Does Insurance Cover Hospice Care? Essential Guide

Yes, in most cases, health insurance, Medicare, and Medicaid cover hospice care. They typically pay for the broad range of services needed to manage pain and symptoms for a terminal illness, focusing on comfort and quality of life rather than cure. Understanding your specific plan details is key.

Facing a serious illness is tough, and figuring out healthcare costs can add stress. Many people wonder if their insurance will help with the expenses of hospice care. The good news is that hospice is designed to be accessible, and most insurance plans, including Medicare and Medicaid, include coverage for its services. This guide will walk you through what you need to know, making it simple to understand your options. We’ll break down how insurance typically works with hospice care, so you can focus on what truly matters.

Understanding Hospice Care

Hospice care is a special type of support designed for individuals facing a life-limiting illness. The main goal isn’t to cure the illness, but to provide comfort, manage pain and other symptoms, and improve the quality of life for both the patient and their family. It’s a holistic approach that addresses physical, emotional, and spiritual needs.

Hospice care can be provided in various settings:

At home: The most common setting, allowing patients to remain in a familiar and comfortable environment.

In a hospice facility: Specialized centers that offer round-the-clock care.

In hospitals or skilled nursing facilities: For patients who need a higher level of medical attention or for respite care.

The hospice team often includes doctors, nurses, social workers, aides, chaplains, and volunteers. They work together to create a personalized care plan that meets the patient’s unique needs and wishes.

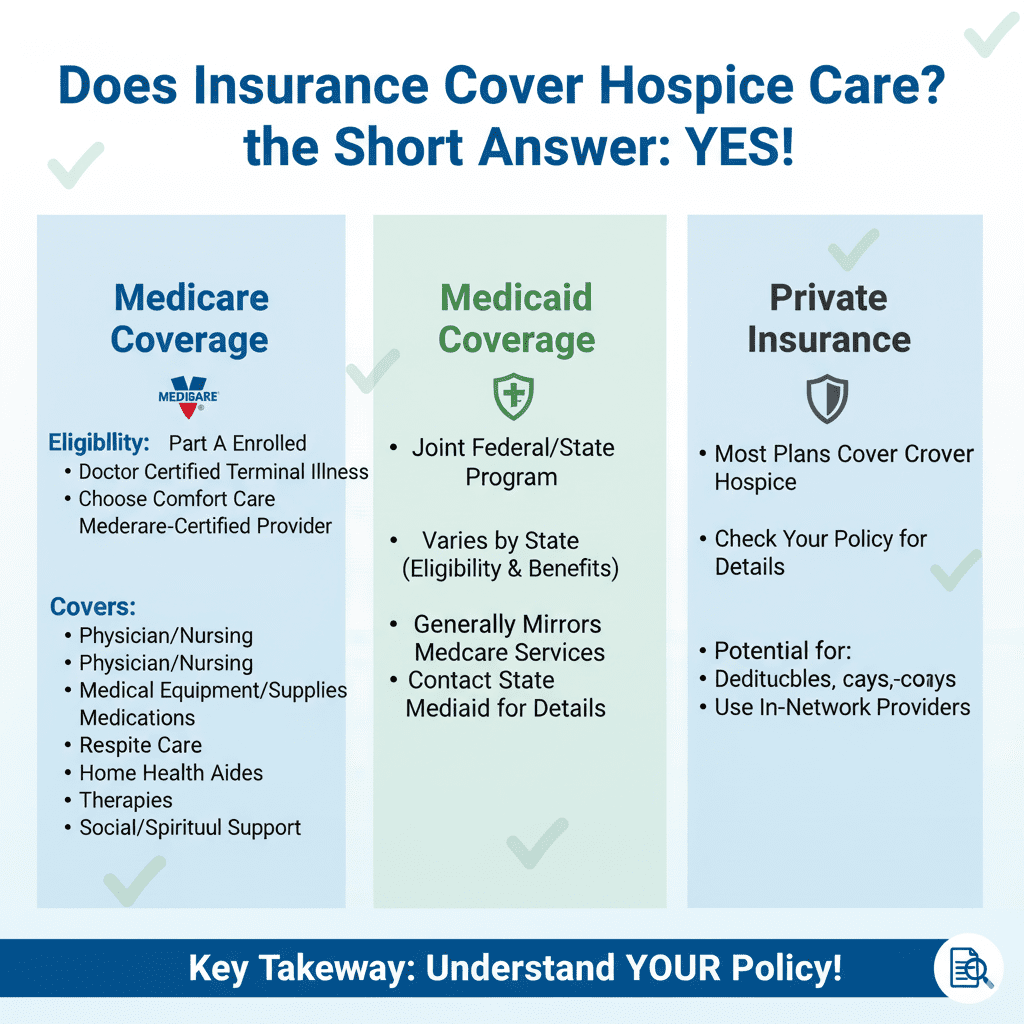

Does Insurance Cover Hospice Care? The Short Answer Is Yes!

The overwhelming answer to “does insurance cover hospice care?” is a resounding yes, but it comes with understanding the specifics of different insurance types.

For most people, hospice care is covered by their primary health insurance, Medicare, or Medicaid. These programs recognize the importance of providing comfort and support during a terminal illness and aim to remove financial barriers to accessing these services. However, the extent of coverage and what is included can vary slightly depending on the specific plan and the type of insurance you have. It’s important to get familiar with the details of your policy.

Medicare Coverage for Hospice Care

Medicare is a significant provider of hospice coverage in the United States. It provides a comprehensive benefit for hospice care for individuals who meet certain eligibility requirements.

Here’s what Medicare typically covers:

Physician and nursing services: Regular visits from doctors and nurses to manage pain and symptoms.

Medical equipment and supplies: Items like hospital beds, oxygen, and walkers needed for comfort.

Medications: Drugs related to the terminal illness and pain management.

Respite care: Short-term inpatient care to give family caregivers a break.

Home health aide and homemaker services: Assistance with daily personal care and household tasks.

Therapy services: Such as physical, occupational, and speech therapy, if needed for symptom management.

Social and spiritual support: Counseling and support services for the patient and family.

To be eligible for Medicare hospice benefits, a patient must:

Be enrolled in Medicare Part A.

Have the terminal illness certified by a doctor.

Choose hospice care instead of standard medical treatments to cure the illness.

Get care from a Medicare-certified hospice provider.

You can find more detailed information directly from the official Medicare website:

Medicare Coverage of Hospice Care

Medicaid Coverage for Hospice Care

Medicaid also provides coverage for hospice care, often mirroring Medicare’s benefits. Coverage details can vary by state, as Medicaid programs are administered at the state level.

State-Specific Variations: While the core services are generally covered, specific co-pays, deductibles, or provider networks might differ from one state to another.

Eligibility: Eligibility for hospice care under Medicaid may be tied to the individual’s overall Medicaid eligibility status.

For the most accurate information regarding your state, it’s best to consult your state’s Medicaid agency or your hospice provider.

You can find general information from the Centers for Medicare & Medicaid Services:

Private Health Insurance Coverage

Most private health insurance plans, including those offered by employers or purchased through the Health Insurance Marketplace, cover hospice care. These plans operate similarly to Medicare and Medicaid in ensuring access to comfort-focused care.

Key aspects of private insurance coverage include:

Benefit Plans: Hospice care is usually a covered benefit under the major medical portion of your plan.

Deductibles and Co-pays: You may still be responsible for deductibles, co-pays, or co-insurance, depending on your specific plan. It’s crucial to check your policy documents or contact your insurance provider.

Network Providers: Ensure that the hospice agency you choose is in-network with your private insurance plan to maximize coverage and minimize out-of-pocket costs.

It’s always a good idea to review your Explanation of Benefits (EOB) from your insurance provider to understand what costs are covered and what your financial responsibility might be.

What Services Does Hospice Care Typically Cover?

Hospice care is comprehensive, aiming to provide all necessary services for comfort and support. The core philosophy is to manage symptoms effectively and enhance the patient’s quality of life.

Here’s a breakdown of common services covered by insurance:

Medical Care:

Pain management and symptom control (nausea, shortness of breath, anxiety).

Regular physician and nursing care.

Coordination with your regular doctor.

Support Services:

Home health aides for personal care (bathing, dressing, feeding).

Social workers for emotional and practical support for the patient and family, including assistance with care planning and navigating difficult conversations.

Chaplains or spiritual counselors for spiritual support.

Grief and bereavement counseling for the family, both before and after the patient’s death.

Supplies and Equipment:

Medical equipment such as hospital beds, oxygen, and walkers.

Medical supplies like bandages and catheters.

Medications:

Prescription drugs related to the terminal illness and its symptoms.

Other Services:

Volunteer support for companionship or respite for caregivers.

Respite care (short-term stays in a facility to allow caregivers a break).

Continuous home care or inpatient care when required for symptom crisis.

What is Generally NOT Covered by Hospice Insurance?

While hospice insurance is extensive, it’s important to know what might fall outside its scope to avoid surprises. Hospice care focuses on comfort and symptom management for the terminal illness. Therefore, treatments aimed at curing the illness are typically not covered.

Curative Treatments: Any medical treatments intended to cure the terminal illness are generally not covered by hospice benefits. For example, if a patient chooses to stop hospice care to pursue experimental cancer treatment, that treatment would likely not be covered under the hospice benefit.

Room and Board: For hospice care received at home, insurance generally does not cover the costs of room and board. However, if hospice care is received in a facility, the room and board costs are usually covered by Medicare, Medicaid, or private insurance as part of the hospice benefit.

Services Not Related to the Terminal Illness: If a patient requires treatment for a condition wholly unrelated to their terminal diagnosis, coverage for that specific treatment will depend on their underlying health insurance plan.

Emergency Room Visits: Hospice patients are expected to contact their hospice team for urgent symptom management needs rather than going to the emergency room, unless it’s a true, life-threatening emergency that the hospice team cannot manage, and the condition is unrelated to the terminal illness.

How to Qualify for Hospice Care

Qualifying for hospice care involves meeting specific clinical criteria. The primary factor is a prognosis that suggests a life expectancy of six months or less if the illness runs its usual course.

Key Qualification Factors:

1. Physician Certification: A doctor must certify that the patient has a terminal illness with a prognosis of six months or less to live, assuming the illness progresses as expected. This certification is a cornerstone of hospice eligibility for all insurance types.

2. Patient/Family Choice: The patient (or their legal representative) and their family must choose to forgo curative treatments and opt for comfort-focused palliative care.

3. DNR/Advance Directives: While not always a strict requirement, healthcare providers often discuss Do Not Resuscitate (DNR) orders and other advance care planning documents with patients choosing hospice.

4. Hospice Agency Screening: Once a physician makes a referral, the chosen hospice agency will conduct its own assessment to confirm eligibility and develop a care plan.

It’s important to have open conversations with your doctor about your prognosis and care preferences. They are your best resource for understanding if hospice care is the right choice for you or a loved one.

Navigating Insurance and Hospice Providers

Choosing a hospice provider and navigating the associated insurance can feel overwhelming, but by taking a structured approach, you can ensure smooth care.

Steps to Take:

1. Talk to Your Doctor: Discuss your diagnosis, prognosis, and preferences for care with your physician. They can help you understand if hospice is appropriate and provide referrals to reputable agencies.

2. Verify Insurance Coverage: Contact your insurance provider (Medicare, Medicaid, or private insurer) to confirm your hospice benefits. Ask specific questions about what is covered, any co-pays or deductibles, and if there are network restrictions.

Have your insurance ID card handy.

Ask for the hospice benefit details.

Inquire about covered services, equipment, and medications.

Understand any out-of-pocket expenses.

3. Research Hospice Agencies:

Ask your doctor for recommendations.

Check reviews and ask for references.

Inquire about the services they offer, the expertise of their staff, and their availability (e.g., 24/7, on-call services).

Ensure they are certified by Medicare and accredited by organizations like The Joint Commission or the Community Health Accreditation Partner (CHAP).

4. Meet with Potential Agencies: Schedule meetings with a few hospice agencies to discuss their approach, answer your questions, and see if they are a good fit for your family.

5. Understand the Care Plan: Once you choose an agency, they will work with you and your doctors to create a personalized care plan. Make sure you understand what services are included and how often care will be provided.

6. Review Statements: Keep track of all bills and insurance statements related to hospice care. If anything seems unclear or incorrect, don’t hesitate to ask your hospice agency or insurance provider for clarification.

Key Questions to Ask Your Insurance Provider:

Asking the right questions upfront can save you from confusion and unexpected costs. Here are some essential questions:

| Question | What to Ask For | Why It’s Important |

|---|---|---|

| Is hospice care a covered benefit? | Confirm that hospice services are included in your plan. | This is the fundamental question to ensure any coverage at all. |

| What are the eligibility requirements for hospice? | Understand the clinical criteria, prognosis requirements, and any specific documentation needed. | Helps you and your doctor confirm you meet the necessary conditions for coverage. |

| What services are covered under hospice? | Get a detailed list of covered medical, social, emotional, and spiritual support services, as well as equipment and medications. | Ensures you know exactly what to expect and what the plan will provide. |

| Are there any co-pays or deductibles for hospice? | Clarify your out-of-pocket expenses per visit, per service, or for specific items. | Crucial for budgeting and understanding your financial responsibility. |

| Do I need to choose providers from a specific network? | Ask if there are in-network hospice agencies or if you have the freedom to choose any certified provider. | Choosing an in-network provider can significantly reduce costs. |

| What is the process for getting prior authorization? | Understand if any services require pre-approval from the insurance company. | Prior authorization ensures services are approved before they are rendered, preventing claim denials later. |

| Does coverage include inpatient respite care? | Clarify the conditions and duration for respite care coverage. | Respite care is vital for caregiver well-being, so understanding its availability is key. |

| What is covered if I need care in a facility? | Inquire about coverage for room and board and associated medical care if hospice is provided in a nursing home or inpatient facility. | Clarifies costs and benefits when care moves from home to a facility. |

Key Questions to Ask a Hospice Agency:

When you’re speaking with potential hospice providers, ask these questions to ensure they meet your needs and coordinate well with your insurance.

What are your agency’s hours of operation? Do you provide 24/7 on-call support?

What types of professionals are on your care team (doctors, nurses, social workers, aides, chaplains)?

What is your patient-to-staff ratio?

How do you handle pain and symptom management?

What is your process for developing and updating a care plan?

What training do your staff and volunteers receive?

What types of medications, equipment, and supplies do you provide?

How often will nurses and aides visit?

What services do you offer for families and caregivers?

Are you certified by Medicare and accredited by a national organization?

Do you have experience working with my specific insurance plan?

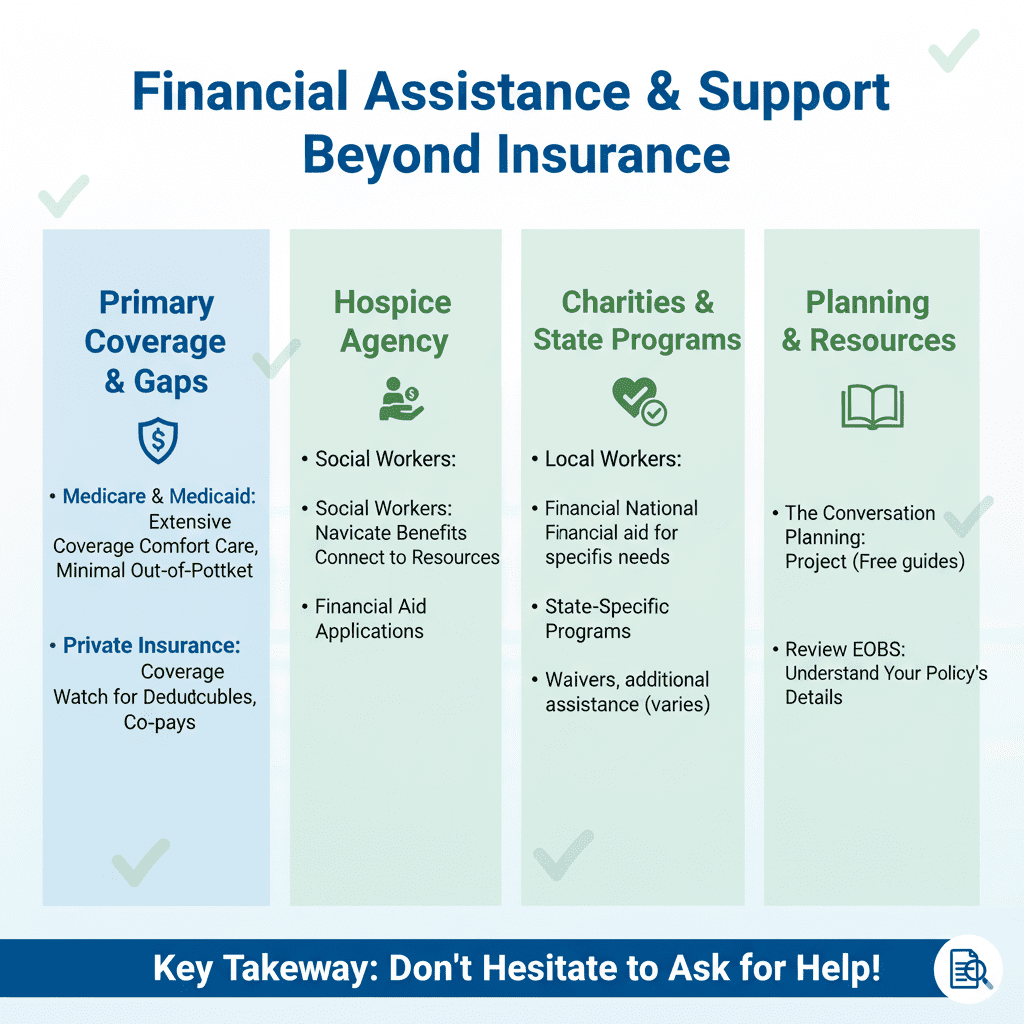

Financial Assistance and Support Beyond Insurance

While insurance covers a significant portion of hospice care, there might still be some costs or situations where additional support is beneficial.

Medicare and Medicaid: As discussed, these are primary payers and offer extensive coverage, minimizing out-of-pocket expenses.

Private Insurance Deductibles and Co-pays: If you have private insurance, be prepared for potential deductibles, co-pays, or co-insurance. Your hospice agency can often help you understand these costs.

Advance Care Planning Resources: Organizations like The Conversation Project offer free resources to help families discuss and document their end-of-life care wishes, which can prevent future financial or emotional burdens.

Charitable Organizations and Foundations: Some local or national charities may offer financial assistance for end-of-life care expenses, particularly for those who don’t qualify for or have exhausted other benefits.

State-Specific Programs: Some states may have additional programs or waivers to help cover costs associated with end-of-life care.

Hospice Agency Support: Many hospice agencies have social workers who are excellent resources for identifying financial assistance or navigating benefits. They can often connect families with local resources or apply for aid on their behalf.

Don’t hesitate to ask your hospice agency’s social worker about any potential financial concerns or available support. They are there to help ensure that financial worries don’t impede access to care.

Frequently Asked Questions (FAQ)

Q1: Does Medicare cover hospice care if I still want some treatments for my illness?

Generally, to be eligible for Medicare hospice benefits, you must choose to stop treatments aimed at curing your terminal illness. Hospice care focuses on comfort and symptom management. If you wish to continue curative treatments, Medicare may cover those treatments under its standard medical benefits, but not under the hospice benefit. It’s important to discuss this with your doctor.

Q2: What happens to my Medicare coverage while I’m on hospice care?

When you elect hospice care, your Medicare Part A coverage shifts. It will cover the hospice services provided by your chosen hospice agency. Standard Medicare Part B medical insurance will continue to cover services from your regular doctor if those services are unrelated to your terminal illness, or if the doctor is not part of the hospice team. Services directly related to the terminal illness are the responsibility of the hospice agency.

Q3: Can I switch hospice providers if I’m not satisfied?

Yes, absolutely. You have the right to change your hospice provider at any time. If you’re unhappy with your current agency, you can discuss transferring to another Medicare-certified hospice provider. Your current agency should cooperate in transferring your care to the new provider.