How to Remove Yourself from a Cosigned Car Loan

Dealing with a cosigned car loan can feel tricky. Many people find themselves in this situation without knowing the best way to handle it. If you’re looking for answers on How to Get Out of a Cosigned Car Loan Legally, you’re in the right place.

We’ll break down the steps clearly and simply so you can understand your options.

Understanding Your Cosigned Car Loan

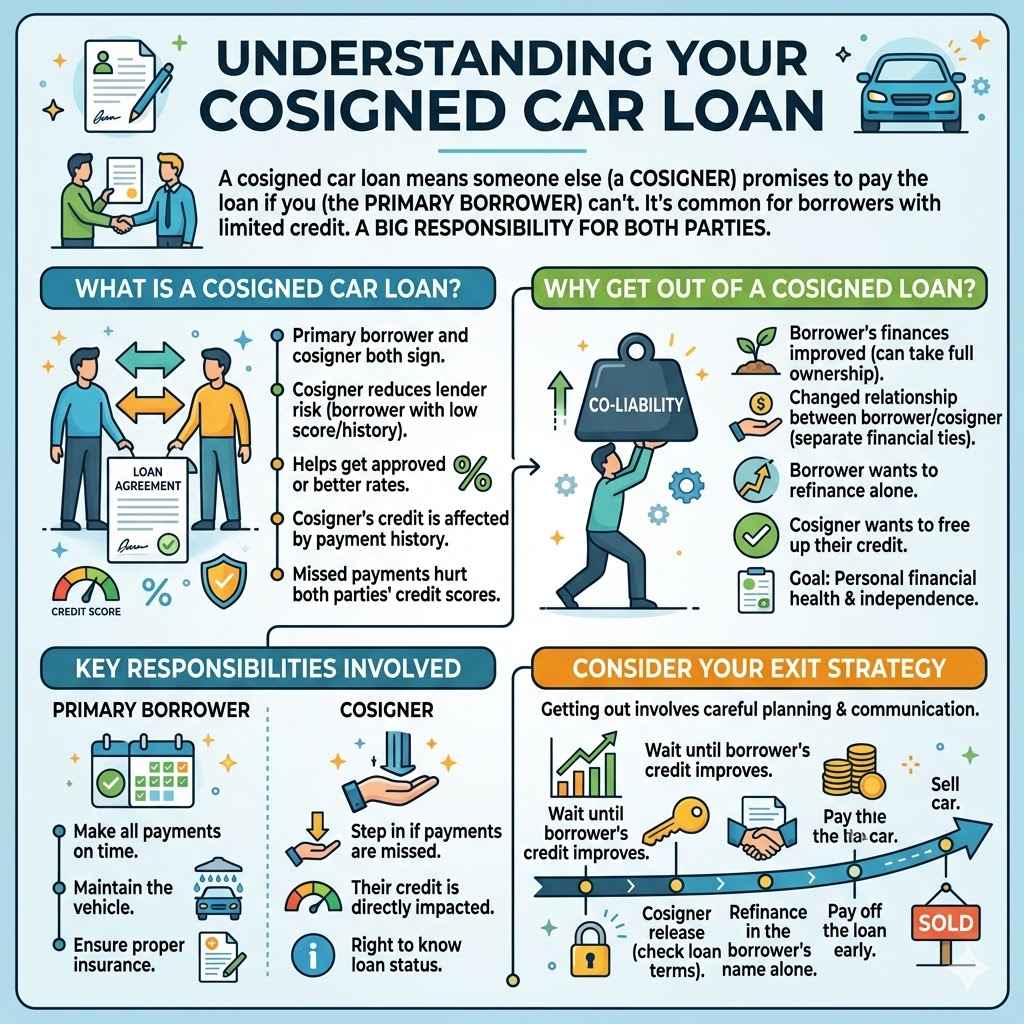

A cosigned car loan means someone else promised to pay the loan if you can’t. This is common when a borrower has a limited credit history or needs a co-signer to get approved. It’s a big responsibility for both parties.

When you want to get out of this agreement, it often involves careful planning and communication. This section will help you grasp the basics of what this type of loan entails and why finding a legal exit strategy is important.

What is a Cosigned Car Loan

A cosigned car loan is an agreement where one person (the primary borrower) applies for a car loan, and another person (the cosigner) signs onto the loan as well. The cosigner agrees to be responsible for the loan payments if the primary borrower fails to make them. Lenders often require a cosigner to reduce their risk, especially if the primary borrower has a low credit score or limited credit history.

This can help the primary borrower get approved for a loan or secure better interest rates.

The cosigner’s credit score is also on the line. If payments are missed, it will negatively affect both the primary borrower’s and the cosigner’s credit reports. This can make it harder for either party to get loans or credit cards in the future.

It’s essential for both individuals to understand the terms and their obligations fully before signing.

Why Get Out of a Cosigned Loan

There are several reasons why someone might want to get out of a cosigned car loan. Perhaps the primary borrower’s financial situation has improved, and they wish to take full ownership of the loan. Maybe the relationship between the borrower and cosigner has changed, leading to a desire to separate their financial ties.

It’s also possible that the primary borrower wants to refinance the loan in their name alone, or the cosigner wants to remove their name from the liability.

Separating financial obligations is often a goal for maintaining personal financial health and independence. Leaving a cosigned loan can free up the cosigner’s credit and reduce their financial risk. For the primary borrower, it can be a step towards full financial responsibility and building their credit history independently.

Key Responsibilities Involved

Both the primary borrower and the cosigner have significant responsibilities under a cosigned car loan. The primary borrower is expected to make all payments on time and in full. They are also responsible for maintaining the vehicle and ensuring it is properly insured.

The loan agreement usually specifies these duties.

The cosigner’s main responsibility is to step in and make payments if the primary borrower cannot. Their credit score is directly impacted by the payment history of the loan. They also have the right to know the loan’s status and can take action if payments are missed.

Understanding these roles is key before considering any exit strategy.

Legal Ways to Remove Yourself or the Cosigner

Removing yourself or a cosigner from a car loan requires specific actions and often the cooperation of the lender. It’s not always straightforward, but there are several legal avenues to explore. This section will detail the most common and effective methods for achieving this separation, focusing on the legal aspects and necessary steps.

Refinance the Loan

Refinancing is one of the most common ways to get out of a cosigned car loan. This process involves taking out a new loan to pay off the existing one. If the primary borrower can qualify for a new loan on their own, with better terms or simply in their name alone, they can then use this new loan to clear the old debt.

This effectively removes the cosigner from the original loan agreement.

To refinance, the primary borrower will need to apply for a new loan with a bank, credit union, or online lender. The new lender will assess the borrower’s creditworthiness, income, and the car’s value. If approved, the new loan’s funds will be used to pay off the outstanding balance of the cosigned loan.

Once the original loan is paid, the lender will release both the primary borrower and the cosigner from their obligations.

Requirements for Refinancing

To successfully refinance a cosigned car loan, the primary borrower typically needs a good credit score. Lenders look for a history of on-time payments and a manageable debt-to-income ratio. A higher credit score will increase the chances of approval and may secure a lower interest rate.

The borrower must also demonstrate sufficient income to prove they can handle the monthly payments independently.

The vehicle itself also plays a role. Lenders will consider the car’s age, mileage, and overall condition. If the car has depreciated significantly or has high mileage, it might be more difficult to refinance.

Some lenders may also require a down payment for refinancing, especially if the borrower’s credit is not ideal.

Steps in the Refinancing Process

The refinancing process begins with researching different lenders and comparing their interest rates and loan terms. Once a lender is chosen, the primary borrower will submit a loan application. This application will require personal information, employment details, and financial history.

The lender will then review the application, check the credit report, and appraise the vehicle’s value.

If the loan is approved, the borrower will review and sign the new loan documents. The new lender will then disburse the funds directly to the original lender to pay off the cosigned loan. After the original loan is satisfied, the lien on the car will be released, and the primary borrower will be the sole owner of the car and responsible for the new loan.

The cosigner is then fully removed from the original loan.

Loan Assumption or Transfer

A loan assumption or transfer is a process where one party agrees to take over the remaining debt of a loan from another party. In the context of a cosigned car loan, this could mean the primary borrower transferring the loan solely into their name, or a new borrower taking over the loan from both the original primary borrower and the cosigner. This is less common than refinancing and often requires lender approval.

For a loan assumption to be successful, the lender must agree to release the cosigner from the contract and allow the primary borrower to take over the full responsibility. Alternatively, if the primary borrower wants to exit, they might try to find another individual willing to assume the loan. This often involves a credit check for the new party, similar to refinancing.

Lender Approval for Assumptions

Lender approval is a critical hurdle for loan assumptions. Many auto loan agreements do not easily allow for the assumption of the loan by another party without a new application and approval process. The lender will want to ensure that the party taking over the loan is creditworthy and can meet the payment obligations.

This process is often as rigorous as applying for a new loan.

The lender’s policies vary greatly. Some lenders might have a formal process for loan assumption, while others may simply require the original parties to pay off the loan and for a new loan to be originated for the party taking over. It’s crucial to contact the lender directly to understand their specific procedures and requirements for loan transfers.

When a Transfer Might Work

A loan transfer might work best when the primary borrower has improved their credit significantly and can now qualify for the loan on their own. In this scenario, they can apply to have the loan formally transferred into their name, with the lender agreeing to release the cosigner. This is essentially a formal modification of the loan terms.

Another scenario is if the car is being sold, and the buyer wishes to take over the existing loan. If the lender permits this, the buyer would undergo a credit check and a formal assumption process. This allows the original borrower and cosigner to be released from their obligations upon a successful transfer to the new owner.

Selling the Vehicle

Selling the vehicle is a direct way to resolve a cosigned car loan, especially if neither party wishes to keep the car or if refinancing isn’t an option. The proceeds from the sale can be used to pay off the remaining loan balance. This method requires cooperation between the primary borrower and the cosigner, and often involves the lender.

If the sale price is higher than the outstanding loan balance, the excess can be split or used as agreed. If the sale price is less than the loan balance, the difference (a deficit) will need to be paid by either the primary borrower, the cosigner, or both, according to their agreement.

Selling and Paying Off the Loan

To sell the vehicle and pay off the loan, you’ll first need to determine the current loan payoff amount from your lender. This is the exact amount needed to fully discharge the loan. Then, you’ll need to find a buyer for the car.

You can sell it privately or trade it in at a dealership. A private sale often yields a higher price.

Once a buyer is found and an agreement is reached on the price, the loan payoff process begins. Typically, the buyer will pay you, and you will immediately use those funds to pay off the lender. The lender will then release the title, allowing you to transfer ownership to the buyer.

If the sale price is less than the payoff amount, you’ll need to cover the difference.

Handling a Shortfall After Sale

A shortfall occurs when the sale price of the car is less than the amount owed on the loan. For example, if you owe $10,000 and sell the car for $8,000, there is a $2,000 shortfall. In this situation, the loan agreement dictates who is responsible for this remaining debt.

Legally, both the primary borrower and the cosigner are still obligated to pay the remaining balance to the lender.

It is crucial for the primary borrower and cosigner to discuss and agree on how to cover this shortfall. This could involve splitting the difference, with the primary borrower taking on a larger portion if they are the ones choosing to sell. Failure to pay the shortfall can result in the lender pursuing legal action against both parties and further damaging their credit scores.

Buyout by the Primary Borrower

A buyout by the primary borrower means the primary borrower pays off the loan amount to remove the cosigner’s obligation. This is different from refinancing because it doesn’t necessarily involve taking out a new loan, although it often does. The core idea is that the primary borrower provides the funds to satisfy the existing loan entirely, releasing the cosigner.

This can be achieved through savings, a personal loan, or even a loan from family or friends. The primary borrower will need to secure the funds equivalent to the loan’s payoff amount and then present it to the lender to close out the loan. This is a clean way to sever financial ties if the funds are available.

Funding the Buyout

The primary borrower needs to secure the exact payoff amount from their lender. This amount might differ slightly from the current balance due to accrued interest or fees. Once the precise figure is known, the borrower can explore funding options.

Using personal savings is the most straightforward method if sufficient funds are available.

If savings are insufficient, the borrower might consider a personal loan from a bank or credit union. This would involve a new loan application based on their creditworthiness. Alternatively, borrowing from family or friends can be an option, but it’s essential to have a clear, written agreement to avoid future misunderstandings.

Release of Liability

Once the buyout funds are provided to the lender and the loan is fully paid off, the lender is obligated to release both the primary borrower and the cosigner from all liability associated with that loan. This is usually documented with a letter of satisfaction or by providing a lien release if the car title was held by the lender.

It is vital for the cosigner to ensure they receive official confirmation from the lender that their name has been removed from the loan and that they are no longer responsible. This confirmation serves as proof and protects the cosigner moving forward. This official release is the final step in severing the cosigner’s financial connection to the car loan.

Negotiating with the Lender

Dealing with lenders can sometimes be the key to finding a solution when other options seem limited. They are interested in getting paid, and sometimes they are willing to work with borrowers to achieve this. This section explores how to approach your lender and what kind of agreements you might be able to negotiate.

Direct Communication is Key

Open and honest communication with your auto loan lender is crucial. If you’re facing difficulties making payments or want to change the loan’s structure, contact them as soon as possible. Explain your situation clearly and calmly.

They may have programs or options available that you’re not aware of.

When contacting the lender, be prepared to provide details about your loan and your financial situation. Having a clear idea of what you want to achieve—whether it’s removing a cosigner, refinancing, or modifying payments—will make the conversation more productive. It’s always better to proactively discuss issues rather than wait for default.

Possible Lender Agreements

Lenders may be open to various agreements depending on your circumstances. One possibility is a loan modification, where they agree to change the terms of the loan, such as extending the repayment period to lower monthly payments. Another option could be a temporary forbearance, which allows you to pause payments for a set period during financial hardship, though interest may still accrue.

In some cases, if a primary borrower has significantly improved their credit, a lender might agree to remove a cosigner directly without requiring a full refinance, especially if the loan has been in good standing. However, this is less common and depends heavily on the lender’s policies and the borrower’s demonstrated creditworthiness. The most frequent outcome is refinancing, which the lender facilitates.

What to Do if the Lender Refuses

If your lender refuses your request or proposes an unfavorable solution, don’t despair. You still have options. The first step is to understand why they refused.

Was it due to credit history, the vehicle’s value, or their internal policies? Knowing the reason can help you address the specific issue.

If the refusal is due to the primary borrower’s credit, focus on improving that credit score. This might involve paying down other debts, disputing errors on your credit report, or making all payments on time for a period. If the lender’s refusal seems unreasonable or based on misinformation, consider seeking advice from a consumer protection agency or a financial advisor.

Legal and Financial Implications

Understanding the legal and financial consequences of a cosigned car loan is vital. It affects your credit, your financial freedom, and your relationship with the cosigner. This section outlines these implications so you can make informed decisions about how to proceed.

Impact on Credit Scores

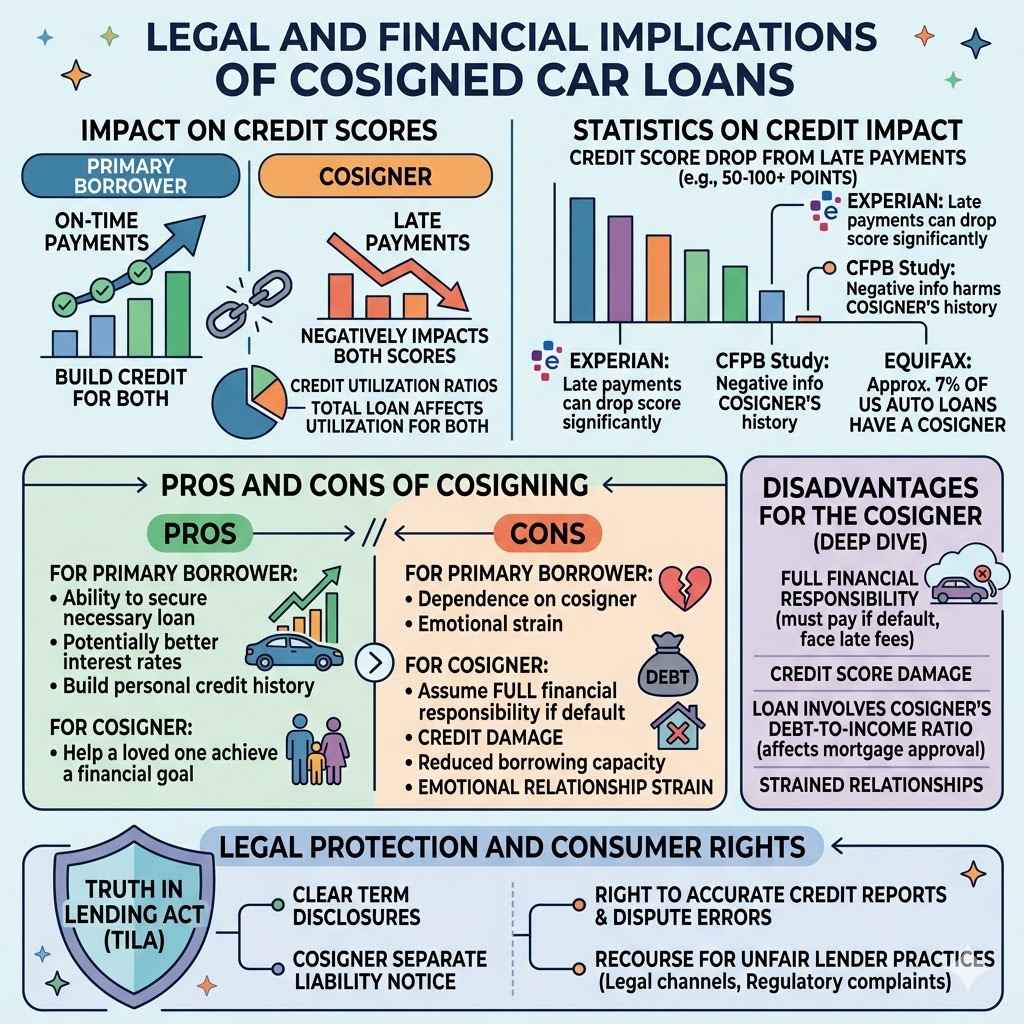

A cosigned car loan significantly impacts both the primary borrower’s and the cosigner’s credit scores. Every on-time payment made by the primary borrower helps build credit for both individuals. However, even a single late payment can negatively affect both credit scores, making it harder to obtain future credit or loans.

The presence of the loan also affects credit utilization ratios. The total loan amount is factored into the credit calculations for both parties. If the primary borrower fails to make payments, the cosigner’s credit will be hit hard, potentially dropping significantly.

This can have long-term consequences, affecting interest rates on other financial products for years.

Statistics on Credit Impact

According to Experian, one of the major credit bureaus, having accounts with late payments can lower your credit score by 50 to 100 points or more, depending on your score before the delinquency. For cosigned loans, this impact is shared. Furthermore, a study by the Consumer Financial Protection Bureau (CFPB) noted that negative information on a cosigned debt can significantly harm the cosigner’s credit history, even if the primary borrower was the one who caused the issue.

For instance, a report from Equifax indicated that approximately 7% of auto loans in the United States have a cosigner. This means millions of individuals are sharing the risks and rewards of these agreements, highlighting the widespread nature of this financial arrangement and its potential for credit score impact.

Pros and Cons of Cosigning

Cosigning a car loan comes with both advantages and disadvantages. For the primary borrower, the main pro is the ability to secure a loan that they might otherwise not qualify for, potentially at a better interest rate. This can be a crucial step in obtaining necessary transportation and building credit.

For the cosigner, the primary pro is helping a loved one achieve a financial goal. However, the cons for the cosigner are substantial. They assume full financial responsibility if the primary borrower defaults, their credit score can be damaged, and the loan counts against their own borrowing capacity.

The emotional strain on relationships can also be a significant con if the loan becomes problematic.

Advantages for the Primary Borrower

The primary borrower gains access to financing for a vehicle, which is essential for many people to get to work, school, or manage daily life. A cosigner can help them secure loan approval when their own credit history is insufficient. This can lead to a more affordable loan with a lower interest rate, saving money over the life of the loan.

Successfully managing a cosigned loan can also help the primary borrower build their own credit history. By making on-time payments, they demonstrate financial responsibility. This can pave the way for them to qualify for loans and credit cards in their own name in the future, eventually leading to financial independence.

Disadvantages for the Cosigner

The cosigner faces significant risks. If the primary borrower misses payments, the cosigner is legally obligated to pay. This can lead to late fees, damage to the cosigner’s credit score, and potential repossession of the vehicle.

The loan also impacts the cosigner’s debt-to-income ratio, which can affect their ability to get approved for their own loans, such as a mortgage.

Furthermore, the relationship with the primary borrower can be strained or broken if financial problems arise. The cosigner might feel financially burdened or taken advantage of. It’s a significant commitment that requires careful consideration and clear communication from the outset.

Legal Protection and Consumer Rights

Both primary borrowers and cosigners have certain legal protections. The Truth in Lending Act (TILA) requires lenders to disclose the terms and conditions of loans clearly. Cosigners must receive a separate notice informing them of their liability and that they are responsible for the debt if the primary borrower defaults.

Consumers have the right to receive accurate credit reports and to dispute any errors. If a lender engages in unfair or deceptive practices, consumers may have recourse through legal channels or by filing complaints with regulatory agencies. Understanding these rights empowers individuals when dealing with lenders and loan agreements.

Frequently Asked Questions

Question: Can I remove my name from a cosigned car loan without paying it off

Answer: Generally, no. Removing your name usually requires paying off the loan or refinancing it into the primary borrower’s name alone. Lenders typically won’t release a cosigner without the loan being satisfied or a new, qualified borrower taking over responsibility.

Question: What happens if the primary borrower stops paying the car loan

Answer: If the primary borrower stops paying, the lender will likely report the missed payments to both their credit and the cosigner’s credit. The car could be repossessed. The cosigner then becomes fully responsible for paying the outstanding balance, including any late fees and collection costs.

Question: Can I sell the car if it’s under a cosigned loan

Answer: Yes, you can sell the car, but both parties typically need to agree. The proceeds from the sale must be used to pay off the loan balance. If there’s a shortfall, the primary borrower and cosigner remain responsible for the remaining debt.

Question: Will refinancing hurt my credit

Answer: Applying for refinancing involves a hard credit check, which can temporarily lower your credit score by a few points. However, successfully refinancing into a loan solely in the primary borrower’s name, and making on-time payments, can ultimately benefit credit scores by establishing independent credit history and removing shared liability.

Question: What if the lender won’t work with me to get the cosigner off the loan

Answer: If the lender is unwilling to modify the loan or allow a transfer, your best options are usually to refinance the loan independently, sell the car to pay it off, or the primary borrower can buy out the loan with other funds. If these aren’t feasible, maintaining consistent on-time payments is critical.

Summary

Getting out of a cosigned car loan legally involves understanding your options. Refinancing the loan into the primary borrower’s name is often the most direct path. Selling the vehicle to pay off the debt is another effective solution.

Negotiating with your lender can sometimes open doors to new agreements.

Always be aware of the credit and legal implications. By taking informed steps, you can successfully separate your financial obligations and achieve your goals.