How to Find a Cosigner for a Car Loan Fast

Getting a car loan can be tough, especially if you’re new to it. Many people find it hard to get approved on their own. This is where finding a cosigner comes in handy.

A cosigner can make a big difference in getting your loan approved. This guide will make it simple and show you the exact steps to follow. Let’s get started and learn how to find a cosigner for a car loan fast.

Why You Might Need a Car Loan Cosigner

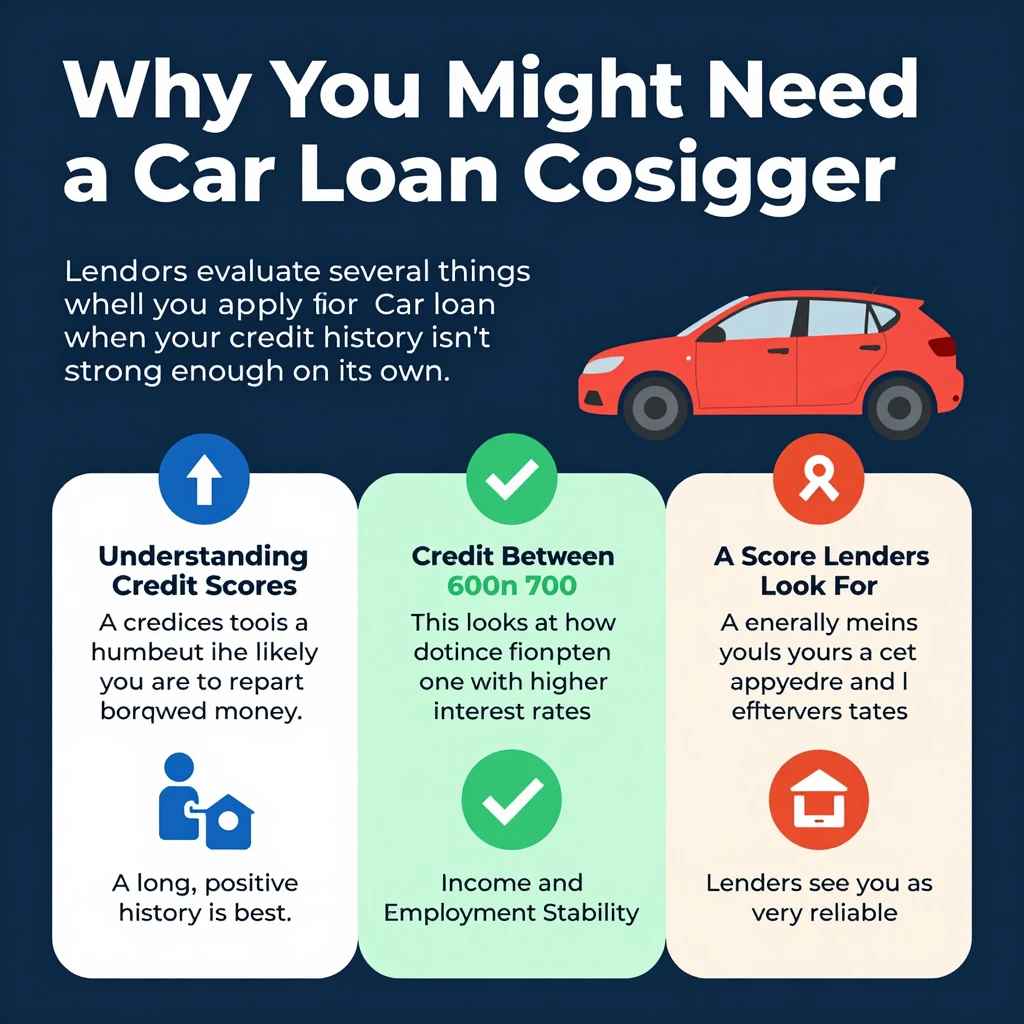

Finding a cosigner for a car loan often becomes necessary when your credit history isn’t strong enough on its own. Lenders look at your credit score and financial history to decide if you can repay a loan. If these factors are weak, they see you as a risk. A cosigner steps in to reduce that risk for the lender. They essentially promise to pay the loan if you can’t. This significantly boosts your chances of getting approved for a car loan.

Understanding Credit Scores

A credit score is a number that shows how likely you are to repay borrowed money. It’s based on your past borrowing and repayment behavior. A higher score means you’re a lower risk to lenders. Scores typically range from 300 to 850.

A score below 600 often makes it difficult to get approved for loans without help. This is because lenders see a higher chance of missed payments or defaults. Lenders use this score to quickly assess risk.

A score between 600 and 700 might get you approved, but often with higher interest rates. This means you’ll pay more over the life of the loan. It reflects a moderate level of risk for the lender.

A score above 700 generally means you’re a good borrower. You’ll likely get approved for loans with favorable terms and lower interest rates. Lenders see you as very reliable.

What Lenders Look For

Lenders evaluate several things when you apply for a car loan. They want to be sure you can handle the monthly payments and the total loan amount. This helps them avoid losing money if you can’t pay.

Credit History: This looks at how you’ve managed debt in the past. It includes things like paying bills on time, how much credit you’ve used, and any bankruptcies or collections. A long, positive history is best.

Income and Employment Stability: Lenders want to see that you have a steady job and enough income to cover loan payments. They often ask for proof of income, like pay stubs or tax returns. Consistent employment is key.

Debt-to-Income Ratio (DTI): This compares your monthly debt payments to your gross monthly income. A lower DTI shows you have more money left over after paying your debts, making you a better candidate for new loans.

The Role of a Cosigner

A cosigner is someone who agrees to share responsibility for your loan. They have a good credit history and steady income. If you miss payments, the lender can ask the cosigner to pay.

This is a big favor to ask. The cosigner’s credit score can be affected if you miss payments. It’s important for them to trust that you will make all payments on time.

Their involvement reduces the lender’s risk. This makes them more likely to approve your loan, even if your own credit isn’t perfect. They are a safety net for the lender.

Having a cosigner can also help you get better loan terms. This includes a lower interest rate, which saves you money over time. They can be a bridge to more affordable financing.

Who Can Be a Cosigner for Your Car Loan

Choosing the right cosigner is a crucial step. This person should have a strong financial standing and be someone you trust deeply. Their willingness to help can significantly impact your ability to secure a car loan. Think carefully about who you ask.

Family Members

Parents, siblings, or other close relatives are often the first people you consider. They usually have your best interests at heart and may have a solid financial history. It’s a common practice for them to help out younger family members.

Parents are a popular choice because they often have established credit and stable incomes. They’ve likely managed loans for years. This makes them attractive to lenders.

Siblings can also be a good option if they have strong credit. However, it’s important to consider how this might affect your relationship if something goes wrong with the loan payments.

This choice depends heavily on the strength of your family relationships and their financial capability. Open communication is vital.

Close Friends

A trusted close friend with a good credit history can also be a cosigner. This requires a very strong and honest friendship. Both parties need to be clear about the responsibilities and potential risks involved.

Ensure your friend fully understands what it means to cosign. They need to know their credit could be impacted. It’s a significant financial commitment for them.

This option works best when there’s a long history of trust and open communication between you. You should both feel comfortable discussing financial matters.

It’s wise to have a written agreement between you and your friend. This outlines responsibilities and expectations, even if it’s not legally binding for the lender.

Spouse or Partner

If you are married or in a long-term partnership, your spouse or partner is a natural choice. Their financial situation is often intertwined with yours anyway. They are likely to have a good understanding of your financial habits.

Their credit score and income will be considered alongside yours. This can present a stronger overall application to the lender. Joint financial applications are common.

It’s essential to discuss this decision together. Ensure you both agree on the car purchase and the loan terms. Shared financial goals are important.

This option is often the easiest because you already share financial responsibilities. It’s a natural extension of your partnership.

Considerations Before Asking

Before you approach anyone, think about their financial health. They need to be in a position to handle the loan if necessary. Asking is a big deal, so be prepared.

Make sure they have a good credit score themselves. Lenders will check their credit too. A low score on their part won’t help your application.

Confirm they have stable income. They need to show they can afford the monthly payments. Proof of income will likely be required from them.

Discuss the loan terms openly. They need to know the loan amount, interest rate, and repayment period. Transparency is key for everyone involved.

Steps to Finding a Cosigner Quickly

To find a cosigner fast, you need a clear plan. Start by assessing your own situation, then approach potential cosigners with confidence and all the necessary information. Having a list of people you might ask can speed things up.

1. Prepare Your Financial Information

Gather all your financial documents before you ask anyone to cosign. This shows you are serious and organized. It makes the process smoother for both you and the potential cosigner.

Income Proof: Collect recent pay stubs, bank statements, or tax returns. This shows lenders your ability to repay. You need to demonstrate a consistent income stream.

Credit Report: Obtain a copy of your credit report. Understand your credit score and identify any errors. Knowing your score helps you explain your situation.

Loan Details: Have a clear idea of the car you want and its price. Know the loan amount you need and the approximate monthly payment you can afford. This shows you’ve done your homework.

2. Make a List of Potential Cosigners

Think about people who meet the criteria we discussed. Who among your family, friends, or partner has good credit and a stable income? Who would be willing to help you?

Start with immediate family members like parents or siblings. They are often the most willing to help. Their financial stability is usually well-known to you.

Consider close friends who have a strong financial background. Only ask those you trust completely. Their willingness is a testament to your friendship.

If married or partnered, your spouse or significant other is a primary candidate. Their financial life is likely already integrated with yours.

3. Approach Them with Confidence and Information

When you ask someone to be your cosigner, be direct and honest. Explain why you need one and what it means for them. Provide them with all the information you’ve gathered.

Explain your credit situation clearly and what you’ve done to improve it. Be upfront about any challenges. Honesty builds trust.

Show them your financial preparedness. Share your income documents and your budget. This demonstrates responsibility.

Clearly outline the loan details. Let them know the car price, loan amount, and estimated monthly payments. They need to understand the financial commitment.

4. Offer Reassurance and Transparency

Your potential cosigner is taking on a significant risk. Reassure them that you are committed to making all payments on time. Maintain open communication throughout the loan process.

Promise to keep them updated on your payment status. Let them know if any issues arise, even small ones. Proactive communication prevents surprises.

Discuss a repayment plan with them. How will you ensure you make every payment? Having a concrete plan can ease their worries.

Emphasize that you view this as a temporary situation. Your goal is to eventually manage loans independently. This shows your long-term financial vision.

5. Have a Backup Plan

It’s possible your first choice for a cosigner might not be able to help. Have a few other people in mind. The more options you have, the faster you can secure a loan.

Don’t be discouraged if someone says no. They might have their own financial reasons or concerns. It’s not a reflection on you.

Try to understand their reasons for declining. This might help you refine your approach or choose someone else. Learn from each interaction.

Keep the process moving. If one person can’t help, move to the next person on your list promptly. Time is of the essence for getting a car loan fast.

Tips for a Faster Car Loan Approval with a Cosigner

Once you have a willing cosigner, the next step is to make the loan application process as smooth and quick as possible. Lenders appreciate efficiency and preparedness. Presenting a strong, well-organized application speeds things up.

Choose the Right Lender

Not all lenders are the same. Some specialize in working with cosigners, while others may have stricter requirements. Researching and selecting a lender that is known to be flexible can make a big difference.

Credit Unions: These member-owned financial institutions often offer more personalized service. They may be more willing to work with individuals who have a cosigner. Their focus is on member benefit rather than just profit.

Banks: Traditional banks can be a good option, especially if you have an existing relationship with them. They have a wide range of loan products. However, their approval criteria can sometimes be rigid.

Online Lenders: Many online lenders offer fast application processes and quick funding. Some may be more open to cosigned auto loans, but it’s essential to read reviews and check their specific requirements. Their technology often speeds up the decision-making.

Provide All Required Documentation Promptly

The key to a fast approval is having everything ready. When the lender asks for documents, submit them immediately. Delays in providing paperwork are a common reason for slow loan approvals.

Cosigner’s Information: The lender will need the same information from your cosigner as they do from you. This includes proof of income, identification, and their credit report authorization. Ensure your cosigner is ready to provide these details quickly.

Vehicle Information: Have details about the car you want to buy ready. This includes the Vehicle Identification Number (VIN), make, model, and year. Some lenders may require a purchase agreement or bill of sale.

Application Accuracy: Double-check all information on the loan application for accuracy. Errors or inconsistencies can cause significant delays as the lender seeks clarification. A simple mistake can hold up the whole process.

Be Prepared for a Joint Application Review

The lender will assess both your financial situation and your cosigner’s. They look at the combined financial strength of both applicants. Your cosigner’s good credit history is a major asset.

The lender will calculate the combined debt-to-income ratio. A lower DTI for both applicants strengthens the loan request. This shows a lower overall risk to the lender.

They will also evaluate the stability of both your and your cosigner’s employment. Consistent employment history is a positive indicator. This reassures the lender about future repayment ability.

The lender wants to see that even if one applicant has issues, the other can cover the loan obligations. This dual assessment is why a strong cosigner is so important.

Negotiate Terms Wisely

With a cosigner, you have more leverage to negotiate. Don’t just accept the first offer. Compare rates and terms from different lenders. Your goal is to get the best possible deal.

Use the best interest rate offered by one lender as a bargaining chip with another. Lenders often want your business and may be willing to match or beat competitors’ rates. This competition benefits you.

Discuss the loan term (how long you have to repay). A shorter term usually means lower interest paid overall, but higher monthly payments. A longer term means lower monthly payments but more interest paid over time.

Understand all fees associated with the loan. This includes origination fees, application fees, and any prepayment penalties. Knowing all costs helps you compare offers accurately.

Scenario Example for Faster Approval

Imagine Sarah wants to buy a car but has a limited credit history. Her father, who has excellent credit and a stable job, agrees to cosign. Sarah gathers her pay stubs, bank statements, and her father provides his income verification and ID.

She applies at a local credit union where she has a banking relationship. The credit union reviews their combined finances, sees strong income and credit from her father, and approves her loan within two business days, allowing her to get her car quickly. This efficient process highlights the benefit of preparedness.

Understanding the Risks and Responsibilities

Having a cosigner is a serious commitment for both parties. It’s vital to understand the potential downsides and responsibilities involved to avoid future problems. Open communication and a clear plan are essential.

For the Cosigner

The cosigner takes on significant financial risk. Their credit score can be negatively impacted if payments are missed or late. They are legally obligated to pay the loan if the primary borrower defaults.

Impact on Credit Score: Any missed or late payments will appear on the cosigner’s credit report, lowering their score. This can make it harder for them to get loans or credit in the future. It can also affect their ability to rent an apartment or even get certain jobs.

Legal Obligation: The cosigner is just as responsible for the debt as the primary borrower. The lender can pursue the cosigner for payment if the primary borrower fails to pay. This is a legally binding agreement.

Financial Strain: If the primary borrower struggles, the cosigner might have to make payments from their own funds. This can put a strain on their personal finances and budgeting. It’s a commitment that requires careful consideration of their own financial stability.

For the Primary Borrower

As the primary borrower, you have the main responsibility for the loan. You must make all payments on time to protect your cosigner’s credit and your own. Failing to do so can damage relationships.

Payment Responsibility: You must ensure payments are made in full and on time every month. This is the most important aspect of managing the loan. Your primary goal should be to avoid causing any issues for your cosigner.

Maintaining Good Financial Habits: Continue to manage your finances responsibly. Avoid taking on excessive new debt while the car loan is active. This shows you are committed to your financial health.

Communication is Key: If you anticipate any difficulty making a payment, inform your cosigner immediately. Work together to find a solution before a payment is missed. Proactive communication can prevent major problems.

What Happens If Payments Are Missed

If you miss a payment, the consequences can be swift and severe for both you and your cosigner. The lender will likely contact both parties immediately to arrange payment.

Late Fees and Penalties: Missed payments usually incur late fees, increasing the total amount owed. These fees can add up quickly. The loan agreement will detail these penalties.

Credit Damage: A missed payment will be reported to credit bureaus, affecting both your credit scores. This is damaging for both parties. It will make future borrowing more difficult and expensive.

Default and Repossession: If payments continue to be missed, the loan can go into default. The lender can then repossess the car. This means you lose the vehicle, and you and your cosigner are still likely responsible for any remaining debt.

Sample Scenario of Missed Payments

Let’s say John is the primary borrower and his mother is his cosigner. John loses his job unexpectedly and can’t make his car payment for two months. The lender first contacts John. When he can’t pay, they contact his mother. Her credit score drops significantly. The lender may also begin repossession proceedings for the car. This situation illustrates the direct negative impact on both individuals. It highlights the importance of having a plan for financial emergencies.

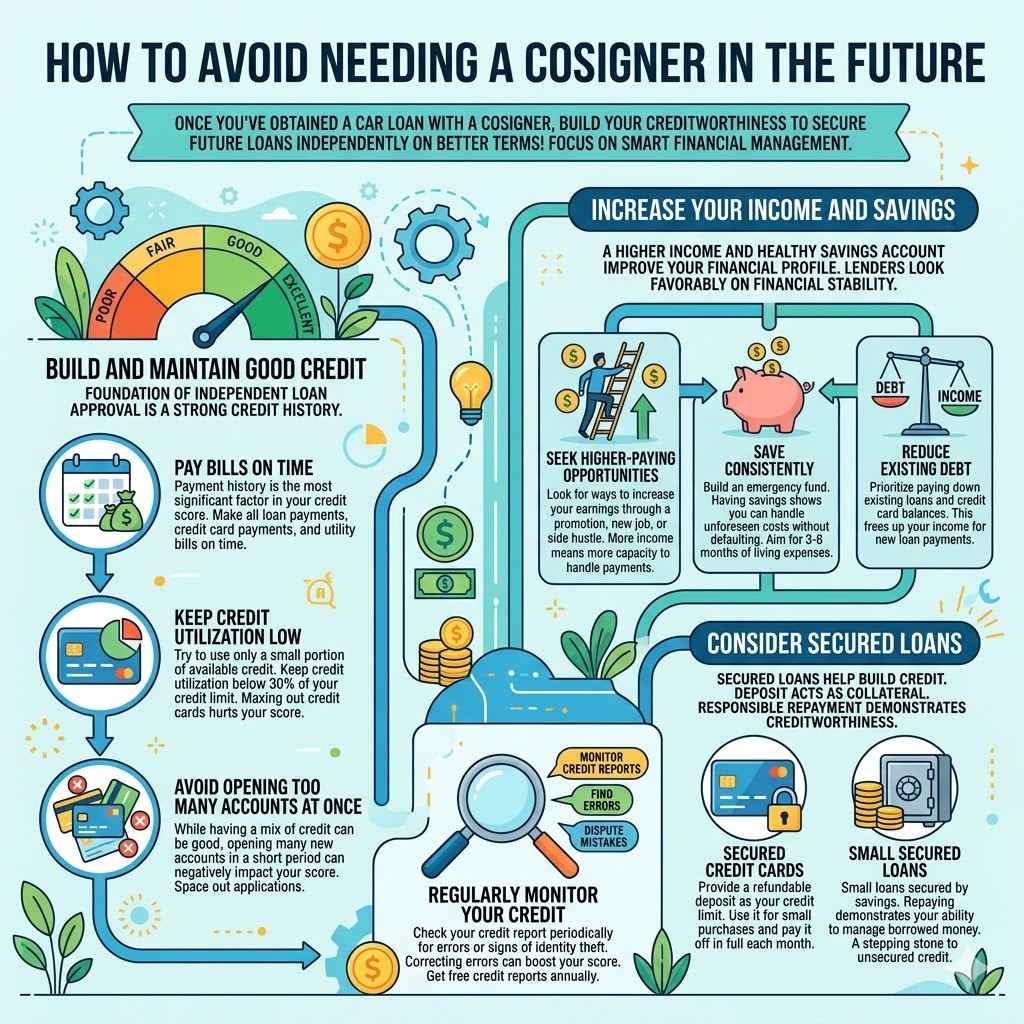

How to Avoid Needing a Cosigner in the Future

Once you’ve successfully obtained a car loan with a cosigner, your next goal should be to build your creditworthiness. This will allow you to secure future loans independently and on better terms. Focus on smart financial management.

Build and Maintain Good Credit

The foundation of independent loan approval is a strong credit history. Consistently demonstrating responsible borrowing behavior is key. This takes time and consistent effort.

Pay Bills On Time: Payment history is the most significant factor in your credit score. Make all your loan payments, credit card payments, and utility bills on time, every time. Even a single late payment can hurt.

Keep Credit Utilization Low: Try to use only a small portion of your available credit. Experts recommend keeping credit utilization below 30% of your credit limit. Maxing out credit cards hurts your score.

Avoid Opening Too Many Accounts at Once: While having a mix of credit can be good, opening many new accounts in a short period can negatively impact your score. Space out applications for new credit.

Increase Your Income and Savings

A higher income and a healthy savings account can improve your financial profile. Lenders look favorably on borrowers who demonstrate financial stability and a cushion for unexpected expenses.

Seek Higher-Paying Opportunities: Look for ways to increase your earnings, whether through a promotion, a new job, or a side hustle. More income means more capacity to handle loan payments. This also gives you more financial flexibility.

Save Consistently: Build an emergency fund. Having savings shows lenders you can handle unforeseen costs without defaulting on loans. Aim for at least 3-6 months of living expenses saved.

Reduce Existing Debt: The less debt you have, the better your debt-to-income ratio will be. Prioritize paying down existing loans and credit card balances. This frees up your income for new loan payments.

Consider Secured Loans

Secured loans, like a secured credit card or a small secured loan, can help build credit. You typically put down a deposit, which acts as collateral. Responsible repayment of these loans demonstrates your creditworthiness.

Secured Credit Cards: These are designed for people looking to build or rebuild credit. You provide a refundable deposit, and that becomes your credit limit. Use it for small purchases and pay it off in full each month.

Small Secured Loans: Some institutions offer small loans that are secured by savings. Repaying these loans demonstrates your ability to manage borrowed money. They are a stepping stone to unsecured credit.

Regularly Monitor Your Credit: Check your credit report periodically for errors or signs of identity theft. You can get free credit reports annually from major credit bureaus. Correcting errors can boost your score.

Frequently Asked Questions

Question: How long does a cosigner stay on my car loan?

Answer: The cosigner is typically responsible for the loan for its entire duration unless specific steps are taken to remove them. This usually involves refinancing the loan in your name alone once you have established sufficient credit history and can qualify on your own.

Question: Can my cosigner back out after agreeing to help?

Answer: Once the loan is approved and signed, the cosigner is legally bound to the agreement. They cannot simply “back out” of their responsibility. If they wish to be released, the loan would generally need to be refinanced under your name only.

Question: What if I can’t find anyone to cosign?

Answer: If you can’t find a cosigner, you might explore options like looking for a less expensive car, saving up for a larger down payment, or seeking out lenders who specialize in subprime auto loans (though these often have very high interest rates).

Question: Does my cosigner need to have a perfect credit score?

Answer: Not necessarily perfect, but a strong credit score is essential. Lenders look for cosigners with a history of responsible borrowing, typically a score in the good to excellent range (often 700 or higher), to significantly reduce their risk.

Question: Will having a cosigner guarantee my car loan approval?

Answer: While a cosigner greatly increases your chances of approval, it doesn’t guarantee it. The lender still reviews both applicants’ financial situations, and if there are major red flags for either person, approval might still be denied.

Summary

Learning how to find a cosigner for a car loan fast involves preparation and smart outreach. Gather your financial documents, identify trustworthy individuals with good credit and income, and present your case clearly. By understanding the responsibilities, choosing the right lender, and acting quickly, you can secure the loan you need. Focus on building your own credit to avoid needing a cosigner for future purchases.