Does United Explorer Card Cover Rental Car Insurance: Proven

Yes, the United Explorer Card offers primary rental car insurance. This means it covers theft and collision damage for most rental cars in the U.S. and abroad. To use it, you must decline the rental company’s collision damage waiver (CDW) and pay for the entire rental with your United Explorer Card.

Renting a car can be stressful. You stand at the counter, tired from your flight, and they push a bunch of extra insurance options at you. Do you need it? Is it a good deal? It’s confusing, and nobody wants to pay for something they don’t need. This is a common problem for drivers everywhere.

But what if you already have great coverage in your wallet? Many people don’t realize that their credit card can save them a lot of money and worry. We are going to walk through exactly what the United Explorer Card offers. You will learn what it covers, what it doesn’t, and how to use it correctly. You’ll feel confident the next time you rent a car.

Renting a car should be simple, but the insurance part often feels like a pop quiz. The most common add-on the rental company tries to sell you is the Collision Damage Waiver (CDW), also known as a Loss Damage Waiver (LDW). This isn’t technically insurance. It’s an agreement where the rental company agrees not to charge you if the car is damaged or stolen. However, this waiver can cost you an extra $15 to $30 per day, which adds up fast!

The good news is, if you have the United Explorer Card, you can confidently say “no, thank you” to the rental company’s expensive CDW. Your card comes with a powerful benefit that can protect you and save you a significant amount of money. Let’s break down exactly how it works.

Understanding Your Card’s Built-In Protection

The United Explorer Card provides an “Auto Rental Collision Damage Waiver.” This is a form of insurance that covers you against theft or damage to the rental vehicle. The most important thing to know about this benefit is that it is primary coverage.

This is a huge deal, and it’s what sets this card apart from many others. So, what does “primary” mean in simple terms?

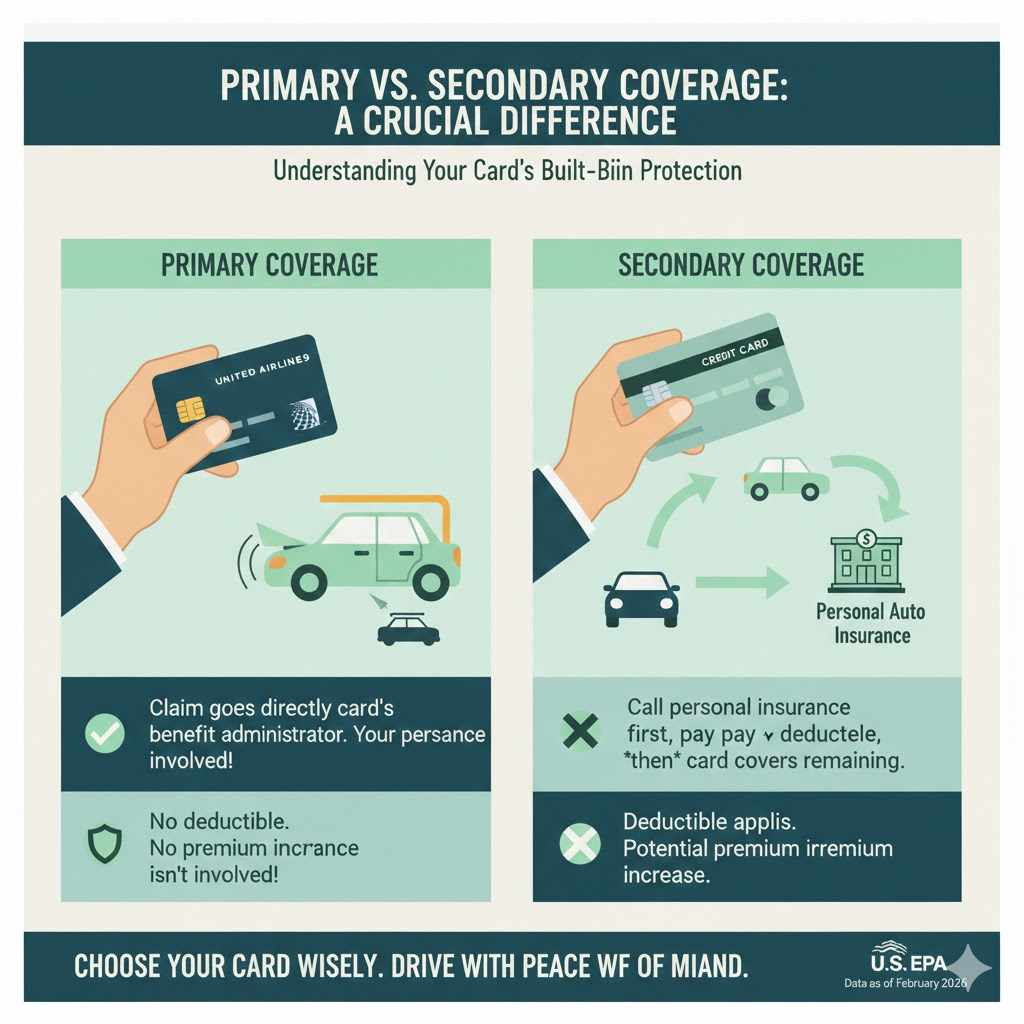

Primary vs. Secondary Coverage: A Crucial Difference

Imagine you have two friends who can help you move a heavy box. A “primary” helper is the one you call first. A “secondary” helper is the one you call only if the first one can’t do the job. Car rental insurance from credit cards works the same way.

- Primary Coverage (Like the United Explorer Card): This is your first line of defense. If your rental car is damaged or stolen, you file a claim directly with the credit card’s benefit administrator. You do not have to involve your personal car insurance company at all. This means you don’t have to pay your personal insurance deductible, and your premiums won’t go up because of the claim.

- Secondary Coverage (Common on many other cards): This coverage only kicks in after your personal auto insurance has paid out. You have to file a claim with your own insurance first, pay your deductible, and then the credit card’s benefit may cover what’s left over. It’s better than nothing, but it’s not nearly as convenient or valuable as primary coverage.

Because the United Explorer Card offers primary coverage, it acts like the main insurance for your rental car’s physical well-being. This gives you incredible peace of mind and can save you from a major headache and financial hit if something goes wrong.

What Does the United Explorer Card Rental Insurance Cover?

The coverage is quite comprehensive for most typical rental situations. It’s designed to protect you from the most common and costly issues you might face with a rental car. Think of it as a shield for the vehicle itself.

Here’s a clear breakdown of what is generally included:

| Covered Events | Description |

|---|---|

| Collision Damage | This covers physical damage to the rental car, whether it’s a small dent in a parking lot or significant damage from an accident. |

| Theft | If the rental car is stolen, the coverage will reimburse you for the value of the vehicle. |

| Vandalism | Covers damage caused by intentional acts, such as a broken window or slashed tires. |

| Loss of Use Charges | If the car needs repairs, the rental company loses money because they can’t rent it out. They will charge you for this “loss of use.” Your card’s benefit covers these charges, as long as they are substantiated by the rental company. |

| Towing Charges | Covers reasonable towing expenses to get the damaged vehicle to the nearest qualified repair shop. |

Essentially, this benefit covers the actual cash value of the vehicle. It’s designed to make the rental company whole again without you having to pay out of pocket for damage or theft.

What Is NOT Covered? Important Exclusions to Know

While the coverage is excellent, it’s not a magic wand that covers everything. Knowing the exclusions is just as important as knowing the benefits. This helps you make smart decisions and avoid any surprises.

Here are the key things the United Explorer Card’s rental insurance does not cover:

- Liability Insurance: This is the most critical exclusion. The card’s benefit does not cover damage to other vehicles, property, or injuries to other people. You are still responsible for liability. You can learn more about liability requirements from sources like the Insurance Information Institute. Most drivers have this through their personal auto policy, which often extends to rental cars. If you don’t own a car or your policy doesn’t cover rentals, you may need to purchase a separate liability policy from the rental company.

-

Certain Vehicles: The policy has limits on the types of vehicles it covers. Excluded vehicles typically include:

- Expensive, exotic, or antique cars (like a Ferrari or a car over 20 years old).

- Large passenger vans designed for more than 9 people.

- Trucks with open beds.

- Limousines, RVs, and campers.

- Off-road vehicles.

- Specific Countries: While coverage is worldwide, there are a few countries that are often excluded from coverage. These can include places like Israel, Jamaica, and Ireland, though this list can change. Always check your card’s guide to benefits before traveling internationally.

- Long-Term Rentals: The coverage is valid for rental periods of 31 consecutive days or less. If you need a car for longer, this benefit won’t apply.

- Personal Injury: Your own medical expenses or those of your passengers are not covered by this benefit. That would fall under your personal health insurance or the medical payments coverage on your auto policy.

- Personal Belongings: If your laptop or luggage is stolen from the rental car, this policy will not cover it. That would be covered by your homeowner’s or renter’s insurance.

How to Activate Your United Explorer Card Rental Car Insurance: A Step-by-Step Guide

Using this benefit is very easy, but you have to follow two simple rules. If you miss either of these steps, the coverage will not apply, and you could be responsible for the full cost of any damage.

Follow these steps every time you rent a car:

Decline the Rental Company’s CDW/LDW

When you get to the rental counter, the agent will offer you their Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW). You must politely but firmly decline this coverage. If you accept and pay for their waiver, even for a single day, you void your credit card’s primary coverage for the entire rental period. Be clear and say, “I will be using the primary coverage provided by my credit card, so I am declining your CDW.”

Pay for the Entire Rental with Your United Explorer Card

You must use your United Explorer Card to pay for the entire rental transaction. You cannot split the payment with another card, use cash for part of it, or use rental points for the full amount. The name on the credit card must also match the name of the primary driver on the rental agreement.

That’s it! By following these two steps, your primary insurance coverage is automatically activated. There are no forms to fill out beforehand and no need to call anyone to “turn it on.”

Card Insurance vs. Rental Counter Insurance: A Cost Comparison

So, how much can this benefit really save you? Let’s look at a simple comparison for a one-week car rental. The cost of a CDW from a rental agency can vary, but we’ll use a conservative estimate.

| Feature | United Explorer Card Benefit | Rental Company CDW/LDW |

|---|---|---|

| Cost | $0 (Included with your card) | $15 – $30 per day (or $105 – $210 per week) |

| Coverage Type | Primary (Doesn’t involve your personal insurance) | Waiver (From the rental company) |

| Deductible | $0 | Often $0, but read the fine print |

| Benefit | Saves you money and protects your personal insurance record from claims. | Convenient but expensive. Adds a significant cost to your rental. |

As you can see, relying on your United Explorer Card can easily save you over $200 on a single week-long trip. Over several rentals a year, this benefit alone can more than cover the card’s annual fee.

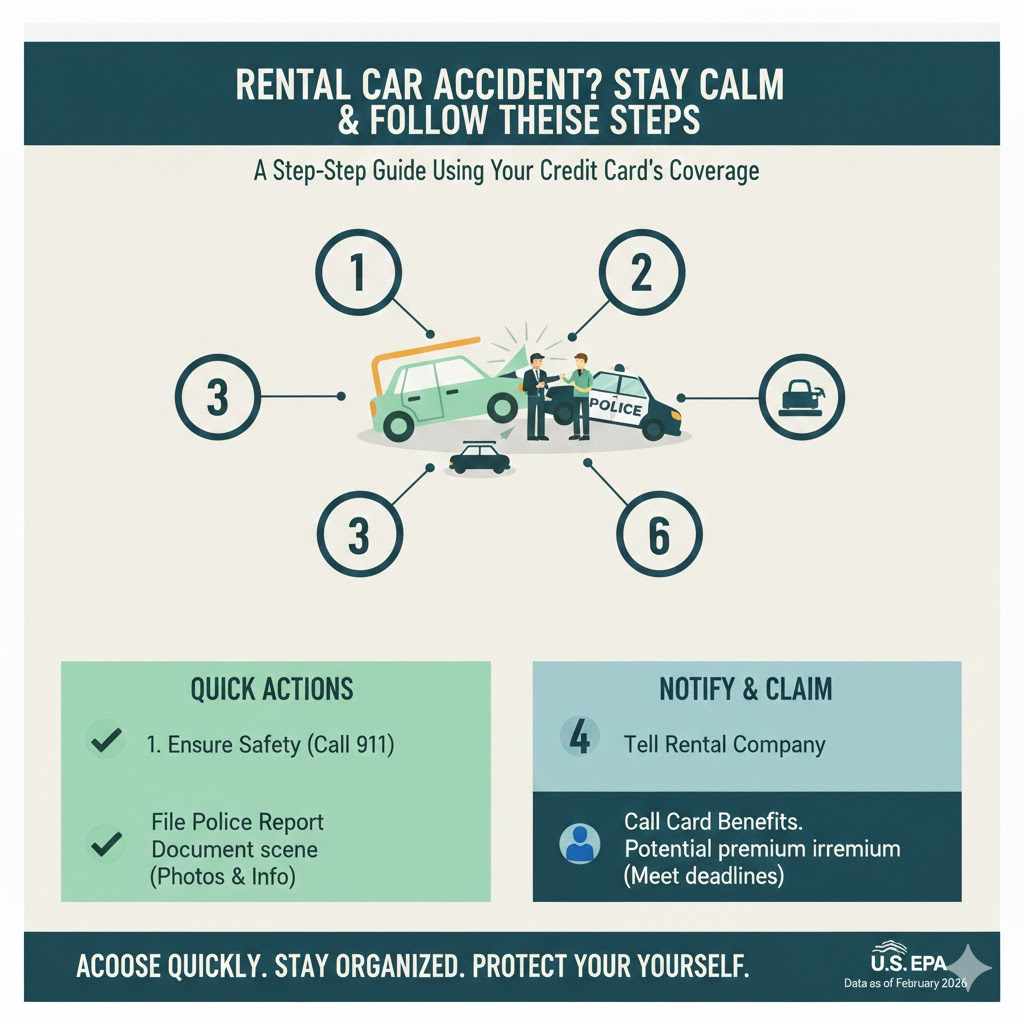

What to Do If You Have an Accident in a Rental Car

Accidents are stressful, but knowing what to do can make the process much smoother. If you get into an accident or the car is stolen while using your United Explorer Card’s coverage, follow these steps:

- Ensure Everyone’s Safety: First and foremost, check if anyone is injured and call for medical help if needed. Move to a safe location if you can.

- File a Police Report: Always get an official police report, no matter how minor the accident seems. The benefits administrator will require this for your claim.

- Document Everything: Take photos of the damage to your rental car and any other vehicles involved. Get the contact and insurance information from any other drivers. Write down the names and phone numbers of any witnesses.

- Notify the Rental Car Company: Report the incident to the rental car company as soon as possible. Follow their instructions and fill out their accident report form.

- Call the Benefits Administrator: You need to report the incident to the card’s benefits service right away. The number is on the back of your card or in your guide to benefits. You can also find it on the official Chase benefits website. They will open a claim for you and explain what documents you need to submit.

- Submit Your Paperwork Promptly: You will typically need to submit a completed claim form, the rental agreement, the police report, photos, and the final repair bill from the rental company. Be sure to meet the deadlines they give you, which is usually within 60 to 100 days of the incident.

Acting quickly and keeping organized records will help ensure your claim is processed smoothly and efficiently.

Frequently Asked Questions (FAQ)

1. Do I need to buy any insurance from the rental company at all?

You still need liability insurance. The United Explorer Card covers damage to your rental car, not damage you might cause to other people or their property. Your personal auto insurance policy often covers this. If you don’t own a car, you should consider purchasing the supplemental liability insurance (SLI) from the rental company.

2. Does the insurance cover international rentals?

Yes, the coverage is valid in most countries around the world. However, some countries like Israel, Ireland, and Jamaica are typically excluded. It’s always a good idea to call the number on the back of your card before your trip to confirm coverage for your specific destination.

3. What types of vehicles are not covered?

The policy does not cover expensive luxury cars (like Porsche or Lamborghini), antique vehicles, large vans that carry more than 9 people, trucks, RVs, motorcycles, or limousines. For most standard car, SUV, or minivan rentals, you will be covered.

4. Does it cover rentals from services like Turo or U-Haul?

No. The benefit generally applies to vehicles rented from commercial rental agencies. It does not cover car-sharing services like Turo or Zipcar, nor does it cover moving trucks like U-Haul or Penske.

5. Do I have to be flying on United Airlines to use this benefit?

No, not at all! You can use the car rental insurance benefit regardless of which airline you fly or even if you aren’t flying at all. As long as you follow the rules of declining the CDW and paying with your United Explorer Card, the benefit is active.

6. What if I use United miles to pay for part of the rental?

To be covered, the entire rental transaction must be charged to your United Explorer Card. If you use miles or points to cover the full cost, the benefit will not apply. If you pay for even a portion with points, it may void the coverage, so it is safest to charge the full amount to your card.

7. Does it cover other drivers?

Yes, as long as the additional driver is listed on the rental agreement, they are typically covered by the card’s insurance benefit. This is a great feature for trips with a spouse or friend.

Conclusion: Drive with Confidence

So, does the United Explorer Card cover rental car insurance? The answer is a resounding yes, and it does it exceptionally well. By providing primary coverage for collision and theft, it stands out as one of the best credit card benefits available for travelers.

Relying on this perk is a smart financial move. It saves you from paying for the rental company’s expensive daily waivers, protects your personal auto insurance policy from claims, and eliminates your deductible. It simplifies the rental process and allows you to drive with confidence, knowing you have a powerful layer of protection.

The next time you’re at that rental car counter, you can feel empowered. You know the rules: decline their CDW, pay with your United Explorer Card, and drive away knowing you’re covered. It’s one of the easiest ways to save money and reduce stress on your travels.