Can You Lease A Car With EIN: Genius Guide

Yes, you can often lease a car with an EIN (Employer Identification Number) if you are leasing for a business. Most dealerships and leasing companies require a credit check, and for businesses, this often means using the business’s EIN and credit history instead of a personal Social Security Number.

Leasing a car can be a fantastic way to drive a new vehicle without the long-term commitment or high upfront costs of buying. But what happens when you’re looking to lease for your business? You might be wondering, “Can you lease a car with an EIN number?” It’s a common question for entrepreneurs and business owners. The good news is, yes, it’s often possible! This guide will walk you through exactly how it works, what you’ll need, and how to make it a smooth process.

Understanding EIN Leases: How It Works

An Employer Identification Number (EIN), also known as a Federal Tax Identification Number, is like a Social Security Number for your business. The IRS assigns it, and it’s crucial for various business financial activities, including opening business bank accounts, filing business taxes, and, yes, applying for business financing like a car lease.

When you decide to lease a car for your business using your EIN, the leasing company looks at your business’s financial health, not just your personal credit. This can be a great advantage, especially if your personal credit isn’t perfect or if you want to keep business and personal finances separate.

Why Lease a Car for Your Business?

Leasing a vehicle for business purposes offers several compelling benefits:

Tax Deductions: Business-related car lease payments and associated expenses (like fuel, maintenance, and insurance) are often tax-deductible. Consulting with a tax professional is always recommended to understand your specific business tax situation.

Newer Fleet: Businesses can maintain a modern and reliable fleet, projecting a professional image. Newer vehicles are typically more fuel-efficient and require less unexpected maintenance, reducing downtime.

Lower Monthly Payments: Business car leases often have lower monthly payments compared to purchasing the same vehicle outright, freeing up capital for other business investments.

Flexibility: Leasing allows businesses to upgrade vehicles more frequently, keeping pace with technological advancements and changing business needs.

Simplified Budgeting: Predictable monthly lease payments make it easier to budget for transportation costs.

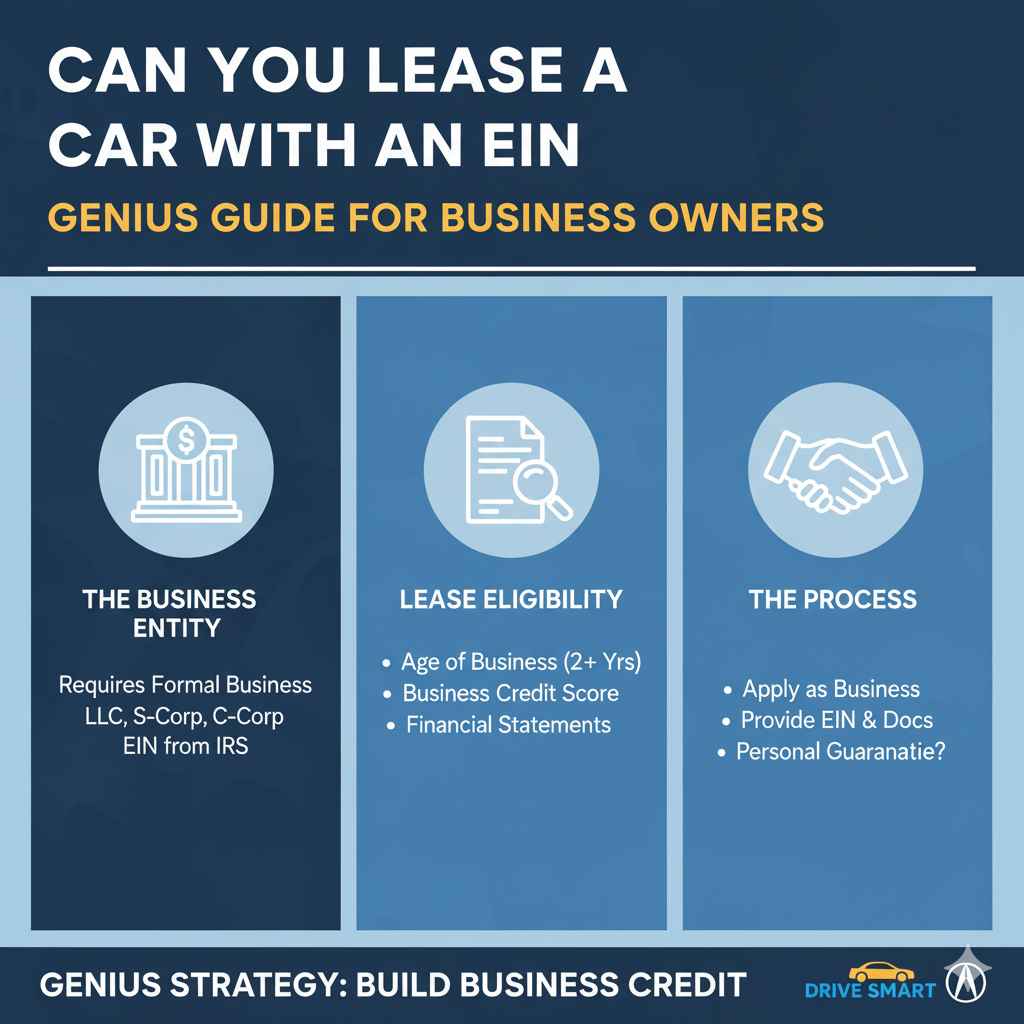

Can You Lease a Car With an EIN Number? The Process Explained

The core principle is that a business entity can take on financial obligations, and the EIN is the primary identifier for that entity. When you apply to lease a car as a business, the dealership or leasing company will require information to assess the business’s creditworthiness.

Here’s a breakdown of the typical process:

1. Gather Your Business Information

Before you even step into a dealership, get your business documents in order. You’ll need:

Your Business EIN: You can obtain an EIN from the IRS website for free.

Business Legal Structure: Are you a sole proprietorship, partnership, LLC, or corporation? This affects how the lease is structured. For example, sole proprietors might still need to provide a personal SSN alongside their EIN.

Business Bank Statements: Lenders want to see that your business has a healthy cash flow. They’ll typically ask for statements covering the last 3-6 months.

Business Financial Statements: This could include profit and loss statements and balance sheets, especially for larger businesses or more complex lease agreements.

Business Formation Documents: Such as articles of incorporation or organization.

2. Check Your Business Credit Score

Just like individuals have personal credit scores, businesses have business credit scores. These are reported by commercial credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business.

How to Check: You can often obtain a report from these bureaus, sometimes for a fee. Looking up your business credit report allows you to see what lenders see and identify any errors.

Importance: Your business credit score is a major factor in whether your lease application is approved and what terms you’ll be offered. A strong business credit history is key.

3. Choose Your Vehicle and Dealership

When you’re ready to lease, you can approach a dealership. Be upfront about your intention to lease for your business using your EIN. Some dealerships are more accustomed to business leases than others.

Look for Business Programs: Many manufacturers and dealerships have specific business or fleet sales departments. These departments are often more experienced with EIN leases and may offer special programs or incentives for businesses.

Compare Offers: Don’t settle for the first offer. Shop around at different dealerships and even contact fleet managers directly to compare lease terms, rates, and pricing.

4. Complete the Lease Application

This is where you’ll submit all your gathered business information, including your EIN. The leasing company will then conduct a “hard pull” on your business credit report.

Lender Requirements Vary: Some lenders might also require a personal guarantee from the business owner, especially for newer businesses or smaller operations. This means you would be personally responsible if the business defaults on the lease.

What to Expect: Be prepared to provide details about your business’s age, industry, annual revenue, and how many vehicles you currently operate (if any).

5. Review and Sign the Lease Agreement

Once approved, carefully review all the terms of the lease agreement. Pay close attention to:

Monthly Payment: Ensure it fits your business budget.

Lease Term: Typically 24, 36, or 48 months.

Mileage Allowance: How many miles per year can you drive? Exceeding this can incur significant fees.

Wear and Tear: Understand what is considered excess wear and tear.

End-of-Lease Options: Will you return the car, buy it, or lease a new one?

What if You’re a Sole Proprietor?

If you operate as a sole proprietor, you and your business are legally the same entity. In this case, you’ll likely use both your personal Social Security Number (SSN) and your business EIN on the lease application if you have one. The lender will assess both your personal creditworthiness and your business’s ability to generate income to cover the lease payments.

Key Differences: Personal Lease vs. Business Lease

While the goal of driving a new car remains, leasing for personal use versus business use involves some important distinctions:

| Feature | Personal Lease | Business Lease (Using EIN) |

|---|---|---|

| Primary Credit Check | Personal Credit Score (SSN) | Business Credit Score (EIN), potentially with personal credit tie-in |

| Documentation Required | Proof of income (pay stubs, tax returns), proof of address | EIN, business bank statements, financial statements, formation documents |

| Lease Use | Personal use only | Primarily business use; limited personal use may be permitted |

| Tax Implications | Generally no tax deductions for lease payments | Lease payments and expenses may be tax-deductible (consult a tax professional) |

| Vehicle Choice | Any vehicle | Often benefits from fleet programs; some luxury/exotic vehicles may have restrictions for business use |

Common Challenges and How to Overcome Them with an EIN Lease

Even with an EIN, securing a business car lease isn’t always straightforward. Here are common hurdles and how to navigate them:

1. New Business or Limited Business Credit History

If your business is new or hasn’t established a strong credit profile, lenders might be hesitant.

Solution:

Personal Guarantee: Be prepared to offer a personal guarantee. This shows the lender your commitment and provides them with additional security.

Strong Business Plan: Have a robust business plan demonstrating revenue forecasts and stability.

Build Business Credit: Open business bank accounts, get a DUNS number (Dun & Bradstreet), and establish trade lines with suppliers who report to business credit bureaus.

Significant Down Payment: A larger down payment can reduce the lender’s risk.

2. Fluctuating Business Cash Flow

Leasing requires consistent monthly payments. If your business revenue varies significantly, this can be a concern.

Solution:

Accurate Financial Projections: Provide realistic and well-supported financial projections that demonstrate your ability to meet payments even during slower periods.

Business Reserve Funds: Show that your business has sufficient liquid assets to cover lease payments for several months.

Negotiate Terms: Explore if shorter lease terms or slightly higher upfront costs in exchange for lower monthly payments are an option.

3. Dealership Unfamiliarity with EIN Leases

Some retail dealerships might be more focused on personal leases and may not have extensive experience with business EIN applications.

Solution:

Seek Out Fleet Departments: Specifically target dealerships with dedicated fleet or commercial sales departments. They are equipped to handle business leases.

Educate Yourself: Understand the process yourself so you can confidently explain your needs to the salesperson.

Direct Manufacturer Contact: Sometimes, contacting the manufacturer’s business leasing division directly can be more efficient.

4. Misunderstanding Business vs. Personal Use

It’s important to clearly define how the vehicle will be used. If claiming tax deductions, extensive personal use can be problematic.

Solution:

Maintain Detailed Records: Keep meticulous logs of business mileage, dates, destinations, and the business purpose of each trip. This is crucial for tax audits.

Consult a Tax Professional: Work with a CPA or tax advisor to understand what constitutes legitimate business use and how to properly document it.

Separate Insurance: Ensure your business auto insurance policy is correctly set up for the vehicle’s use.

Tips for a Smoother EIN Car Lease Experience

Securing a car lease with your EIN is achievable with preparation and the right approach. Here are some expert tips:

- Start Early: Don’t wait until the last minute. Building business credit takes time. Begin the process of gathering documents and checking your business credit score well in advance.

- Separate Business and Personal Finances: This is fundamental for any business. Use a dedicated business bank account for all business income and expenses, including your car lease payments.

- Know Your Numbers: Be intimately familiar with your business’s financial statements, cash flow, and credit history before approaching a lender.

- Be Transparent: Clearly state that you are leasing for business purposes and provide all required business documentation. Honesty builds trust.

- Negotiate Like a Business: Approach the negotiation process professionally. Focus on the total cost of the lease, including fees, interest rates (money factor), and residual value, rather than just the monthly payment.

- Understand All Fees: Ask for a clear breakdown of all fees, including acquisition fees, disposition fees, and any potential early termination fees.

- Read the Fine Print: Never skim the lease agreement. If anything is unclear, ask for clarification. Consider having legal counsel review it for significant business leases.

Frequently Asked Questions (FAQ)

Q1: Can I lease a car for my personal use with my EIN?

Generally, no. An EIN is for business entities. While a sole proprietor might use their EIN and SSN, the lease is still intended for business purposes if using the EIN. Most lenders will have separate processes for personal leases which rely on your personal credit history.

Q2: What if my business is brand new and doesn’t have an EIN yet?

You’ll need to obtain an EIN from the IRS first. The process is free and usually takes minutes online. Once you have it, you can proceed with the business lease application.

Q3: What’s the difference between leasing with an EIN and using a business loan?

A lease is an agreement to use a vehicle for a set period, after which you typically return it, buy it, or lease a new one. A business loan is a direct borrowing of funds that you repay over time, with the option to use the funds for purchasing a vehicle outright.

Q4: Can any business lease a car with an EIN?

Yes, most registered business entities (LLCs, corporations, partnerships, and often sole proprietors with an EIN) can apply. Lenders assess creditworthiness, not just the type of business, although certain high-risk industries might face more scrutiny.

Q5: How long does it take to get approved for a business car lease?

The approval timeline can vary. For well-established businesses with strong credit, it might be quick, sometimes within a day. For newer businesses or those with complex financials, it could take several days or even a week as lenders perform more thorough due diligence.

Q6: What happens if my business can no longer afford the lease payments?

If you included a personal guarantee, you would be personally liable for the payments. If not, the leasing company may repossess the vehicle. This can severely damage your business credit, and potentially your personal credit if you provided a guarantee. It’s crucial to have a solid financial plan.

Conclusion

Navigating the world of car leasing as a business owner might seem daunting, but with the right knowledge, it can be a smooth and advantageous process. The ability to lease a car using your EIN opens up valuable opportunities for businesses to acquire necessary vehicles while potentially benefiting from tax advantages and simplified fleet management.

Remember, preparation is key. Ensure your business is properly registered, your financials are in order, and your business credit is as strong as possible. By understanding the process, gathering the right documentation, and working with dealerships that specialize in commercial or fleet sales, you can confidently secure the vehicle your business needs. Don’t hesitate to consult with financial advisors and tax professionals to ensure you’re making the most informed decisions for your business’s growth and financial health. Happy leasing!