Does Mastercard Cover Car Rental Insurance? Full Guide

Many people wonder about car rental insurance when they rent a car. It can be a bit confusing, especially if you’re new to it. You might ask yourself, Does Mastercard Cover Car Rental Insurance?

Full Guide. This article is here to help! We will walk through everything in a simple way, step by step.

You’ll learn what you need to know to make smart choices for your next rental. Get ready to find clear answers!

Understanding Mastercard Car Rental Coverage

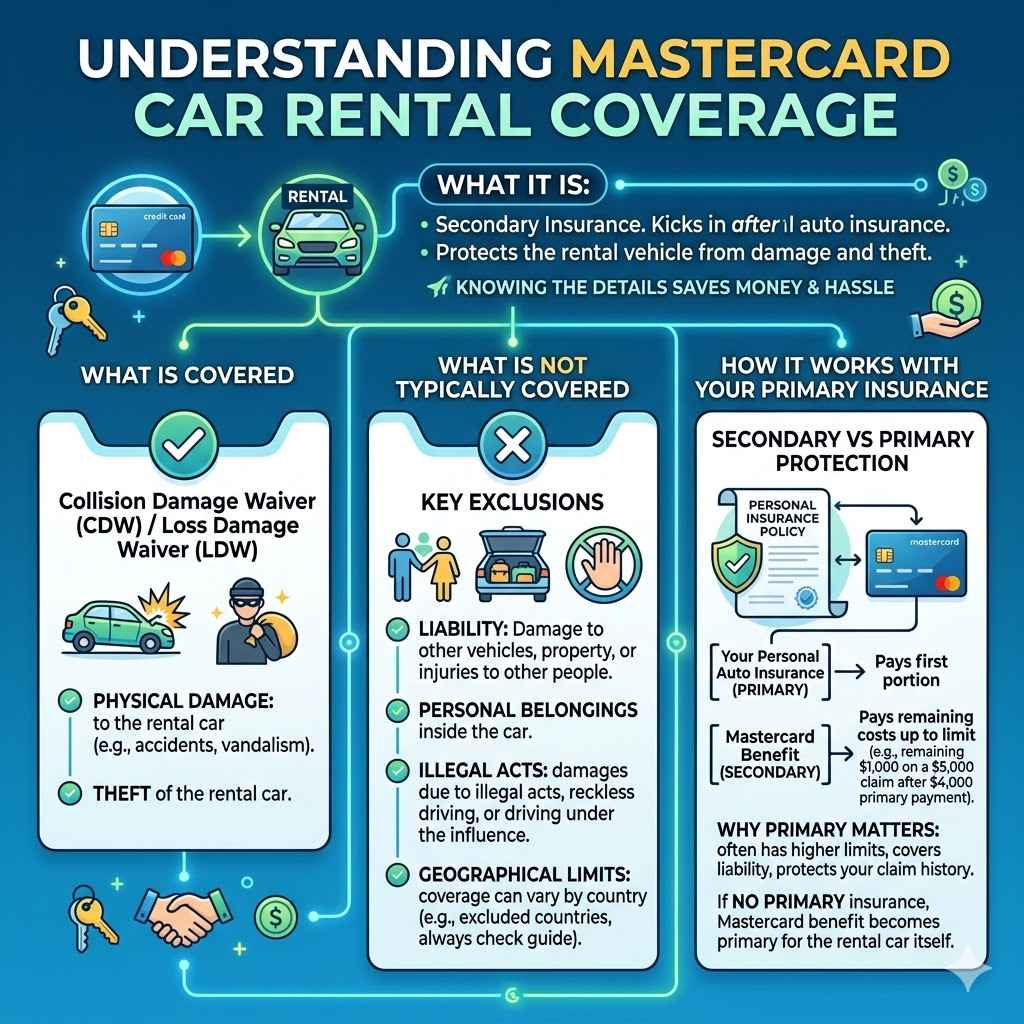

Mastercard offers valuable benefits to cardholders, and rental car insurance is one of them. This coverage acts as a secondary insurance, meaning it kicks in after any primary insurance you might have. It can protect you from damage to the rental vehicle or theft.

Knowing the details can save you money and hassle when renting a car.

What Type of Coverage Is Provided

Mastercard’s rental car insurance typically provides Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW) protection. This covers physical damage to the rental car caused by collision or theft. It does not cover liability, which is damage to other vehicles or injuries to other people.

This is an important distinction to remember.

Collision Damage Waiver CDW Explained

Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW) is a service offered by rental car companies. When you accept CDW, the rental company waives its right to charge you for any damage that occurs to the rental vehicle while it is in your possession. This includes damage from accidents, vandalism, or theft.

It is not insurance, but a waiver. Mastercard’s coverage often acts like this waiver, covering costs up to a certain limit.

What is Not Typically Covered

It’s crucial to know what is left out. Personal belongings inside the car are generally not covered. Liability for damage to other cars or property, or for injuries to other people, is also usually excluded.

Damages due to illegal acts, reckless driving, or driving under the influence of alcohol or drugs are also typically not covered by Mastercard’s benefit.

Geographical Limitations

Mastercard’s rental car insurance benefits can vary based on where you rent the car. Coverage is generally available in the United States, Canada, and many other countries. However, certain countries may be excluded.

Always check your specific Mastercard benefits guide to confirm the coverage area for your card.

The Role of Primary Insurance

Your personal auto insurance policy is often considered your primary insurance for rental cars. If you have comprehensive and collision coverage on your own car, it may extend to rentals. Mastercard’s coverage acts as secondary protection.

This means if you file a claim with your personal insurance, Mastercard’s benefit will cover any remaining costs up to its limits after your personal insurance has paid its portion.

Why Primary Insurance Matters

Having primary insurance is important because it often has higher coverage limits and may cover liability. It also protects your personal insurance claim history. If you don’t have personal auto insurance, or if your policy does not cover rentals, then Mastercard’s secondary coverage becomes your primary protection for the rental car itself.

How Secondary Coverage Works

When you use Mastercard’s benefit, it pays after your primary insurance. For example, if the rental car has $5,000 in damage and your personal insurance covers $4,000, Mastercard’s secondary coverage would step in to pay the remaining $1,000, up to the benefit limit. This can help you avoid paying out-of-pocket for damages.

Activating Your Mastercard Rental Coverage

To benefit from Mastercard’s rental car insurance, you must follow specific steps. These steps are key to ensuring your coverage is active and valid. If you do not meet these requirements, your claim might be denied.

It is essential to be diligent about these details before and during your rental.

Paying with Your Mastercard

The most critical step to activate your coverage is to pay for the entire rental car transaction with your eligible Mastercard. This includes all rental fees, taxes, and charges. If you use another payment method for any part of the rental, you risk invalidating the coverage for the entire rental period.

This is a strict rule.

Eligible Mastercard Types

Not all Mastercard cards offer this benefit. Typically, this coverage is provided with World Mastercard and World Elite Mastercard cards. Standard Mastercard or Standard Plus Mastercard cards may not include rental car insurance.

You should verify the specific benefits associated with your card by checking your cardholder agreement or the Mastercard website.

The Full Rental Cost Requirement

You must pay the full rental charge with your Mastercard. This means the entire cost of the rental agreement, from the daily rate to all associated fees and taxes, must be charged to your card. If you pay for part of the rental with another card or cash, the insurance benefit usually becomes void.

Declining the Rental Company’s Insurance

When you rent a car, the rental company will offer its own Collision Damage Waiver or insurance. To use your Mastercard coverage, you must decline the rental company’s CDW or LDW. If you accept their insurance, your Mastercard benefit will not apply.

This is because their insurance becomes your primary coverage.

Why Declining is Necessary

Mastercard’s benefit is designed to be secondary to your personal insurance, but it acts as primary if you do not have personal coverage or if you decline the rental company’s expensive insurance. Accepting the rental company’s insurance voids your Mastercard benefit because you are essentially opting for their protection instead.

Keeping Records of Your Decision

Make sure to get confirmation in writing from the rental agent that you have declined their insurance. This documentation is very important if you ever need to make a claim. It proves you did not accept their coverage, thus making your Mastercard benefit applicable.

Renting from Approved Companies

Mastercard’s coverage typically only applies when you rent from approved rental car agencies. Most major car rental companies are usually included, but it’s wise to check. Some discount or specialty rental agencies might not be covered.

Major Rental Agencies Covered

Companies like Hertz, Avis, Budget, Enterprise, Alamo, and National are generally recognized by Mastercard for rental car insurance benefits. These are the most common providers you will encounter. However, it is always best to verify before booking.

Checking for Exclusions

Some rental arrangements may be excluded. For instance, renting vehicles for extended periods beyond a certain number of days (often 31 consecutive days) might not be covered. Also, rentals from private owners or through certain car-sharing platforms might not qualify.

Always review your card’s benefits guide.

Making a Claim with Mastercard

If you experience damage or theft of a rental car that was paid for with your eligible Mastercard and you declined the rental company’s insurance, you can file a claim. The process involves contacting the benefits administrator and providing necessary documentation.

Contacting the Benefits Administrator

The first step in filing a claim is to contact the Mastercard benefits administrator. They will provide you with the claim forms and guide you through the process. You usually have a limited time to report the incident and submit your claim, so act quickly.

How to Find Contact Information

The contact information for the benefits administrator is typically found on the Mastercard website or in your cardholder benefits guide. You can usually find a dedicated phone number for claims. Keep this information handy.

What to Report

When you contact them, be prepared to provide details about the rental car company, the rental dates, the amount of damage, and how the incident occurred. The sooner you report it, the better.

Required Documentation for Claims

A successful claim requires thorough documentation. This includes the rental agreement, a police report if applicable, repair estimates, and proof of payment with your Mastercard. Missing documents can delay or deny your claim.

Rental Agreement Details

You’ll need a copy of the complete rental agreement. This should show your name, the car details, the rental period, and the total cost. It must clearly show you paid with your Mastercard and declined the rental company’s insurance.

Damage Reports and Receipts

If the car was damaged, you’ll need a police report (if one was filed) and a damage report from the rental company. Receipts for any towing, repairs, or loss of use charges are also essential. Mastercard will review all these to determine reimbursement.

Proof of Payment

A statement from your Mastercard showing the full rental charge is vital. This proves you met the primary condition for activating the coverage. Without this, your claim will not proceed.

Claim Processing Timeframes

Claim processing can take several weeks to a few months, depending on the complexity of the case and the completeness of your submitted documents. Prompt submission of all required information speeds up the process.

Factors Affecting Speed

The speed of the claim depends on how quickly you submit your documents and the cooperation of the rental company. Investigations into the circumstances of the damage can also take time. Be patient, but follow up if you don’t hear back within expected timeframes.

What to Expect

You will be kept informed about the status of your claim. Once a decision is made, you will receive notification. Approved claims will be reimbursed according to the terms of your Mastercard’s benefits.

Comparing Mastercard Coverage to Other Options

Understanding how Mastercard’s rental car insurance stacks up against other options is key. This helps you decide whether to rely on your card benefit or purchase additional coverage.

Mastercard vs. Rental Company Insurance

Rental companies often charge daily fees for their CDW/LDW, which can add up significantly. Mastercard’s coverage is a no-cost benefit for eligible cardholders. While the rental company’s insurance might offer broader coverage, including liability, it comes at a higher price.

Cost Comparison

Rental company insurance can cost anywhere from $15 to $30 per day or more. Mastercard’s coverage, on the other hand, is included with your card. This makes it a much more budget-friendly option for protecting the rental car itself.

Coverage Scope

Rental companies often provide more comprehensive packages that include liability protection. Mastercard’s benefit typically covers only damage to or theft of the rental vehicle. You might need separate liability insurance, either through your personal policy or by purchasing it from the rental agency.

Mastercard vs. Personal Auto Insurance

Your personal auto insurance might already cover rental cars. However, using your personal insurance for a rental can lead to higher premiums if you make a claim. Also, your personal policy’s deductible might be higher than what Mastercard’s benefit covers.

Impact on Premiums

Making a claim on your personal auto insurance for a rental car can increase your monthly premiums. Using Mastercard’s benefit, which is a separate perk, usually does not affect your personal insurance rates. This is a major advantage.

Deductible Differences

If your personal auto insurance has a high deductible, like $500 or $1,000, you’ll be responsible for paying that amount before your insurance covers the rest. Mastercard’s benefit can cover the cost of damage up to its stated limits, potentially saving you from paying a large deductible.

Mastercard vs. Travel Credit Cards

Some other travel credit cards also offer rental car insurance. The terms, coverage limits, and eligibility requirements can differ significantly between card issuers. It is essential to compare the specific benefits of your Mastercard against any other cards you hold.

Comparing Benefit Details

Each card issuer has its own set of rules. Some may offer primary coverage, while others offer secondary coverage, just like Mastercard. The maximum coverage amounts can also vary greatly.

Always read the fine print for each card’s benefits.

Card Type Matters

Just as with Mastercard, not all cards from other issuers will provide this benefit. Premium travel cards are more likely to include robust rental car insurance. It is worth checking the benefits guide for any travel-focused credit cards you possess.

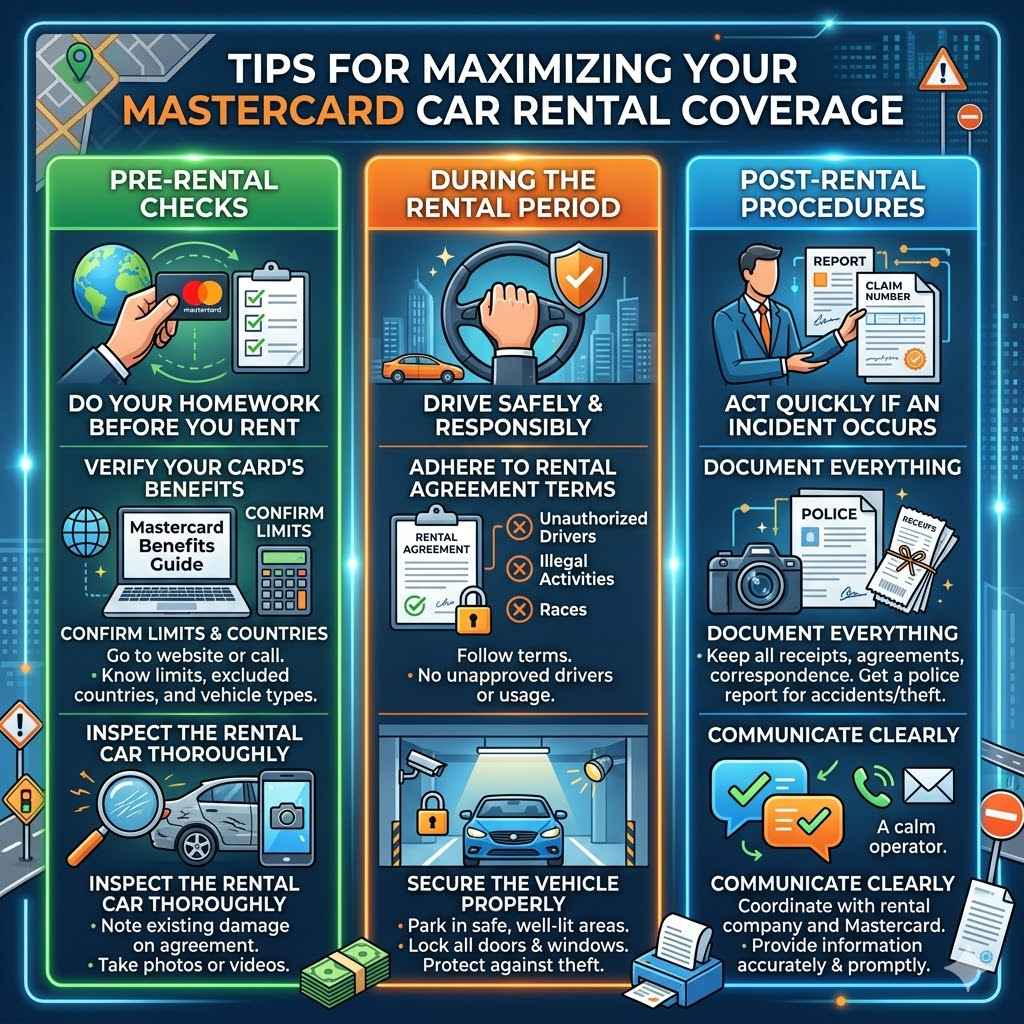

Tips for Maximizing Your Coverage

To get the most out of your Mastercard rental car insurance, follow these practical tips. Being prepared can prevent issues and ensure you have the coverage you need.

Pre-Rental Checks

Before you even pick up the car, do your homework. Confirm your card’s specific benefits, check rental car company exclusions, and know your claim process beforehand. This preparation can save you from unwelcome surprises.

Verify Your Card’s Benefits

Go to the Mastercard website or contact your bank to get the official benefits guide for your specific card. Understand the coverage limits, the countries included, and any specific vehicle types that are excluded. This information is your best defense.

Inspect the Rental Car Thoroughly

Upon picking up the car, carefully inspect it for any existing damage. Make sure any pre-existing scratches, dents, or interior wear are noted on the rental agreement before you drive away. Take photos or videos of the car’s condition as well.

During the Rental Period

Drive safely and responsibly. Avoid any situations that could void your coverage, such as illegal parking, reckless driving, or consuming alcohol before driving.

Adhere to Rental Agreement Terms

Always follow the terms of your rental agreement. Do not allow unauthorized drivers to operate the vehicle, and do not use the car for illegal activities or races. These actions will certainly invalidate any insurance or waiver benefits.

Secure the Vehicle Properly

When parking the car, ensure it is in a safe, well-lit area. Lock all doors and windows. If possible, use a secured parking garage.

Theft coverage depends on you taking reasonable steps to protect the vehicle.

Post-Rental Procedures

If an incident occurs, act quickly to report it and gather documentation. The sooner you start the claim process, the smoother it will be.

Document Everything

Keep all receipts, rental agreements, and any correspondence related to the rental. If there was an accident or theft, get a copy of the police report. Documenting every detail helps build a strong case for your claim.

Communicate Clearly

When dealing with the rental company and the Mastercard benefits administrator, communicate clearly and politely. Provide all requested information accurately and promptly. This cooperative approach can lead to a more efficient resolution.

Frequently Asked Questions

Question: Does Mastercard cover all rental car insurance?

Answer: No, Mastercard provides a specific type of coverage, usually a Collision Damage Waiver or Loss Damage Waiver, for damage to or theft of the rental vehicle. It typically does not cover liability for damage to other vehicles or people.

Question: Do I need to decline the rental company’s insurance?

Answer: Yes, you must decline the rental company’s Collision Damage Waiver or Loss Damage Waiver for your Mastercard coverage to be valid. Accepting their insurance means you are opting for their coverage instead.

Question: What if I don’t have personal car insurance?

Answer: If you do not have personal car insurance, your Mastercard’s rental car coverage will act as your primary protection for damage to or theft of the rental car, up to the benefit limits.

Question: Can I use my Mastercard benefit for international rentals?

Answer: Coverage for international rentals varies by card. Some World and World Elite Mastercard cards offer coverage in many countries, but you must verify the specific terms and conditions for your card to confirm geographic limitations.

Question: How long does it take to get reimbursed after a claim?

Answer: Reimbursement timeframes can vary. Generally, it can take several weeks to a few months, depending on the complexity of the claim and how quickly all necessary documentation is submitted and processed.

Conclusion

Mastercard offers a valuable rental car insurance benefit for many cardholders. By paying with your eligible Mastercard and declining the rental company’s insurance, you can protect yourself from significant costs. Always confirm your card’s specific terms and keep all rental documentation.

This makes your rental experience much smoother and safer.