Why Is My Car Loan More Than Purchase Price: Secret Costs

Your car loan is more than the purchase price because it includes taxes, dealership fees, registration costs, and optional add-ons like extended warranties or GAP insurance. If you traded in a car with negative equity (owing more than it’s worth), that old debt is also rolled into your new loan, increasing the total amount you finance.

Hi there, Md Meraj here! It’s a moment of pure excitement: you’ve found the perfect car. You agree on a price, shake hands, and head to the finance office. But when you see the final loan amount, your heart sinks. It’s thousands of dollars more than the sticker price you discussed. How did this happen? It’s a confusing and frustrating feeling, but don’t worry, you’re not alone. This happens to many people.

Today, I’m going to pull back the curtain on car financing. We’ll walk through all the “secret” costs that get tacked onto a car loan. I’ll explain everything in simple terms so you can feel confident and in control the next time you buy a car. Let’s break it down together.

Understanding the Total Financed Amount vs. The Sticker Price

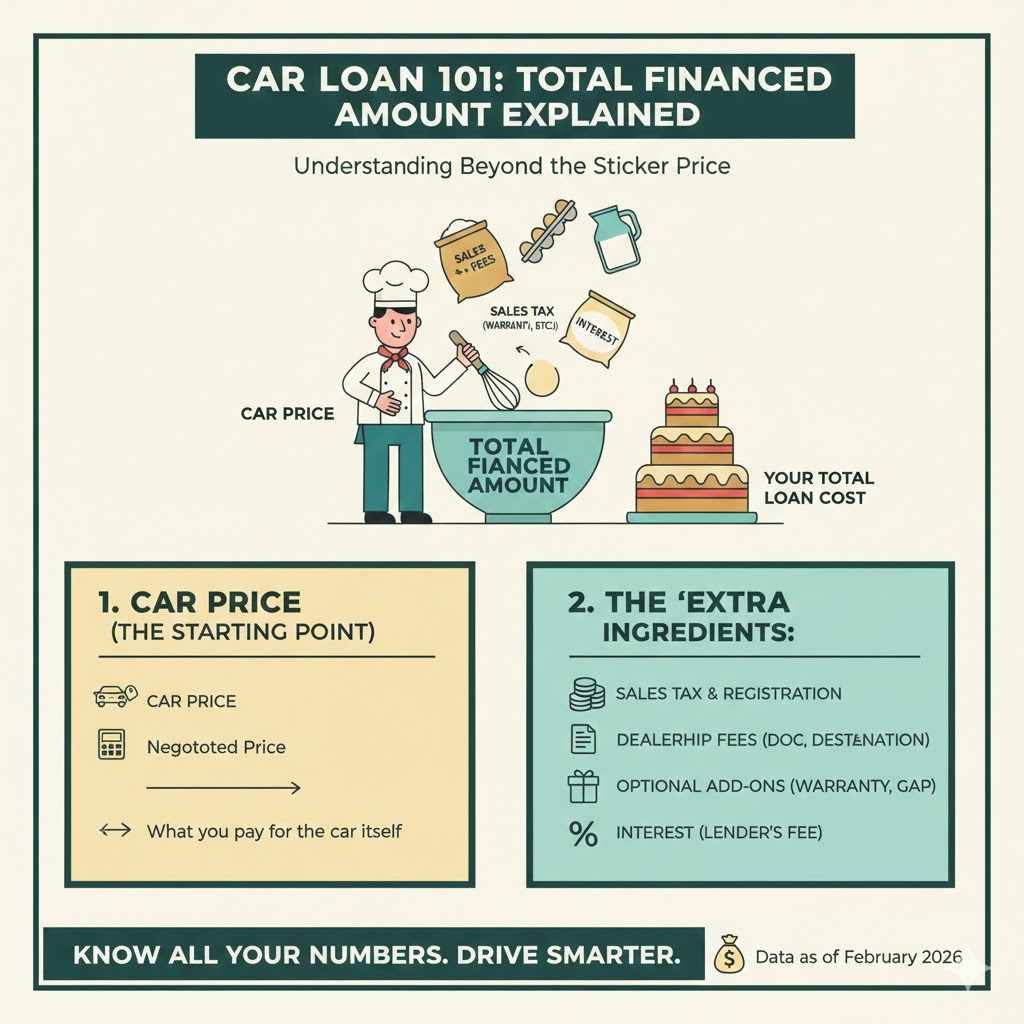

The first thing to understand is the difference between the price of the car and the amount you actually borrow. Think of the car’s sticker price (or the price you negotiated) as the starting point. The final loan amount, often called the “amount financed,” is that starting price plus a bunch of other costs.

It’s like baking a cake. The flour is the main ingredient (the car’s price), but you also need to add eggs, sugar, and milk (taxes, fees, and add-ons) to get the final product (your total loan). Let’s look at what those extra ingredients are.

The Unavoidable Costs: Taxes and Government Fees

These are the costs you generally can’t avoid. They are required by your state or local government and are collected by the dealership on their behalf. While you can’t skip them, knowing what they are helps you budget accurately.

1. Sales Tax

Just like when you buy a TV or a gallon of milk, you have to pay sales tax on a car. The rate varies widely depending on your state, county, and even your city. This can add a significant amount to your purchase. For example, a 7% sales tax on a $25,000 car is an extra $1,750 that gets added to your loan.

2. Title and Registration Fees

Your state’s Department of Motor Vehicles (DMV) or equivalent agency charges fees to put the car’s title in your name and to register it so you can legally drive it on the road. This covers the cost of your license plates and official ownership documents. These fees typically range from $50 to a few hundred dollars.

3. Documentation Fee (Doc Fee)

This is a fee the dealership charges to handle all the paperwork involved in the sale. This includes preparing the sales contract, title documents, and registration forms. Doc fees vary wildly by dealership and state. Some states cap these fees, but in others, they can be several hundred dollars. While it’s a dealership fee, not a government one, it’s almost always non-negotiable.

The Sneaky Extras: Dealership Add-Ons and Protection Plans

This is where the loan amount can really swell. After you’ve agreed on a price for the car, you’ll meet with a finance manager. Their job is to sell you additional products and services. While some can be useful, they all add to the total amount you finance, meaning you pay interest on them for years.

It’s important to remember that almost all of these are optional. You can say “no, thank you.”

Common Dealership Add-Ons:

- Extended Warranty (or Vehicle Service Contract): This covers repair costs after the manufacturer’s warranty expires. It can provide peace of mind, but it can also add thousands of dollars to your loan.

- GAP (Guaranteed Asset Protection) Insurance: If your car is totaled in an accident, your regular car insurance only pays out its current market value. If you owe more on your loan than the car is worth (which is common in the first few years), GAP insurance covers that “gap.” It can be valuable, but you can often buy it cheaper from your own insurance company.

- Paint and Fabric Protection: A special coating for the car’s paint and a treatment for the interior upholstery to protect against stains and damage. Dealerships often charge a premium for this service, which has debatable effectiveness.

- VIN Etching: This involves etching the Vehicle Identification Number (VIN) onto the windows to deter theft. Some insurance companies offer a discount for it, but the cost at the dealership can be much higher than what a third-party service would charge.

- Tire and Wheel Protection: A plan that covers the cost of repairing or replacing tires and wheels damaged by road hazards like potholes.

- Prepaid Maintenance Plans: This allows you to pay for future oil changes, tire rotations, and other routine services upfront by rolling the cost into your loan. It might seem convenient, but you’re paying interest on future maintenance.

Example Breakdown of Added Costs

Let’s see how these costs can inflate a car loan. Imagine you’re buying a car with a negotiated price of $25,000.

| Item | Cost | Running Total |

|---|---|---|

| Negotiated Car Price | $25,000 | $25,000 |

| State Sales Tax (7%) | $1,750 | $26,750 |

| Title & Registration Fees | $250 | $27,000 |

| Dealer Doc Fee | $500 | $27,500 |

| Extended Warranty (Optional) | $2,500 | $30,000 |

| GAP Insurance (Optional) | $800 | $30,800 |

| Final Amount Financed | – | $30,800 |

As you can see, the car you bought for $25,000 ended up with a loan for $30,800. That’s $5,800 more than the purchase price, and we haven’t even talked about interest yet!

The Biggest Culprit: Negative Equity

One of the most significant reasons a car loan exceeds the purchase price is something called “negative equity,” also known as being “upside-down” or “underwater” on your trade-in.

What is Negative Equity?

Negative equity happens when you owe more money on your current car loan than the car is actually worth. For example, you might still owe $15,000 on your car, but its trade-in value is only $12,000. That leaves you with $3,000 of negative equity.

How Does It Affect Your New Loan?

When you trade in a car with negative equity, that leftover debt doesn’t just disappear. The dealership pays off your old $15,000 loan, takes your $12,000 car, and adds the remaining $3,000 debt onto your new car loan. This is called “rolling over” negative equity.

An Example of Rolling Over Negative Equity

Let’s go back to our $25,000 car purchase, but this time, you have a trade-in with negative equity.

| Item | Amount | Explanation |

|---|---|---|

| New Car Price | $25,000 | The price you agreed on for the new vehicle. |

| Taxes & Fees | $2,500 | Combined cost of sales tax, title, registration, and doc fees. |

| Subtotal | $27,500 | Your cost before the trade-in is considered. |

| Your Trade-In Situation | ||

| Amount Owed on Trade-In | $15,000 | Your remaining loan balance on your old car. |

| Actual Value of Trade-In | $12,000 | What the dealer is giving you for your old car. |

| Negative Equity | ($3,000) | The debt that must be paid off. |

| Amount Added to New Loan | +$3,000 | The negative equity is rolled into your new financing. |

| Total Amount Financed | $30,500 | ($27,500 + $3,000) |

In this scenario, you started with a $25,000 car but are now financing $30,500—before any optional add-ons! Rolling over negative equity is a dangerous cycle, as it makes it much harder to get “right-side up” on your new loan.

Don’t Forget About Interest: The Cost of Borrowing

While interest isn’t part of the initial amount financed, it dramatically increases the total amount you will pay over the life of the loan. The higher your initial loan amount (from taxes, fees, add-ons, and negative equity), the more interest you will pay.

Your interest rate (APR) is based on your credit score, the loan term, and the lender. A longer loan term, like 72 or 84 months, will give you a lower monthly payment, but you’ll pay much more in interest over time. The Consumer Financial Protection Bureau (CFPB) offers great resources to help you understand your loan terms.

How Loan Term Affects Total Cost

Let’s look at a $30,000 loan at a 6% APR over different time periods.

| Loan Term | Monthly Payment | Total Interest Paid | Total Amount Paid |

|---|---|---|---|

| 48 Months (4 years) | $698 | $3,504 | $33,504 |

| 60 Months (5 years) | $580 | $4,799 | $34,799 |

| 72 Months (6 years) | $498 | $5,816 | $35,816 |

| 84 Months (7 years) | $439 | $6,876 | $36,876 |

Choosing the 7-year loan instead of the 4-year loan lowers your payment by $259 per month, but it costs you an extra $3,372 in interest! This is why focusing only on the monthly payment can be a costly mistake.

How to Keep Your Loan Amount in Check

Now that you know how a car loan can balloon, how can you prevent it? Here are some simple, practical steps to take control of your car-buying experience.

- Make a Larger Down Payment: A substantial down payment (ideally 20% of the purchase price) reduces the amount you need to finance. This means you’ll pay less interest, and it provides a buffer against depreciation, helping you avoid becoming upside-down.

- Get Pre-Approved for a Loan: Before you even step into a dealership, talk to your own bank or a local credit union. Getting pre-approved for a loan gives you a firm budget and a competitive interest rate to compare against the dealership’s offer.

- Focus on the “Out-the-Door” Price: Don’t just negotiate the car’s sticker price. Ask the salesperson for the “out-the-door” price. This number includes the car’s price, taxes, and all fees. It’s the real bottom line and prevents surprises later.

- Just Say No to Unnecessary Add-Ons: Politely but firmly decline extras you don’t need or want. If you are interested in something like GAP insurance, tell them you’ll shop around for it later. Remember, these are optional profit-makers for the dealership.

- Review the Buyer’s Order Carefully: Before you sign anything, read every line of the buyer’s order or sales contract. Make sure all the numbers match what you agreed to. Check for added fees or products you didn’t ask for. Don’t be afraid to ask questions!

- Know Your Trade-In’s Value: If you’re trading in a car, research its value beforehand using sources like Kelley Blue Book or Edmunds. Also, find out your exact loan payoff amount from your current lender. This helps you know if you have positive or negative equity. If you’re underwater, it’s often better to try and pay down the loan before trading in, if possible.

FAQs: Your Car Loan Questions Answered

1. Can I refuse all dealership add-ons?

Yes, absolutely. Products like extended warranties, paint protection, and VIN etching are almost always optional. The finance manager may be persistent, but you have the right to politely decline them. The only things you typically can’t refuse are government-mandated taxes and fees, and the dealer’s doc fee (though you can try to negotiate it or the car’s price to offset it).

2. What is a “doc fee” and is it negotiable?

A “doc fee” (documentation fee) is what dealerships charge for processing the sale paperwork. While the fee itself is rarely negotiable, you can negotiate the overall price of the car to compensate for a high doc fee. For example, if the doc fee is $500, ask for an additional $500 off the car’s price.

3. Is GAP insurance a good idea?

GAP insurance can be very valuable, especially if you’re making a small down payment or have a long-term loan (60+ months). In these cases, you’ll likely be upside-down on your loan for the first few years. However, you can almost always buy it for less from your personal auto insurance provider than from the dealership. It’s worth getting a quote from your insurer first.

4. How can I find out my trade-in’s true value?

Use online resources like Kelley Blue Book (KBB), Edmunds, and NADAguides to get an estimate. For the most accurate picture, get quotes from multiple sources. You can take your car to a dealer like CarMax for a no-obligation written offer, which you can then use as a baseline when negotiating with the dealership where you’re buying your new car.

5. Can I pay off my car loan early to save on interest?

In most cases, yes. Most auto loans are simple interest loans, meaning you can make extra payments or pay the loan off entirely without a penalty. This is a great way to save a lot of money on interest. Always check your loan agreement to make sure there is no “prepayment penalty,” though this is rare for standard auto loans. The U.S. government offers tips on vehicle ownership that can help you plan your finances.

6. Does a long loan term (like 84 months) really save me money?

No, it costs you more. While a longer loan term lowers your monthly payment, it dramatically increases the total amount of interest you pay over the life of the loan. You also stay upside-down on your loan for much longer, increasing your financial risk if the car is damaged or you need to sell it. It’s best to choose the shortest loan term you can comfortably afford.

Conclusion: Drive Away with Confidence

Seeing your car loan total jump higher than the sticker price can be alarming, but it’s not a mystery when you know where the extra costs come from. By understanding taxes, fees, optional add-ons, and the major impact of negative equity, you can walk into any dealership with the knowledge to protect your wallet.

Remember, buying a car is a major financial decision. Take your time, do your research, and don’t be afraid to ask questions or say no. By preparing ahead of time—getting pre-approved, knowing your trade-in value, and focusing on the out-the-door price—you put yourself in the driver’s seat of the negotiation. Now you have the tools to make a smart purchase and drive away happy, without any costly surprises.