Is It Illegal To Put Money Down On A Car: Essential Guide

No, it is not illegal to put money down on a car. In fact, a down payment is a very common and often beneficial part of buying a vehicle. This guide clarifies what a down payment is, why it’s legal, and how it works in car purchases.

Buying a car is a big step! You’ve likely spent time researching models, thinking about features, and maybe even dreaming about that feeling of driving your new ride. One of the first financial steps you’ll encounter is the “down payment.” It’s totally normal to wonder about the rules and if there’s anything tricky involved. You might even ask yourself, “Is it illegal to put money down on a car?” Don’t worry, this is a common question, and the answer is a simple and reassuring “no.”

Putting money down on a car is not only legal but also a standard practice in the automotive and finance industries. It’s a way to show your commitment and reduce how much you need to borrow. In this guide, we’ll break down exactly what a down payment is, why it’s a smart move, and everything else you need to know to feel confident about your car purchase. Let’s clear up any confusion and get you ready for the road!

What Exactly is a Down Payment on a Car?

A down payment is simply the amount of money you pay upfront when you buy a car. Instead of financing the entire cost of the vehicle, you contribute a portion of the price in cash. The remaining balance is then what you’ll borrow from a lender, such as a bank, credit union, or the dealership’s financing department.

Think of it like this: if a car costs $20,000 and you decide to put down $4,000, you’ll only need to finance $16,000. The $4,000 is your down payment.

Why is Putting Money Down on a Car Legal?

There is absolutely nothing illegal about making a down payment on a car. In fact, it’s a fundamental part of the car buying process for millions of people every year. Here’s why it’s perfectly fine and widely accepted:

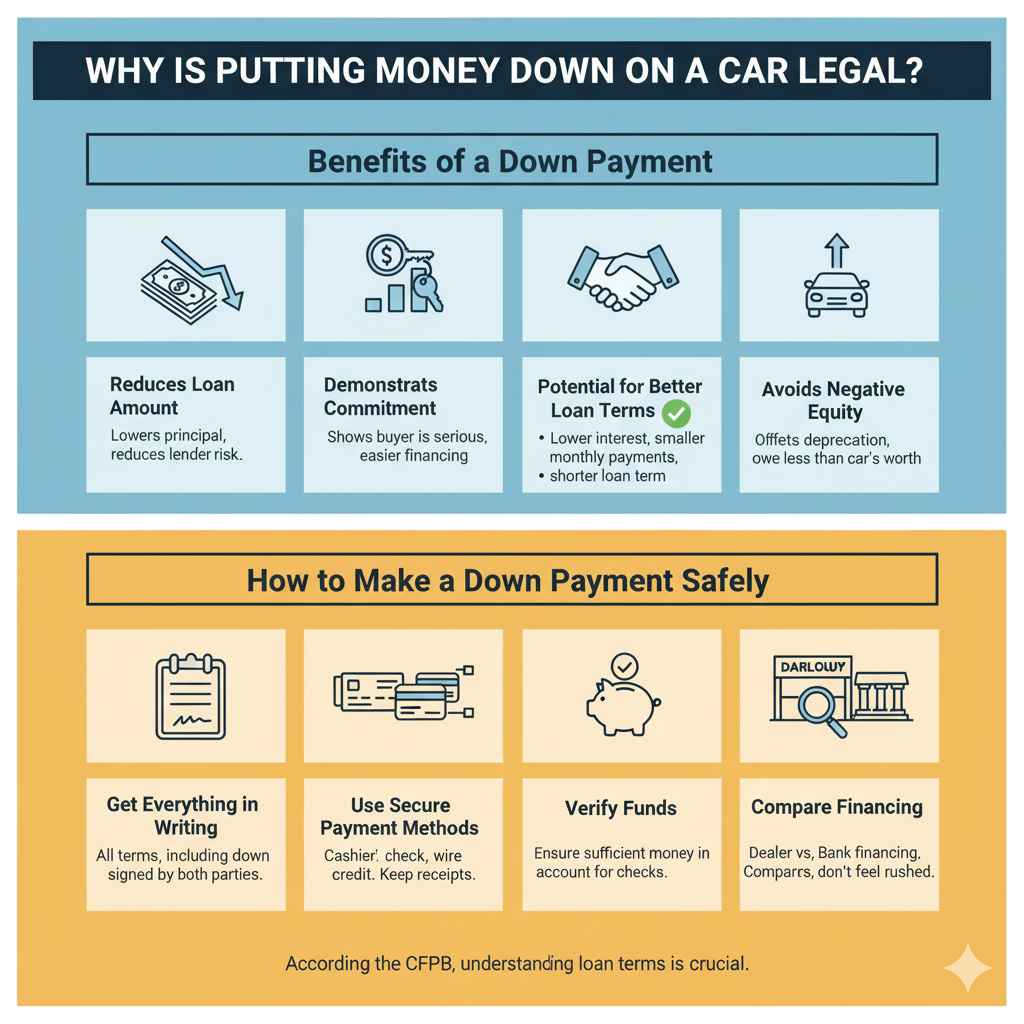

Reduces the Loan Amount

The primary purpose of a down payment is to lower the amount of money you need to borrow. Lenders are generally more comfortable offering loans when there’s a smaller principal amount involved. This reduces their risk.

Demonstrates Buyer Commitment

When you make a down payment, you’re showing the seller and the lender that you are serious about buying the car. This commitment can make it easier to secure financing and get better loan terms.

Potential for Better Loan Terms

Many lenders view a buyer with a down payment as less risky. This can translate into several benefits for you, including:

- Lower interest rates on your loan.

- Smaller monthly payments.

- A shorter loan term (meaning you pay it off faster).

Avoiding Negative Equity

New cars, in particular, depreciate (lose value) the moment they are driven off the lot. If you finance the entire car price without a down payment, there’s a chance you could owe more on your loan than the car is worth. This is called negative equity or being “upside down” on your loan. A down payment helps offset this initial depreciation, making it less likely you’ll end up in this situation.

According to the Consumer Financial Protection Bureau (CFPB), understanding your loan terms, including what you pay upfront, is crucial when borrowing money.

Building Equity Faster

Equity is the difference between your car’s current market value and the amount you owe on the loan. By making a down payment, you start with positive equity right away. This means you own a portion of the car’s value from day one.

How Does a Down Payment Actually Work?

The process of making a down payment is straightforward. Here’s a step-by-step look at how it typically happens:

1. Agree on the Car Price

First, you’ll negotiate the price of the car with the seller (dealership or private party). This is the agreed-upon purchase price before any taxes, fees, or financing are considered.

2. Determine Your Down Payment Amount

You’ll decide how much you want to pay upfront. This could be a few hundred dollars, a few thousand, or even a significant portion of the car’s price. There’s no universal rule for how much you must put down, but common amounts range from 5% to 20% of the car’s price.

3. Submit the Payment

When it’s time to finalize the purchase (often at the finance office if you’re at a dealership), you’ll provide your down payment. This can usually be done through:

- Cash

- Personal check

- Cashier’s check

- Debit card

- Credit card (though some dealerships may limit this due to fees)

- Trade-in vehicle (the value of your old car can sometimes act as a down payment)

4. Finance the Remaining Balance

After your down payment is accepted, the dealer or lender will calculate the remaining amount that needs to be financed. This balance, plus interest and fees, will be the basis for your car loan.

5. Sign the Loan and Purchase Agreements

You’ll then review and sign all the necessary paperwork, including the loan agreement, which will outline your interest rate, monthly payments, loan term, and other important details.

Factors Influencing Down Payment Requirements

While there’s no legal minimum down payment, lenders and dealerships might have their own requirements or recommendations based on several factors:

| Factor | Impact on Down Payment | Explanation |

|---|---|---|

| Credit Score | Higher score, lower requirement | A good credit score shows reliability, reducing lender risk and potentially allowing for a smaller down payment or even no down payment at all. A lower score might require a larger down payment to secure a loan. |

| Loan Type | New vs. Used car loans | Lenders may have different down payment expectations for new cars (which depreciate faster) versus used cars. |

| Lender Policies | Varies by institution | Each bank, credit union, or finance company has its own rules and risk tolerance regarding down payments. |

| Dealership Recommendations | Often suggest 10-20% | Dealerships might encourage down payments to secure better loan terms for you and to reduce their own risk if they are involved in the financing. |

| Vehicle Price | Higher price, potentially higher down payment | A larger purchase price often necessitates a more significant down payment to make the loan amount more manageable. |

Pros and Cons of Making a Down Payment

While generally beneficial, it’s good to consider both sides of making a down payment.

Pros of a Down Payment

- Lower Monthly Payments: By reducing the loan principal, your monthly payments will be smaller.

- Reduced Interest Paid: You’ll pay less interest over the life of the loan because the amount you’re borrowing is smaller.

- Better Loan Approval Chances: Lenders see you as lower risk, increasing your chances of loan approval, especially with less-than-perfect credit.

- Avoid Negative Equity: Helps prevent owing more than the car is worth, especially with new cars.

- Build Equity Faster: You start owning more of the car from the beginning.

- Potentially Lower Insurance Premiums: Some insurance companies may offer lower rates when there’s less financing involved.

Cons of a Down Payment

- Requires Upfront Cash: You need to have the funds readily available, which might be a challenge for some buyers.

- Less Cash for Other Needs: Tying up a large sum in a down payment leaves less money for emergencies or other immediate expenses.

- May Not Save Significantly on Interest: If you have a very high credit score and can qualify for a very low interest rate, the savings from a down payment on interest might be minimal.

What If I Can’t Make a Down Payment?

If you’re unable to make a down payment, it’s not the end of the road! Many people buy cars with “zero down.”

Zero-Down Car Loans

These loans finance 100% of the car’s purchase price. While they offer the immediate benefit of not needing cash upfront, they often come with:

- Higher Interest Rates: Lenders charge more because the risk is higher.

- Higher Monthly Payments: You’re financing the full amount, so your monthly payments will be larger.

- Increased Risk of Negative Equity: You’re more likely to owe more than the car is worth.

Having a strong credit score is usually essential to qualify for a zero-down loan. It’s also important to carefully review the terms, as outlined by resources like Experian, to ensure it’s the right choice for your financial situation.

Options for Buyers with Limited Cash:

- Improve Your Credit Score: Work on paying bills on time and reducing debt to boost your credit score. This can help you qualify for better loan terms in the future, potentially with a smaller down payment requirement.

- Save Up: Even a small amount saved can help. Consider setting a savings goal for a down payment.

- Look for Special Dealer Programs: Some dealerships occasionally offer special promotions for zero-down or low-down payment options, though it’s crucial to read the fine print.

- Consider a Less Expensive Car: If your budget is tight, a more affordable vehicle will require a smaller loan and potentially a smaller or no down payment.

Your Rights When Making a Down Payment

When you put money down on a car, you have rights and protections. Here are a few key points to keep in mind:

- Right to Information: You have the right to clear and understandable information about the purchase price, the loan terms, your down payment’s role, and any associated fees.

- Truth in Lending Act (TILA): This federal law requires lenders to disclose the true cost of borrowing money. This includes the Annual Percentage Rate (APR), finance charges, and the total amount you’ll repay. Your down payment affects these numbers.

- Right to a Cooling-Off Period (Rare): While not common for car purchases, some states have specific laws or dealership policies that might offer a very short window to back out, but this is usually for specific circumstances and not a standard right. Always clarify this with the dealership.

- Contract Review: Ensure all figures on contracts match what you agreed upon, especially the confirmed down payment amount.

The Federal Trade Commission (FTC) provides valuable information on vehicle sales and financing to help consumers make informed decisions and understand their rights.

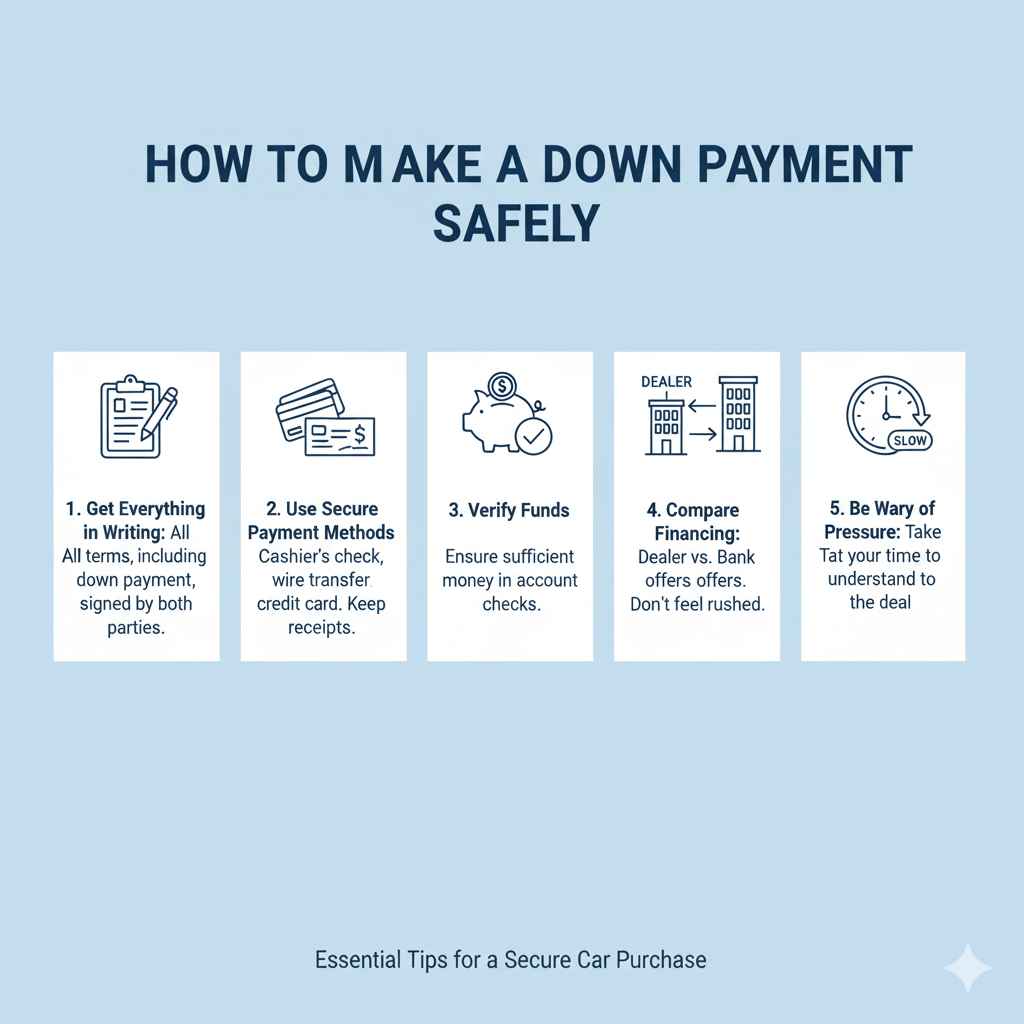

How to Make a Down Payment Safely

To ensure your transaction is as smooth and secure as possible, follow these tips:

- Get Everything in Writing: Before you hand over any money, ensure all agreed-upon terms, including the down payment amount, are written down and signed by both parties.

- Use Secure Payment Methods: Opt for methods that offer protection, like cashier’s checks or wire transfers for larger amounts, or credit cards if the dealership allows and you understand any associated fees. Keep receipts.

- Verify Funds: If you’re paying with a personal check, ensure you have sufficient funds in your account to cover it.

- Understand Dealer Financing vs. Bank Financing: Sometimes, a dealer might require a larger down payment if they’re arranging the financing internally, compared to if you secure a loan from your own bank or credit union beforehand. Compare offers!

- Be Wary of Pressure: Don’t feel rushed into making a down payment. Take your time to understand the deal.

Frequently Asked Questions About Car Down Payments

Is it illegal to put down more money upfront than I can afford?

No, it is not illegal to put down more money than you feel you can comfortably afford. However, it is financially unwise. You should always ensure you have sufficient funds remaining for other essential expenses and an emergency fund. Making a down payment should not strain your personal finances.

Can I use a personal loan as a down payment for a car?

Technically, yes, you can use funds from a personal loan to make a down payment on a car. However, this is generally not recommended. You would be taking on two loans (the personal loan and the car loan) simultaneously, increasing your monthly debt obligations and potentially leading to a higher overall interest cost.

What happens to my down payment if I can’t get approved for a car loan?

If you make a down payment and your loan application is subsequently denied, the down payment should be returned to you. This is usually stipulated in the purchase agreement. Always ensure this is clearly stated in writing before you make the payment. If the dealership refuses to return it, they may be acting illegally.

Are there any taxes or fees on down payments?

In most cases, the down payment itself is not taxed directly. However, many states charge sales tax on the entire purchase price of the vehicle, not just the financed amount. If this is the case, your down payment will reduce the total amount on which sales tax is calculated. Some dealerships might charge a small administrative fee for processing different payment types, but this should be disclosed upfront.

Can a dealership force me to make a down payment?

A dealership cannot legally force you to make a down payment if you wish to finance the entire vehicle. However, they can refuse to sell you the car or offer financing without one, especially if you have a lower credit score or are financing a new car. You always have the option to shop around for lenders who offer zero-down financing.

Is a down payment required for private car sales?

No, a down payment is not automatically required in private car sales. These transactions are more flexible and are typically negotiated directly between the buyer and seller. Often, private sales involve the full payment upfront, or the buyer and seller agree on payment terms without formal financing.