Do You Need Car Insurance To Drive Off The Lot: Essential Guide

Yes, you absolutely need car insurance before driving your new car off the dealership lot. In nearly all states, driving without at least minimum liability insurance is illegal and can lead to significant fines, license suspension, and even vehicle impoundment. This guide will walk you through why it’s essential and what you need to know.

Hey there! Buying a new car is an incredibly exciting moment, and the thought of that first drive home is pure joy. But before you turn that key and imagine cruising down the road, there’s a crucial step that absolutely cannot be skipped: car insurance. Many folks wonder, “Do you really need car insurance to drive off the lot?” The short answer is a resounding yes! It’s one of those requirements that feels like a hurdle, but it’s there to protect you and others. Don’t worry, we’ll break down exactly why it’s so important and what you need to have squared away before you even think about leaving the dealership. Stick around, and we’ll make sure you head home with peace of mind and in compliance with the law.

Why Driving Off the Lot Without Insurance is a Huge No-No

Let’s get straight to the point: driving a vehicle without insurance is illegal in almost every single state in the U.S. Think of car insurance as your essential safety net. It’s not just about avoiding trouble; it’s about being prepared for the unexpected, which in the world of driving, can happen in an instant.

Legal Requirements: It’s the Law!

Every state, with the exception of New Hampshire, requires drivers to carry a minimum amount of car insurance. This is known as financial responsibility. The core idea is that if you cause an accident, you have the means to pay for the damages and injuries you cause. The laws are in place to protect not only you but also other drivers, passengers, and pedestrians.

Liability Coverage: This is the fundamental requirement in most states. It covers damages to other people and their property if you are at fault in an accident. It typically includes:

Bodily Injury Liability: Covers medical expenses, lost wages, and pain and suffering for those injured in an accident you cause.

Property Damage Liability: Covers the cost of repairing or replacing property that you damage in an accident, such as other vehicles, fences, or buildings.

The specific minimum liability limits vary by state. For instance, a state might require 25/50/25 coverage, which translates to $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage per accident. You can find your state’s specific minimums on government websites. For example, the National Association of Insurance Commissioners (NAIC) offers a wealth of information on auto insurance for new drivers.

Driving without meeting these minimums can lead to severe penalties.

Penalties for Driving Uninsured

The consequences of getting caught driving without insurance can be tough, and they often start the moment you’re pulled over.

Fines: You’ll likely face significant fines. These can range from a few hundred dollars for a first offense to several thousand dollars for subsequent offenses.

License Suspension or Revocation: Your driver’s license could be suspended for a period, or even permanently revoked.

Vehicle Impoundment: The police may seize your vehicle, and you’ll have to pay towing and storage fees to get it back.

SR-22 Requirement: In many cases, you’ll be required to file an SR-22 form. This is a certificate of financial responsibility that proves you have the necessary insurance coverage. It’s typically required for a set period and can lead to higher insurance premiums.

Inability to Recover Damages: If you cause an accident while uninsured, you might not be able to recover damages for your own vehicle or injuries from the other party, even if they were partially at fault.

Securing Insurance BEFORE You Pick Up Your Car

This is perhaps the most crucial point: you need to have insurance before you drive your new car off the dealership’s property. Many dealerships will not let you take possession of a vehicle without proof of insurance. It’s a standard part of their sales process, and for good reason.

How to Get Insured on a New Car

The good news is that getting insurance for a new car is usually straightforward. Here’s how you can approach it:

1. Shop Around and Get Quotes: Before you even finalize your purchase, start getting insurance quotes. Do this a few days or even a week before you plan to pick up your car. You can do this online, over the phone, or by visiting an insurance agent.

2. Gather Necessary Information: When you get quotes, you’ll need information about yourself, any other drivers in your household, and details about the vehicle you’re buying (make, model, year, VIN).

3. Understand Coverage Options: Beyond the state minimums, consider what other types of coverage might be beneficial for a new car. We’ll dive into this more later.

4. Inform Your Insurer: Once you’ve decided on a car, call your insurance company or agent to inform them. They will need the details of the new vehicle to add it to your policy or start a new one.

5. Receive Proof of Insurance: Your insurance provider will give you proof of insurance, which might be an insurance card or a policy document. You’ll need to have this available when you pick up your car.

What Happens at the Dealership

Dealerships have a legal and ethical obligation to ensure their vehicles are driven off the lot legally. This means they will ask for proof of insurance.

Verification: The sales team will verify your insurance information. This might involve a quick phone call to your agent or a look at a digital copy of your insurance card.

If You Don’t Have It: If you don’t have insurance ready, the dealership will likely not let you drive the car away. They might offer to help you secure a policy through their affiliated insurance providers, but you are not obligated to use them. You can always arrange your own insurance.

Adding a New Car to an Existing Policy: If you already own a car and have insurance, you can usually add the new vehicle to your existing policy. Most policies have a grace period (e.g., 10–30 days) during which your new car is covered automatically, but it’s crucial to officially update your policy as soon as possible to avoid gaps in coverage or incorrect premium assessments.

Understanding Your Insurance Policy: What You Need

When buying a new car, it’s the perfect time to ensure you have adequate coverage. While states mandate minimum liability, these often aren’t enough to fully protect you, especially with a brand-new vehicle.

Essential Coverage Types for a New Car

Here’s a breakdown of commonly available coverage types and why they’re important, especially for a new vehicle.

| Coverage Type | What It Covers | Why It’s Important for a New Car |

|---|---|---|

| Liability Coverage (Bodily Injury & Property Damage) | Damages and injuries you cause to others in an at-fault accident. | Mandatory in almost all states. Protects you from financially devastating lawsuits if you injure someone or damage their property. |

| Collision Coverage | Damage to your car resulting from a collision with another vehicle or object (like a tree or guardrail), regardless of who is at fault. | Crucial for new cars. If you crash your new car, this pays for its repair or replacement (minus your deductible). Deals with those “oops” moments. |

| Comprehensive Coverage | Damage to your car from non-collision events like theft, vandalism, fire, flood, falling objects, or hitting an animal. | Highly recommended for new cars. Protects your investment against a wide range of unexpected events that aren’t accidents. |

| Uninsured/Underinsured Motorist (UM/UIM) Coverage | Covers your medical expenses and sometimes vehicle damage if you’re hit by a driver who has no insurance or not enough insurance to cover your costs. | Invaluable. Protects you when the other driver is at fault but can’t pay for the damages they caused. |

| Medical Payments (MedPay) or Personal Injury Protection (PIP) | Covers medical expenses for you and your passengers, regardless of fault. PIP may also cover lost wages and other related expenses. (PIP is mandatory in “no-fault” states). | Provides immediate financial help for medical care after an accident, easing the burden while fault is determined. |

Optional but Recommended Coverages for New Cars

Gap Insurance: This is particularly important for new cars, especially if you financed or leased your vehicle. If your car is totaled, your collision or comprehensive coverage will pay out its current market value. With a new car, this value depreciates quickly, and you might owe more on your loan than the car is worth. Gap insurance covers the difference, or “gap,” between what your insurance pays and what you still owe.

Roadside Assistance: If you break down or need a tow, this coverage can be a lifesaver. It typically covers services like towing, battery jump-starts, tire changes, and lockout assistance.

Rental Car Reimbursement: If your car is being repaired after a covered incident, this coverage helps pay for a rental car so you can still get around.

How to Choose the Right Insurance for Your New Car

Selecting an insurance policy can feel overwhelming, but it doesn’t have to be. A little research can go a long way in finding coverage that fits your needs and budget.

Factors Influencing Your Premium

Your car insurance premium is the amount you pay to the insurance company. Several factors influence this cost:

Your Driving Record: Accidents, tickets, and DUIs will increase your rates. A clean record usually means lower premiums.

Your Location: Where you live and park your car can affect rates due to factors like traffic density, crime rates, and weather patterns.

The Type of Car: More expensive, high-performance, or high-theft-risk vehicles typically cost more to insure.

Your Coverage Levels: The more coverage you choose, and the higher your limits, the more it will cost.

Your Deductible: This is the amount you pay out-of-pocket before your insurance kicks in for collision and comprehensive claims. A higher deductible usually means a lower premium, but remember you’ll pay more if you have a claim.

Your Credit Score: In many states, your credit-based insurance score is used to help determine your premium.

Your Age and Gender: Younger, less experienced drivers and males historically pay more.

Annual Mileage: How much you drive can impact your premium.

Tips for Getting the Best Rate

Bundle Policies: If you own a home or have other insurance needs, bundling your auto insurance with your homeowners or renters insurance can often lead to discounts.

Ask About Discounts: Insurers offer a variety of discounts, such as for good students, safe drivers, low mileage, anti-theft devices, and being a member of certain organizations. Always ask your provider what discounts are available.

Increase Your Deductible (Wisely): If you have a healthy emergency fund, consider a higher deductible for collision and comprehensive coverage. This can significantly lower your premium. Just make sure you can comfortably afford to pay the deductible if needed.

Maintain a Good Driving Record: The best way to keep your rates low is to drive safely and obey traffic laws.

Shop Around Annually: Don’t just set it and forget it. Re-evaluate your insurance needs and shop for quotes from different companies at least once a year or when you experience a life event (like moving or adding a driver).

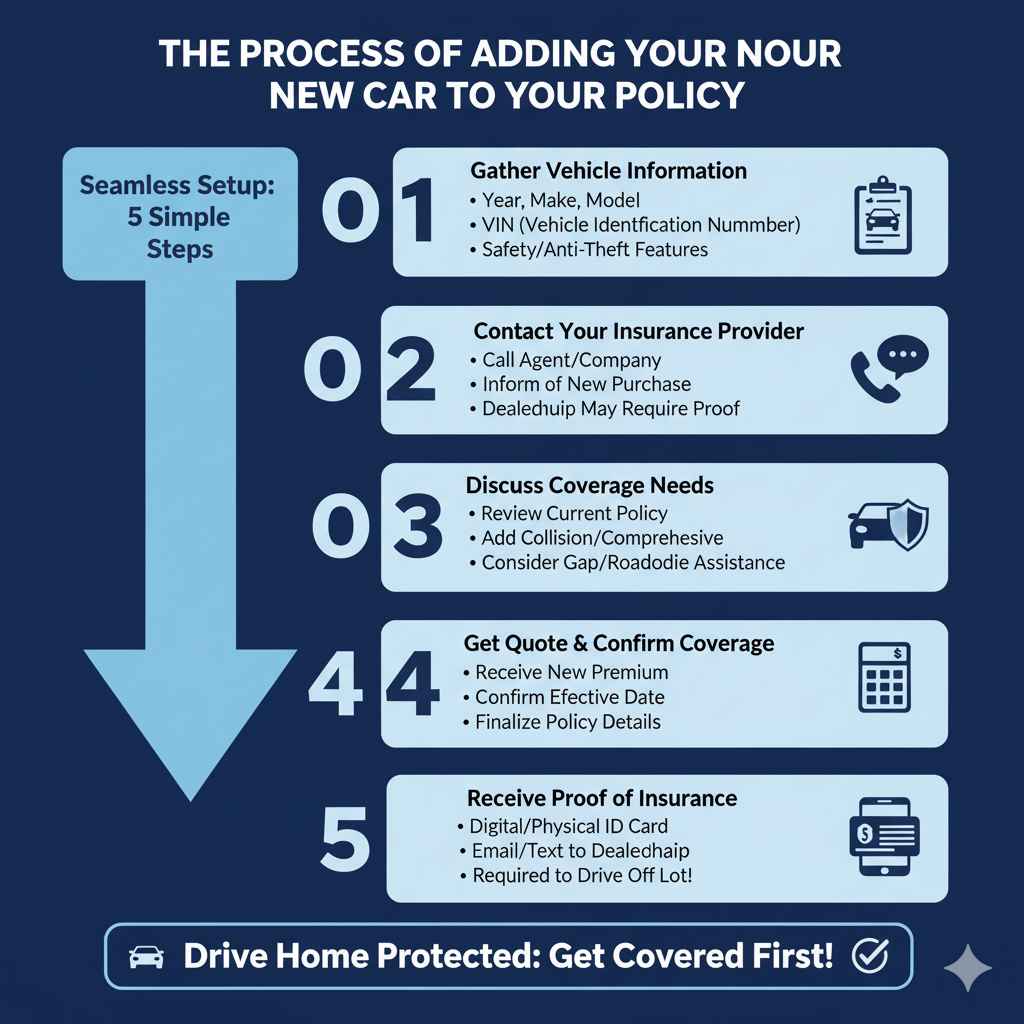

The Process of Adding Your New Car to Your Policy

So, you’ve picked out the perfect car, and you’re ready to drive it home. Here’s a step-by-step look at how to make sure your new wheels are covered:

-

Gather Vehicle Information: Before you call your insurance agent or company, have the following details ready for your new car:

- Year, Make, and Model

- Vehicle Identification Number (VIN)

- Any safety features or anti-theft devices.

- Contact Your Insurance Provider: Call your current insurance company or agent. Explain that you are purchasing a new vehicle and need to add it to your policy. If you are buying from a dealership, they will likely require proof of insurance before you can take possession of the car.

- Discuss Coverage Needs: Review your current coverage. Do you need to add collision and comprehensive coverage for your new car, especially if it’s financed or leased? Discuss options like gap insurance or roadside assistance if they are relevant to your situation.

- Get a Quote and Confirm Coverage: Your insurer will provide a quote for adding the new vehicle. This may adjust your premium. If you accept the new coverage, confirm the effective date and coverage details.

- Receive Proof of Insurance: Your insurance provider will send you an updated insurance card or policy documents. This is what you’ll need to show the dealership. Many insurers can send this digitally to your phone or email immediately.

- Inform the Dealership: Present your proof of insurance to the dealership’s finance or sales department. Once they verify it, you’ll be good to go!

Common Questions About Driving Off the Lot

Q1: Can I legally drive my new car off the lot without insurance?

A1: No, in nearly all states, it is illegal to drive any vehicle, new or used, without at least the state’s minimum required liability insurance. Dealerships will also require proof of insurance before letting you drive a vehicle off their lot.

Q2: What if I buy my car on a Saturday and my insurance agent doesn’t work weekends?

A2: Most insurance companies have 24/7 customer service lines or online portals that allow you to add a vehicle and get proof of insurance outside of regular business hours. It’s best to have your insurance company’s contact information for such situations readily available.

Q3: My dealership offered me insurance. Should I take it?

A3: You can, but it’s always wise to compare their offer with quotes from other insurance providers before agreeing. Sometimes dealership-offered insurance can be more expensive or offer less comprehensive coverage than what you could find elsewhere. You are not obligated to buy insurance from the dealership.

Q4: How much does car insurance cost for a new car?

A4: The cost varies significantly based on the vehicle, your location, your driving history, coverage choices, and the insurance company. For a new car, you can expect slightly higher premiums than for an older vehicle, particularly if you opt for comprehensive and collision coverage. Shopping around is key to finding the best rate.

Q5: Do I need full coverage for a new car loan?

A5: Yes, if you have a loan or lease on your new car, the lender or leasing company will almost certainly require you to carry full coverage, which includes collision and comprehensive insurance, in addition to liability. This protects their financial interest in the vehicle.

Q6: How long do I have to get insurance for a car I just bought?

A6: You need insurance before* you drive the car off the lot. If you are adding a car to an existing policy, there are usually grace periods (often 10-30 days) where the new car is automatically covered, but you must formally update your policy to ensure continuous coverage. Don’t risk being uninsured.

Q7: What is the “grace period” for car insurance when buying a new car?

A7: If you have an existing auto insurance policy, many companies offer a grace period (typically 10-30 days) during which a newly purchased vehicle is automatically covered under your existing liability, collision, and comprehensive coverage. However, you MUST notify your insurer promptly to make the coverage official and avoid potential issues or inaccurate coverage. It’s not a substitute for immediate notification.

Conclusion: Drive Away with Confidence and Protection

Navigating the process of buying a new car can be exciting, and ensuring you have the right car insurance in place before you drive it off the lot is a critical step. It’s not just a legal formality; it’s your shield against financial hardship and a guardian of your peace of mind.

Remember, “Do you need car insurance to drive off the lot?” is a question with a straightforward, non-negotiable answer: Yes, you do. By understanding the legal requirements, exploring your coverage options, and taking the time to shop around for the best rates, you can secure the protection you need.

Don’t let the insurance aspect diminish the joy of your new vehicle. With the right preparation, you can drive away from the dealership knowing you’re covered, confident in your decision, and ready to enjoy every mile ahead. Safe travels!