking at $250-$350+ per month for a very basic new car.

To reach $100 per month, you’d need:

- A car with a very low MSRP (e.g., under $20,000).

- A very high residual value (meaning it depreciates very little).

- A significant promotional offer from the manufacturer (lease cash, low money factor).

- Potentially a substantial down payment.

- Possibly a longer lease term than usual, with its associated risks.

The only truly realistic scenarios for a $100 monthly payment usually involve ultra-basic, small economy cars under special, limited-time manufacturer programs, or potentially heavily discounted older models. Think of something like a Mitsubishi Mirage or a very base model Chevrolet Spark during a manufacturer-sponsored sale.

What You Can Realistically Expect for Low Monthly Payments

If $100/month is unattainable, what’s a more realistic low-end budget for leasing?

For a new, basic, small economy car with a good deal and perhaps a modest down payment, you might be looking at:

- $150 – $250 per month: This is more achievable for compact cars or subcompacts with incentives, especially if you put down a few thousand dollars and have good credit.

- $250 – $350 per month: This opens up more options, including slightly larger sedans or smaller SUVs, though still likely base models with special offers.

Remember, the “cost of the car” often quoted in lease ads is usually before taxes, fees, and any down payment. Always understand the “out-the-door” lease price.

Finding the Best Lease Deals

If you’re determined to get the lowest possible monthly payment, here’s how to search:

1. Research Your Local Market

Car prices and incentives vary significantly by region. Check the websites of manufacturers and local dealerships for current lease specials. Look for deals on models that are known for good residual values.

2. Look for “Special Lease Offers”

Manufacturers and dealerships often highlight these prominently. They might be for specific models, trims, or require certain qualifications (like loyalty discounts).

3. Consider Less Popular Models

Sometimes, less in-demand models have steeper discounts to boost sales. If you’re not set on the latest or most popular car, you might find a better deal.

4. Negotiate the Price (Capitalized Cost)

The most important number in a lease is the negotiated price of the car (the capitalized cost). Just like buying, you can negotiate this price. A lower cap cost directly translates to a lower monthly payment. Experts advise negotiating the price before discussing the lease terms.

5. Understand ALL the Fees

Be aware of:

- Acquisition fee

- Disposition fee (at lease end)

- Dealer fees (documentation fee, etc.)

- Taxes (vary by state)

- Registration and title fees

6. Check Your Credit Score

Lease offers advertised at the lowest rates (money factor) are almost always for buyers with excellent credit (generally 700+ FICO score). If your credit is less than perfect, expect higher money factors and thus higher monthly payments.

Key Lease Terms to Know

Here’s a quick rundown of essential lease terminology:

| Term | Meaning | Why It Matters |

|---|---|---|

| Capitalized Cost | The negotiated price of the vehicle for the lease. Also called “cap cost.” | Lower cap cost = lower monthly payment. Negotiate this first! |

| Money Factor | The interest rate on your lease, expressed as a decimal (e.g., .00125). | A lower money factor means less paid in interest. Multiply by 2400 to get an approximate APR (e.g., .00125 * 2400 = 3%). |

| Residual Value | The estimated value of the car at the end of the lease term. | Higher residual value = lower depreciation = lower monthly payment. |

| Depreciation | The difference between the cap cost and the residual value. This is what you essentially pay for over the lease term. | The biggest component of your monthly payment. |

| Acquisition Fee | A fee charged by the leasing company to set up the lease. | This can be rolled into the monthly payment or paid upfront. |

| Disposition Fee | A fee charged at the end of the lease when you return the car. | Avoid this fee if you plan to buy out your lease or lease a new car from the same brand whose dealership waives it. |

| Mileage Allowance | The maximum number of miles you can drive per year without penalty. | Exceeding this limit results in a per-mile charge at lease end (often $0.20 – $0.30 per mile). |

Pros and Cons of Leasing

Leasing can be a great option for some, but it’s not for everyone. Understanding the trade-offs is key.

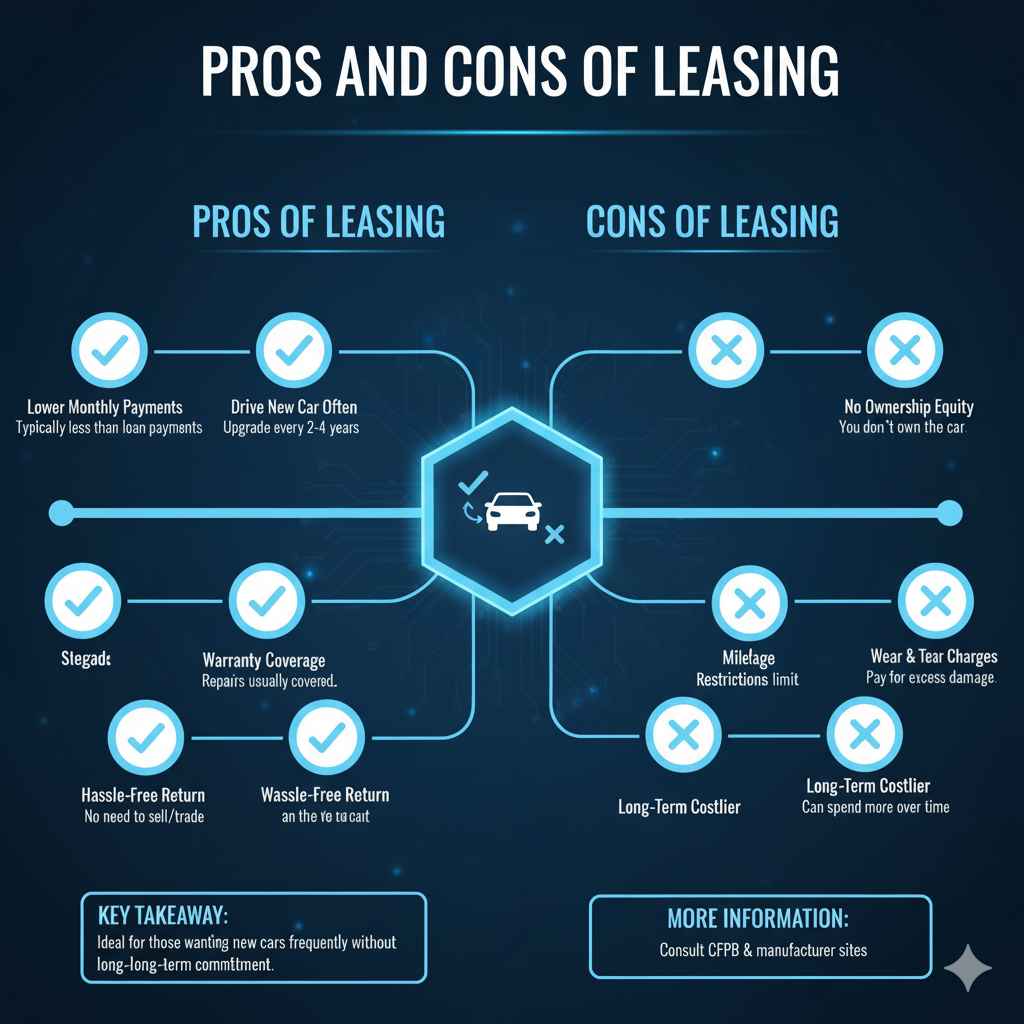

Pros of Leasing:

- Lower Monthly Payments: Generally, lease payments are lower than loan payments for the same car.

- Drive a New Car More Often: You can typically afford a new car every 2-4 years.

- Warranty Coverage: Most leases fall within the manufacturer’s warranty period, so major repairs are usually covered.

- Hassle-Free Resale: You don’t have to worry about selling or trading in the car; you just return it at the end of the lease.

- No Depreciation Worries: You’re not responsible for the car’s value tanking after a few years.

Cons of Leasing:

- No Ownership Equity: You don’t own the car. At the end of the lease, you have nothing to show for your payments.

- Mileage Restrictions: Exceeding allowed mileage can lead to expensive penalties.

- Wear and Tear Charges: You’ll likely pay for any excessive damage beyond normal wear and tear.

- Higher Costs in the Long Run: If you lease continuously, you’ll likely spend more over time than if you bought and kept a car for many years.

- Limited Customization: Modifying leased vehicles is generally not allowed.

- Early Termination Penalties: Getting out of a lease early can be very costly.

For a deeper dive into the financial aspects of leasing vs. buying, you can consult resources from organizations like the Consumer Financial Protection Bureau (CFPB).

Frequently Asked Questions (FAQ)

What is the difference between a lease and a loan?

A loan means you are buying the car and will own it once the loan is paid off. A lease is essentially a long-term rental where you pay for the car’s depreciation over a set period and return it at the end.

What credit score do I need for a good lease deal?

Most advertised lease deals are for individuals with excellent credit, generally a FICO score of 700 or higher. Your credit score significantly impacts the money factor (interest rate) offered.

Can I negotiate the price of a leased car?

Yes! The negotiated price of the car (capitalized cost) is one of the most critical factors in determining your monthly payment. Always try to negotiate this down before discussing lease terms.