Can You Buy A Car At 17 Without Parents? Essential Guide

Yes, it’s possible to buy a car at 17 without your parents’ direct involvement, but it requires careful planning. You’ll need to navigate legal age restrictions, financing, insurance, and registration, often with an adult co-signer or parent’s permission for certain steps. This guide breaks down how to do it safely and legally.

Buying your first car is a huge milestone! The freedom a car brings is exciting, and many teenagers start dreaming about it early. But if you’re 17, you might be wondering, “Can you buy a car at 17 without parents?” The straight answer is, it’s complicated, but not impossible. There are legal hurdles and practical steps you need to tackle. Many dealerships and private sellers might shy away from a 17-year-old buyer due to age and contract laws. But with the right approach and understanding of the process, you can absolutely set yourself up for car ownership. This guide will walk you through everything you need to know, making this exciting goal achievable.

Navigating the Legal Landscape for 17-Year-Old Car Buyers

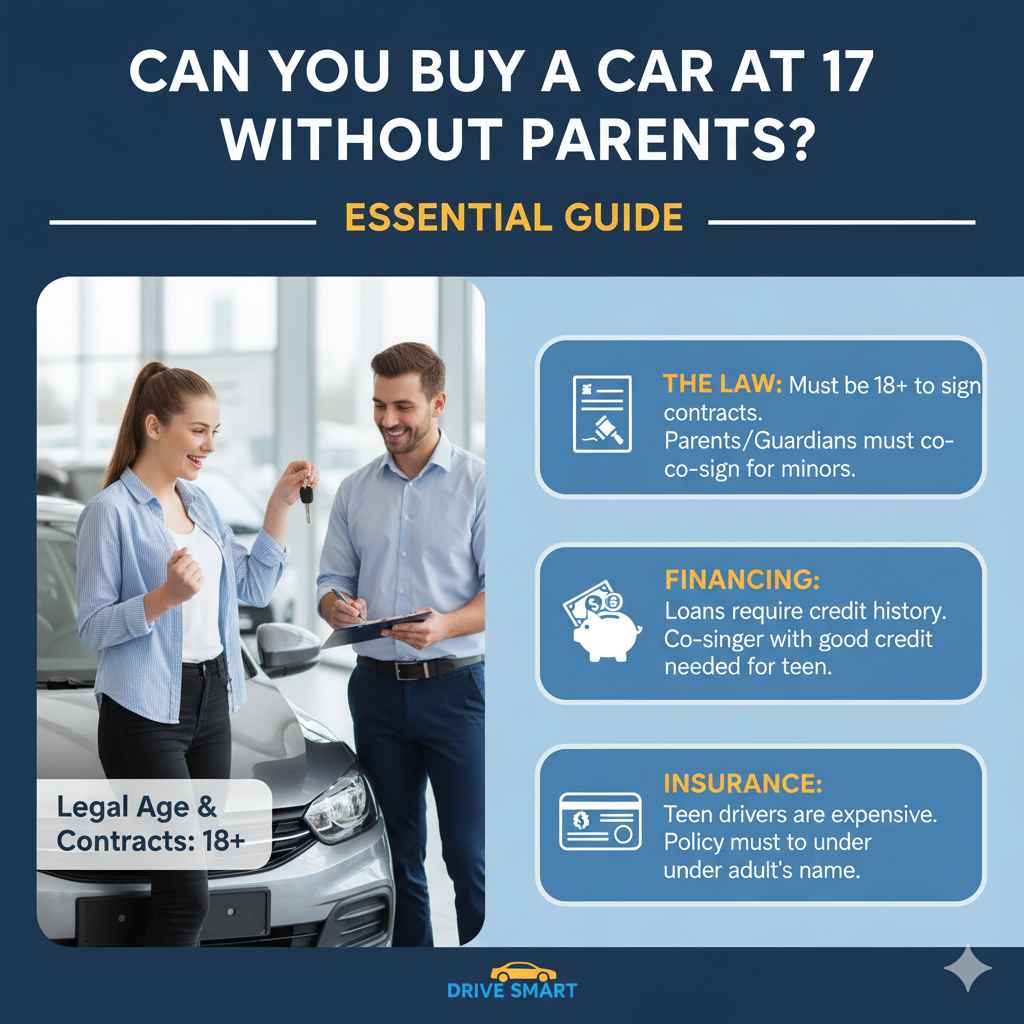

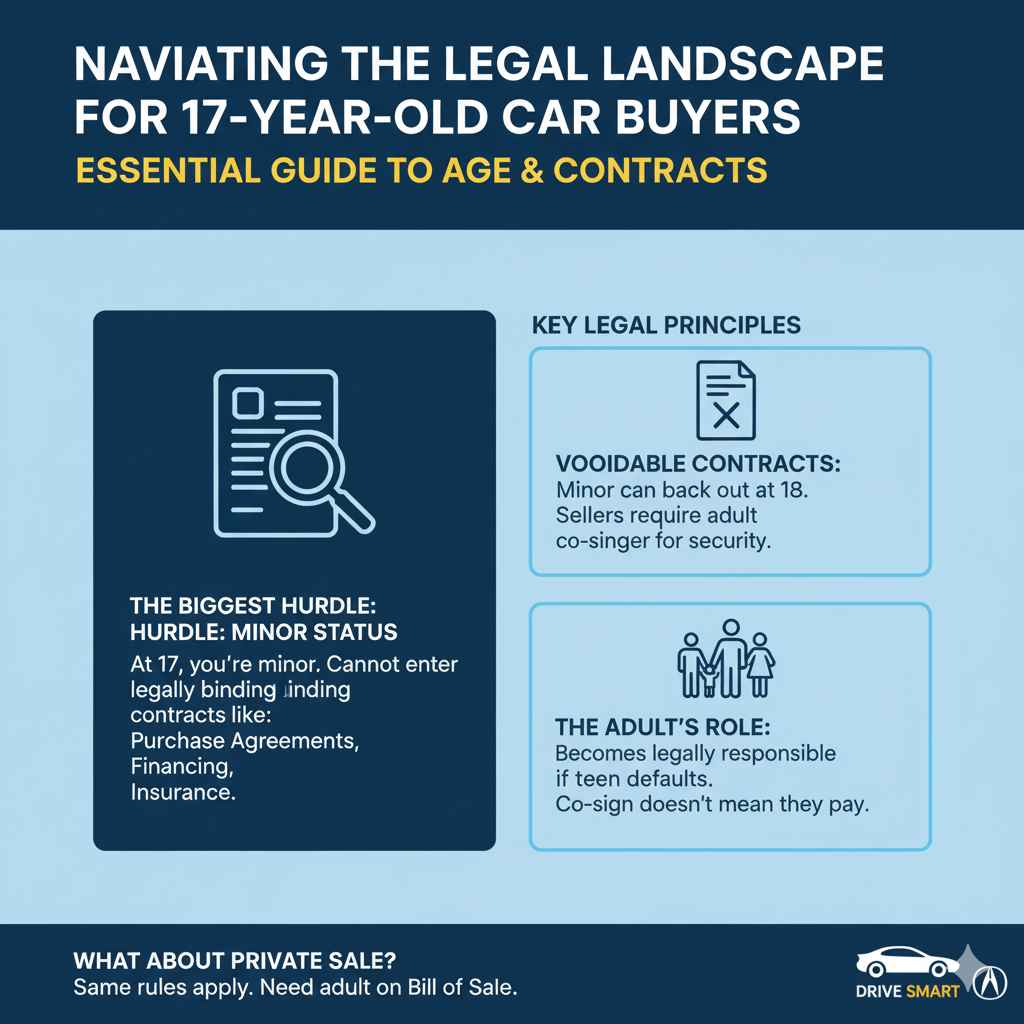

The biggest hurdle for a 17-year-old buying a car is that, in most places, you’re considered a minor. This means you generally can’t enter into legally binding contracts on your own. Think of it like signing a lease for an apartment or getting a credit card – these require you to be 18 or older. Buying a car involves a lot of contracts: the purchase agreement, financing agreements, and insurance policies. This is where depending on your parents or a legal guardian becomes crucial, even if they aren’t directly paying for the car.

Understanding Age Restrictions and Contracts

Legally, a contract signed by a minor is often “voidable.” This means the minor can choose to back out of the contract once they reach the age of majority (usually 18), and the other party might have no recourse. Dealerships and private sellers want to avoid this uncertainty. They need assurance that the sale is final and that the buyer is legally responsible for the terms of the sale, including loan payments and vehicle maintenance. Therefore, most sellers will require an adult (usually a parent or guardian) to co-sign any purchase or financing agreement.

This doesn’t mean your parents have to buy the car for you or even pay for it. Their role is primarily to provide the legal standing needed to complete the transaction. They become legally responsible if you default on payments or violate contract terms, which is why they’ll want to be involved in discussing your financial plan and the car choice.

What About Buying Privately?

Buying from a private seller might seem like a loophole, but the legal principles are the same. A private seller still needs to ensure the sale is legitimate and that they are transferring ownership to a legally responsible party. While a private sale might involve less paperwork than a dealership, the underlying contract requirements for a minor persist. You’ll likely still need an adult to sign the bill of sale and any related transfer documents.

Financing Your First Car at 17

Even if you have savings, many 17-year-olds don’t have the credit history needed to secure a car loan independently. This is another area where parental involvement is often necessary. Car loans are significant financial commitments.

Can You Get a Loan at 17?

Generally, no. Lenders need to ensure they are dealing with someone who is legally capable of entering into a loan agreement and who has a proven ability to repay. At 17, you typically haven’t had enough time to build the credit history or income verification that lenders require.

This is where a co-signer comes in. If your parent or guardian co-signs the loan with you, they are essentially vouching for your ability to repay. Their credit history and income will be used to qualify for the loan. This makes the lender more comfortable, but also means your co-signer is equally responsible for the debt.

Options for Financing with an Adult

- Parental Co-signer: This is the most common route. Your parent or guardian agrees to sign the loan application with you. They will need to meet the lender’s credit and income requirements.

- Personal Loan from Family: A less formal option is borrowing money directly from family members. Be sure to draw up a clear repayment agreement to avoid misunderstandings.

- Dealership Financing with Co-signer: Many dealerships have financing departments that work with various lenders. They can help guide you through the process of applying for a loan with a co-signer.

- Credit Unions: Sometimes, credit unions might offer more flexible options for young borrowers, especially if your parents are already members.

Building Your Own Credit (The Long Game)

While you might need help now, you can start building your own credit for future purchases. If your parents add you as an authorized user to their credit card with a good repayment history, or if you get a secured credit card yourself and use it responsibly, this can help establish a credit score over time. However, this won’t typically help you qualify for a car loan at 17 without a co-signer.

Insurance: A Non-Negotiable Requirement

Having car insurance is almost always legally required to drive on public roads. For anyone under 18, insurance companies also have specific rules that often involve a parent or guardian.

Insurance for Underage Drivers

Insurance companies view young drivers, especially those under 18, as higher risk due to lack of driving experience. This translates to higher premiums. Most insurance policies will require a parent or legal guardian to be listed on the policy for a minor driver. Sometimes, the policy is structured with the adult as the primary policyholder who then adds the young driver as a listed driver.

When you’re 17, you can’t legally hold an insurance policy in your own name in most states. Your parents will likely need to add you to their existing policy as a driver, or they will need to take out a new policy in their name with you as the listed driver.

Factors Affecting Premiums

- Age: Younger drivers pay significantly more.

- Driving Record: Any tickets or accidents dramatically increase costs.

- Type of Car: Sportier cars or those with high theft rates are more expensive to insure.

- Location: Urban areas with higher traffic and accident rates often have higher premiums.

- Coverage Levels: The amount of coverage you choose impacts the price.

Choosing the Right Car for a 17-Year-Old

As a young driver, your first car is a fantastic opportunity, but it’s wise to be practical. Focus on safety, reliability, and affordability rather than flashy features.

Prioritizing Safety and Reliability

When looking for a car, especially as your first vehicle, prioritize safety ratings. Excellent safety features can make a significant difference. Look for cars that perform well in crash tests. Websites like the National Highway Traffic Safety Administration (NHTSA) offer star ratings for new vehicles and safety information for older models.

Reliability is also key. You don’t want a car that’s always in the repair shop, especially when you’re managing your own expenses or relying on it for school or work. Researching the reliability ratings of different makes and models can save you a lot of headaches and money down the road. Consumer Reports and J.D. Power are great resources for this information.

Budget-Friendly Options

Consider cars that are known for being affordable to buy, insure, and maintain. Older, well-maintained sedans or smaller SUVs are often good choices.

| Car Type | Pros for Young Drivers | Cons for Young Drivers |

|---|---|---|

| Compact Sedans | Great fuel economy, lower insurance rates, easy to park. | Limited passenger and cargo space, can feel less substantial on the highway. |

| Small SUVs | Higher driving position, more cargo space, often good in varied weather. | Higher insurance costs and less fuel-efficient than sedans. |

| Older Reliable Sedans/Hatchbacks | Very affordable to purchase, often inexpensive to insure and repair (e.g., Honda Civic, Toyota Corolla). | May have fewer modern safety features, potential for age-related repairs. |

Pre-Purchase Inspection (PPI)

Before buying any used car, always get a pre-purchase inspection (PPI) from an independent mechanic. This costs a small fee but can save you thousands by identifying potential problems you might not see. It’s a crucial step for any buyer, and especially important when you might not have extensive mechanical knowledge yourself.

The Purchase Process: Step-by-Step

Successfully buying a car at 17 involves several steps, many of which will require adult assistance. Here’s a breakdown of what to expect:

- Budgeting: Determine how much you can realistically afford for the car purchase, monthly payments, insurance, fuel, and maintenance. This is where you’ll likely need to discuss this with parents to ensure everyone is on the same page, especially if they are co-signing or helping with costs.

- Saving for a Down Payment: A larger down payment can help you qualify for better loan terms or reduce the amount you need to borrow.

- Finding a Car: Research models that fit your budget, needs, and safety preferences. Look at dealerships, online marketplaces (like Manheim for dealer auctions or even general consumer sites), and private sellers.

- Securing Financing: If you need a loan, work with lenders or your parents to get pre-approved. This shows sellers you are a serious buyer.

- Test Drive & Inspection: Test drive the car thoroughly. If buying used, get a pre-purchase inspection from your own trusted mechanic.

- Negotiation: Negotiate the price. If you have a co-signer, they can be present and assist in this phase.

- Paperwork: This is where your parent or guardian will be essential. They will likely need to co-sign the purchase agreement, financing documents, and potentially the title transfer.

- Insurance: Ensure you have insurance coverage in place before you drive the car off the lot. Your parent will need to arrange this.

- Registration and Title: You and your parent will need to go to your local Department of Motor Vehicles (DMV) or equivalent agency to register the car and get the title in the appropriate name(s). Depending on your state, a minor may not be able to hold title alone, requiring an adult to be on the title as well.

Dealership vs. Private Sale

Each has its pros and cons:

| Aspect | Dealership | Private Seller |

|---|---|---|

| Price | Typically higher, but may include warranties or post-sale services. | Generally lower, more room for negotiation. |

| Financing | Easier to arrange loans, but interest rates can vary. | Cash purchase usually expected; financing requires separate arrangements. |

| Legal/Paperwork | Dealership handles most paperwork, but requires adult co-signing. | Buyer and seller handle paperwork; adult co-signing is still necessary for minors. |

| Vehicle Inspection | Cars often go through a dealer inspection, but a PPI is still recommended. | No guarantee on condition; PPI is highly recommended. |

Title and Registration

The process of transferring the title and registering the vehicle varies by state. You will likely need to visit your local DMV. Typically, any registered owner must be of legal age. If you are a minor, this means your parent or guardian will likely need to be listed on the title as a co-owner. This ensures legal ownership and responsibility. Proof of insurance is always required to register a vehicle.

Responsibilities of Car Ownership

Owning a car is more than just driving it. It comes with significant responsibilities. As a 17-year-old, learning these early will set you up for success.

Maintenance and Repairs

Regular maintenance is key to keeping your car running smoothly and preventing costly repairs. This includes:

- Oil Changes: Follow the manufacturer’s recommended interval (check your owner’s manual).

- Tire Rotations and Pressure: Keeps tires wearing evenly and improves fuel efficiency.

- Fluid Checks: Coolant, brake fluid, power steering fluid, and windshield washer fluid levels.

- Brake Inspections: Listen for squealing or grinding sounds.

- Battery Checks: Ensure terminals are clean and the battery is holding a charge.

When repairs are needed, having a trusted mechanic is invaluable. Many online resources can help you understand common issues and potential costs. Websites like RepairPal provide estimated repair costs for various makes and models.

Fuel, Parking, and Other Costs

Beyond the purchase price and loan payments, don’t forget about:

- Fuel: The cost of gasoline or diesel.

- Parking: Fees for parking at school, work, or in public areas.

- Tolls: If you’ll be using toll roads.

- Washing and Detailing: Keeping your car clean helps preserve its value.

- Unexpected Repairs: Always set aside some money for unforeseen issues.

Frequently Asked Questions

Q1: Can I legally buy a car in my name at 17?

Generally, no. Most states consider you a minor, and contracts for large purchases like cars require you to be 18. You will likely need an adult (parent or guardian) to co-sign or be involved in the ownership.

Q2: Do I need my parents to buy a car?

While you might be able to find a way to technically own it if an adult co-signs and is on the paperwork, you will almost certainly need your parents’ or a guardian’s help to sign financing agreements, insurance policies, and potentially the title. They are legally responsible if you can’t meet the contract’s obligations.

Q3: What if my parents refuse to help?

If your parents are unwilling to co-sign for a loan, insurance, or be involved in the purchase, buying a car independently at 17 becomes extremely difficult, if not impossible, due to legal and financial restrictions. You may need to wait until you turn 18.