Cancelling an Auto Loan After Signing: Is It Possible?

Buying a car is exciting, but sometimes things change after you sign on the dotted line for a car loan. You might wonder, “Cancelling an Auto Loan After Signing: Is It Possible?” This can feel tricky, especially for folks new to buying cars. It’s a common question for a good reason.

Many people worry about being stuck with a loan they no longer want or can afford. Don’t worry, though! We’ll break it down simply and show you what steps you can take.

Let’s explore your options and see how you can handle this situation.

Understanding Auto Loan Agreements

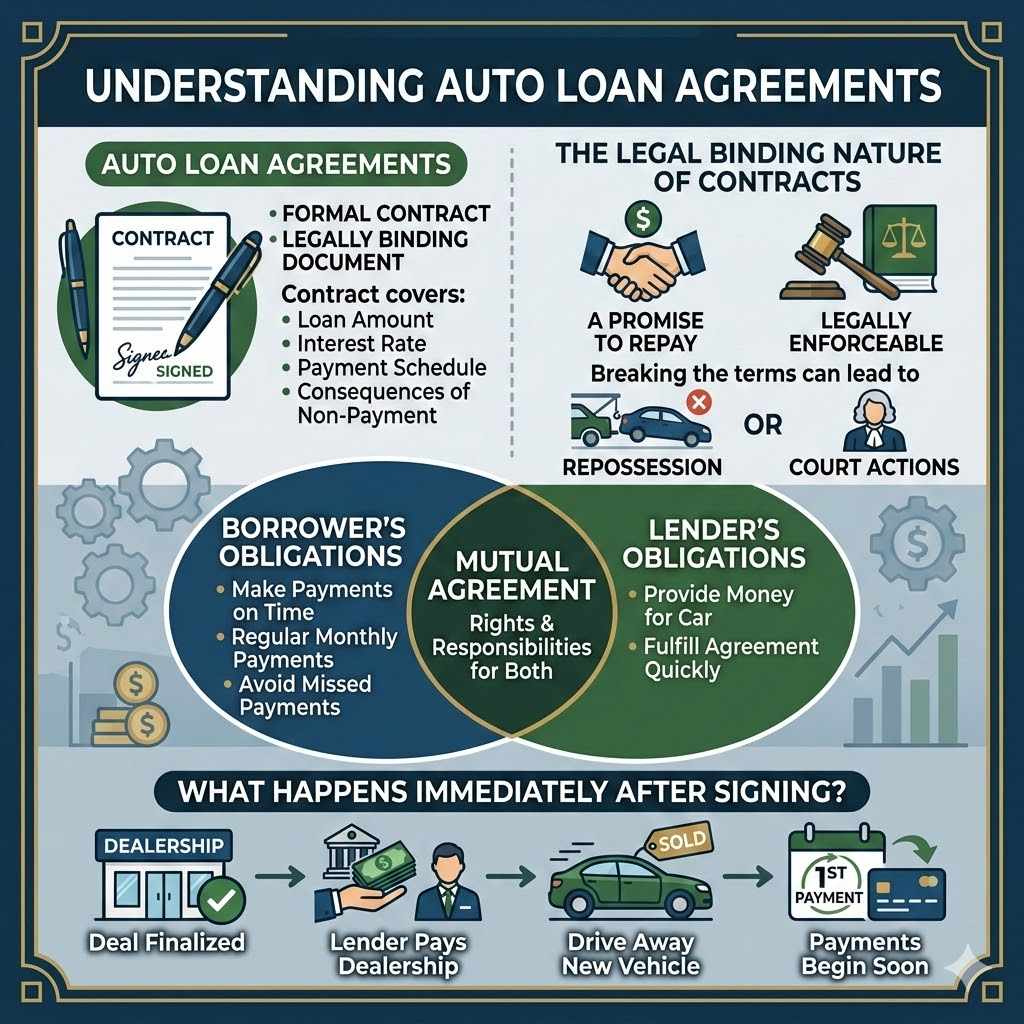

An auto loan agreement is a formal contract. It spells out the terms between you and the lender. This includes the loan amount, interest rate, payment schedule, and what happens if you don’t pay.

Once signed, it’s a legally binding document. This means both parties have obligations. For buyers, the main job is to make payments on time.

For lenders, it’s to provide the money for the car. Understanding this contract is the first step before thinking about cancelling it.

The Legal Binding Nature of Contracts

When you sign an auto loan contract, you’re making a promise. You’re promising to repay the money borrowed. The lender, in turn, promises to give you the funds.

This agreement is legally enforceable. If you break the terms, like not making payments, the lender can take actions. They might repossess the car or take you to court.

This is why cancelling a signed contract isn’t straightforward. It’s not like changing your mind about a casual purchase. It involves legal and financial commitments.

- Legally Binding Agreement: An auto loan contract is a serious legal document. It creates rights and responsibilities for both you and the lender. Once signed, you are bound by its terms, and so is the lender. This ensures fairness and predictability in the transaction for both parties involved. It’s not a document to be taken lightly.

- Lender’s Obligations: The lender’s primary obligation is to provide you with the loan amount as agreed. They have fulfilled their part by giving you the money to purchase your vehicle. This often happens immediately after signing. This action solidifies the lender’s commitment and expectation of repayment.

- Borrower’s Obligations: Your obligation is to repay the loan according to the agreed-upon schedule. This typically involves making regular monthly payments. Missing payments can lead to serious consequences, including damage to your credit score and potential repossession of the vehicle.

What Happens Immediately After Signing?

Right after signing, the deal is typically finalized. The dealership gets paid for the car by the lender. You drive away with your new vehicle, and the loan payments begin soon after.

This is the standard process for most car purchases. The lender has now committed funds, and the car is yours to use. The contract is active and in effect from the moment of signing.

It’s important to know this to understand why cancelling becomes difficult.

The car is registered in your name, and the loan is recorded. This makes the transaction official in the eyes of the law and financial institutions. It’s a significant financial step that creates a lasting relationship between you and the lender.

Think of it like a marriage of finances for the duration of the loan term.

Exploring Options for Cancelling an Auto Loan

While cancelling a signed auto loan is tough, there are a few paths you might be able to explore. These aren’t guaranteed to work, but they are worth looking into. They depend heavily on specific circumstances and the terms of your loan.

Success often hinges on how quickly you act and the goodwill of the involved parties.

The “Cooling-Off” Period Myth

Many people think there’s a “cooling-off” period, like with some retail purchases, where you can return the car and cancel the loan within a few days. This is generally a myth for auto loans. Once you sign the contract and the lender disburses the funds, the loan is active.

There isn’t a standard legal right to cancel just because you’ve had second thoughts. This is a key difference from other types of transactions.

- No Automatic Right to Cancel: Unlike some consumer contracts, auto loan agreements do not typically include an automatic right to cancel within a set number of days without penalty. The signing of the contract creates an immediate financial obligation.

- Dealership Policies Vary: Some dealerships might have their own return policies, but these are separate from the loan contract. They may allow you to return a vehicle within a certain timeframe, but this doesn’t automatically cancel the loan itself. The dealership would then have to deal with the lender.

- Financing Contingencies: In rare cases, a deal might be contingent on final financing approval. If financing falls through even after signing, the contract might be voided. However, this is usually determined before you drive the car off the lot.

Negotiating with the Dealership

Your first point of contact should almost always be the dealership where you purchased the car. They facilitated the loan, and they have the most direct relationship with you and the lender. They might be willing to work with you to find a solution.

This could involve returning the car and finding a different buyer or a different loan. It’s a negotiation, so be prepared to present your case clearly.

Explain your situation honestly and calmly. Perhaps you’ve had a sudden change in income, or there’s an unforeseen personal emergency. The dealership wants to maintain good customer relations.

They might be more inclined to help if they see you as a reasonable person facing genuine hardship.

Communicating with the Lender

If the dealership can’t help directly, you may need to speak with the actual lender. This could be a bank, credit union, or a finance company. Explain your situation and ask about any options they might offer.

They might have programs for temporary hardship or be willing to discuss options like refinancing or a loan modification. However, direct cancellation is unlikely.

Lenders are businesses focused on recouping their investment. They may be more open to solutions that prevent default. A default can be more costly for them than working out a temporary arrangement.

Be polite and professional when you communicate with them.

Rescission Rights (Limited Circumstances)

In very specific situations, you might have “rescission rights.” This is a legal right to cancel a contract. For auto loans, this usually only applies if there was fraud, misrepresentation, or a violation of certain consumer protection laws. This is not a common scenario for typical car buyers.

It typically requires legal advice to determine if you qualify.

These rights are part of consumer protection laws designed to prevent predatory lending. If you believe you were misled or that illegal practices occurred, consulting a consumer protection lawyer is essential. They can assess your case and advise on whether rescission is a viable option.

Key Factors Affecting Cancellation Possibilities

Several factors play a big role in whether you can cancel an auto loan. The timing of your attempt, the specific terms of your contract, and the policies of the dealership and lender are all critical. Understanding these elements will help you gauge your chances.

The Time Factor

Acting quickly is essential. The sooner you try to cancel, the better your chances. If you try to cancel days or weeks after signing, it becomes much harder.

The loan is already active, and payments may have already started. The lender has processed the funds, and the car is officially yours.

Each day that passes makes the transaction more solidified. This increases the complexity of unwinding it. If you realize you made a mistake or have a change of heart, reach out immediately.

Don’t delay in exploring your options.

Contract Terms and Conditions

Read your loan agreement very carefully. Look for any clauses related to early payoff, cancellation, or return policies. While unlikely to find a direct cancellation clause, there might be provisions for early repayment without significant penalties.

This is not the same as cancelling, but it could be a way to get out of the loan sooner if other options fail.

Your contract outlines the entire relationship. It details what is permissible and what is not. Any potential recourse you have will be rooted in what is written in that document.

If something is not in the contract, it’s generally not an option.

Dealership and Lender Policies

Each dealership and lender has its own set of policies. Some might be more flexible than others. A dealership that values customer satisfaction might go the extra mile.

A lender that wants to avoid bad debt might be willing to discuss options. However, these policies are internal and not legal mandates.

A dealership might have a policy of accepting returns within 7 days, but this is their choice, not a legal requirement. The loan itself remains a separate agreement with the lender. You need to understand how their internal rules interact with the loan contract.

Credit Score Impact

Any attempt to cancel or modify a loan can impact your credit score. If you try to return the car and the dealership or lender incurs a loss, it could be reported. If you miss payments while trying to sort things out, that will definitely hurt your score.

It’s important to understand the potential credit implications before proceeding.

A damaged credit score can make it harder to get loans in the future. It can also lead to higher interest rates. This is a significant long-term consequence to consider.

Weigh the immediate problem against the potential long-term damage.

Steps to Take if You Want to Cancel

If you’ve decided you absolutely need to try and cancel your auto loan, here’s a structured approach. This is a plan to follow to maximize your chances, however slim they might be. Remember, patience and clear communication are key.

-

Review Your Contract Immediately:

The very first step is to get your auto loan contract and review it thoroughly. Look for any clauses that mention early termination, buybacks, or specific return conditions. Pay close attention to the details regarding loan origination and the disbursement of funds.

Understanding the exact wording of your agreement is crucial before you talk to anyone.

-

Contact the Dealership Urgently:

Reach out to the dealership where you purchased the vehicle. Explain your situation clearly and honestly. Request to speak with the finance manager or the sales manager.

Be prepared to explain why you need to cancel the loan and return the car. Ask if they have a policy or any options available for returning the vehicle shortly after purchase.

-

Be Prepared to Negotiate Terms:

If the dealership is open to discussing a return, you may need to negotiate. They might propose you purchase a less expensive vehicle or ask you to cover certain costs associated with returning the car. Understand that they may have incurred costs, such as dealership fees or commissions, that they will want to recover.

-

Involve the Lender If Necessary:

If the dealership cannot resolve the issue directly, you may need to speak with the lender. The dealership might facilitate this conversation. Present your case to the lender, explaining your reasons for wanting to cancel.

They might offer alternatives like refinancing the loan to a more manageable term or amount, if possible.

-

Consider Professional Advice:

If you believe there were fraudulent practices or significant misrepresentations, consult with a consumer protection attorney. They can advise you on your legal rights and options, which might include contract rescission. Legal action is a last resort but can be effective in cases of severe wrongdoing.

Scenario 1: The Quick Change of Heart

Imagine you bought a car and drove it home. The next morning, you realize the monthly payments are higher than you can comfortably afford due to an unexpected bill. You immediately call the dealership.

They might be sympathetic if you haven’t driven the car much and it’s still in pristine condition. They could agree to take the car back and find a less expensive model for you, or perhaps void the sale if their policy allows. This is a best-case scenario.

Scenario 2: Discovering Hidden Fees

You purchased a car and thought everything was fine. A week later, you discover there were hidden fees in the contract that weren’t clearly explained. You feel misled.

In this situation, you might have grounds to argue for rescission based on misrepresentation. You would need to gather all documentation and potentially seek legal counsel. This is a more complex scenario with potentially stronger legal standing.

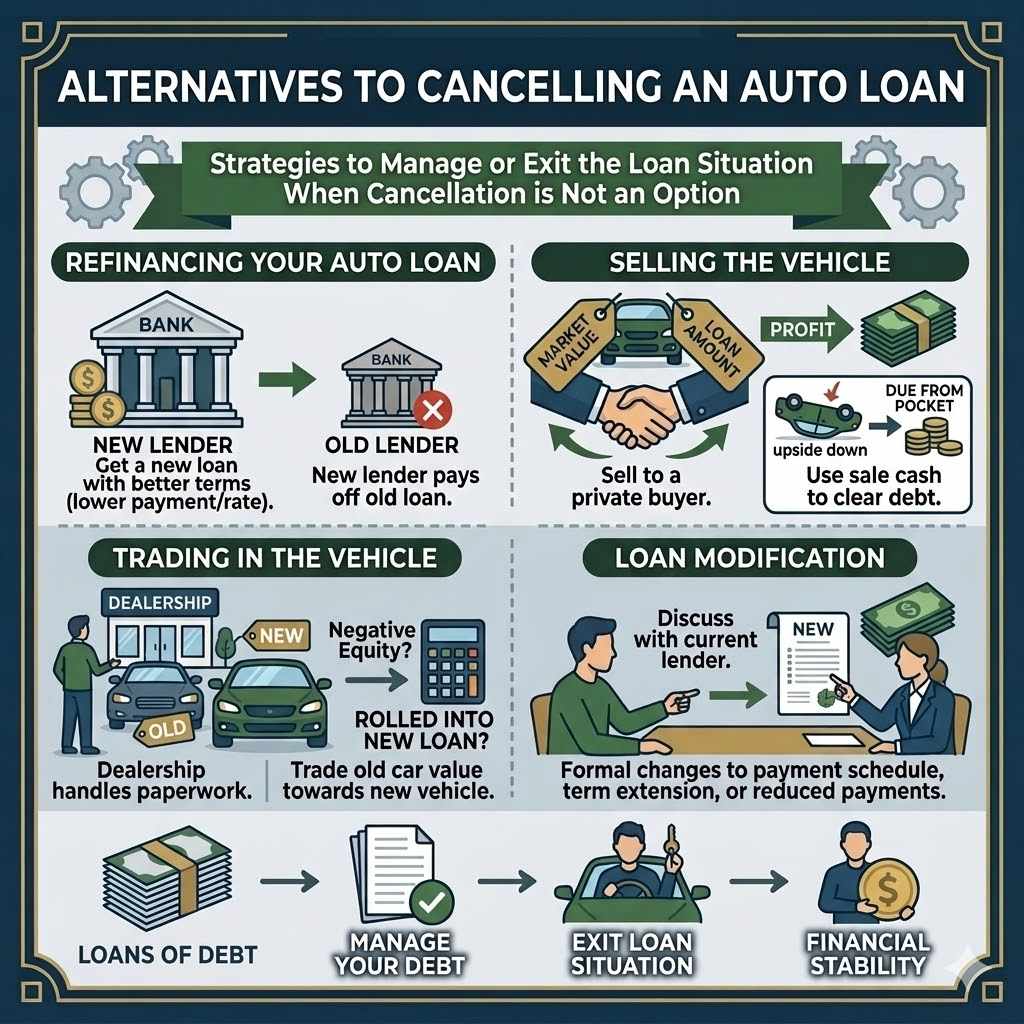

Alternatives to Cancelling an Auto Loan

If cancelling the loan proves impossible, there are other strategies you can use to manage your auto loan. These alternatives can help ease the financial burden or help you exit the loan situation over time. They are often more feasible than outright cancellation.

Refinancing Your Auto Loan

If your goal is to lower your monthly payments or interest rate, refinancing is a great option. You can apply for a new loan with a different lender to pay off your existing loan. If you have a better credit score or interest rates have dropped since you got your original loan, you might qualify for better terms.

This doesn’t cancel the loan, but it can make it more manageable.

Refinancing involves a new loan application. The new lender pays off your old loan, and you then make payments to the new lender. It’s a common way to get more favorable loan terms without the hassle of trying to cancel the original contract.

Selling the Vehicle

You can always sell the car yourself. If the amount you owe on the loan is less than the car’s market value, you can sell it and pay off the loan. The profit from the sale can help you cover any remaining balance.

If you owe more than the car is worth, you’ll have to pay the difference out of pocket to satisfy the loan. This is often called being “upside down” on your loan.

Selling the car provides you with cash. This cash is then used to clear your debt. It’s a direct way to end your obligation to the lender and the car itself.

This requires finding a buyer and completing the sale process.

Trading In The Vehicle

Similar to selling, you can trade the car in at another dealership for a different vehicle. If the trade-in value covers what you owe, you can walk away from the loan. If you owe more than the trade-in value, the dealership might roll that negative equity into a new loan.

Be cautious with this, as it can lead to higher payments on your next car.

Trading in is often simpler than selling privately. A dealership handles much of the paperwork. However, you need to be aware of how negative equity is handled.

It can be a hidden cost.

Loan Modification

If you’re facing temporary financial hardship, talk to your lender about a loan modification. They might be willing to adjust your payment schedule, extend the loan term, or temporarily lower your payments. This keeps you in good standing and avoids the negative consequences of default.

A loan modification is a formal agreement to change the terms of your existing loan. It’s designed to help borrowers who are struggling to make their current payments. This can be a lifeline for people facing unexpected financial difficulties.

Common Questions About Cancelling Auto Loans

Frequently Asked Questions

Question: Can I cancel my car loan if I change my mind a week after signing?

Answer: Generally, no. Auto loan contracts are legally binding agreements. There isn’t a standard “cooling-off” period that allows you to cancel just because you’ve changed your mind.

You would need to explore options like returning the car to the dealership or selling it, which are not guaranteed.

Question: What happens if the dealership agrees to take the car back?

Answer: If the dealership agrees to take the car back, they will likely unwind the sale. This might involve you returning the vehicle and them cancelling the loan with the lender. Be aware that they might charge you a restocking fee or for any depreciation the car experienced.

Question: Can my credit score be affected if I try to cancel my auto loan?

Answer: Yes, your credit score can be affected. If the cancellation process leads to late payments or a deficiency balance (owing more than the car is worth), this can be reported to credit bureaus. Even attempting to void a contract without proper grounds can sometimes lead to negative reporting.

Question: Are there any legal rights that allow me to cancel an auto loan after signing?

Answer: In most cases, no. However, you might have legal recourse if there was fraud, misrepresentation, or if specific consumer protection laws were violated during the sale or financing process. This usually requires professional legal advice to determine if you qualify.

Question: What is the best first step to take if I regret signing my car loan?

Answer: The best first step is to immediately review your auto loan contract. Then, contact the dealership where you purchased the car as soon as possible. Acting quickly gives you the best chance to find a solution before the loan is fully settled and the terms are irreversible.

Conclusion

Cancelling an auto loan after signing is very challenging, but not always impossible. Quick action, clear communication, and understanding your contract are key. While a simple change of mind is rarely enough, exploring options with the dealership and lender might offer solutions.

Always know the potential impact on your credit.