Can Dealerships Refuse Visa Payments In Canada Explained

Many people wonder, Can a Dealership Refuse a Visa Payment in Canada? Explained. This is a common question, especially when buying a car, because it can feel tricky to know your rights.

Don’t worry, it’s simpler than it sounds. We’ll walk you through it step by step so you understand everything clearly. Get ready to learn how this works so you can shop with confidence.

Understanding Payment Acceptance At Canadian Dealerships

This section explores the general rules and common practices regarding payment methods accepted by car dealerships in Canada. It will cover the legal framework, typical dealership policies, and the reasons behind their choices. Understanding these basics is the first step to knowing your rights and options when making a vehicle purchase.

We will look at why dealerships have specific rules about payments.

Legal Rights and Payment Options

In Canada, there isn’t a broad law that forces every business, including car dealerships, to accept all forms of payment like Visa. While Visa is a very popular payment method, businesses can set their own policies on what they accept. This is often because of the fees associated with processing credit card payments.

Dealerships have to pay fees to credit card companies for each transaction. These fees can be a significant cost, especially for large purchases like vehicles. Because of this, some dealerships may choose not to accept credit cards for the full price of a car.

They might, however, allow credit cards for smaller items like deposits or accessories.

- Payment Acceptance Policies: Dealerships decide what payment methods they will take. They are not legally required to accept Visa for the entire purchase price of a vehicle.

- Transaction Fees: Credit card companies charge fees to businesses for processing payments. These fees can be higher for larger amounts, making dealerships hesitant to accept Visa for big car sales.

- Dealership Discretion: Ultimately, it’s up to each dealership to decide their payment policies. They often weigh the benefits of customer convenience against the cost of transaction fees.

The choice to accept or decline certain payment methods is a business decision. Dealerships aim to manage their costs while serving their customers. This means some might accept Visa, some might not, and some might have specific rules about how it can be used.

The Role of Credit Card Companies

Visa, along with other credit card networks like Mastercard and American Express, acts as an intermediary between the buyer’s bank and the seller’s bank. When you use a Visa card, Visa facilitates the transaction by authorizing the payment and ensuring funds are available.

However, Visa also charges merchants, like car dealerships, a fee for every transaction processed. This is called a merchant fee or interchange fee. These fees are a percentage of the total sale amount and can add up quickly, especially for expensive items like vehicles.

For a car costing tens of thousands of dollars, these fees can represent hundreds or even thousands of dollars for the dealership.

Because of these substantial fees, many businesses have policies that limit the use of credit cards for large purchases. They might cap the amount that can be put on a credit card or opt out of accepting them altogether for vehicle sales. This is a standard business practice to control operational costs.

Common Dealership Practices

It is quite common for car dealerships in Canada to have specific policies about accepting Visa payments for vehicle purchases. Many dealerships will not allow a customer to pay the full price of a car using a Visa card.

Instead, they often prefer payment methods that do not incur significant transaction fees. These can include bank drafts, certified cheques, personal cheques (with prior approval), or direct bank transfers (e-transfers or wire transfers). These methods typically have lower or no processing fees for the dealership.

Some dealerships might offer a compromise. For example, they may permit a customer to use a Visa card for a portion of the purchase price, like a deposit or to cover a small part of the total. This can help with cash flow for the buyer while the dealership limits its exposure to high credit card fees.

- Limited Acceptance for Full Payment: Most dealerships will not let you pay the entire cost of a car with a Visa card due to merchant fees.

- Preferred Payment Methods: They usually prefer bank drafts, certified cheques, or wire transfers for larger sums.

- Partial Payment Options: Some may allow Visa for a deposit or a small percentage of the total cost.

These practices are not meant to be difficult but are a way for dealerships to manage their business costs effectively. It’s always a good idea to ask about their payment policies upfront before you finalize your car purchase.

Why Dealerships Might Decline Visa Payments

This section explains the specific reasons why a car dealership might choose not to accept Visa payments. The primary driver is the cost associated with credit card processing. We’ll break down these costs and how they impact a dealership’s bottom line, and explore other potential reasons for declining such payments.

Merchant Fees Explained

Merchant fees are charges that businesses pay to credit card companies, like Visa, for the service of processing customer payments. These fees are not a flat rate; they are typically a percentage of the transaction amount plus a small fixed fee.

For everyday purchases, these fees are usually manageable for most businesses. However, when it comes to high-value items like cars, these fees can become very substantial. For example, if a car costs $30,000 and the merchant fee is 2%, the dealership would have to pay $600 in fees for that single sale.

This cost directly impacts the dealership’s profit margin. They might have to absorb this cost, which reduces their earnings, or pass it on to the customer, which could make the car seem more expensive than advertised. To avoid this, many dealerships set limits or decline Visa for large purchases.

The exact percentage of merchant fees can vary based on several factors. This includes the type of business, the volume of sales, the specific credit card network, and the agreement negotiated between the merchant and the payment processor. Dealerships, especially those with high sales volumes, might negotiate slightly lower rates, but the fees remain significant for large transactions.

Impact on Profit Margins

Profit margins in the automotive industry can be tight. Dealerships have many overhead costs, including staff salaries, building maintenance, inventory management, and advertising. The cost of processing credit card payments eats directly into these already slim margins.

Imagine a dealership selling a car with a profit of $1,000. If they accept Visa and incur a $600 merchant fee on that sale, their actual profit is reduced to $400. This makes a significant difference to their overall profitability and ability to operate.

By declining Visa for full vehicle payments, dealerships can protect their profit margins. This allows them to remain competitive and continue offering good prices on vehicles. It’s a strategic business decision to ensure financial health.

Alternative Payment Methods And Why They Are Preferred

Dealerships often prefer payment methods like bank drafts, certified cheques, and wire transfers for a few key reasons. Firstly, these methods usually have no or very low processing fees for the dealership. This means the full amount paid by the customer goes towards the vehicle sale, preserving the dealership’s profit margin.

Secondly, these methods are generally considered more secure and final. Once a bank draft or certified cheque is issued, the funds are guaranteed. Wire transfers are also direct and secure.

This reduces the risk of payment disputes or chargebacks, which can be a concern with credit cards.

E-transfers can also be used for smaller amounts, and while they do have some processing by the banks, they are generally less costly than credit card fees. Allowing these payment types helps dealerships manage their cash flow and minimize financial risks associated with large transactions.

- No or Low Fees: Methods like bank drafts and wire transfers don’t cost the dealership money to process.

- Guaranteed Funds: These payments are secure and the funds are confirmed.

- Reduced Risk: Dealerships avoid potential chargebacks that can happen with credit cards.

By guiding customers towards these preferred methods, dealerships can ensure a smoother and more financially sound transaction for both parties involved.

Risk of Chargebacks

One significant concern for businesses accepting credit card payments is the risk of chargebacks. A chargeback occurs when a cardholder disputes a transaction with their bank, requesting that the charge be reversed. This can happen for various reasons, such as suspected fraud, dissatisfaction with the product or service, or an unauthorized transaction.

When a chargeback is initiated, the credit card company investigates the claim. If the dispute is found in favor of the cardholder, the merchant not only loses the sale amount but also often incurs additional fees related to the chargeback process. For high-value items like cars, a chargeback can result in a substantial financial loss for the dealership.

This risk is a major factor that influences a dealership’s decision on whether to accept credit cards for the full purchase price of a vehicle. By limiting or declining Visa payments for large transactions, dealerships can significantly reduce their exposure to the unpredictable and potentially costly nature of chargebacks.

Can A Dealership Refuse A Visa Payment In Canada Explained In Practice

This section will discuss real-world scenarios and how the policies on Visa payments play out at Canadian car dealerships. We will look at what you can expect when you try to use your Visa and how to handle different situations. This practical advice will help you be prepared.

Scenario One A Customer Wants To Pay In Full With Visa

Imagine Sarah walks into a dealership ready to buy a new car priced at $35,000. She plans to pay the full amount using her Visa credit card to earn travel rewards points. She informs the sales associate of her intention.

The sales associate, following dealership policy, politely explains that they do not accept Visa for the full purchase price of vehicles. They mention that the merchant fees associated with such a large transaction are too high for the dealership to absorb. Instead, they offer Sarah alternative payment methods:

- A bank draft or certified cheque for the full $35,000.

- A wire transfer directly from her bank.

- They might also suggest using her Visa for a smaller portion, perhaps a deposit of up to $5,000, with the remaining balance paid via one of the preferred methods.

Sarah understands the dealership’s position and decides to arrange for a bank draft to complete her purchase. She appreciates being informed upfront about the payment options.

Scenario Two A Customer Wants To Use Visa For A Deposit

David is looking to buy a car and finds one he loves at a dealership. The total price is $40,000. He asks if he can put down a deposit of $2,000 using his Visa card to secure the vehicle while he arranges his financing for the rest.

In this situation, the dealership is likely to agree. A $2,000 deposit is a much smaller amount compared to the total vehicle price. The merchant fees associated with this deposit are manageable for the dealership.

They see the value in securing the sale and accommodating the customer’s request for convenience.

So, David successfully uses his Visa card for the $2,000 deposit. He then proceeds to pay the remaining $38,000 balance using a certified cheque as per the dealership’s policy for larger amounts. This is a common compromise that works well for both parties.

Negotiating Payment Terms

While dealerships have policies, there can sometimes be room for negotiation, especially for larger purchases. If a dealership generally doesn’t accept Visa for full payment, you could try to discuss options.

For instance, you could ask if they would accept Visa for a significant portion, perhaps 10-20% of the vehicle’s price, if you commit to paying the rest via a method with lower fees. You might also inquire if they have any special promotions or partnerships with credit card companies that might allow for payment under certain conditions.

Be prepared to explain why you prefer to use your Visa. If it’s for loyalty points or rewards, the dealership might not be swayed. However, if you have a strong credit history and can offer assurances about the remaining funds, they might consider it.

It’s always worth having a polite conversation with the sales manager.

- Ask About Specific Limits: Find out if they accept Visa for any portion of the sale and what the maximum is.

- Propose a Combination: Suggest paying a percentage with Visa and the rest with a bank draft or wire.

- Understand Their Position: Be respectful of their business needs and cost considerations.

Remember that their willingness to negotiate will depend on various factors, including your relationship with the dealership, the specific vehicle, and current sales targets.

What To Do If Your Visa Payment Is Refused

If a dealership refuses your Visa payment, don’t be surprised or upset. As we’ve discussed, it’s a common business practice. Your best course of action is to be prepared with alternative payment methods.

Before you even go to the dealership, find out their payment policies. You can call ahead or ask the salesperson as soon as you start discussing numbers. This way, you won’t be caught off guard.

Have your bank’s information ready. Know how to arrange for a bank draft, certified cheque, or how to initiate a wire transfer. If you plan to use your bank’s bill payment system for an e-transfer, make sure you know the dealership’s details and any daily limits.

By being proactive and informed, you can ensure a smooth transaction, regardless of the payment method. The goal is to buy the car, and being flexible with payment will help you achieve that.

Understanding The Visa Payment Process In Canada

This section clarifies how Visa payments work in Canada, from the consumer’s perspective to the dealership’s perspective. We will break down the technical aspects of a Visa transaction and the associated costs, helping you understand the entire system.

How A Visa Transaction Works

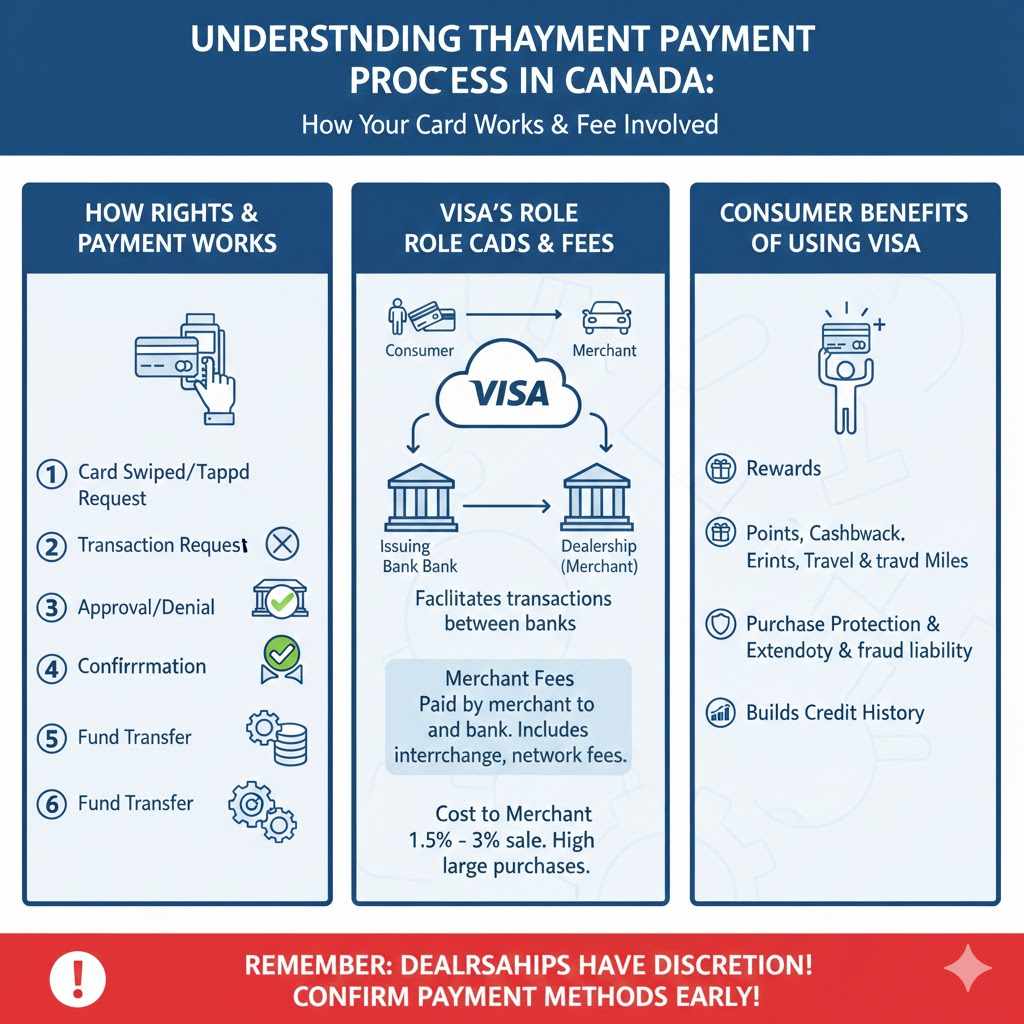

When you use your Visa card at a dealership, a series of events happens very quickly. First, the dealership’s point-of-sale (POS) terminal or online system sends your card information securely to Visa’s network.

Visa then communicates with your issuing bank (the bank that gave you the Visa card) to verify your identity and check if you have enough available credit for the purchase. If approved, Visa sends an authorization back to the dealership’s system.

This whole process typically takes just a few seconds. Once authorized, the sale is completed. The funds are then transferred from your bank, through Visa, to the dealership’s bank account.

This transfer of funds involves various fees paid by the merchant.

- Card Swiped/Tapped: You present your Visa card to the merchant’s payment terminal.

- Authorization Request: The terminal sends a request to Visa’s network.

- Bank Verification: Visa contacts your bank to confirm credit availability and legitimacy.

- Approval/Denial: Your bank approves or denies the transaction.

- Confirmation: Visa sends the authorization status back to the merchant.

- Fund Transfer: Once approved, funds are moved from your bank to the merchant’s bank.

The speed and security of this system are what make Visa such a popular payment method for consumers worldwide.

Visa’s Role And Fees

Visa itself is not a bank and does not issue cards or hold accounts. Instead, it operates the payment network that facilitates transactions between consumers, merchants, and financial institutions. Visa makes money by charging fees to the financial institutions that issue Visa cards and to the banks that provide merchant services.

For merchants, the fees they pay are not directly to Visa in most cases. Instead, they pay their acquiring bank (the bank that provides them with the ability to accept card payments). The acquiring bank then pays fees to Visa and the card networks for using their infrastructure.

These fees are what are commonly referred to as merchant fees. They include interchange fees (paid to the cardholder’s bank), network fees (paid to Visa/Mastercard), and processor markups. The total percentage a merchant pays can range from 1.5% to over 3% or even higher for certain types of transactions or businesses.

Consumer Benefits Of Using Visa

Using a Visa card for purchases, when accepted, offers several benefits to consumers. One of the most attractive benefits is the ability to earn rewards. Many Visa cards offer points, cashback, or travel miles on every purchase, which can add up to significant savings or perks over time.

Visa also provides purchase protection and extended warranty benefits on eligible items, which can offer peace of mind. Furthermore, Visa’s fraud protection is very strong. If your card is used fraudulently, you are typically not liable for unauthorized charges.

Using a Visa can also help build your credit history. Responsible use and timely payments can improve your credit score, which is important for future loans, mortgages, and other financial products. While dealerships may decline Visa for full vehicle purchases, these benefits make it a preferred payment method for many consumers for other transactions.

Frequently Asked Questions

Question: Can a dealership legally refuse to accept my Visa payment in Canada

Answer: Yes, a dealership can legally refuse to accept your Visa payment for a vehicle purchase in Canada. There is no law that requires businesses to accept all forms of payment, and dealerships can set their own payment policies.

Question: What are the main reasons dealerships decline Visa payments

Answer: The primary reason is the merchant fees charged by Visa, which can be substantial on large purchases like vehicles, impacting the dealership’s profit margin. They also aim to reduce the risk of chargebacks.

Question: Can I use my Visa for a car deposit

Answer: Many dealerships will allow you to use Visa for a deposit, as the amount is much smaller and the associated merchant fees are more manageable for them.

Question: What payment methods do dealerships prefer for car purchases

Answer: Dealerships often prefer payment methods like bank drafts, certified cheques, wire transfers, or e-transfers, as these typically have lower or no processing fees.

Question: What should I do if a dealership refuses my Visa payment

Answer: Be prepared with alternative payment methods like bank drafts or certified cheques. It is also advisable to inquire about the dealership’s payment policies beforehand.

Wrap Up

So, can a dealership refuse a Visa payment in Canada? Yes, they can. This is usually due to merchant fees that cut into profits.

They often prefer bank drafts or certified cheques. You can usually use Visa for a deposit, though.