Does Car Insurance Cover Natural Disasters? Full Guide

Figuring out if your car insurance helps when a storm hits can be tricky for beginners. Many people wonder, Does Car Insurance Cover Natural Disasters? Full Guide, and it seems complicated.

But don’t worry, we’ll make it super simple. We’ll walk you through everything step-by-step so you know exactly what to expect. Get ready to find out what your policy covers.

What Does Car Insurance Cover for Natural Disasters

This section breaks down the types of car insurance that are key to understanding natural disaster coverage. It’s important to know that not all policies are the same. Some cover specific types of damage, while others offer broader protection.

We’ll explain the differences so you can make informed choices.

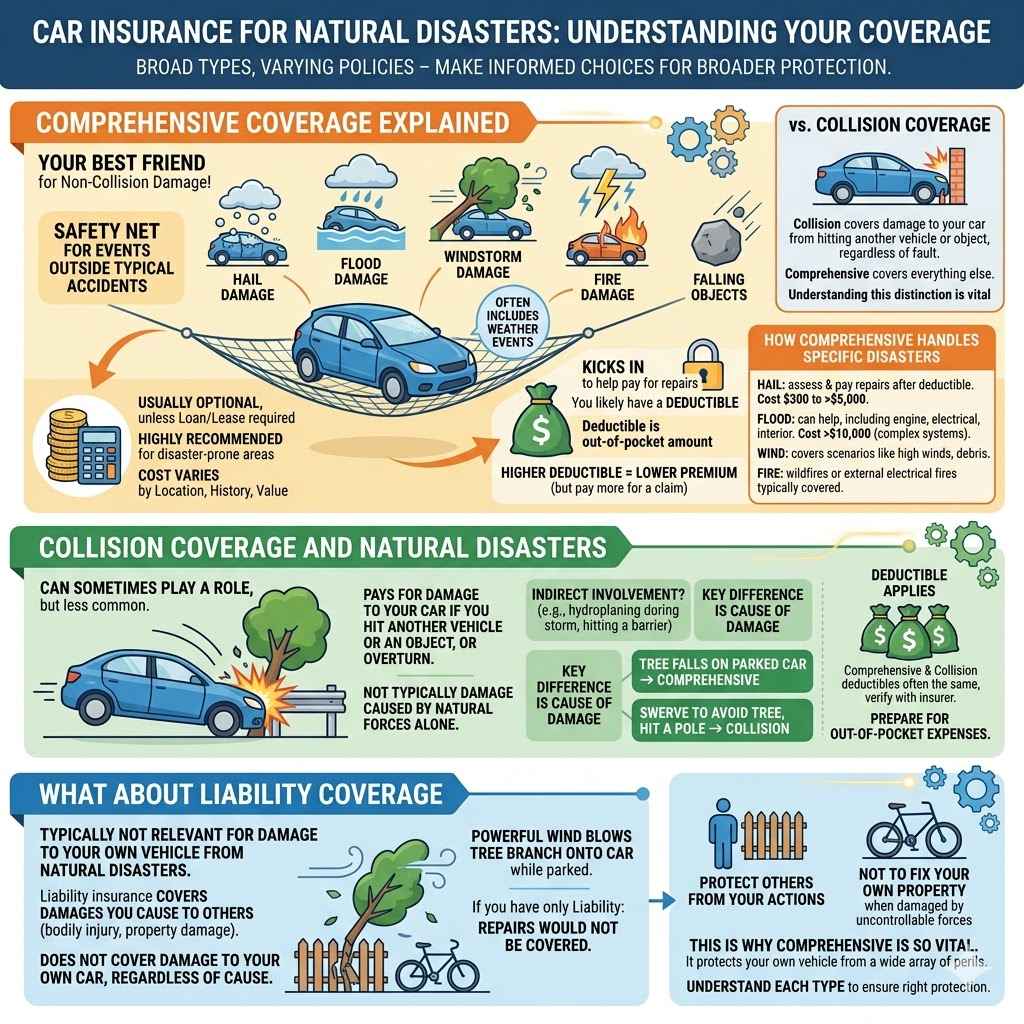

Comprehensive Coverage Explained

Comprehensive coverage is your best friend when it comes to non-collision damage, including many natural disasters. Think of it as a safety net for events outside of a typical car accident. It typically covers things like theft, vandalism, fire, and falling objects.

Most importantly for our topic, it often includes damage from weather events like hail, floods, and windstorms.

This type of coverage is usually optional unless you have a car loan or lease. Lenders want to protect their investment, so they require it. Even if it’s optional, it’s highly recommended for drivers living in areas prone to severe weather.

The cost can vary depending on your location, driving history, and the value of your car.

When a natural disaster occurs, your comprehensive coverage kicks in to help pay for repairs. You will likely have a deductible, which is the amount you pay out-of-pocket before your insurance starts paying. This deductible can range from a few hundred dollars to over a thousand dollars.

Choosing a higher deductible often means a lower premium, but you’ll pay more if you need to file a claim.

Many people confuse comprehensive with collision coverage. Collision covers damage to your car from hitting another vehicle or object, regardless of fault. Comprehensive covers everything else.

Understanding this distinction is vital when assessing your protection against natural events.

How Comprehensive Handles Specific Disasters

- Hail Damage: When hailstones batter your vehicle, causing dents and broken glass, comprehensive coverage usually steps in. The insurance company will assess the damage and pay for repairs after you meet your deductible.

- Flood Damage: If your car is submerged in floodwaters, comprehensive coverage can help. This includes damage to the engine, electrical systems, and interior. It’s crucial to understand that flood damage can be extensive and very costly to repair.

- Windstorm Damage: High winds can cause significant damage, from knocking down trees onto your car to blowing debris that strikes your vehicle. Comprehensive coverage is designed to cover these scenarios.

- Fire Damage: Wildfires or electrical fires originating from external causes are typically covered under comprehensive. This ensures that even if the fire wasn’t a direct result of a collision, your car can be repaired or replaced.

The average cost of hail damage repairs can range from $300 to over $5,000, depending on the severity of the dents. For flood damage, repairs can easily exceed $10,000 due to the complex electrical and mechanical systems involved. This highlights the importance of having adequate comprehensive coverage in disaster-prone regions.

Collision Coverage and Natural Disasters

While comprehensive coverage handles most weather-related damage, collision coverage can sometimes play a role, though it’s less common. Collision coverage pays for damage to your car if you hit another vehicle or an object, or if your car overturns. It does not typically cover damage caused by natural forces alone.

However, there are situations where collision might be involved indirectly. For instance, if you are driving during a severe storm and lose control of your car due to hydroplaning, hitting a ditch or a barrier, the resulting damage might be considered under collision coverage. This is because your vehicle made contact with an object.

The key difference lies in the cause of the damage. If a tree falls on your parked car during a storm, it’s comprehensive. If you swerve to avoid a falling tree and hit a pole, it’s collision.

It’s essential to review your policy to understand precisely how these two types of coverage interact with different scenarios.

Deductibles also apply to collision coverage. If your claim falls under collision, you will pay your collision deductible. Often, comprehensive and collision deductibles are the same, but it’s always best to verify this with your insurer.

This ensures you’re prepared for out-of-pocket expenses.

What About Liability Coverage

Liability coverage is typically not relevant for damage to your own vehicle from natural disasters. Liability insurance covers damages you cause to others, including bodily injury and property damage, if you are found at fault in an accident. It does not cover damage to your own car, regardless of the cause.

For example, if a powerful wind blows a tree branch onto your car while it’s parked, and you have only liability coverage, the repairs would not be covered. Your liability insurance is designed to protect others from your actions, not to fix your own property when it’s damaged by forces beyond anyone’s control.

This is why comprehensive coverage is so vital. It’s the part of your policy that protects your own vehicle from a wide array of perils, including natural disasters that are not caused by a collision. Understanding the purpose of each coverage type is crucial for ensuring you have the right protection in place.

Common Natural Disasters and Insurance Impact

Different natural disasters affect cars in unique ways, and how your insurance responds can depend on the specific event. We’ll explore how common events like floods, hurricanes, and wildfires impact your vehicle and what your policy likely covers.

Flood Damage and Your Car

Flooding is one of the most devastating natural disasters for vehicles. When a car is submerged, water can infiltrate every part of the vehicle, from the engine and transmission to the complex electronic systems and the interior. The damage can be so severe that it often renders the car irreparable or unsafe to drive.

Comprehensive coverage is what typically covers flood damage. If your car is damaged by rising waters from a river, hurricane surge, or even a severe localized flash flood, your comprehensive policy will pay for the repairs, minus your deductible. However, if you drove your car into floodwaters intentionally, insurance companies may deny the claim.

It’s important to understand that even if a car is repaired after flood damage, it may have lingering issues. Electrical problems can surface months later. For this reason, many flood-damaged vehicles are declared a total loss by insurance companies.

This means they will pay out the actual cash value of the car before it was damaged.

Real-life Example: Sarah lived in Texas and experienced a major hurricane. Her car was parked in her garage, but floodwaters rose rapidly, submerging the vehicle up to its windows. The engine, most of the electronics, and the interior were ruined.

Her comprehensive insurance covered the loss, paying her the actual cash value of the car after she paid her $500 deductible.

The Federal Emergency Management Agency (FEMA) reports that flood damage is a leading cause of vehicle loss in the United States. Insurers paid out over $10 billion in flood-related auto claims in a single decade, underscoring the significant risk.

Water Damage Scenarios

- Submerged Vehicle: If your car is completely underwater, the damage will be extensive. Comprehensive coverage is your primary recourse.

- Standing Water on Roads: Driving through deep standing water can cause engine damage (hydro-locking) if water enters the air intake. This is usually covered by comprehensive.

- Damage from Storm Surge: Coastal areas hit by hurricanes can experience significant storm surges that flood streets and vehicles. This falls under comprehensive.

- Leaking Roof or Sunroof: If heavy rain or leaks cause interior damage while parked, this is also a scenario where comprehensive coverage might apply.

Hurricane Damage

Hurricanes bring a combination of threats to vehicles, including high winds, heavy rain, flooding, and flying debris. The damage can be catastrophic, affecting cars in numerous ways. Understanding how your insurance policy handles these multifaceted events is crucial.

Comprehensive coverage is designed to handle most hurricane-related damages. This includes damage from wind, rain, and hail. If a tree falls on your car due to high winds, or if flooding occurs, your comprehensive policy will be the one to rely on.

However, there’s a critical distinction with flood damage caused by hurricanes. While comprehensive covers it, policies might have specific exclusions or higher deductibles for named storms or floods in certain areas. It’s always best to check your policy documents and speak with your insurance agent to confirm the exact details of your coverage.

When a hurricane is imminent, insurers often implement a “wind and hail” or “named storm” exclusion period, meaning they won’t cover damage that occurs after a certain date if a storm has been named. This is why it’s essential to have your comprehensive coverage in place well before hurricane season.

Scenario: A car is parked outside during a hurricane. A large tree limb breaks off due to high winds and crashes onto the roof and windshield. This damage would be covered under the car’s comprehensive insurance.

If the car was also caught in storm surge flooding, that water damage would also be covered by comprehensive.

Hail Damage

Hailstorms can occur suddenly and cause significant damage to a car’s exterior, particularly the roof, hood, trunk, and side panels. Dents and chipped paint are common. In severe cases, windows can also be broken.

Comprehensive coverage is the part of your auto insurance policy that typically pays for hail damage. Your insurer will assess the severity of the dents and determine whether to repair them or declare the car a total loss, depending on the extent of the damage and the car’s value.

The deductible for hail damage is usually your comprehensive deductible. Some states have a separate “comprehensive deductible” for specific perils like hail, which might be lower than your standard comprehensive deductible. This varies by policy and location.

It’s wise to check your policy for these specifics.

Many car owners opt for paintless dent repair (PDR) for hail damage. PDR is a method that repairs dents without disturbing the paint. It’s often faster and cheaper than traditional body shop repairs and may even be covered by your comprehensive policy with no deductible in some cases, though this is not standard.

Statistics show that hail is responsible for billions of dollars in auto insurance claims annually. In some regions, like Colorado, hail damage is so common that it significantly impacts insurance premiums.

Wildfire Damage

Wildfires pose a direct threat to vehicles, especially in regions prone to them. Cars can be damaged by flames, smoke, and ash. The heat from a wildfire can warp metal, melt plastic components, and crack glass.

Comprehensive coverage generally covers damage from wildfires. If your car is directly impacted by flames or damaged by extreme heat and smoke from a wildfire, your comprehensive policy will help pay for repairs or replacement, subject to your deductible.

Smoke damage can be insidious. Even if your car isn’t directly burned, smoke and ash can penetrate the ventilation system and interior, causing lingering odors and potential damage to sensitive components. Comprehensive coverage usually extends to these types of damages as well.

In situations where a wildfire forces evacuations, it’s crucial to try and protect your vehicle if possible, such as parking it in a garage or moving it to a safer location if time permits. However, if the wildfire occurs suddenly, comprehensive coverage is your primary protection.

Case Study: During a large wildfire in California, a family evacuated their home and car. While their home was destroyed, their car, parked a short distance away, survived the initial flames but was covered in thick ash and soot. The heat had warped some exterior plastic parts.

Their comprehensive insurance paid for a thorough detailing and the replacement of the damaged plastic components.

Making an Insurance Claim for Natural Disaster Damage

When your car is damaged by a natural disaster, filing an insurance claim is your next step. It’s important to follow a clear process to ensure everything goes smoothly. This involves documenting the damage and working with your insurance company.

When to File a Claim

You should file a claim as soon as it is safe to do so after the natural disaster has passed. The sooner you report the damage, the faster the claims process can begin. Most insurance companies have a timeframe within which claims must be reported, so don’t delay.

If your car is not drivable, you’ll need to arrange for it to be towed to a safe location or a repair shop. Contact your insurance company to understand your options for towing and temporary storage. They can guide you on the best course of action.

It’s also wise to consider the potential impact on your insurance premium. While you shouldn’t avoid filing a legitimate claim, if the damage is minor and your deductible is high, you might choose to pay for the repairs yourself. However, for significant damages caused by natural disasters, filing a claim is almost always necessary.

Documenting the Damage

Thorough documentation is critical for a successful insurance claim. Before attempting any cleaning or repairs, take clear photos and videos of the damage from various angles. Capture as much detail as possible, including the overall condition of the vehicle and close-ups of specific damages.

Keep records of everything related to the event. This includes dates and times of the disaster, any evacuation orders, receipts for temporary repairs or towing, and communications with your insurance company. This detailed record-keeping will be invaluable throughout the claims process.

If possible, make a list of all the damaged parts or areas of your car. This will help you communicate effectively with the insurance adjuster. The more information you can provide upfront, the smoother and quicker the claims process is likely to be.

Sample Scenario: After a flood, you find your car’s interior soaked and the engine making strange noises. Before starting the car, take pictures of the water line on the exterior and interior. Document any visible damage to upholstery, electronics, and the engine bay.

Then, have it towed and note the tow truck’s company and arrival time.

What to Include in Your Documentation

- Photos of Exterior Damage: Capture dents, broken windows, damaged paint, and any other visible issues.

- Photos of Interior Damage: Document water levels, mold growth, damaged upholstery, and electronic controls.

- Photos of Engine Bay: If safe to do so, take pictures of any visible water or debris in the engine compartment.

- Video Walkthrough: A short video showing the general condition of the car and highlighting key damaged areas can be very helpful.

- Receipts for Emergency Services: Keep records of any towing, temporary storage, or emergency repair costs.

Working with the Insurance Adjuster

Once you’ve filed a claim, an insurance adjuster will be assigned to assess the damage to your vehicle. This person works for the insurance company and their role is to evaluate the extent of the damage and determine the cost of repairs or replacement based on your policy.

Be present and prepared when the adjuster inspects your car. Point out all the damage you’ve documented. Ask questions if anything is unclear.

It’s your right to understand their assessment and the basis for their findings.

If you disagree with the adjuster’s assessment, you have the right to get a second opinion from an independent appraiser or a trusted mechanic. Your insurance policy may have provisions for arbitration or appraisal if you cannot reach an agreement. Don’t hesitate to advocate for yourself.

Remember that the adjuster’s job is to assess the damage based on your policy. Having all your documentation ready will help them do their job accurately and efficiently. This collaboration can lead to a fair settlement.

Total Loss vs. Repair

If the cost to repair your car after a natural disaster exceeds a certain percentage of its actual cash value (ACV), the insurance company will likely declare it a total loss. The ACV is the market value of your car just before it was damaged. Each state has specific regulations regarding when a vehicle is deemed a total loss.

When a car is declared a total loss, the insurance company will pay you the ACV of your vehicle, minus your deductible. You will then surrender the totaled car to the insurance company. They will typically sell it for salvage.

This can be a difficult outcome, but it ensures you receive fair market value for your vehicle.

If the car is deemed repairable, the insurance company will pay for the repairs, up to the cost of its ACV, minus your deductible. They will often work with a preferred repair shop, but you usually have the option to choose your own mechanic. Always ask about this option.

It’s important to understand that even if a car is repaired, its value may be affected. Some people prefer to replace a car that has been significantly damaged by a natural disaster, even if it’s repaired. Your insurance payout for a total loss is based on the ACV, not the cost of a new car, so be prepared for that difference.

Statistic: In the aftermath of major hurricanes, the number of vehicles declared total losses can be in the hundreds of thousands. For instance, Hurricane Harvey in 2017 resulted in over 300,000 vehicle insurance claims, with a significant portion declared total losses.

Tips for Choosing Car Insurance and Staying Protected

Choosing the right car insurance is essential, especially if you live in an area prone to natural disasters. This section offers practical advice to help you select a policy that provides adequate protection and manages your costs effectively.

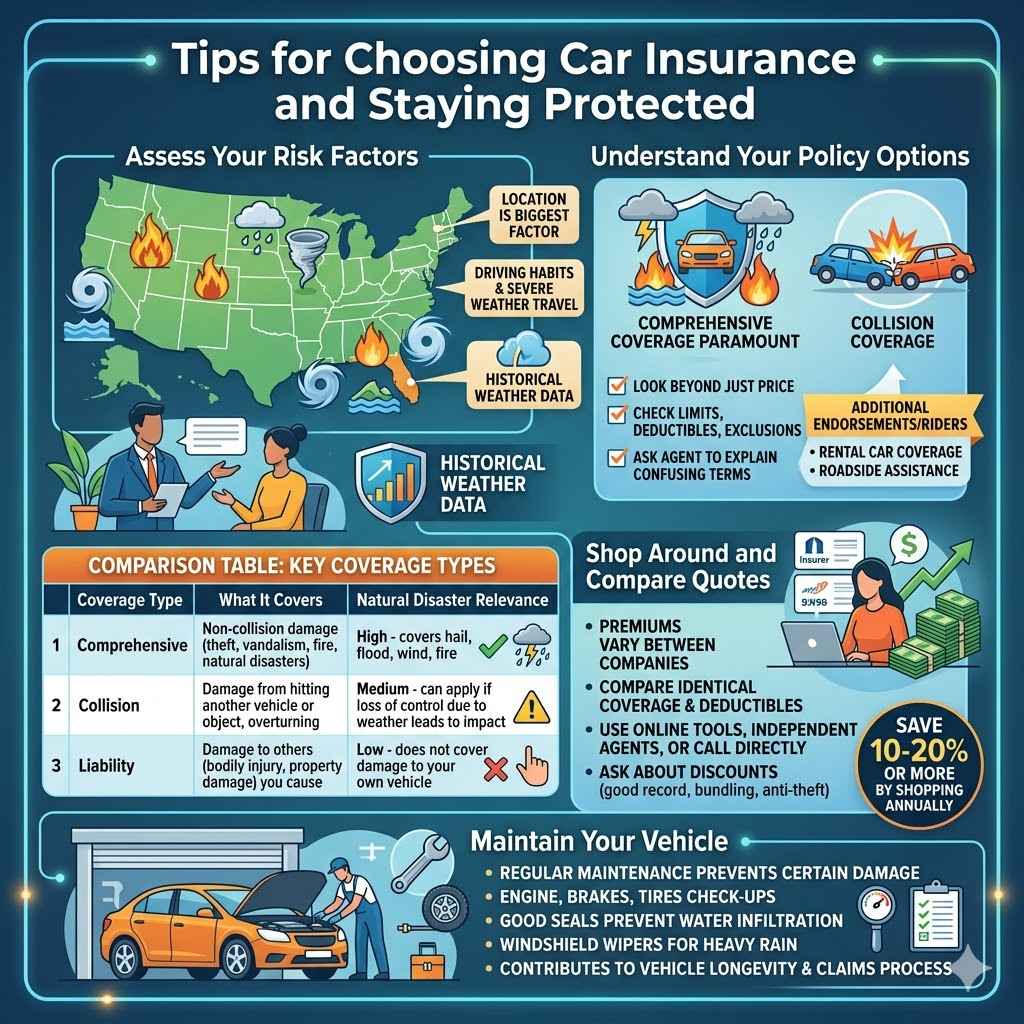

Assess Your Risk Factors

Your location is the biggest factor in assessing your risk for natural disasters. If you live in a coastal area, you face hurricane and flood risks. If you’re in the Midwest, hail and tornadoes are more common.

If you’re in the West, wildfires and earthquakes (though earthquake damage usually requires a separate policy) are concerns.

Consider your driving habits too. Do you drive frequently? Do you often travel through areas known for severe weather?

These factors can influence the type and amount of coverage you need. Taking the time to understand your personal risks helps you choose wisely.

Reviewing historical weather data for your area can also be informative. Knowing the frequency and severity of past natural disasters can help you anticipate future risks and adjust your insurance accordingly. This proactive approach can save you a lot of trouble and expense down the line.

Understand Your Policy Options

As discussed, comprehensive coverage is paramount for natural disaster protection. Ensure you have it, and understand your deductible amount. Collision coverage can also be important, depending on your circumstances.

When comparing policies, look beyond just the price. Pay close attention to the coverage limits, deductibles, and any specific exclusions. A cheaper policy might offer less protection when you need it most.

Don’t be afraid to ask your insurance agent to explain any confusing terms or coverage details.

Some insurers offer additional endorsements or riders that can enhance your coverage. For example, you might be able to add coverage for rental cars if yours is damaged, or roadside assistance. These extras can provide valuable peace of mind.

Comparison Table: Key Coverage Types

| Coverage Type | What It Covers | Natural Disaster Relevance |

|---|---|---|

| Comprehensive | Non-collision damage (theft, vandalism, fire, natural disasters) | High – covers hail, flood, wind, fire |

| Collision | Damage from hitting another vehicle or object, overturning | Medium – can apply if loss of control due to weather leads to impact |

| Liability | Damage to others (bodily injury, property damage) you cause | Low – does not cover damage to your own vehicle |

Shop Around and Compare Quotes

Insurance premiums can vary significantly between companies for the same coverage. It’s always a good idea to shop around and get quotes from multiple insurers. This can help you find the best coverage at the most competitive price.

When comparing quotes, make sure you are comparing identical coverage levels and deductibles. A quote that seems much lower might be for a policy with less coverage. Use online tools, contact independent agents, or call insurance companies directly to gather your quotes.

Don’t forget to ask about discounts. Many insurers offer discounts for good driving records, bundling multiple policies (like home and auto), or installing anti-theft devices. These savings can add up and make your insurance more affordable.

Statistic: Consumers can often save 10-20% or more by shopping for car insurance quotes annually. This simple step can lead to significant cost savings without sacrificing necessary coverage.

Maintain Your Vehicle

Regular maintenance can help prevent certain types of damage and ensure your car is in good working order, which might help mitigate some disaster-related issues. For example, ensuring your car’s seals are in good condition can help prevent water from entering the cabin during heavy rain.

Keeping up with routine check-ups for your engine, brakes, and tires is always a good practice. A well-maintained vehicle is safer to drive, and in some cases, might be less susceptible to certain types of damage if a natural event occurs. For instance, properly functioning windshield wipers are crucial during heavy rain.

While maintenance won’t prevent damage from a direct hit by a tornado or a major flood, it contributes to the overall longevity and condition of your vehicle. It also ensures that when you do file a claim, your car is in the best possible state, which can sometimes influence repair decisions.

Frequently Asked Questions

Question: Does car insurance cover damage from fallen trees during a storm

Answer: Yes, damage caused by a tree falling on your car due to a storm is typically covered under your comprehensive insurance coverage. This falls under non-collision related damage.

Question: What if my car is damaged by wind-blown debris

Answer: Damage from wind-blown debris, such as branches, signs, or other objects propelled by strong winds, is generally covered by comprehensive auto insurance.

Question: Does my insurance cover damage if I drive through floodwaters and my engine is damaged

Answer: While comprehensive coverage usually covers flood damage, driving intentionally into floodwaters can lead to a denied claim. If the floodwaters rose unexpectedly and damaged your engine, it would likely be covered by comprehensive.

Question: How is the value of my car determined if it’s declared a total loss

Answer: If your car is declared a total loss, the insurance company will pay you its actual cash value (ACV) at the time of the damage. This is the market value your car would have sold for just before the incident, not the cost of a new car.

Question: Is earthquake damage to my car covered by standard auto insurance

Answer: Standard auto insurance policies typically do not cover earthquake damage. This type of coverage usually needs to be purchased as a separate endorsement or policy.

Conclusion

Your car insurance, specifically comprehensive coverage, is your best ally against natural disaster damage. It protects your vehicle from events like floods, hail, windstorms, and wildfires. Understanding your policy’s deductibles and exclusions is key to proper preparation.

Always document damage thoroughly and work closely with your insurer to ensure fair claim resolution. Choosing the right coverage means peace of mind when unexpected weather strikes.