How Many Car Payments Missed before Repossession: Crucial Insights

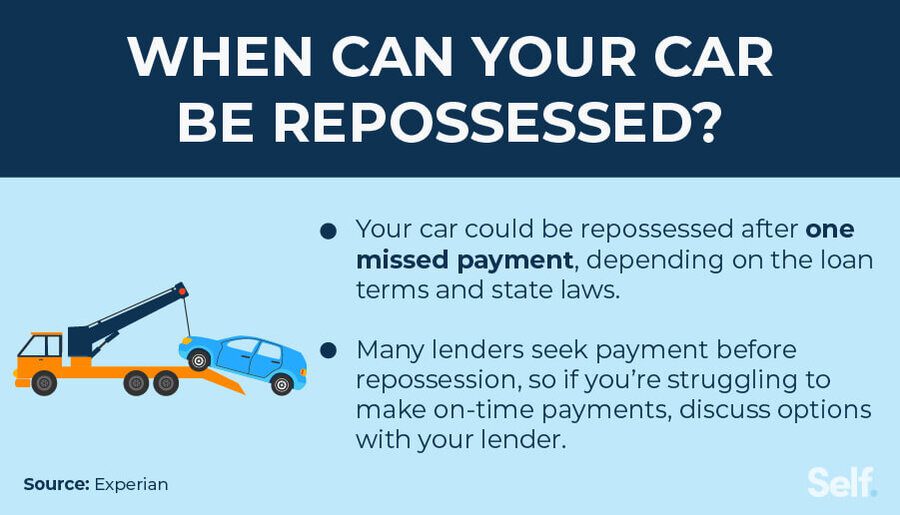

You might wonder how many car payments you can miss before repossession happens. Generally, missing two to three payments may lead to your car being repossessed.

This varies by lender and loan agreement. Owning a car is essential for many, providing freedom and mobility. But financial troubles can make keeping up with payments tough. Understanding the repossession process can help you manage your finances better. It’s crucial to know how many payments you can miss and what steps to take if you fall behind.

This knowledge can save you from losing your vehicle and facing credit issues. In this blog, we’ll explore the factors that determine repossession timelines and provide tips to avoid it. Stay informed and protect your vehicle.

Credit: www.self.inc

Repossession Process

Missing car payments can lead to trouble. First, you get reminder calls or letters. The lender may contact you to discuss the issue. They want to help you avoid repossession.

Payments are important. Missing too many can hurt your credit score. It can also lead to losing your car. Stay in touch with your lender to find a solution.

If you keep missing payments, the lender may start legal action. They will follow legal steps to take back the car. This is called repossession. The number of missed payments before this happens can vary.

Usually, after three missed payments, the process begins. Laws differ by state, so check your local rules. You may receive a notice. This gives you a chance to pay and keep your car. Act quickly to avoid losing it.

Credit: www.creditninja.com

Financial Implications

Missing car payments can hurt your credit score. Each missed payment stays on your credit report. This can lower your score. A low credit score makes it hard to get loans. It can also lead to higher interest rates. Keeping up with payments is very important. Your credit score depends on it.

Late payments often come with extra charges. Lenders may add late fees to your account. These fees can add up quickly. Repossession also has costs. You may need to pay for towing and storage. All these fees make it harder to catch up on payments. It is best to avoid missing payments.

Grace Periods

Lender Policies can vary. Some lenders allow a few days. Others may give weeks. It’s important to know your lender’s rules. Missing payments can hurt your credit score. Always check your loan agreement. It will tell you the grace period.

State Regulations differ across the country. Some states have strict rules. Others are more lenient. Many states require notices before repossession. These notices warn you about missed payments. Understanding state laws can help you avoid surprises. Check your state’s rules for more details.

Credit: obryanlawoffices.com

Preventive Measures

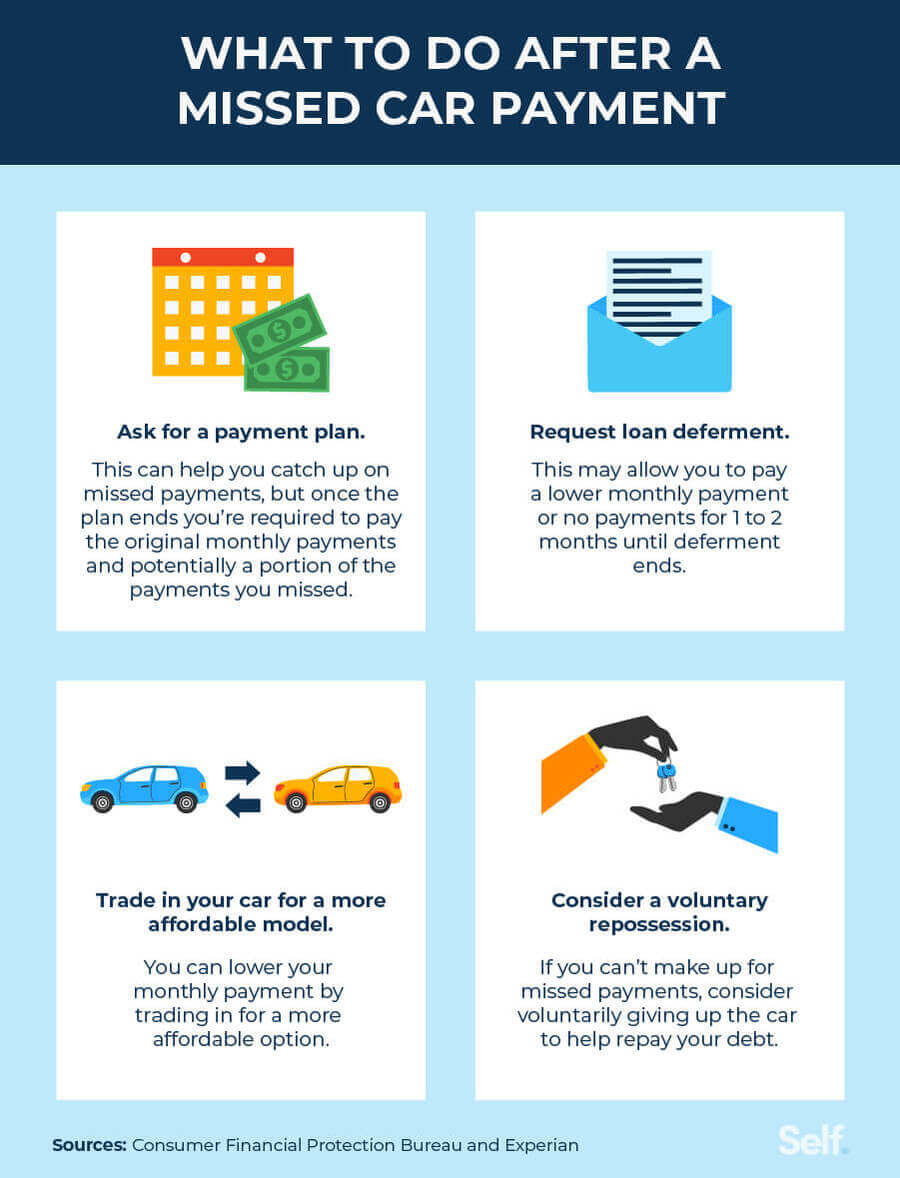

Loan modification can help if struggling with payments. Lenders may change terms to lower monthly costs. This can include reducing the interest rate or extending the loan term. Modified loans can make payments easier. Always talk to your lender about options.

Refinancing means getting a new loan to replace the old one. This can lower monthly payments. New loan terms can be more favorable. It might extend the repayment period or lower the interest rate. Refinancing can prevent missing payments. Check with your bank or financial advisor for options.

Communication With Lenders

Missing car payments can lead to repossession. Lenders often initiate repossession after two or three missed payments. Communication with lenders is crucial to avoid this situation.

Proactive Steps

It is important to talk to your lender early. Let them know if you have trouble paying. Honesty is key. Explain your situation. Lenders may offer helpful options. They could give you more time to pay. Or they might adjust your payment plan. Acting fast can prevent serious issues.

Negotiation Tactics

Try to negotiate with your lender. Ask if you can lower your payments. See if they will reduce fees or interest. Offer to pay a part of the debt. This shows you are trying. Stay calm and polite. Good communication can lead to a better deal. It can help you keep your car.

Alternative Solutions

If you can’t make your car payments, selling the car is an option. This can help you avoid repossession. You can use the money from the sale to pay off the loan. This may stop the damage to your credit score. Selling the car yourself often brings more money than trading it in. This extra money can help you pay off other bills too. Make sure to let your lender know about your plan.

Voluntary repossession means you give the car back to the lender. This may seem scary, but it can be better than having the car taken away. This way, you avoid extra fees. Tell the lender you want to do this. Make sure to return the car in good condition. This can reduce the amount you owe. Your credit score will still be affected, but it may be less severe.

Legal Rights

Missing two to three car payments can lead to repossession. Lenders may start the process after 60-90 days of non-payment. Keeping communication open with the lender can sometimes help avoid this outcome.

Consumer Protections

Knowing your rights can help you avoid losing your car. Lenders must follow the law before they can repossess your vehicle. They can’t take your car without notice in most cases. State laws may give you extra protections. Always check your local laws.

Repossession Laws

Repossession laws vary by state. Some states need court approval. Others allow self-help repossession. This means the lender can take the car without going to court. Missed payments can lead to this action. Usually, a lender will act after three missed payments. But some states let them act sooner. Know your state’s rules to protect yourself.

Long-term Consequences

Missing car payments can affect your credit score. A low score makes it hard to get future loans. Banks see you as a high-risk borrower. This can lead to higher interest rates or loan denial. Even if you get a loan, it may have strict terms.

Repossession impacts your financial status. You may need to pay extra fees. This can delay your financial recovery. It’s important to make a plan to recover. Pay off debts as soon as you can. Save money for unexpected expenses. Over time, you can improve your credit score. This will help you in future.

Frequently Asked Questions

How Long After A Missed Car Payment Before Repossession?

Repossession can begin as soon as one missed payment, depending on the lender’s policy. Typically, it happens after 60-90 days.

What Happens If You Are 3 Months Behind On Your Car Payment?

Your car may be repossessed. Late fees and damage to your credit score can occur. Contact your lender immediately.

How Do I Know When My Repo Is Coming?

Check your repo’s tracking number for updates. Visit the carrier’s website or app to see the estimated delivery date.

How Long Before They Stop Trying To Repo Your Car?

Car repossession timelines vary by state. Lenders typically stop trying to repossess after the debt is resolved. Check local laws.

Conclusion

Missing car payments can lead to repossession. Stay informed about your lender’s policies. Communicate with them if you’re struggling. It’s important to act early. Avoiding repossession protects your credit. Seek help if needed. Financial advice can be beneficial. Take charge of your car payments.