How to Afford Your Dream Car: Proven Guide

To afford your dream car, create a detailed budget, explore financing options like loans and leases, consider a down payment, and maintain good credit. Prioritize saving, potentially by cutting expenses or increasing income. Researching car values and insurance costs beforehand is also key.

We’ve all been there – that moment you see it. The perfect car. It gleams under the sun, its engine hums a sweet melody, and you just know it’s the one. But then reality hits: how on earth can you afford that dream car? It can feel like an impossible mountain to climb, leaving you frustrated and staring longingly at the showroom window. Don’t let that feeling stop you! With a smart plan and a little dedication, making your dream car a reality is absolutely within reach. This guide will break down exactly how you can bridge the gap between your current situation and cruising in your dream ride.

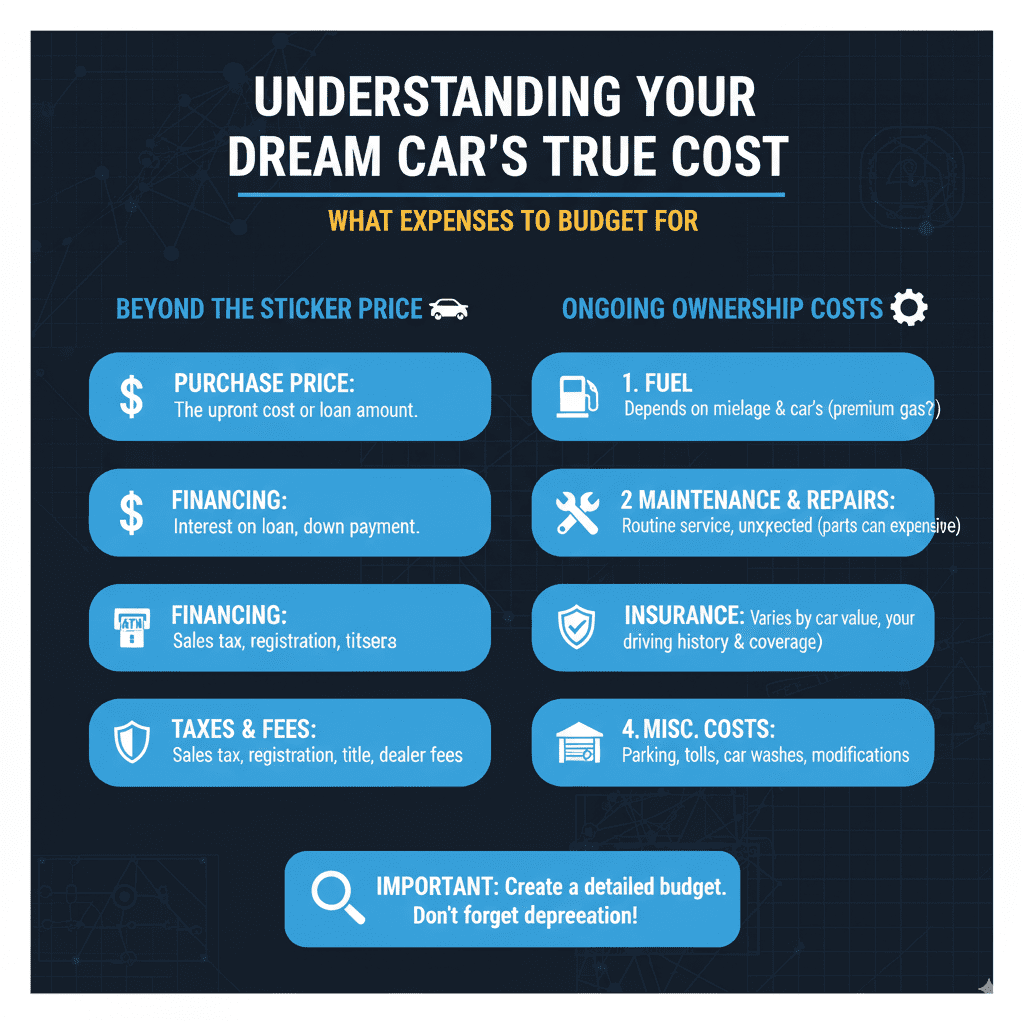

Understanding Your Dream Car’s True Cost

Before you even think about signing any papers, you need to get a clear picture of what your dream car will really cost you. It’s not just the sticker price. We need to consider all the expenses that come with owning a car, especially a dream one that might be newer, higher-performance, or simply more luxurious than your current vehicle.

The Sticker Price Isn’t the Whole Story

That number on the windshield is just the beginning. Think about:

- Base Price: The manufacturer’s suggested retail price (MSRP).

- Optional Features: Leather seats, sunroof, premium sound system – these all add up!

- Taxes and Fees: Sales tax, registration fees, documentation fees, and more can add a significant chunk. Check your local government’s website for tax rates. For example, the U.S. government provides general information on taxes.

- Delivery Charges: Some dealerships charge a fee for transporting the car.

Ongoing Ownership Costs

These are the expenses you’ll face month after month, year after year:

- Insurance: This is crucial. More expensive cars often cost more to insure. Get quotes before you buy!

- Fuel: Consider the car’s MPG (miles per gallon) and your typical driving habits.

- Maintenance and Repairs: Luxury or performance cars can have higher maintenance costs. Research common issues and service intervals for the specific model you want.

- Registration and Inspection: Annual fees to keep your car legal on the road.

Step 1: Budgeting is Your Best Friend

This is where we get practical. A solid budget is the foundation for affording anything significant, especially a car.

Assess Your Current Financials

Take an honest look at where your money is going right now. You’ll need to know:

- Your Income: How much money do you bring home after taxes each month?

- Your Expenses: List everything you spend money on – rent/mortgage, utilities, groceries, debt payments, entertainment, savings, etc.

Create a Realistic Car Budget

Based on your income and expenses, decide how much you can realistically afford for a monthly car payment, insurance, and gas. A good rule of thumb is that your total car expenses (loan payment, insurance) shouldn’t exceed 10-15% of your take-home pay. Some people even suggest keeping it below 10% to be truly comfortable. Use a budget calculator or spreadsheet to track this. A great resource for understanding budgeting principles can be found through organizations like the Consumer Financial Protection Bureau.

Saving for a Down Payment

A larger down payment means a smaller loan, lower monthly payments, and potentially less interest paid over time. Aiming for at least 10-20% of the car’s price is a smart goal.

| Car Price | 10% Down Payment | 20% Down Payment |

|---|---|---|

| $30,000 | $3,000 | $6,000 |

| $40,000 | $4,000 | $8,000 |

| $50,000 | $5,000 | $10,000 |

Step 2: Boost Your Savings Power

Now that you know how much you need to save, let’s find ways to accelerate that process.

Cut Unnecessary Expenses

Go through your budget with a fine-tooth comb. Are there subscriptions you don’t use? Dining out too often? Impulse buys? Even small cuts add up significantly over time.

- Cancel unused gym memberships.

- Reduce impulse shopping.

- Pack lunches instead of buying them.

- Find free or low-cost entertainment options.

Increase Your Income

Can you earn extra money? Consider:

- A Side Hustowww: Freelancing, driving for a rideshare service, selling crafts, or tutoring.

- Asking for a Raise: If you’ve been performing well at your current job, prepare a case and ask your manager for a salary increase.

- Selling Unused Items: Declutter your home and sell items you no longer need online or at a yard sale.

Automate Your Savings

Set up automatic transfers from your checking account to a dedicated savings account for your dream car fund. “Set it and forget it” makes saving much easier.

Step 3: Improve Your Credit Score

Your credit score is a huge factor in getting approved for a car loan and for the interest rate you’ll pay. A higher score opens doors to better loan terms, saving you thousands of dollars in interest over the life of the loan.

What is a Credit Score?

A credit score is a three-digit number that lenders use to assess your creditworthiness – how likely you are to repay borrowed money. Scores typically range from 300 to 850. Check your credit report annually from the three major credit bureaus (Equifax, Experian, and TransUnion) for free at AnnualCreditReport.com.

How to Improve Your Credit

- Pay Bills on Time, Every Time: Payment history is the most significant factor in your credit score.

- Reduce Credit Card Balances: Keep your credit utilization low (ideally below 30% of your credit limit).

- Don’t Open Too Many New Accounts at Once: This can temporarily lower your score.

- Dispute Errors: If you find any mistakes on your credit report, dispute them immediately.

Step 4: Explore Financing Options

Once you have a solid savings plan and a good credit score, it’s time to look at how you’ll finance the bulk of the car’s price.

Car Loans

A car loan is the most common way to finance a vehicle. You borrow money from a bank, credit union, or dealership and repay it with interest over a set period (loan term).

- Dealership Financing: Convenient, but sometimes not the best rates.

- Banks and Credit Unions: Often offer competitive rates, especially if you have an existing relationship.

- Online Lenders: Can provide pre-approval quickly, but compare rates carefully.

Leasing a Car

Leasing means you’re essentially renting the car for a set period (usually 2-4 years). Your monthly payments are typically lower than a loan because you’re only paying for the depreciation of the car during your lease term.

Pros of Leasing:

- Lower monthly payments.

- Drive a new car every few years.

- Less hassle with selling the car later.

- Often includes maintenance packages.

Cons of Leasing:

- No ownership equity – you don’t own the car at the end.

- Mileage restrictions – exceeding them incurs hefty fees.

- Less freedom for customization.

- Wear and tear charges can apply at lease end.

Securing Pre-Approval

Before you even step into a dealership, get pre-approved for a car loan. This tells you exactly how much you can borrow and at what interest rate. It gives you negotiating power and prevents you from falling in love with a car you can’t afford.

| Financing Method | Who it’s Best For | Key Consideration |

|---|---|---|

| Car Loan (Buying) | Those who want to own the car long-term and build equity. | Monthly payment amount and total interest paid. |

| Leasing | Those who want lower monthly payments, a new car every few years, and don’t mind mileage limits. | Mileage limits, wear and tear fees, and end-of-lease options. |

Step 5: Smart Shopping and Negotiation

You’ve done the groundwork. Now it’s time to find your dream car at the best possible price.

Research, Research, Research!

Know the exact make, model, and trim level you want. Understand its market value. Websites like Kelley Blue Book (KBB) and Edmunds provide pricing guides and reviews.

Consider Used or Certified Pre-Owned (CPO)

A car loses a significant portion of its value in the first few years. Buying a gently used or CPO vehicle can save you tens of thousands of dollars compared to buying new, while still offering reliability. CPO vehicles typically come with extended warranties and have passed rigorous inspections.

Shop Around at Different Dealerships (and Online)

Don’t feel pressured to buy from the first place you visit. Get quotes from multiple dealerships. Also, explore online car retailers like Carvana or Vroom, which can offer competitive pricing and home delivery.

Negotiate with Confidence

Once you’ve secured pre-approval, you have the upper hand. Negotiate the out-the-door price, which includes all taxes and fees. Focus on the final number, not just the monthly payment. Your pre-approved loan rate is your benchmark; if the dealership can’t beat it, use your own financing.

Step 6: Maintaining Your Dream Car

Congratulations, you’ve got your dream car! Now, let’s talk about keeping it running smoothly and affordably.

Follow the Maintenance Schedule

Your owner’s manual is your best friend. Regular oil changes, tire rotations, and scheduled check-ups prevent minor issues from becoming costly repairs. Many newer cars even have maintenance reminders built into the dashboard.

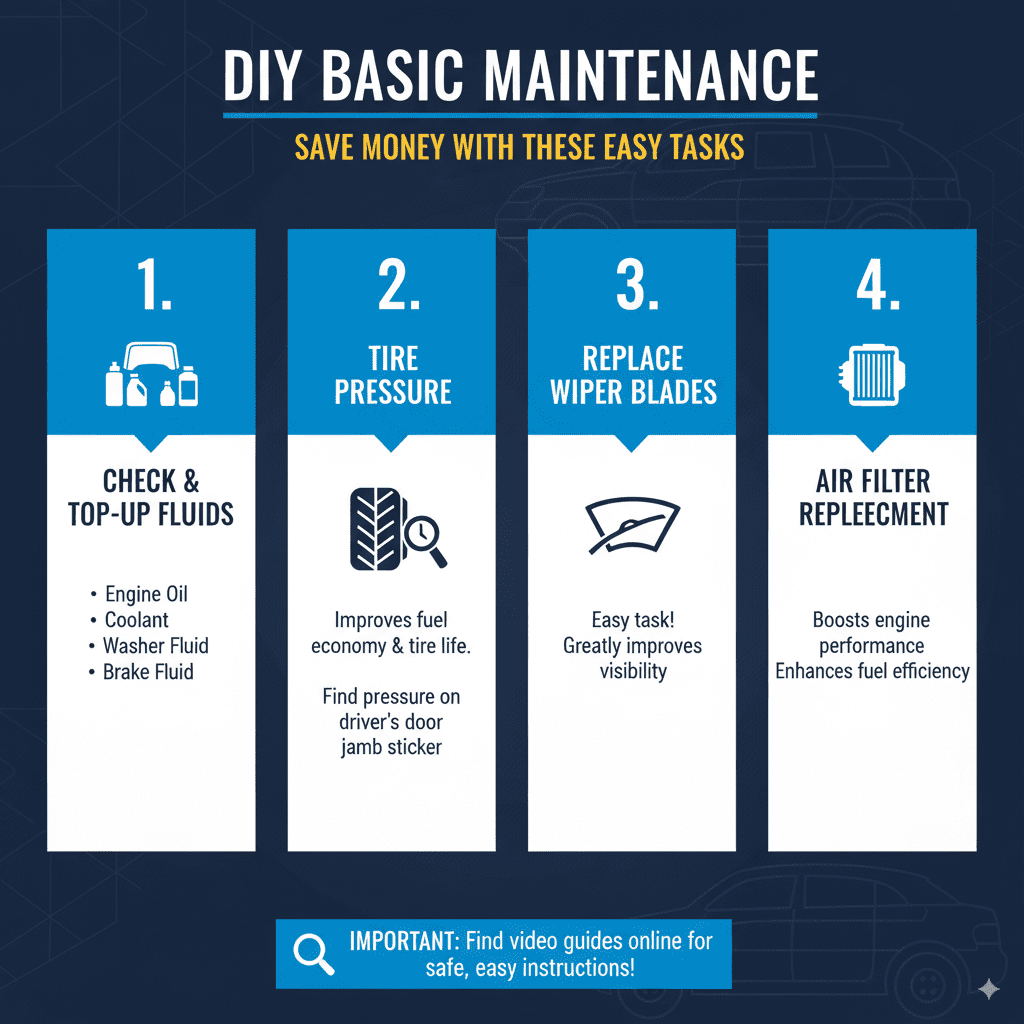

DIY Basic Maintenance

There are many simple maintenance tasks you can learn to do yourself, saving money on labor costs. These include:

- Checking and Topping Up Fluids: Engine oil, coolant, windshield washer fluid, and brake fluid.

- Tire Pressure: Properly inflated tires improve fuel economy and tire life. Look for the recommended pressure on a sticker inside your driver’s side door jamb.

- Replacing Wiper Blades: A quick and easy task that greatly improves visibility.

- Air Filter Replacement: This affects engine performance and fuel efficiency.

There are countless videos and guides available online to show you how to do these tasks safely. For instance, a reputable resource for DIY car maintenance info could be found on automotive enthusiast sites or manufacturer support pages.

Find a Trusted Independent Mechanic

While dealerships offer specialized knowledge, independent mechanics often provide more affordable service. Ask friends for recommendations or look for mechanics with good online reviews and certifications like ASE (Automotive Service Excellence).

Frequently Asked Questions (FAQ) About Affording Your Dream Car

Q1: Is buying my dream car worth the financial strain?

A1: This is a personal decision. While it’s great to enjoy your dream car, it’s essential that it doesn’t put you in a position of constant financial stress. Ensure your budget can comfortably handle all ownership costs without sacrificing other important financial goals like saving for retirement or an emergency fund.

Q2: How much of a down payment should I aim for?

A2: Aiming for at least 10-20% of the car’s price is a good goal. A larger down payment reduces your loan amount, lowers your monthly payments, and can help you secure a better interest rate. For very high-end dream cars, a larger down payment might be necessary to get approved for financing.

Q3: Should I finance through the dealership or a bank?

A3: It’s often best to get pre-approved for a loan from your bank or credit union before visiting the dealership. This gives you a benchmark interest rate. Then, you can present the dealership with your pre-approval and see if they can offer you a better rate. Compare all offers carefully.

Q4: What if my credit score isn’t great right now?

A4: Don’t worry! Focus on improving your credit score before applying for a loan. Pay down existing debt, make all your payments on time, and avoid opening new credit lines. It might take a few months, but a better score will save you money in the long run.

Q5: Is it better to buy new or used for a dream car?

A5: For affording your dream car, a used or certified pre-owned (CPO) vehicle is often the most financially sound choice. Cars depreciate significantly in their first few years. Buying a car that’s 2-5 years old can save you a substantial amount of money while still getting a fantastic vehicle.

Q6: How can I cut costs if my dream car is expensive to insure?

A6: Shop around extensively for insurance quotes. Consider increasing your deductible (though ensure you can afford to pay it if needed). Ask about discounts you might qualify for (e.g., low mileage, good driver, multi-car policy). In some cases, choosing a less expensive trim level or optional feature might also impact insurance premiums.

Conclusion

Affording your dream car is a journey, not an overnight event. By meticulously planning your budget, diligently saving, improving your creditworthiness, understanding your financing choices, and shopping smartly, you can absolutely turn that automotive fantasy into a tangible reality. Remember, the goal is to enjoy your dream car responsibly, without letting it derail your financial well-being. Take it step by step, celebrate your progress, and soon you’ll be behind the wheel of the car you’ve always wanted.