How to Buy Car Cash Without IRS: Genius, Essential

Buying a car with cash directly from a private seller or dealership is completely legitimate and doesn’t inherently involve the IRS, unless you’re dealing with significant undeclared income. Focus on secure payment methods and proper title transfer. This guide simplifies the process, ensuring a smooth, worry-free cash car purchase.

Dreaming of that new-to-you car? A cash purchase often seems like the simplest way to go. No loans, no monthly payments – just you and your new ride. But sometimes, the process can feel a bit foggy, especially when you hear whispers about regulations or the IRS. You might wonder, “How do I buy a car with cash and keep everything above board?” It’s a common question, and you’re in the right place! I’m here to demystify the whole process, from finding the right car to signing the paperwork. We’ll cover everything you need to know to make a smart, secure cash car purchase, completely stress-free. Let’s get you on the road with confidence!

Why Buy a Car with Cash?

Buying a car with cash offers a lot of appeal. It means you own the car outright from day one, free from the burden of interest payments and monthly loan installments. This can lead to significant savings over the life of the vehicle compared to financing. Plus, the transaction is often simpler and quicker than dealing with loan applications and approvals. For many, the peace of mind that comes with owning something free and clear is the biggest draw.

The Benefits of a Cash Car Purchase

- No Interest Charges: You avoid paying interest, which can add thousands of dollars to the total cost of a financed car.

- Immediate Ownership: The car is yours from the moment of purchase. There are no lender claims on the title.

- Simpler Transactions: The buying process can be more straightforward, especially when dealing with private sellers.

- Budget Control: You know exactly what the car will cost you upfront, making budgeting easier.

- No Monthly Payments: Free up your monthly budget for other expenses or savings goals.

Understanding the IRS and Cash Transactions

Let’s clear up a common misconception: the IRS isn’t concerned with your decision to buy a car with cash, as long as the funds used are from legitimate, declared sources. The IRS primarily tracks large cash transactions to prevent money laundering and tax evasion. For individuals, this typically involves reporting requirements if you are depositing or withdrawing very large sums of cash ($10,000 or more) from a financial institution. When you buy a car with cash, especially if the money is already in your possession or obtained through standard banking procedures (like withdrawing from your savings), the IRS is not directly involved in the car purchase itself.

The key is transparency with your own finances. If your income is declared and taxes are paid, using your lawfully obtained money to buy a car cash is perfectly fine. The “without IRS” part generally refers to avoiding unnecessary complications or scrutiny that could arise if a transaction were structured in a way that seemed unusual or lacked proper documentation of its source of funds. We’ll focus on keeping your transaction straightforward and well-documented.

For instance, if you sell a previous car and use that cash, or withdraw savings you’ve accumulated over time, these funds are generally considered “clean.” The IRS’s concern is with “unreported income” or “structuring” transactions to avoid reporting thresholds, which is not what you’re doing when you simply use your existing, declared funds to make a purchase.

Where to Find Cars for Cash Purchase

There are several avenues to explore when you’re looking to buy a car with cash. Each has its own set of pros and cons, and understanding them will help you find the best fit for your needs and budget.

Private Sellers

This is often where the best deals can be found. Private sellers are individuals looking to sell their personal vehicles. You’ll typically find them through online marketplaces, local classifieds, or even word-of-mouth.

- Pros: Often lower prices, more room for negotiation, direct interaction with the owner.

- Cons: Higher risk as typically sold “as-is” with no warranties, requires more due diligence from the buyer (inspections, title checks), payment needs to be handled very carefully.

Popular platforms include Craigslist, Facebook Marketplace, AutoTrader (which also lists private sellers), and eBay Motors. When searching, use terms like “cash only,” “private party sale,” or simply look for listings without financing mentions.

Dealerships

While dealerships are more accustomed to financing, they absolutely sell cars for cash. You might find cash deals on used car lots or even for new cars, though the savings might be less pronounced on new vehicles as dealerships often benefit from finance commissions.

- Pros: Often more reputable, potential for warranties or service plans, easier financing transfer if you change your mind last minute (though we’re focusing on cash!), more structured sales process.

- Cons: Prices may be higher than private sellers due to overhead, less negotiation room, additional fees (like dealer prep or documentation fees).

Approach a salesperson and clearly state your intention to pay cash. This can sometimes give you leverage for a small discount, though their primary motivation often lies in financing deals.

Online Auctions and Sales

Websites like eBay Motors, Bring a Trailer, or Cars & Bids specialize in online car sales and auctions. Many of these transactions involve cash or bank wire transfers for payment.

- Pros: Wide selection, competitive bidding can drive prices, unique vehicles often available.

- Cons: Can be harder to inspect the vehicle before purchase (especially auction sites), requires trust in the seller and platform, payment methods may be more complex (like wire transfers).

Always read the auction rules carefully regarding payment methods and buyer protections.

Step-by-Step Guide: How to Buy a Car with Cash

Ready to make your cash purchase? Follow these steps to ensure a smooth and secure transaction.

Step 1: Set Your Budget and Get Pre-Approved (if needed)

Even though you’re paying cash, it’s crucial to know exactly how much you can spend. This includes the car’s price plus taxes, registration fees, and potential immediate maintenance. If your cash is tied up in investments or you want to keep a reserve, you might still consider a small loan for part of it. A pre-approved loan gives you a firm spending limit.

Step 2: Research and Find Your Car

Determine the type of car you need or want. Research makes, models, common problems, and pricing using resources like Kelley Blue Book (KBB.com) or Edmunds (Edmunds.com) to get a realistic idea of market value. This research is vital whether buying from a private seller or a dealership.

Step 3: Inspect the Vehicle Thoroughly

This is arguably the most critical step, especially for private sales. Never skip this!

- Visual Inspection: Check for rust, dents, mismatched paint (indicating accident repair), tire wear, and the condition of the interior.

- Test Drive: Listen for strange noises, check how the engine starts, feel the transmission shifting, test the brakes, and ensure all electronics (AC, radio, windows) work.

- Pre-Purchase Inspection (PPI): Take the car to an independent mechanic you trust. For a small fee (usually $100-$200), they can identify potential issues you might miss. This is a non-negotiable step for peace of mind.

If the seller refuses a PPI, walk away. You can find reputable mechanics through online reviews or by asking friends for recommendations.

Step 4: Check the Vehicle History Report

A vehicle history report (like CARFAX or AutoCheck) can reveal accident history, title issues (salvage, flood, lemon), odometer discrepancies, and ownership history. While not foolproof, it’s an essential piece of the puzzle.

- You can often get a VIN from the seller online.

- Purchase a report for your chosen vehicle.

This can save you from buying a car with hidden problems.

Step 5: Negotiate the Price

Based on your research, the car’s condition, and the vehicle history report, you can negotiate the price. Be polite but firm. Reference any issues found during the inspection or any market data that supports your offer. Know your walk-away price.

Step 6: Prepare Your Cash Payment

Once you agree on a price, it’s time to prepare the funds.

- For Private Sales: It’s generally safest to meet at your bank. You can withdraw the exact amount in cash, and the bank can often provide a cashier’s check made out to the seller. This provides a traceable record of payment and comfort for both parties. Alternatively, if withdrawing cash, ensure you have it in a secure place. Avoid carrying large amounts of cash unnecessarily.

- For Dealerships: They will likely accept a cashier’s check from your bank or a wire transfer. Bringing a large amount of physical currency to a dealership is usually not preferred and may raise security concerns for them. Confirm their preferred payment methods in advance.

Step 7: Complete the Paperwork – The Title Transfer

This is where ownership officially changes hands. You’ll need the seller to sign over the vehicle’s title. Ensure the title is clear (no liens) and correctly filled out. Both you and the seller will likely need to sign and have your signatures notarized, depending on your state’s regulations.

- Bill of Sale: Always create a Bill of Sale. This document details the buyer, seller, vehicle information (VIN, make, model, year), sale price, and date. It serves as proof of the transaction. You can find templates online or ask your local Department of Motor Vehicles (DMV) or equivalent agency for a sample.

- DMV Visit: After the sale, you will need to go to your local DMV (or equivalent agency) to transfer the title into your name, pay applicable sales tax and fees, and register the vehicle. Bring the signed title, Bill of Sale, proof of insurance, and your identification.

You can check your state’s specific requirements on the USA.gov portal, which links to each state’s motor vehicle services.

Step 8: Insure and Register Your Car

Before you can legally drive your newly purchased car, you need to get it insured. Contact your insurance provider to add the car to your policy or start a new one. Then, take your proof of insurance and the completed title transfer documents to the DMV to register the vehicle and get your license plates.

Payment Methods and Security

When buying a car with cash, your primary concern should be the security of the transaction. Here are the most common and secure methods:

Cashier’s Check

A cashier’s check is drawn on the bank’s own funds rather than your personal account. This means the money is guaranteed. This is often the preferred method for both buyers and sellers in private transactions, especially if you meet at the bank.

Personal Check

Generally not recommended for large cash purchases. The seller risks the check “bouncing” if you don’t have sufficient funds, and it can delay the title transfer until the check clears.

Bank Wire Transfer

Commonly used for online purchases or when sending funds to a dealership. It’s fast and secure but can sometimes involve fees. Ensure you have verified the recipient’s details thoroughly.

Physical Cash

While straightforward, carrying large amounts of physical cash can be risky. If you do use cash, meet in a safe, public place, ideally at a bank. A bank can also verify the bills if there’s any concern about counterfeits, though this is rare.

Escrow Services

For high-value vehicles or online purchases, an escrow service acts as a neutral third party. You deposit the funds with them, the seller ships the car, and once you’ve inspected and approved it, the escrow service releases the funds to the seller.

Common Pitfalls to Avoid

Buying a car cash is usually straightforward, but being aware of potential issues can save you a lot of headaches.

- “As-Is” Sales: Most private sales are strictly “as-is.” This means once you buy it, repairs are your responsibility. This is why inspections are crucial.

- Title Issues: Always ensure the seller has a clear title in their name. A lien on the title means a bank or lender still has a claim on the car, and you can’t legally transfer ownership without resolving it.

- Odometer Fraud: Though less common with modern cars due to electronic odometers and reporting laws, always check history reports for discrepancies and be wary of suspiciously low mileage.

- Unsafe Meeting Locations: Never agree to meet a private seller in a secluded area. Always opt for a busy, well-lit public place, preferably a bank or police station parking lot.

- Pressure Tactics: If a seller is pressuring you to make a quick decision or buy without an inspection, it’s a major red flag.

Here’s a quick comparison table:

| Scenario | Key Considerations | IRS Relevance |

|---|---|---|

| Buying with cash from savings (declared income) | Secure payment (cashier’s check, bank wire), proper title transfer, bill of sale, DMV registration. | None, as funds are from legitimate, declared sources. |

| Selling your old car and using that cash for a new one | Ensure previous car sale is properly documented. Use funds for new purchase. | None, as long as previous sale income was declared. |

| Buying a car with cash from an undeclared source of income | This can raise red flags if audited. It’s best to declare all income. | High potential for issues, including penalties and investigation. |

| Structuring cash deposits/withdrawals (e.g., multiple small deposits to avoid $10k reporting) | This itself is illegal and can trigger IRS scrutiny. | Directly relevant; considered an illegal act. |

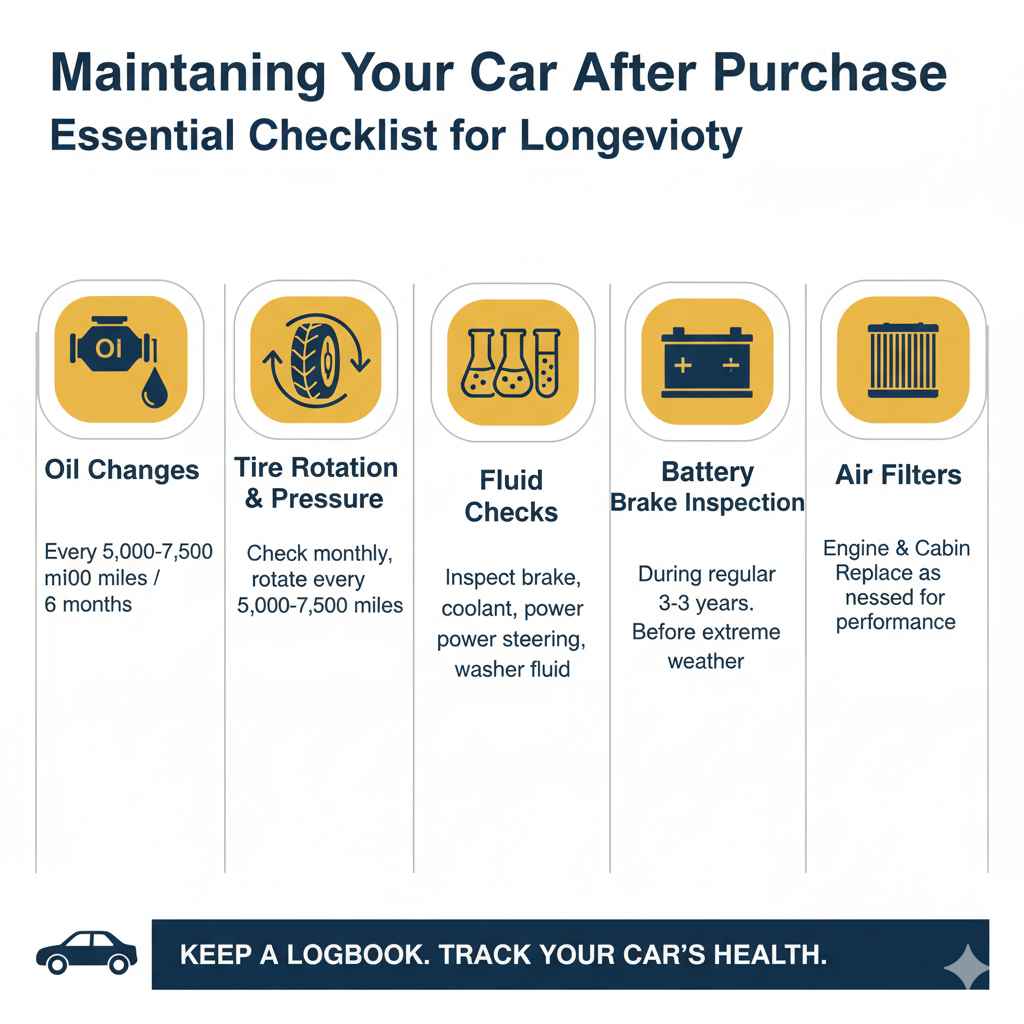

Maintaining Your Car after Purchase

Once you’ve got your cash-bought car, the journey isn’t over! Regular maintenance is key to keeping it reliable and preventing costly repairs down the line. Think of it like taking care of a new friend.

Essential Maintenance Checklist

- Oil Changes: Follow the manufacturer’s recommended interval, typically every 5,000-7,500 miles or every 6 months.

- Tire Rotation and Pressure: Check tire pressure monthly and rotate tires every 5,000-7,500 miles to ensure even wear and extend their life.

- Fluid Checks: Regularly inspect brake fluid, coolant, power steering fluid, and windshield washer fluid.

- Brake Inspection: Have your brakes checked during regular service appointments. Worn brake pads are a safety hazard.

- Battery Check: Car batteries typically last 3-5 years. Have yours tested, especially before extreme weather seasons.

- Air Filters: Engine air filters and cabin air filters should be checked and replaced as needed. A clean engine air filter improves performance and fuel efficiency.

Keeping a simple logbook of maintenance performed can also be helpful for tracking your car’s history and future needs.

Frequently Asked Questions

Q1: Do I need to tell the IRS I’m buying a car with cash?

No, you do not need to inform the IRS that you are buying a car with cash, provided the funds you are using are from legitimate, declared income. The IRS is not concerned with typical cash car purchases made with personal savings or legally earned money.

Q2: Can a dealership refuse my cash payment?

While rare, some dealerships might prefer financing. However, most will accept cash. If a dealership seems hesitant, clarify their policy or consider another dealer. They typically prefer cashier’s checks or wire transfers over large amounts of physical currency.

Q3: What’s the safest way to pay a private seller with cash?

The safest method is to meet at your bank. You can withdraw the money there and get a cashier’s check made out to the seller. This provides a secure record and comfort for both parties. If using physical cash, meet in a well-lit, public place, ideally with security like a bank or police station parking lot.