Can Dealer Take Car Back After Papers Are Signed? Essential Guide

Generally, once you’ve signed all the purchase agreement and financing papers for a car, the dealer cannot simply “take the car back” without cause. The contract is legally binding. However, if your financing falls through or there are specific clauses in your contract, there are exceptions. This guide explains your rights and what happens.

Can a Dealer Take Back a Car After Papers Are Signed? Your Essential Guide as Md Meraj.

Buying a car is exciting, and signing those papers can feel like the final hurdle. But what happens if, after you’ve driven your new car home, the dealership calls saying they need it back? This can be a scary thought! As your trusted automotive guide, I’m here to break down this confusing situation in a way that makes sense. You’ve signed the paperwork, and you thought everything was finalized. So, can a dealer legally take your car back after the deal is done? Let’s explore your rights and the circumstances where this might happen. Don’t worry, we’ll walk through it together, step by step, so you feel confident and informed.

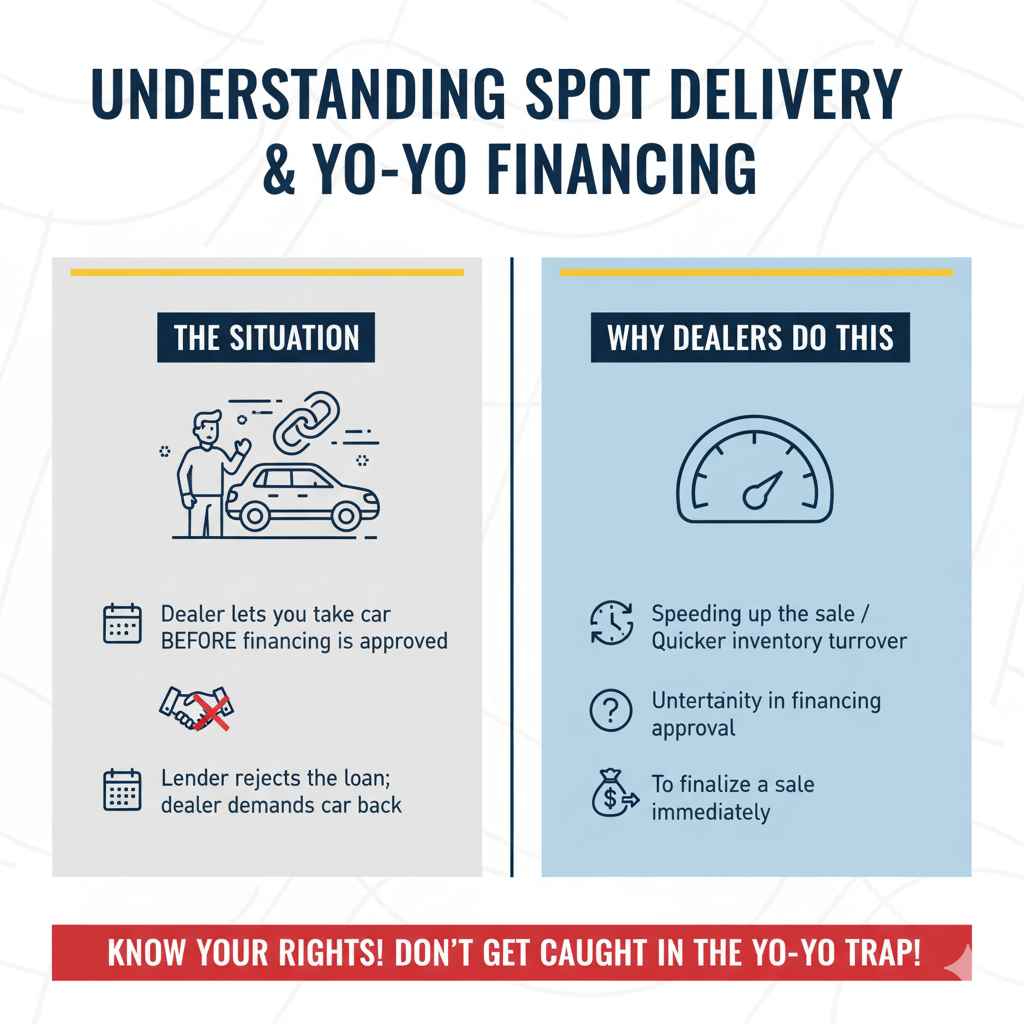

Understanding the “Spot Delivery” or “Yo-Yo Financing” Situation

The scenario where a dealer tries to take back a car after the paperwork is signed often falls under what’s known as “spot delivery” or “yo-yo financing.” This happens when a dealership lets you drive off the lot with a car before the financing has been officially approved by a lender. They essentially “spot” you the car, hoping the bank will approve the loan. If the lender rejects the loan, the dealership then tries to reclaim the vehicle.

This practice can be frustrating and even feel unfair. You believed you had purchased your car, only to be told it’s not a done deal. It’s important to understand that while dealerships want to make sales, they also operate within legal frameworks that protect both them and you, the buyer.

Why Do Dealerships Do This?

Dealerships sometimes use spot delivery to secure a sale immediately, especially if they are unsure about the buyer’s creditworthiness or if there are delays in getting loan approval. They might also do it to move inventory quickly.

- Speeding up the sale: Getting you into the car immediately can make the sale feel more concrete.

- Inventory turnover: Especially with used cars, dealers want to move vehicles quickly.

- Uncertainty in financing: Sometimes, a dealer might have a “preliminary” approval but needs final confirmation from the bank.

When Can a Dealer Legally Take Back Your Car After Signing?

While rare, there are specific circumstances where a dealer might be able to take the car back. These usually hinge on the financing not being finalized or specific clauses within your purchase agreement.

1. Financing Not Approved (The Most Common Reason)

This is the big one. When you sign the papers at the dealership, you often sign a purchase agreement and a retail installment contract (the loan agreement). However, the dealership then sends these documents to a bank or financing company for final approval. If the lender reviews your credit history, income, and debt-to-income ratio and decides they cannot approve the loan as written, the deal has not truly been finalized. The dealer essentially has to take the car back because they haven’t secured the funds to pay for it themselves or for you to pay it off.

Key Takeaway: The contract you sign is often made “subject to lender approval.” This is a crucial phrase to look out for.

2. Contract Clauses and “Buy-Here, Pay-Here” Deals

Some dealerships, particularly “buy-here, pay-here” lots, have specific contracts that allow them to repossess the vehicle if you miss payments or if their internal financing falls through. These contracts can sometimes be more favorable to the dealer.

“Spot Delivery” Agreements: Your contract might contain a clause about spot delivery. Such clauses can sometimes allow the dealer to reclaim the vehicle if the financing isn’t approved within a certain timeframe (typically a few days to a week). Always read your contract thoroughly before signing!

3. Fraud or Misrepresentation

If you provided false information on your loan application or during the purchase process (e.g., lied about your income, traded-in car details), the lender or dealer could void the contract and take the car back. This is a serious issue, and it’s vital to be honest throughout the process.

What Your Purchase Agreement Should Say

A legitimate car purchase agreement should be clear about the terms of the sale. Pay close attention to these sections:

- Financing Contingency: Does the contract state that the sale is contingent upon financing approval by a third-party lender? This is common and protects you.

- “As-Is” Sale: Unless you purchased an extended warranty, cars are often sold “as-is.” This means you accept the car with any existing mechanical issues.

- Delivery Date/Possession: When do you officially take possession?

- Conditions for Return/Repossession: Are there any specific conditions under which the dealer can take the car back?

It’s always a good idea to have a legal professional or consumer rights advocate review a contract if you’re unsure about its terms. Organizations like the Federal Trade Commission (FTC) offer valuable consumer information on car purchases.

Your Rights as a Buyer

You have rights when buying a car. If a dealer tries to “yo-yo” you, understand what you can do. Your rights often depend on your state’s laws and the specific contracts you signed.

1. The Right to Understand Your Contract

You have the right to understand every part of the contract you sign. If you don’t understand a clause, ask for clarification. If the dealer is evasive, it’s a red flag. Never feel pressured into signing something you don’t fully comprehend.

2. The Right to Verified Financing

Once financing is officially approved by the lender, the deal is typically locked in. You should receive a clear confirmation of loan approval, including the interest rate, term, and monthly payment. If the dealer tries to renegotiate terms after initial approval, be wary.

3. Protection Against Unfair “Spot Delivery”

Many states have laws that regulate spot deliveries to protect consumers. These laws might limit the duration the dealer can let you drive the car without final financing approval, or they might require specific disclosures. For instance, some states require dealers to inform you in writing that the sale is conditional on financing approval.

You can often find specific consumer protection laws related to car sales and financing by visiting your state’s Department of Motor Vehicles (DMV) or Attorney General’s office website.

4. The Right to Know About Recourse Options

If the dealer takes the car back, they usually can’t just keep any money you’ve paid as a down payment or trade-in. They may have to return your down payment and any trade-in that they still possess (though they might be able to deduct reasonable costs for the use and depreciation of the car while you had it). This varies by state law.

What to Do if a Dealer Wants Your Car Back

If the dealership contacts you saying they need the car back, stay calm and gather information. Here’s a step-by-step approach:

Step 1: Stay Calm and Ask for an Explanation

Don’t panic. Ask the dealer to explain exactly why they need the car back. Is it a financing issue? Was there a problem with the paperwork? Get the specific reason in writing if possible.

Step 2: Review Your Contract

Pull out all the paperwork you signed. Look for clauses related to financing contingency, spot delivery, or conditions for repossession. Pay attention to any mention of “subject to lender approval.”

Step 3: Verify the Financing Status

If the reason is financing, try to contact the lender directly (if you know who it is) to confirm whether the loan was approved or denied. The dealer should provide you with a denial letter from the lender if the loan was rejected.

Step 4: Understand Your Repayment or Return Options

If financing was denied, the dealer might present you with:

- Returning the Car: You return the vehicle, and your obligation to that specific loan ends (though a new deal might be needed).

- A Different Financing Plan: The dealer might offer to find a different lender or arrange financing with different terms (potentially higher interest rates or a larger down payment).

- A Different Vehicle: They might offer you a less expensive car that you can qualify for.

Step 5: Seek Expert Advice if Needed

If you feel pressured, confused, or believe the dealer is acting unfairly, don’t hesitate to seek help. You can contact consumer protection agencies in your state or consult with an attorney specializing in consumer law. The Consumer Financial Protection Bureau (CFPB) is another excellent resource for understanding your financial rights.

Dealer Take-Back Scenarios: A Comparison Table

Here’s a look at common scenarios and their likely outcomes:

| Scenario | Likely Outcome | Buyer’s Recourse |

|---|---|---|

| Financing Officially Approved | Deal is final. Dealer cannot take the car back. | None required, deal is secured. Report any attempted repossession to authorities. |

| Financing Officially Denied (and contract has contingency) | Dealer can usually take the car back. | Your down payment and trade-in (if still on lot) should be returned. You may need to find another car. Review contract details carefully. |

| Financing Officially Denied (and contract is unconditional) | This is a murky area. Dealer may try to repossess. | Consult an attorney immediately. Your contract terms are critical here. |

| Buyer Provided False Information | Contract can be voided. Dealer can repossess. | Buyer may face legal consequences. Seek legal counsel. |

| “Spot Delivery” Without Clear Contingency & Long Delay | Dealer may attempt repossession. Varies by state law. | Crucial to review state laws and contract. Contact consumer protection agencies. |

Common Misconceptions About Car Dealer Buy-Backs

There are a lot of myths floating around about car dealerships and sales. Let’s clear a few up:

-

Myth: Once I drive it off the lot, the car is mine, no matter what.

Reality: Not always. If the financing isn’t secured and your contract has a contingency, the sale isn’t final. -

Myth: The dealer can take the car back anytime they want if I miss a payment.

Reality: Repossession is a legal process, especially if you’ve already paid for the car and financing is approved. If financing is denied, that’s different. Specific laws govern repossession. -

Myth: If I signed, they can’t change the terms.

Reality: This is usually true for finalized deals. However, if financing is repeatedly denied, they might try to offer different terms or a different vehicle, but you are not obligated to accept if your original deal was finalized.

The Importance of Reading the Fine Print

I can’t stress this enough: read everything before you sign. Look for phrases like:

- “Subject to Lender Approval”

- “Contingent Upon Final Financing Approval”

- “Spot Delivery Agreement”

If any of these are present, it means the sale isn’t truly final until the bank gives the green light. This protects the dealer, but it also means you could potentially have the car taken back.

Pro Tip: Don’t be afraid to ask the finance manager to explain any part of the contract you find confusing. They work with these documents every day and should be able to clarify things. If they can’t or won’t, it’s a sign to proceed with extreme caution.

What Happens to Your Down Payment and Trade-In?

If the dealership successfully takes the car back due to unapproved financing:

- Down Payment: The dealership should return your down payment. They may deduct a fee for the use of the vehicle and any significant depreciation. This deduction amount can sometimes be a point of contention, and state laws often regulate it.

- Trade-In: If the dealership still has possession of your trade-in vehicle, they must return it to you. If they’ve already sold your trade-in, they usually have to give you the fair market value of it, minus any remaining loan balance you owed on it, and potentially reasonable costs for use and depreciation.

It’s crucial to get your money and trade-in back promptly. If there are delays or disputes, document everything and consider contacting consumer protection agencies.

Tips for a Smoother Car Buying Experience

To avoid the stress of a dealer trying to take your car back, follow these tips:

- Get Pre-Approved for Financing: Before you even step into a dealership, get pre-approved for a car loan from your bank or credit union. This gives you a benchmark interest rate and strengthens your negotiating position. It also means the financing is already secured for you, reducing the risk of a spot delivery issue. You can learn more about pre-approval on sites like NerdWallet.

- Be Honest on Your Application: Provide accurate information about your income, employment, and debts.

- Understand Your Budget: Know exactly how much you can afford for a monthly payment, including insurance, gas, and maintenance.

- Negotiate the “Out-the-Door” Price: Focus on the total price of the car, not just the monthly payment. Also, negotiate the terms of your trade-in separately.

- Allow Adequate Time: Don’t rush the process. Take your time to review documents.

- Ask Questions: If anything is unclear, ask!

- Keep Digital and Physical Copies: Save all copies of signed contracts and any correspondence.

Frequently Asked Questions (FAQs)

Q1: Can a dealer take the car back if I signed the papers but didn’t get approved for a loan?

A: Yes, if your contract includes a clause stating the sale is “subject to lender approval” and the financing was ultimately denied, the dealer can usually take the car back. They must typically return your down payment and trade-in.

Q2: What if I already made three car payments?

A: If you’ve made payments and the financing was officially approved, the deal is generally final. If financing was denied and the dealer is now trying to take it back after you’ve made payments, this could be problematic for the dealer. You should review your contract and state laws, and consider seeking legal advice.

Q3: Can the dealer charge me for driving the car if they take it back?

A: In many states, yes. If financing falls through and the car is returned, the dealer may be allowed to deduct a reasonable charge for the miles you drove and any depreciation that occurred. This is often subject to state law and your contract.

Q4: I signed the papers yesterday, and the dealer wants the car back today because financing was denied. Is this legal?

A: If your contract contains a financing contingency and the lender denied the loan, it’s likely legal for them to take the car back. However, ensure they follow proper procedures for returning your down payment/trade-in and that the period of you having the car was reasonable under state law.

Q5: My contract doesn’t mention “subject to lender approval.” Can they still take it back?

A: This is a critical point. If your contract is unconditional and financing was approved, they generally cannot. If financing was denied and the contract is unconditional, it’s a more complex situation. It’s vital to have a lawyer review such a contract as it may be considered a “spot delivery” agreement that could be problematic for the dealer depending on state laws.

Q6: What if the dealer sold my trade-in vehicle?

A: If the dealer took the car back due to financing issues and they had already sold your trade-in, they are typically required to return the cash equivalent of its fair market value (after accounting for any outstanding loan on the trade-in). If they fail to do so, you may need to take legal action