Is It Bad to Sell a Car You Just Bought? Essential Guide

Selling a car you just bought isn’t inherently “bad.” It’s a practical decision that can happen for many reasons. While there are financial considerations, understanding the process and potential impact can help you make the best choice for your situation.

Hey there, fellow drivers! Md Meraj here. Ever bought a car and then, a few weeks or months later, started wondering if it was the right fit? Maybe your needs changed, or you found a better deal. It’s a common thought: “Is it actually bad to sell a car I just bought?” The short answer is no, it’s not inherently bad. Life happens, and sometimes our car choices need a do-over. The good news is, understanding how and why this can happen is totally within reach. We’ll walk through why this situation pops up, what to consider before you sell, and how to navigate the process smoothly.

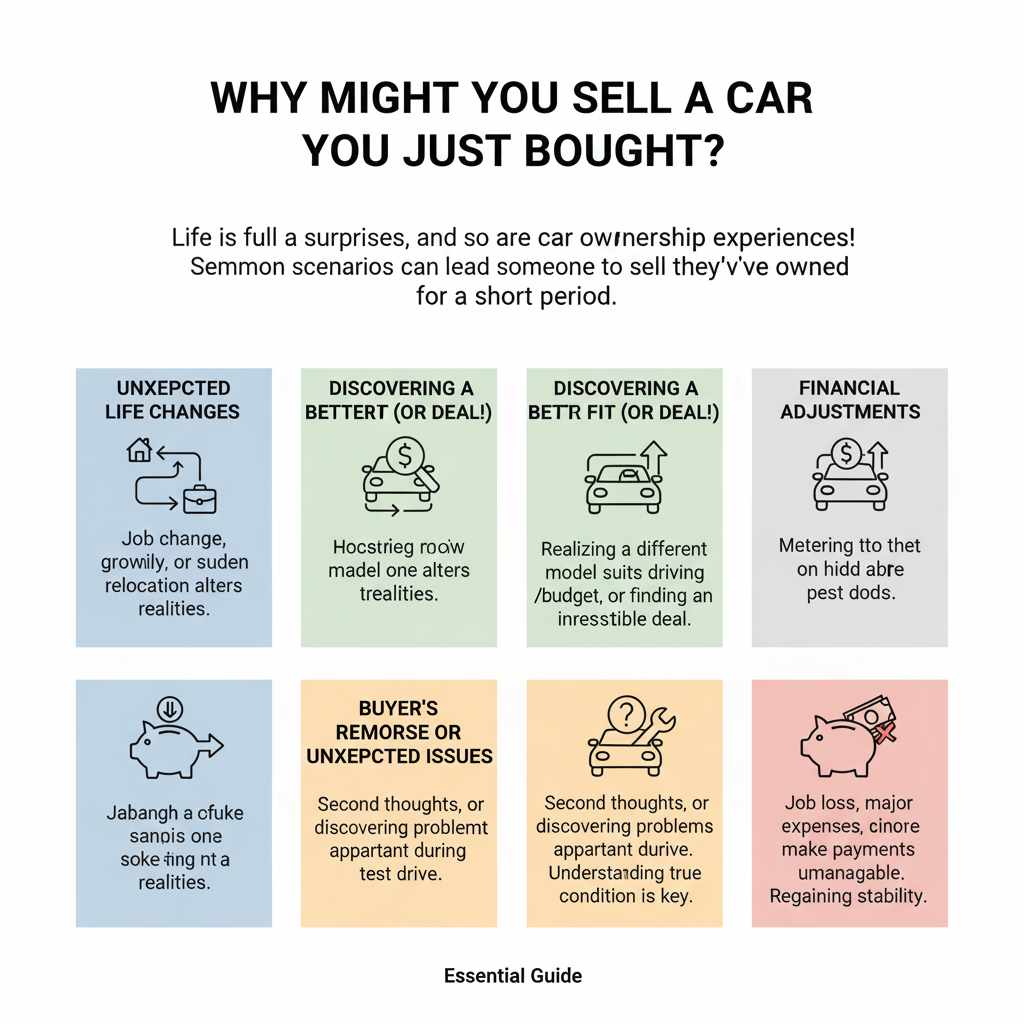

Why Might You Sell a Car You Just Bought?

It’s easy to think that once you sign on the dotted line, you’re stuck with your new ride forever. But life is full of surprises, and so are car ownership experiences! Several common scenarios can lead someone to consider selling a car they’ve owned for a short period.

Unexpected Life Changes

Things shift, and sometimes quite suddenly. Your job might change, requiring a longer commute that your current car just isn’t comfortable for. Maybe your family situation evolves, and you suddenly need more space than you initially anticipated. Even a sudden relocation can change your transportation needs dramatically. These aren’t poor decisions; they’re simply adapting to new realities.

Discovering a Better Fit (or Deal!)

Let’s be honest, the car buying process can be overwhelming. Sometimes, after you’ve had a car for a bit, you might realize it doesn’t quite suit your driving style, or you discover a different model that would have been a much better fit for your lifestyle and budget. It could also be that you spotted a fantastic deal on another vehicle that you simply couldn’t pass up, even if it means parting with your recent purchase.

Buyer’s Remorse or Unexpected Issues

It happens to the best of us. You drive off the lot, and a little voice in your head starts whispering, “Did I make the right choice?” This is classic buyer’s remorse. Sometimes, this feeling is amplified by discovering issues that weren’t apparent during the test drive or initial inspection. While dealerships often offer warranties, understanding the car’s true condition is key.

Financial Adjustments

Unexpected financial shifts are another major reason. A sudden job loss, an unforeseen major expense, or a change in income can make car payments feel unmanageable, no matter when you bought the vehicle. In such cases, selling the car might be a necessary step to regaining financial stability.

Before You Sell: Key Considerations

Thinking about selling a car you just bought? That’s perfectly okay! But before you jump into it, let’s pause and think through a few important things. Making a thoughtful decision now can save you headaches and money down the road.

Financial Impact: Depreciation is Real

The biggest thing to understand is depreciation. Cars lose value the moment they are driven off the lot, and they continue to lose value over time. If you’re selling a car that’s only a few weeks or months old, you’re likely going to sell it for less than you paid for it. This is largely due to the initial depreciation shock. You might have to accept a loss to sell it quickly.

To get a good idea of your car’s current value, you can check resources like Kelley Blue Book (KBB) or Edmunds. These sites use formulas that factor in your car’s make, model, year, mileage, condition, and features to give you an estimated selling price. Remember, these are estimates; your actual selling price will depend on the buyer and the negotiation.

Selling Options: Who Will Buy It?

You have a few main avenues for selling your car, each with its pros and cons:

- Trade-in at a Dealership: This is often the easiest route. You drive your old car in, and they give you credit towards your new one. However, it usually offers the lowest payout because dealerships need to make a profit when they resell it.

- Sell to an Online Car Buyer (e.g., Carvana, Vroom): These companies make selling convenient by handling pickup and paperwork. They often offer competitive prices, but it’s wise to get quotes from a few different online buyers to compare.

- Sell Privately: This generally yields the highest price, but it requires more effort. You’ll need to advertise your car, handle potential buyers (some of whom may be tire-kickers or low-ballers), arrange test drives, and manage all the paperwork yourself.

Your Loan Situation: What’s Owed?

Are you still paying off the car loan? This is a crucial point. If you owe more on the loan than the car is currently worth, you have what’s called being “upside down” or “underwater” on your loan. In this situation, when you sell the car, the sale price won’t cover the loan balance. You’ll have to pay the difference out of pocket to clear the loan, or you might be able to roll that negative equity into a loan for your next car (though this is generally not recommended as it increases your debt).

Understanding your loan balance is straightforward. Call your lender or check your online loan account. Compare this number to your car’s estimated selling price. This will tell you if you’ll have any remaining balance to pay.

The Contract You Signed: Any Restrictions?

When you bought the car, did you sign anything that might make selling it quickly difficult or costly? Most standard car purchase agreements don’t have strict clauses against selling, especially if you bought from a private seller or a dealership as a privately owned vehicle. However, if you financed through a specific program or there were special incentives involved, it’s worth a quick look at your paperwork or a call to the finance company to ensure there are no hidden catches.

Your Selling Options in Detail

Let’s dive a bit deeper into how you can sell your car, especially if it’s a recent purchase. Understanding these routes will help you choose the one that best fits your timeline, effort, and financial goals.

Option 1: Trading It In

Trading in your car at a dealership is often the path of least resistance. You can do this when buying a new car, or sometimes even just to sell without an immediate purchase. The dealership handles most of the work, and the transaction is usually quick.

- Pros: Convenient, fast, reduces hassle of selling. Can be a simple transaction when buying another car.

- Cons: Usually the lowest offer for your car because the dealership needs to profit from the resale.

When is it a good choice? If speed and convenience are your top priorities, and you don’t mind potentially taking a lower price for your car.

Option 2: Selling to Online Car Buyers

Companies like Carvana, Vroom, and Shift have revolutionized how we sell cars. You typically get an instant online offer, schedule a time for them to inspect and pick up the car, and receive payment shortly after. They aim for a smooth, digital experience.

- Pros: Very convenient, no need to meet with individual buyers, often a transparent online offer process.

- Cons: Offers can vary significantly between companies. You still might not get top dollar compared to a private sale.

When is it a good choice? When you want convenience and a streamlined process, and you’ve shopped around to ensure you’re getting a competitive offer amongst these services.

Option 3: Selling Privately

This involves selling directly to another individual. It requires more of your time and effort but usually results in the highest selling price. You’ll need to prepare the car, advertise it, screen buyers, and handle paperwork.

Steps for a Private Sale:

- Prepare Your Car: Clean it thoroughly inside and out. Fix any minor issues if the cost is low and the impact on sale price is high. Consider a pre-sale inspection for transparency.

- Determine the Asking Price: Research your car’s value using resources like KBB, Edmunds, and NADA Guides. Look at similar listings in your area for comparison.

- Create an Advertisement: Write a detailed description, including all key features, condition, mileage, and any recent maintenance. Take high-quality photos from all angles.

- List Your Car: Use online platforms like Facebook Marketplace, Craigslist, eBay Motors, or car-specific sites.

- Screen Buyers: Be cautious of initial contact. Ask questions to gauge genuine interest.

- Arrange Test Drives: Meet in a safe, public place. Consider having a friend with you. Make sure the potential buyer has a valid driver’s license.

- Negotiate the Price: Be prepared to negotiate. Know your lowest acceptable price beforehand.

- Complete the Paperwork: This typically involves signing over the title, completing a bill of sale, and removing your license plates. It’s crucial to follow your state’s specific procedures for transferring ownership. You can usually find this information on your state’s Department of Motor Vehicles (DMV) website. For example, the California DMV offers comprehensive guidance on selling a vehicle.

- Pros: Usually yields the highest sale price.

- Cons: Requires the most effort, time, and personal involvement. Potential safety concerns if not handled carefully.

When is it a good choice? If you have the time, patience, and are looking to maximize your return on investment.

Navigating the Paperwork & Legalities

Selling a car, no matter how recently you bought it, involves essential paperwork to ensure the transfer of ownership is legal and smooth. Not handling this correctly can lead to future problems, like tickets or tolls still being assigned to you.

The Title Transfer

The vehicle title is the legal document that proves ownership. When you sell your car, you’ll need to sign the title over to the new owner. If you purchased the car recently and it was financed, your lender might hold the title. You’ll need to pay off the loan to get the title released to you. If you bought the car outright, you should have the title in your possession already.

Bill of Sale

A bill of sale is a receipt that documents the transaction between the buyer and seller. It should include details like the vehicle’s VIN (Vehicle Identification Number), make, model, year, mileage, the sale price, and the names and addresses of both parties. While not always legally required in every state for title transfer, it’s highly recommended as proof of the sale for both parties. Many DMVs provide downloadable bill of sale forms.

Notifying Your State’s DMV

Crucially, after you’ve sold the car and transferred the title, you need to officially notify your state’s Department of Motor Vehicles (DMV) or equivalent agency. This is often done using a “Notice of Transfer and Release of Liability” form. This step is vital because it informs the state that you are no longer responsible for the vehicle. This protects you from liability for any parking tickets, toll violations, or accidents that occur after the sale date. Check your local DMV website for the exact procedure in your state.

Removing License Plates

In most states, license plates are tied to the owner, not the vehicle. When you sell a car, you generally need to remove your license plates and either transfer them to your next vehicle or return them to the DMV as required by state law. Failing to do this could mean the new owner drives around with your plates!

Common Pitfalls to Avoid

Selling a car you just bought can be a bit tricky, and there are a few common mistakes people make. Being aware of these can help you steer clear of trouble and make the process go more smoothly.

Not Getting an Accurate Value

This is a big one. If you’re guessing your car’s worth or not using reliable sources, you could either undersell it and lose money unnecessarily, or overprice it and struggle to find a buyer. Always do your research using multiple reputable guides.

Skipping the Pre-Sale Inspection or Maintenance

Even if you think your car is perfect, a potential buyer might be wary if it hasn’t been looked at recently. A pre-sale inspection by an independent mechanic can build trust. Small, inexpensive repairs or a good detail can make a big difference in perceived value.

Ignoring the Loan Balance

As mentioned, being “upside down” on your loan is a critical financial hurdle. If you don’t know your exact payoff amount and compare it to the car’s value, you might be in for a nasty surprise when you try to sell.

Rushing the Sale

Selling too quickly can lead to accepting a lower offer than you could have gotten. While you might be eager to move on, give yourself a reasonable amount of time to find the right buyer and get a fair price.

Failing to Complete Paperwork Properly

This ties back to the legalities. Incorrectly filled-out titles, lacking a bill of sale, or not notifying the DMV can lead to significant headaches, including lingering financial responsibility for the vehicle.

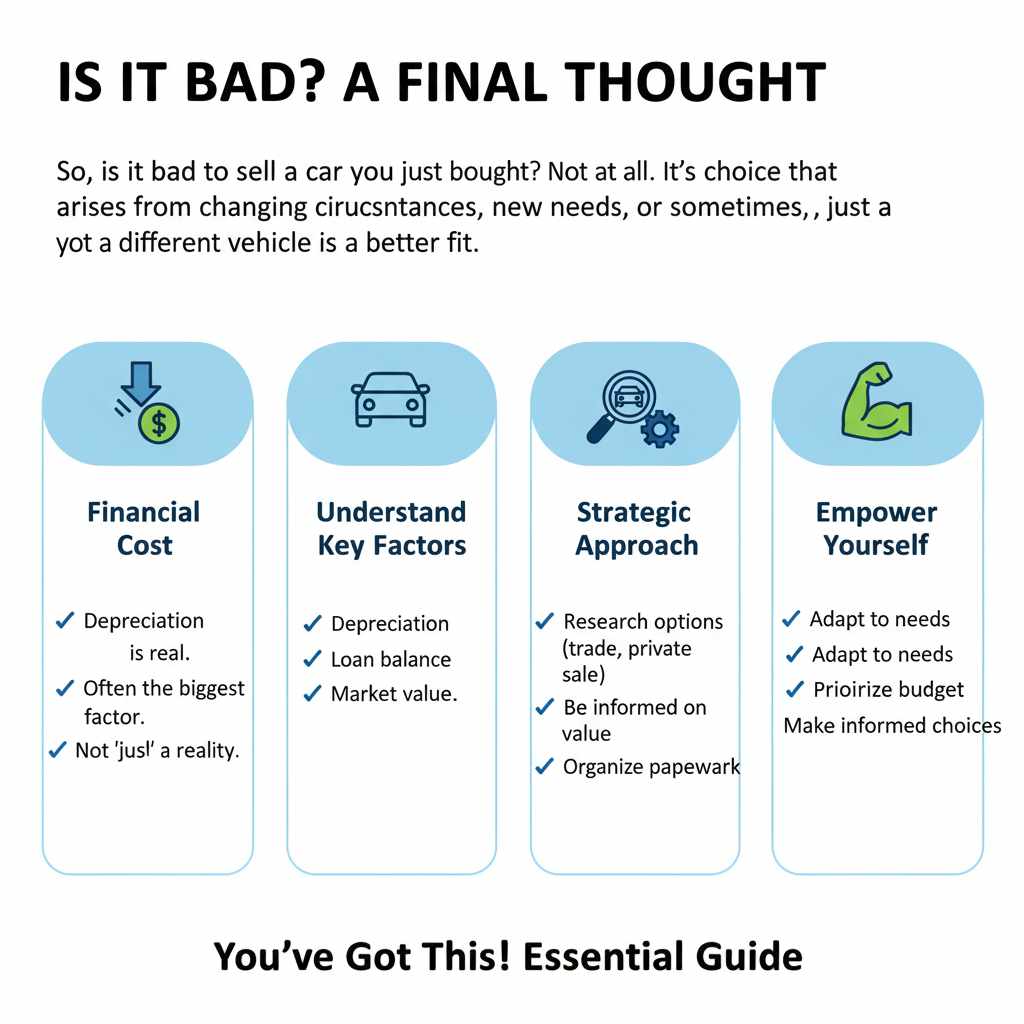

Is It Bad? A Final Thought

So, is it bad to sell a car you just bought? Not at all. It’s a choice that arises from changing circumstances, new needs, or sometimes, just a realization that a different vehicle is a better fit. While there’s often a financial cost due to depreciation, this doesn’t make the decision “bad.” It’s simply a factor to manage.

The key is to approach it with clear eyes. Understand the financial implications—especially depreciation and your loan balance. Research your selling options thoroughly, whether you choose convenience or the highest possible return. And most importantly, navigate the paperwork diligently to ensure a clean break from ownership.

By being informed and strategic, you can sell a car you recently purchased without undue stress or financial detriment. It’s about adapting and making the best decisions for your life and your budget. You’ve got this!

Frequently Asked Questions (FAQ)

Q1: Will I lose money selling a car I just bought?

A: Most likely, yes. Cars depreciate significantly the moment they are driven off the lot. Selling a car that is only a few weeks or months old means you’ll likely get less than you paid for it. This is a financial cost, but not necessarily a “bad” decision depending on your circumstances.

Q2: What if I owe more on my car loan than it’s worth?

A: This is called being “upside down” or “underwater.” When you sell the car, you’ll have to pay the difference between the loan balance and the sale price out of your own pocket to fully pay off the loan. You might be able to roll this negative equity into a new car loan, but this usually means higher monthly payments.

Q3: How soon after buying a car can I sell it?

A: There’s no legal waiting period in most places. You can technically sell a car the day after you buy it. However, the longer you keep it, the more depreciation occurs, and you’ll have more equity built up. Selling very soon after purchase will almost always result in a financial loss.

Q4: Is it better to trade it in or sell it privately if I just bought the car?

A: Selling privately usually gets you the most money, but it takes more effort. Trading it in is much more convenient but typically offers a lower price. For a car you just bought, the difference between trade-in and private sale value might be smaller than on an older car, so weigh convenience against how much money you’re willing to lose.

Q5: Can I sell a car that has a lien on it?

A: Yes, but it’s more complicated. You’ll need to pay off the loan (the lienholder) at the time of sale. Often, the buyer will pay the dealership or lender directly, or you’ll need to facilitate the payoff from the sale proceeds before the title can be transferred to the new owner. You cannot typically transfer ownership without first satisfying the lien.

Q6: What are the risks of selling a car privately?

A: Risks include dealing with unreliable buyers, negotiating with people who may try to scam you, and safety concerns during test drives. It’s crucial to meet in safe, public places, verify potential buyers, and handle all paperwork correctly to protect yourself legally.

Q7: Does selling a recently bought car affect my credit score?

A: Selling the car itself does not directly affect your credit score. However, if you sell it for much less than you owe and have to take out a new loan for the remaining balance (or have to pay a large sum out of pocket), how you manage that new debt or avoid defaulting could impact your score over time.