Is It Haram to Pay Interest on a Car: Essential Guide

Generally, paying interest (riba) on a car loan is considered haram (forbidden) in Islam due to its prohibition in the Quran and Sunnah. Islam encourages interest-free financing methods like Ijara (leasing) or Murabaha (cost-plus financing) for purchasing vehicles.

Buying a car is a big step for many, and figuring out how to pay for it can feel overwhelming. Especially when you’re navigating faith-based guidelines, questions about car loans and interest can pop up. It’s totally understandable to want to make sure you’re doing things right according to Islamic teachings. Many Muslims wonder, “Is it haram to pay interest on a car?” The good news is, with a little clear guidance, you can find solutions that align with your values and get you on the road. This guide is here to break down what Islam says about interest and explore the practical, interest-free ways you can finance your car.

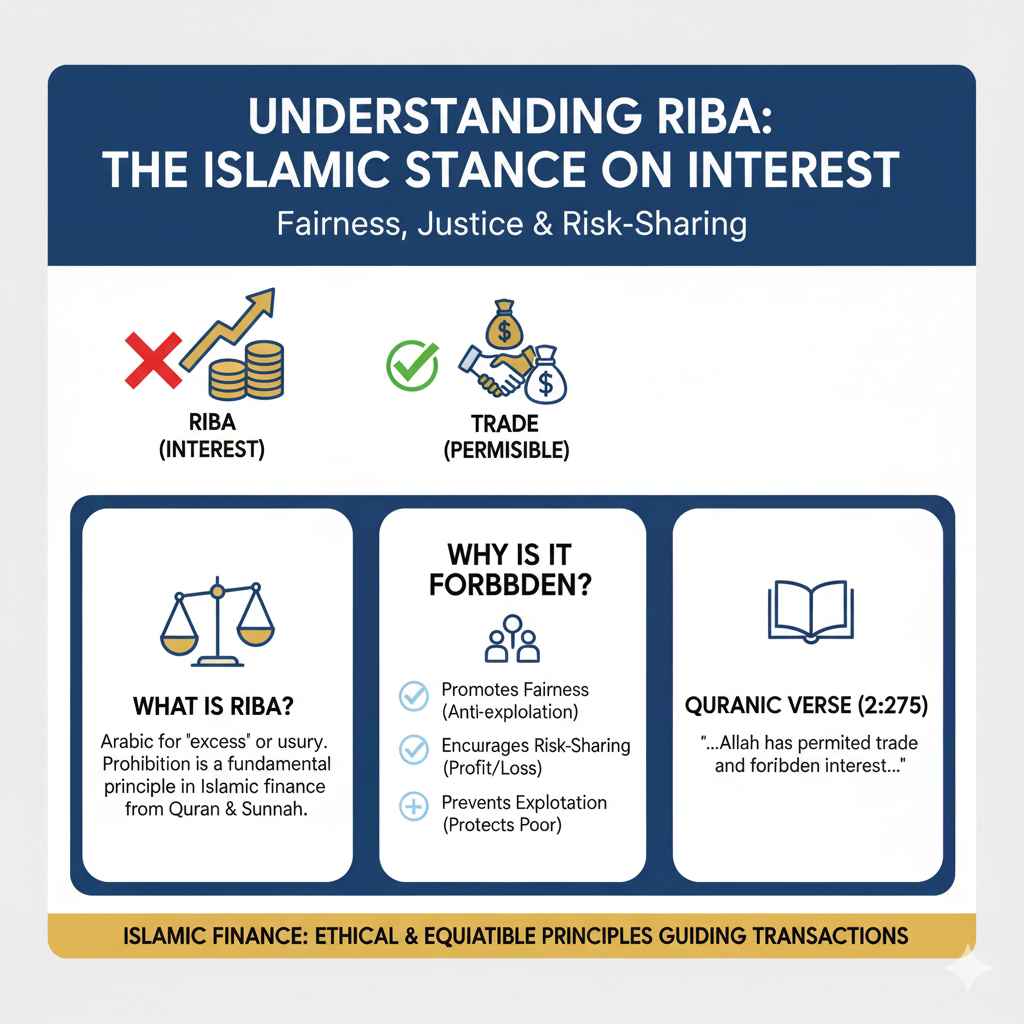

Understanding Riba: The Islamic Stance on Interest

At the heart of this question is the Islamic concept of riba, which directly translates to ‘excess’ or ‘usury’ and is broadly understood as interest. The prohibition of riba is a fundamental principle in Islamic finance, stemming from clear verses in the Quran and the teachings of Prophet Muhammad (peace be upon him).

Why is Riba Forbidden?

Islam discourages riba for several reasons, aiming to create a more equitable and just financial system:

- Promoting Fairness and Justice: Riba is seen as exploiting those in need by charging them extra for borrowing money. This can lead to a cycle of debt for the borrower and wealth accumulation for the lender without any productive work or risk involved.

- Encouraging Risk-Sharing: Islamic finance emphasizes profit and loss sharing. When you invest or lend money, you should share in the potential risks and rewards, rather than guaranteeing a fixed return regardless of the outcome.

- Preventing Exploitation: Charging interest can disproportionately affect the poor and vulnerable, making it harder for them to improve their economic situation.

The Quran states:

“And Allah has permitted trade and forbidden interest. Those who devour interest will not stand except as one stands who is tormented by Satan’s touch. That is because they say, ‘Trade is [just] like interest.’ But Allah has permitted trade and forbidden interest. So whoever receives an admonishment from his Lord and desists may have what was previously past. His affair is for Allah. But those who return [to dealing in interest] – those are the companions of the Fire; they will abide eternally therein.” (Quran 2:275)

This verse clearly distinguishes between permissible trade and prohibited interest, highlighting the severe consequences associated with engaging in riba.

Is Paying Interest on a Car Loan Haram?

Based on the Islamic principle of prohibiting riba, paying interest on a conventional car loan is generally considered haram. This applies to the interest portion of your car payments, not necessarily the principal amount you borrowed. The essence of the prohibition is earning or paying an additional amount on a loan solely based on the passage of time or the amount borrowed, without an underlying permissible transaction linked to an asset or productive activity.

When you take out a car loan from a conventional bank, the agreement typically involves paying back the principal amount borrowed plus a percentage of interest over a set period. This interest component is what falls under the definition of riba.

Alternatives to Conventional Car Loans: Interest-Free Options

The good news is that Islam not only prohibits riba but also offers practical and ethical alternatives for financing major purchases like cars. These methods ensure that your transactions are Sharia-compliant. Here are some of the most common and effective interest-free financing methods:

1. Murabaha (Cost-Plus Financing)

Murabaha is a popular Sharia-compliant financing method where the bank or financier buys the car on your behalf and then sells it to you at a predetermined profit margin. You pay the total cost (original price plus the agreed profit) in installments.

How Murabaha Works for Car Purchases:

- You find the car you want to buy.

- You approach an Islamic bank or financier and express your interest.

- The bank purchases the car from the seller, taking ownership and possession.

- The bank then sells the car to you at an agreed-upon price that includes the original cost and a specific profit margin (which is not stated as interest).

- You pay the bank back in installments over an agreed period.

The key here is that the profit is agreed upon at the outset and is tied to the sale of an asset, not just lending money. This structure is permissible because it’s a sale transaction, not a loan with interest.

2. Ijara (Leasing)

Ijara is an Islamic leasing contract. In this model, the bank or financier purchases the car and then leases it to you for a specified period and a fixed rental fee. At the end of the lease term, there might be an option for you to purchase the car.

Types of Ijara for Cars:

- Ijara wa Iqtina (Leasing with eventual ownership): This is the most common form for car financing. The lease payments contribute towards the purchase price, and you often have the option to buy the car at the end of the lease term, sometimes for a nominal fee.

- Ijara Muntahia Bittamleek (Leasing ending in ownership): Similar to Ijara wa Iqtina, the ownership transfers to you at the end of the lease, either automatically or through a purchase option.

The rental payments in an Ijara contract are considered permissible because they are for the use of an asset that the financier owns and has provided to you. It’s akin to renting a property.

3. Diminishing Musharakah (Partnership with decreasing investment)

This is a more complex partnership model. The financier and you jointly purchase the car. You then lease your portion of ownership from the financier. As you make these lease payments, you also buy out the financier’s share incrementally, hence “diminishing Musharakah.” Eventually, you become the sole owner.

Key Features of Diminishing Musharakah:

- The bank and the customer become co-owners of the car.

- The customer pays rent to the bank for using the bank’s share of the car.

- The customer also makes regular payments to purchase the bank’s share, thereby reducing the bank’s ownership stake over time.

- The rent amount decreases as the customer’s ownership share increases.

This model is Sharia-compliant because it involves co-ownership and rental of a share, rather than interest-based lending.

4. Personal Loans from Family/Friends (Interest-Free)

If you have supportive and trustworthy family members or friends, you might be able to get an interest-free loan to purchase your car. This would require clear terms and agreement to ensure fairness for all parties.

While this is an option, it’s crucial to have a written agreement, even for informal loans, to avoid misunderstandings and maintain relationships. Ensure the lender is able to provide the funds without themselves resorting to interest-based borrowing for this purpose, if that is a concern for you.

Comparing Financing Methods: A Practical Look

To help you decide, here’s a comparison of conventional interest-based loans versus Sharia-compliant alternatives:

| Feature | Conventional Loan (Interest-Based) | Sharia-Compliant (e.g., Murabaha, Ijara) |

|---|---|---|

| Islamic Permissibility | Generally Haram (Forbidden) due to Riba. | Generally Halal (Permissible) as it avoids Riba. |

| Profit/Cost Basis | Interest is a percentage charged on the loan amount. | Profit is based on a sale (Murabaha) or rent for using an asset (Ijara). |

| Risk Sharing | Lender has guaranteed return; no shared risk. | Risk is generally shared or managed through asset ownership/leasing. |

| Ownership Transfer | You own the car from the start, but the bank has a security interest. | In Murabaha, you buy from the bank directly. In Ijara, ownership transfers at the end of the lease. |

| Complexity | Often straightforward, especially with established banks. | Can sometimes be more complex to understand initially, but becoming more mainstream. |

| Availability | Widely available from most banks and financial institutions. | Available from Islamic banks, dedicated Sharia-compliant finance windows, or specialized firms. |

Choosing a Sharia-compliant method ensures that your financial dealings align with your faith, providing peace of mind alongside the practicality of owning a car. While conventional loans might seem simpler at first glance, the long-term ethical compliance with Islamic principles is paramount for many Muslims.

Finding Sharia-Compliant Car Financing

The availability of Sharia-compliant car financing has grown significantly over the years. Many regions now have Islamic banks or financial institutions that offer these services. Here’s how you can start looking:

1. Research Islamic Banks and Financial Institutions

Start by searching for Islamic banks or Sharia-compliant finance providers in your local area or online. These institutions are specifically designed to operate within Islamic financial principles.

2. Inquire About Specific Products

Once you identify potential providers, ask about their car financing products. Do they offer Murabaha, Ijara, or Diminishing Musharakah? Understand the terms, profit rates (or rental fees), repayment schedules, and any associated fees.

3. Understand the Contracts

Before signing anything, thoroughly review the contract. Make sure you understand how the ownership, payments, and eventual transfer of the vehicle work. Don’t hesitate to ask questions to clarify any doubts. Reputable institutions will be happy to explain their processes.

4. Consult a Knowledgeable Scholar or Advisor

If you’re still unsure about the permissibility of a specific financing method or contract, it’s always a good idea to consult with a trusted Islamic scholar or a financial advisor who is knowledgeable in Islamic finance. They can provide personalized guidance based on the details of the contract and your circumstances.

For instance, organizations like IslamicFinder or regional Islamic finance councils can offer directories of institutions and resources.

Are There Any Exceptions or Nuances?

While the general rule is that paying interest is haram, there are ongoing discussions and contemporary interpretations among scholars regarding situations of extreme necessity. However, for a common purchase like a car, intentionally choosing a conventional interest-bearing loan when Sharia-compliant alternatives are available and accessible is generally not considered permissible.

Some scholars might permit taking an interest-bearing loan if there is absolutely no other viable option for a critical need, such as essential transportation for work that cannot be met otherwise, and if attempting to find Sharia-compliant alternatives has proven impossible. This is often seen as a last resort, and it is crucial to document the necessity and the lack of alternatives.

However, for most people seeking to purchase a car for personal use, accessible interest-free options exist, making the prohibition of interest the standard applicable rule. It’s always best to err on the side of caution and seek Sharia-compliant solutions whenever possible.

Making Your Choice with Confidence

Deciding how to finance your car is a significant financial and spiritual decision. By understanding the Islamic prohibition of riba and exploring Sharia-compliant alternatives like Murabaha or Ijara, you can make a choice that aligns with your faith and values.

Remember, seeking knowledge is the first step. Researching local options, understanding the financing contracts, and consulting with experts can empower you to navigate this process confidently. Owning a car is achievable without compromising your religious principles.

Frequently Asked Questions (FAQ)

Q1: What is the main Islamic reason for avoiding interest on a car?

The main reason is the prohibition of riba (interest) in the Quran and Sunnah, which is considered exploitative and unjust. Islamic finance aims to ensure fairness and ethical transactions.

Q2: Is leasing a car from an Islamic bank Halal?

Yes, leasing a car through Sharia-compliant methods like Ijara is generally considered Halal. In this model, you are paying rent for the use of an asset owned by the bank, which is distinct from paying interest on a loan.

Q3: Can I use a conventional car loan if no Islamic banks are available in my area?

This is a nuanced issue. If there is a dire necessity and absolutely no Sharia-compliant alternative is available after exhausting all reasonable options, some scholars may permit it under strict conditions. However, actively seeking alternatives is always the preferred path.

Q4: How is Murabaha different from a regular car loan?

In a regular loan, you pay back the principal plus interest. In Murabaha, the bank buys the car and then sells it to you at a pre-agreed price that includes the bank’s profit. It’s a sale transaction, not a loan with interest.

Q5: What if the Islamic bank’s profit rate is similar to conventional interest rates?

The permissible profit in Murabaha and rental in Ijara are based on sale or rent of an asset, not the time value of money. The structure and the fact that it’s tied to a real transaction make it Halal, even if the percentage seems comparable in some cases. The key is the underlying contract mechanism.

Q6: Can I get an interest-free car loan from a peer-to-peer lender if they operate in a Sharia-compliant way?

Some peer-to-peer platforms might offer Sharia-compliant financing models. It’s crucial to verify their financial structure and ensure they are structured according to Islamic principles, avoiding any interest-based lending or speculative practices.

Q7: What happens if I can’t afford Sharia-compliant financing?

If Sharia-compliant financing is genuinely unaffordable or unavailable, and a car is a critical necessity (e.g., for work that supports your family), you might need to explore alternative transport, save up longer, or consult with an Islamic scholar for specific guidance on your situation.

Conclusion

Navigating car financing while adhering to Islamic principles is entirely possible and commendable. The prohibition of riba (interest) is a clear tenet, but Islam provides a wealth of ethical and practical alternatives. Methods like Murabaha, Ijara, and Diminishing Musharakah offer Sharia-compliant ways to acquire a vehicle, ensuring your transactions are fair, just, and pleasing to Allah. By educating yourself about these options, researching available Islamic financial institutions, and understanding the contract terms, you can confidently make an informed decision. Remember, the aim is not just to own a car but to do so in a way that brings blessings and peace of mind, free from the spiritual concerns associated with interest-based transactions. Your journey to a halal car purchase starts with knowledge and commitment.