How Paying Off A Car Loan Affects Your Credit Score

We’ll break down exactly how paying off your car loan can change your credit picture. You’ll learn what to expect and how to keep your credit looking good. This isn’t about magic numbers; it’s about understanding how loans work with your credit history. Let’s dive in.

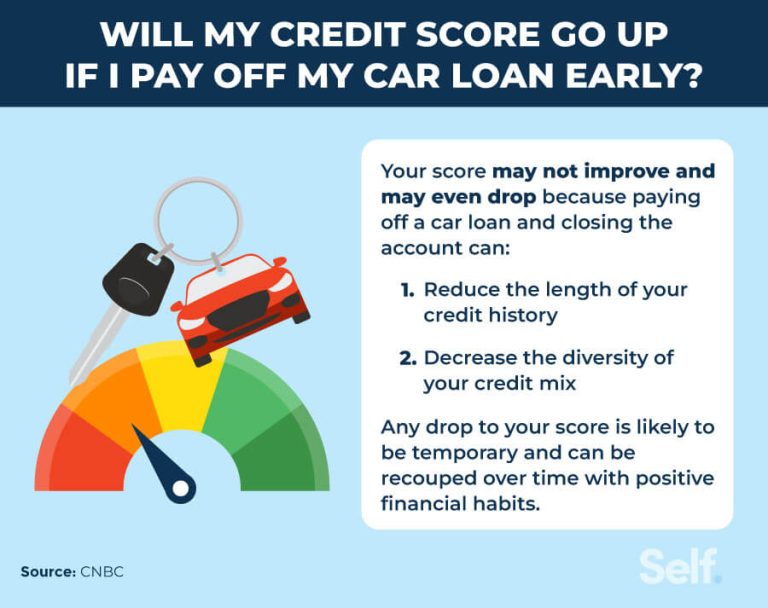

Paying off a car loan is generally a positive step for your credit score. It shows you’re responsible. However, it can cause a small, temporary dip. This happens because your credit mix changes and the loan’s positive payment history is no longer actively building your score. The long-term effect is usually beneficial.

Understanding Your Credit Score After a Loan Is Paid

Your credit score is like a snapshot of your financial health. It tells lenders how likely you are to repay borrowed money. Several factors go into this score. Think of them as puzzle pieces that fit together.

When you pay off a car loan, some of these puzzle pieces shift. It’s not usually a bad thing, but it can be a change. We need to look at how each part of your credit score is affected. This helps us understand the full picture.

The Impact on Credit Mix

One of the key factors in your credit score is your credit mix. This means having different types of credit accounts. Lenders like to see you can handle various kinds of debt responsibly.

Examples include credit cards, student loans, mortgages, and car loans. A car loan is considered an installment loan. These have fixed payments over a set time. Credit cards are revolving credit. They have no set end date and can be used over and over.

When your car loan is paid off, it’s no longer part of your active credit mix. This can be a slight negative. If your car loan was your only installment loan, your credit mix becomes less diverse. Lenders might see this as a minor risk.

Credit Mix: What Lenders Look For

Why it matters: Shows you can manage different types of debt.

Types of credit:

- Installment Loans: Car loans, student loans, mortgages. Fixed payments.

- Revolving Credit: Credit cards, home equity lines of credit. Flexible limits.

Effect of paying off a loan: Reduces the variety of credit accounts you actively manage.

How Payment History Still Matters

Your payment history is the biggest piece of your credit score puzzle. It shows if you pay bills on time. Making every car loan payment on time is a huge plus for your credit. This builds a strong history of reliability.

Even after the loan is paid off, those on-time payments stay on your credit report. They will continue to help your score for years. This positive history is what lenders want to see. It proves you are a good borrower.

The account will simply show as “paid in full” or “closed by consumer.” It doesn’t disappear from your report overnight. This means the good work you did will continue to be recognized.

The Age of Your Credit Accounts

The length of time you’ve had credit accounts open also affects your score. A longer credit history generally looks better. It gives lenders more data to assess your behavior over time.

When you pay off a car loan, the account might be closed by the lender or by you. If it’s closed, it stops contributing to the “average age of accounts” calculation. This could slightly lower the average age of your open credit lines.

However, the good news is that closed accounts with a positive payment history often continue to benefit your score for a while. They remain on your report for up to 10 years. This means their positive influence doesn’t vanish instantly.

Your Credit Report Timeline

What stays:

- All past on-time payments.

- The fact that the loan was paid in full.

- Late payments (if any) for up to 7 years.

- The loan account itself for up to 10 years.

What changes:

- The account no longer shows an active balance.

- It may no longer contribute to the average age of open accounts.

The Average Credit Utilization Ratio

Credit utilization is the amount of credit you use compared to your total available credit. It’s usually most important for credit cards. For example, if you have $10,000 in credit card limits and owe $3,000, your utilization is 30%.

A car loan doesn’t directly factor into your credit utilization ratio as calculated by most scoring models. This is because it’s an installment loan with a set payoff date. You don’t “use up” credit in the same way you do with a credit card.

So, paying off a car loan typically has no direct impact on your credit utilization ratio. This is a relief for many people. You don’t have to worry about this specific aspect changing negatively.

Potential for a Small, Temporary Dip

It’s true that sometimes, a credit score might drop a few points right after a loan is paid off. This is usually not a cause for alarm. It’s often due to the factors we’ve discussed.

The most common reasons for a small dip are the changes in your credit mix and the age of your accounts. If the loan was a significant part of your credit history, its closure can feel like a bigger adjustment for the scoring models.

Think of it like a popular book being removed from a library shelf. It was there, people used it, and now it’s gone. The shelf looks a bit different. But all the other books are still great!

When a Score Dip Might Happen

Scenario: You only had one installment loan (your car) and a couple of credit cards.

Why a dip could occur:

- Credit Mix Change: You lose your only installment loan.

- Age of Accounts: The loan’s closure lowers the average age of your credit.

Important: This is usually temporary and small. Your positive payment history still counts.

My Own Car Loan Payoff Story

I remember the day I made the final payment on my first car. It was a used sedan, and I’d saved up for a good down payment. The loan felt like a mountain for a few years. I made every payment, sometimes early, just to get it done faster.

When the final amount hit my bank account and the lender confirmed it was paid, I felt a huge rush of relief. I checked my credit report a few weeks later, expecting a score jump. Instead, I saw a small, unexpected drop of about 5 points.

Panic! I thought I’d done something wrong. But I remembered reading about credit mix. My car loan was my only installment loan. The other accounts were just credit cards. It made sense that the models saw a change. The good news? Within three months, my score climbed back up and then kept going.

It taught me that credit scores are dynamic. They aren’t set in stone. A temporary change, especially a small one after a positive action like paying off debt, is usually not a long-term problem. The positive history of paying that loan diligently was still the most important factor. It’s a lesson I often share because many people fear these minor shifts.

What Happens to the Account on Your Credit Report?

Once your car loan is fully paid off, the account status will change on your credit report. You’ll see it update from “open” or “current” to “paid in full” or “closed by consumer” (if you closed it) or “closed by lender.”

The important part is that the history associated with that account remains. This includes all your on-time payments. It also includes the original loan amount and the date it was opened.

This information doesn’t vanish. It continues to be part of your credit history. This is why responsible repayment is so crucial. It builds a foundation that supports your score over time, even after the account is no longer active.

Account Status After Payoff

Look for these updates:

- Original Creditor: Name of the bank or finance company.

- Account Type: Auto Loan.

- Loan Amount: The original principal.

- Date Opened: When you first got the loan.

- Payment History: Shows all your monthly payments (hopefully all on time!).

- Status: Will update to “Paid in Full,” “Closed,” or similar.

- Balance: Will show $0.

Duration on report: The account details typically stay for up to 10 years.

The Long-Term Benefits

While there might be a small, temporary fluctuation, paying off a car loan has significant long-term benefits for your creditworthiness.

Firstly, it means you have one less debt obligation. This can improve your debt-to-income ratio, which many lenders consider. A lower debt burden signals financial stability. It shows you are not over-extended.

Secondly, it demonstrates a commitment to fulfilling financial obligations. Consistently paying off loans builds a strong track record. This positive history is invaluable when you need to apply for future credit, like a mortgage or a personal loan.

Finally, being debt-free is a powerful feeling. While not directly tied to your credit score, it frees up your finances. You can then use that money for savings, investments, or other goals. This financial freedom indirectly supports good credit habits.

What If You Had Late Payments?

If your car loan had late payments, paying it off completely is still a good thing. It stops new negative marks from appearing on your report for that loan.

However, those late payments will remain on your credit report for seven years. They will continue to negatively impact your score during that time. Paying it off doesn’t erase past mistakes.

The key is to focus on making all future payments on time for your other accounts. Over time, the impact of older negative marks lessens as positive history builds up. A paid-off loan, even with past issues, is better than an active loan with ongoing problems.

Past Late Payments on Car Loans

The reality: Late payments stay on your report for 7 years.

Impact: They can significantly lower your score.

Paying off the loan:

- Stops new negative reporting for that loan.

- Does NOT remove past late payment history.

- It is still better to pay off than to let it go into default.

Focus on: Building positive history on other accounts moving forward.

When Is It Okay to Close the Account?

Generally, it’s best not to rush to close a credit account just because it’s paid off. If the account is from a lender that doesn’t charge an annual fee, leaving it open can be beneficial.

An open, zero-balance account still contributes to your overall available credit. This helps your credit utilization ratio, especially if you have credit card balances. It also keeps the age of that account on your report for longer.

However, if the lender charges an annual fee for an open, paid-off loan, it might be wise to close it. You don’t want to pay fees for something that isn’t actively helping you.

Monitoring Your Credit After Payoff

It’s always a good idea to keep an eye on your credit report. After paying off your car loan, take a moment to review your report from all three major bureaus: Equifax, Experian, and TransUnion.

You can get a free copy of your credit report annually from each bureau at AnnualCreditReport.com. Look for the car loan account and ensure its status is updated correctly to “paid in full” or “closed.”

Also, check that there are no unexpected errors or new accounts you don’t recognize. This helps you catch any potential issues early and maintain accurate credit information.

Credit Monitoring Checklist

Where to check: AnnualCreditReport.com (free annual reports)

What to look for:

- Car Loan Status: Is it marked “Paid in Full”?

- Zero Balance: Is the balance $0?

- Account Age: Does it still show up and contribute to credit history length?

- Any Errors: Are there any incorrect late payments or open balances?

- New Unknown Accounts: Are there any accounts you didn’t open?

Frequency: Check at least once a year, or after major credit events like paying off a loan.

Real-World Scenarios and Their Effects

Let’s look at a few different situations to see how paying off a car loan plays out for different people.

Scenario 1: Young Adult with Limited Credit

Someone in their early twenties might have a car loan as their primary or only credit account. Paying it off would remove their only installment loan. This could cause a more noticeable dip in their score than for someone with a diverse credit history. They would then need to focus on building credit with other tools like secured credit cards.

Scenario 2: Homeowner with Diverse Credit

A person who owns a home, has a mortgage, student loans, and several credit cards, and then pays off their car loan, might see very little change. Their credit mix is already strong. The car loan was just one piece of a larger, diverse credit profile. The impact would likely be minimal and temporary.

Scenario 3: Individual Focused on Debt Reduction

Someone who aggressively pays off all their debts, including their car loan, is demonstrating strong financial discipline. Even if their credit mix changes, the fact they are consistently paying off obligations demonstrates responsibility. This pattern is viewed positively by lenders in the long run, especially for large loans like mortgages.

Credit Score Impact Comparison

Factor: Credit Mix Diversity

Impact on Score (High): If car loan was your only installment loan.

Impact on Score (Low): If you have other installment loans (mortgage, student loan).

Factor: Length of Credit History

Impact on Score (High): If car loan was one of your oldest accounts.

Impact on Score (Low): If you have many older credit accounts.

What This Means for Your Future Borrowing

Paying off your car loan is a positive step. It means you have less debt. This can make you a more attractive borrower for future loans.

For instance, when you apply for a mortgage, lenders will look at your debt-to-income ratio. Having fewer monthly payments from loans like your car loan will lower this ratio. This can increase your chances of getting approved and possibly getting a better interest rate.

It also shows lenders you can manage a loan responsibly from start to finish. This track record of on-time payments is gold for your credit file. It builds confidence for them to lend you more money in the future.

When to Worry (And When Not To)

You generally don’t need to worry about paying off your car loan. It’s a responsible financial action. The potential small score dip is usually temporary and a sign of change, not failure.

You should worry if you notice a significant drop in your score (more than 10-15 points) after paying off the loan. This could indicate an error on your credit report or an issue with how the account was closed.

Also, worry if you are planning to apply for a major loan soon (like a mortgage) and the temporary dip from your car loan payoff happens right before your application. It might be worth waiting a month or two for your credit score to stabilize.

Signs of Trouble vs. Normal Changes

Normal Change:

- Small, temporary credit score drop (a few points).

- Account status correctly shows “Paid in Full.”

- Your overall credit history remains strong.

Cause for Concern:

- Large credit score drop (10+ points).

- Incorrect negative marks appear (e.g., new late payments).

- The account is missing or shows an incorrect balance.

- You see new accounts you didn’t open.

Action: Immediately review your credit report and dispute any errors.

Quick Tips for Managing Credit Post-Car Loan

After your car loan is paid off, here are a few simple things to keep in mind for your credit health.

Keep Credit Cards Active: If you have credit cards, make sure to use them for small, regular purchases. Pay them off in full each month. This keeps your revolving credit active and your utilization low.

Consider a New Installment Loan (Carefully): If you feel your credit mix is lacking and you can afford it, consider a small, manageable installment loan for a future purchase. However, only do this if you genuinely need it and can easily make payments. Don’t take on debt just for the sake of your credit mix.

Maintain Good Habits: Continue paying all your bills on time. Avoid applying for too much new credit at once. These are timeless rules for good credit.

Frequently Asked Questions

Will paying off my car loan hurt my credit score significantly?

No, it usually does not. You might see a very small, temporary dip in your score. This is often due to changes in your credit mix or the age of your accounts.

The positive history of paying off the loan is more important long-term.

How long does it take for my credit score to recover after paying off a car loan?

If there’s a small dip, your score often recovers within one to three months. This depends on your overall credit profile and how other accounts are managed.

Should I close my car loan account after I pay it off?

It’s usually best to keep it open if there’s no annual fee. An open, zero-balance account contributes to your available credit and credit history length. Only close it if there’s a fee or if you’re trying to simplify your accounts.

Does a paid-off car loan stay on my credit report forever?

No. Paid-off installment loans, like car loans, typically remain on your credit report for up to 10 years after they are closed. They continue to show your positive payment history during that time.

What is a credit mix and why does it matter when my car loan is paid off?

Credit mix refers to the different types of credit you have (e.g., credit cards, installment loans). Having a mix shows you can manage various debts. When a car loan (an installment loan) is paid off, your mix becomes less diverse, which can slightly impact your score.

What if I had late payments on my car loan? Does paying it off help?

Paying off a loan with late payments stops new negative reporting for that account. However, the late payment history will remain on your report for seven years and continue to affect your score during that period.

Final Thoughts on Your Credit Journey

Paying off your car loan is a milestone. It’s a sign of financial progress and responsibility. While your credit score might see a tiny wobble, it’s usually a temporary one. The long-term impact is overwhelmingly positive.

Focus on the fact that you’ve successfully managed and repaid a significant debt. Keep practicing good credit habits, and your score will reflect your continued commitment to financial health.