How to Use a CPN to Get a Car: Proven Way

Using a CPN to get a car can be a powerful tool, but it requires careful and ethical application. This proven method focuses on building a strong profile with your CPN across various financial platforms to establish legitimacy and increase your chances of loan approval. Learn how to navigate this process correctly to secure your vehicle.

Getting behind the wheel of a new car is an exciting prospect, but for many, the journey to car ownership hits a roadblock: credit challenges. If traditional credit building seems daunting or has been a source of frustration, you might have heard about Credit Privacy Numbers, or CPNs. This article is here to demystify how to use a CPN to get a car in a way that’s both effective and responsible. We’ll guide you through the process step-by-step, turning what might seem like a complex topic into something clear and manageable. Forget the jargon and confusion; we’re here to empower you to make smart decisions about your automotive future.

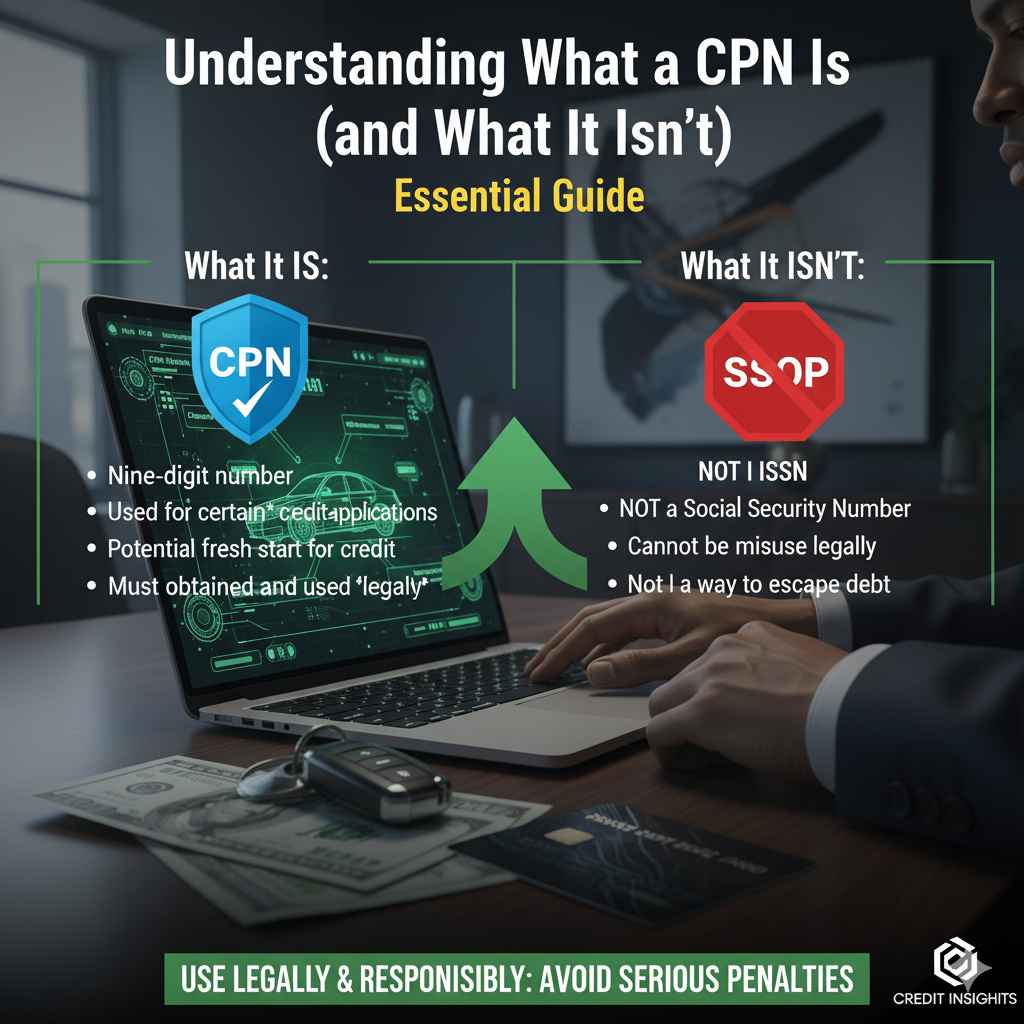

Understanding What a CPN Is (and What It Isn’t)

Before we dive into using a CPN for a car, it’s essential to understand what it is. A Credit Privacy Number (CPN) is a nine-digit number that can be used in place of your Social Security Number (SSN) for certain credit applications. The idea behind a CPN is to separate some of your financial activity from your primary SSN. It’s crucial to know that a CPN is not a Social Security Number. It’s a tool that must be obtained and used legally. Misusing a CPN can lead to serious legal trouble, so understanding its legitimate application is paramount.

Historically, CPNs were developed to help individuals who needed to protect their identity due to fraud or other significant privacy concerns. The legal framework around their use can be intricate, and it’s vital to ensure you are acquiring and using one through legitimate channels. Think of a CPN as a secondary identifier that, when used correctly, can help build a credit profile distinct from your primary SSN-based credit history. This distinction can be particularly useful if your SSN has been compromised or if you’re looking to establish new credit lines separate from past issues.

Why Would Someone Consider a CPN for a Car Loan?

Many people consider using a CPN to obtain a car loan for a variety of reasons. Often, it’s because their primary credit history, built under their SSN, may have inaccuracies, old negative marks, or simply isn’t strong enough to qualify for favorable auto loan terms. Sometimes, individuals may have gone through bankruptcy, experienced significant medical debt, or other financial setbacks that have negatively impacted their SSN-based credit scores. In such cases, a CPN offers a potential fresh start for building credit history that is separate from these past burdens.

It’s also important to acknowledge that some individuals may be seeking to establish credit without their primary SSN being tied to certain financial activities, perhaps due to concerns about identity theft or a desire for a clean slate. The auto industry is a common area where people explore CPNs because a vehicle is a necessity for many, and securing a loan is often the biggest hurdle. This guide focuses on the legitimate and proven ways to leverage a CPN for this purpose.

The Foundation: Obtaining a Legitimate CPN

The absolute first and most critical step is to obtain a legitimate CPN. This is not something you can or should create yourself. Legitimate CPNs are often issued through specific government or private channels, sometimes tied to financial planning services or credit repair agencies that operate within the bounds of the law. Be extremely wary of any service that claims to “sell” you a CPN or offers one with unrealistic promises. A true CPN is assigned, not sold, and its acquisition should align with legal and ethical standards. For instance, some sources indicate CPNs can be obtained through services that help individuals establish new financial identities for privacy reasons, often initiated through specific filings.

The process of obtaining a CPN often involves verifying your identity through a legal process and then receiving a unique nine-digit number. It’s important to understand that this process can take time and may involve fees. Never pay for a CPN that seems too good to be true. Research any provider thoroughly, looking for reviews, industry standing, and clear explanations of their services and the legality of the CPN they provide. A reputable service will educate you on the responsibilities that come with using a CPN.

Key Considerations for CPN Acquisition:

- Legality: Ensure the CPN provider operates within all federal and state laws.

- Verification: The process should involve legitimate identity verification.

- Separation: The CPN should be designed to function independently of your SSN for credit building.

- Transparency: Understand all fees, processes, and requirements upfront.

Building Credit with Your CPN: The Active Strategy

Once you have a legitimate CPN, the real work begins: building a credit profile with it. A CPN is merely a number; it has no inherent credit value. You must actively use it to create a credit history. This involves opening various types of credit accounts that report to the credit bureaus under your CPN. The goal is to demonstrate responsible credit management. This is a deliberate, structured approach, not a quick fix.

The process is similar to building credit with an SSN, but the key is consistently using your CPN for applications and ensuring those accounts report to the major credit bureaus (Equifax, Experian, and TransUnion). This creates a credit report associated with your CPN, which lenders will review when you apply for a car loan. Patience and consistency are crucial here. It takes time to establish a robust credit profile that lenders will trust.

Types of Accounts to Consider for CPN Credit Building:

To build a strong credit profile with your CPN, you’ll want to strategically open and manage different types of credit. Each type helps demonstrate a different aspect of financial responsibility.

- Secured Credit Cards: These are often the easiest to get approved for with a new or limited credit profile. You deposit money upfront, which becomes your credit limit. Use it for small purchases and pay it off in full and on time every month.

- Credit Builder Loans: These are small loans designed specifically to help individuals build credit. You make payments over a set period, and the funds are often held in an account earning interest until the loan is repaid.

- Retail Store Cards: Some store credit cards, particularly those with lower limits, can be accessible. Again, use sparingly and pay off balances diligently.

- Department Store Cards: Similar to retail cards, these can be good starting points, but understand their typically higher interest rates if you carry a balance.

When applying for these, always ensure you are explicitly using your CPN as your primary identifier. Read applications carefully and confirm that your CPN is being recorded, not your SSN. This ensures the positive payment history is building under your CPN’s credit report.

Navigating the Auto Loan Application with a CPN

This is where the strategy comes together. Applying for a car loan with a CPN requires careful planning and understanding of lender requirements. Not all dealerships or lenders are equipped or willing to work with CPNs. You’ll need to find those that are CPN-friendly or have processes in place that accommodate them.

The key is to present a credit profile under your CPN that looks legitimate and responsible. This means having several active, well-managed credit accounts contributing to your CPN’s credit report. Lenders will review this report to assess your creditworthiness. A well-established CPN credit profile, showing consistent on-time payments and a low credit utilization ratio across various accounts, will significantly increase your chances of approval.

Step-by-Step Application Process:

- Verify Your CPN Credit Report: Before you even visit a dealership, obtain your credit report associated with your CPN from the major credit bureaus. Ensure it accurately reflects your CPN and any established accounts. This is your primary document for lenders.

- Research CPN-Friendly Dealerships/Lenders: Look for dealerships or independent finance companies that have experience or are known to work with individuals using CPNs. You might find these through online forums, specialized auto brokers, or by asking directly.

- Gather Documentation: Be prepared to provide proof of identity (like a valid state ID or driver’s license), proof of income (pay stubs), and proof of address. Ensure all documentation is consistent with the information on your CPN credit report.

- Complete the Loan Application: When filling out the auto loan application, clearly use your CPN as your primary identifier. Do NOT use your SSN. Be upfront and honest about using a CPN if asked, explaining you are using it for credit building purposes.

- Negotiate Terms: Once approved, carefully review the loan terms, interest rate, and repayment schedule. Compare offers if you have multiple options. Your goal is to secure a loan with manageable monthly payments and a reasonable interest rate.

It’s important to be aware that some lenders may require more scrutiny when dealing with a CPN, simply because it’s less common than an SSN. Transparency and a strong, well-documented credit history under your CPN are your greatest assets. You can find resources on credit reporting agencies that explain consumer rights regarding credit reports. For example, the Consumer Financial Protection Bureau (CFPB) offers extensive information on credit reports and scores, which can be helpful in understanding what lenders look for and your rights as a consumer.

Building Trust and Legitimacy: The Long Game

Using a CPN to get a car isn’t just about the initial approval; it’s also about continuing to build a solid financial reputation. Lenders and dealerships value consistency and reliability. By making all your car loan payments on time and continuing to manage your other credit accounts responsibly under your CPN, you are reinforcing your credibility.

This sustained responsible behavior can open doors for future financial opportunities. A strong CPN credit history can eventually help you secure better loan terms for future vehicles, mortgages, or other significant purchases. The key takeaway is that a CPN is a tool for building a legitimate financial identity, and like any identity, it needs consistent positive action to be truly effective and trustworthy.

Potential Challenges and How to Overcome Them

While using a CPN can be an effective strategy, it’s not without its potential hurdles. Understanding these challenges beforehand can help you navigate them more smoothly.

Common Challenges:

- Lender Hesitation: Some traditional banks and larger auto finance companies may be unfamiliar with or unwilling to process applications using CPNs.

- Fraud Detection: Financial institutions have sophisticated fraud detection systems. If your CPN usage appears unusual or mirrors fraudulent activity, your application could be flagged.

- Building a Sufficient Credit Profile: It takes time and consistent effort to build a credit report robust enough to secure a car loan.

- Understanding Legalities: Navigating the legal nuances of CPN usage requires diligence and accurate information.

Overcoming Challenges:

- Seek Niche Lenders: Focus your search on credit unions, smaller finance companies, or dealerships with in-house financing that are known to be more flexible.

- Maintain Absolute Honesty: Always use your CPN correctly on all applications. Never misrepresent your identity or provide false information.

- Patient Credit Building: Commit to a structured credit-building plan. Open multiple types of accounts and manage them perfectly for at least 6-12 months before applying for a car loan.

- Educate Yourself: Stay informed about CPN laws and regulations in your state. Reputable CPN providers or financial advisors can be valuable resources. You might find a wealth of information from resources like the U.S. Department of Justice’s Civil Rights Division, which touches upon consumer protection against discriminatory practices in credit lending.

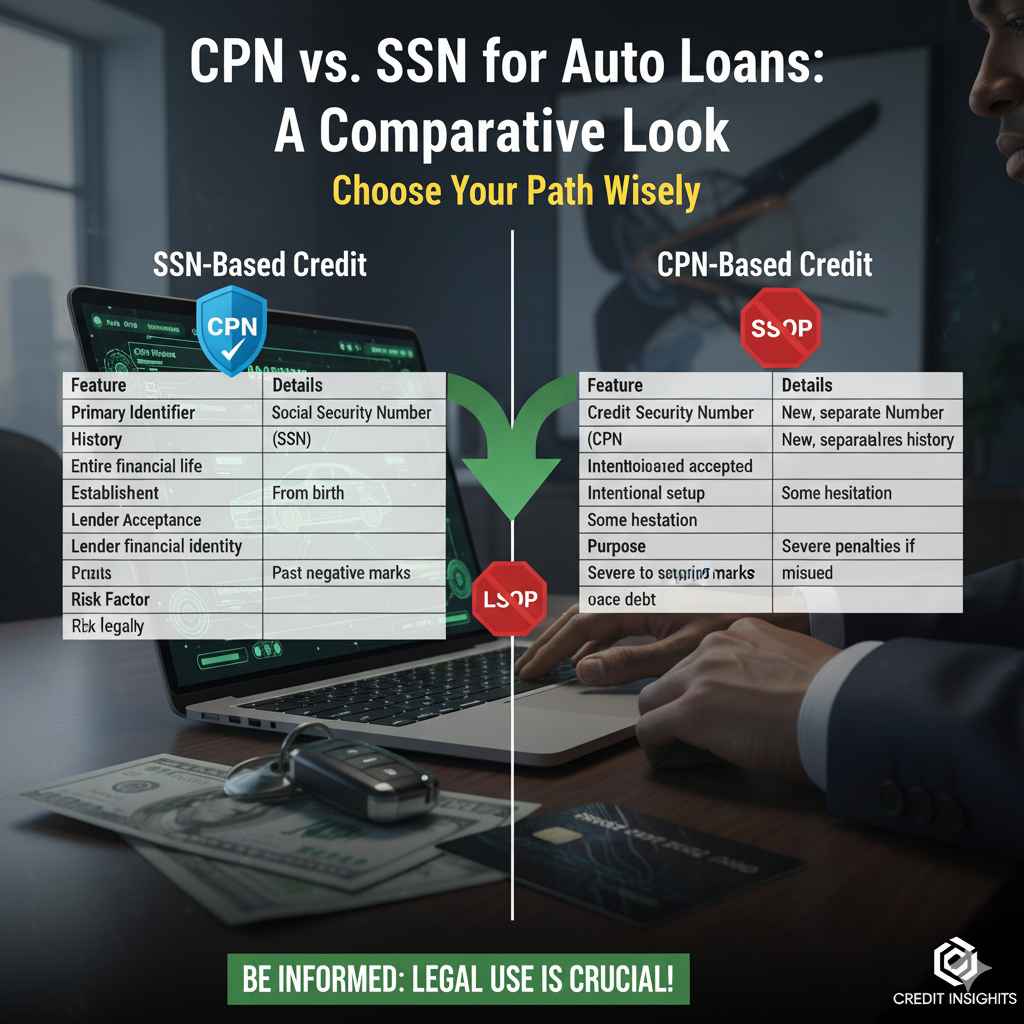

CPN vs. SSN for Auto Loans: A Comparative Look

It’s helpful to compare how an SSN-based credit history and a CPN-based credit history function when applying for a car loan. Your SSN is your primary identifier for most financial transactions in the United States. Building credit with an SSN leverages your entire financial history. A CPN offers a way to build a separate credit profile.

| Feature | SSN-Based Credit | CPN-Based Credit |

|---|---|---|

| Primary Identifier | Social Security Number (SSN) | Credit Privacy Number (CPN) |

| History | Reflects your entire financial life linked to your SSN | Builds a new, separate credit history |

| Establishment | Established from birth or first credit application | Requires intentional setup and credit building |

| Lender Acceptance | Universally accepted by all lenders | May face hesitation from some lenders; requires research for acceptance |

| Purpose | Primary credit building and financial identity | Alternative or supplementary credit building, privacy, or fresh start |

| Risk Factor | Limited if credit is managed well. Potential issues arise from past negative marks. | Requires absolute adherence to legal usage. Misuse can lead to severe penalties. |

The primary distinction lies in universality and established history. An SSN is recognized everywhere. A CPN is a tool that requires more proactive effort to gain acceptance and build a reliable history. However, for those facing significant challenges with their SSN-based credit, a CPN can provide a viable pathway to vehicle ownership.

Frequently Asked Questions (FAQ) About Using a CPN for a Car

Q1: Can I use a CPN to buy any car?

Yes, theoretically, you can use a CPN to buy any car, provided you can secure financing. The key is finding a lender willing to approve your auto loan application based on the credit profile you’ve established with your CPN. Not all dealerships work with CPNs, so research is essential.

Q2: Is using a CPN legal?

Obtaining and using a CPN legally is possible when done correctly and for legitimate purposes, such as establishing credit or protecting privacy. However, using a CPN fraudulently or to deceive lenders is illegal and carries severe penalties. Always ensure your CPN is obtained through legitimate channels and used in compliance with all laws.

Q3: How long does it take to build credit with a CPN?

Building a credit profile with a CPN takes time, similar to building credit with an SSN. You’ll need several months to over a year of consistent, responsible credit usage (making on-time payments, keeping balances low) across various accounts before you have a strong enough report to reliably qualify for an auto loan.

Q4: What if a dealership asks for my SSN?

If a dealership asks for your SSN and you are using a CPN, you must clearly state that you are using your CPN for the application. Be prepared to provide documentation or explanations if they are unfamiliar with CPNs. If they refuse to proceed without an SSN, you will need to find a dealer or lender who accepts CPN applications.

Q5: Can I use a CPN if my SSN has bad credit?

Yes, that’s often a primary reason people explore CPNs. A CPN allows you to build a separate credit history that is not tied to your existing SSN credit report. This can be a way to get a fresh start for financing critical purchases like a car, independent of past credit issues.

Q6: What are the risks of using a CPN?

The main risks involve improper or fraudulent usage, which can lead to legal repercussions, including fines and criminal charges. There’s also the risk of encountering lenders who are unfamiliar with or distrustful of CPNs, leading to application denials. Furthermore, if you acquire a CPN from a fraudulent source, it might be invalid or lead to further complications.

The Proven Way: Summary and Next Steps

The “proven way” to use a CPN to get a car hinges on integrity, patience, and strategic execution. It’s not a shortcut around financial responsibility but rather a method to build a separate, reputable credit profile. The core steps involve legally acquiring a legitimate CPN, actively and responsibly building credit history with it across various financial products, and then strategically applying for auto financing with CPN-friendly lenders.

Consistency in making payments, keeping credit utilization low, and educating yourself about the process are paramount. While challenges exist, particularly in gaining lender acceptance, a well-documented and diligently managed CPN credit history is your strongest asset. By following these steps, you can increase your chances of securing the vehicle you need and build a foundation for future financial success.

Conclusion

Embarking on the journey to car ownership can be a significant and exciting milestone. For those facing credit hurdles, a CPN can present a viable pathway, but it is one that must be navigated with care and a commitment to legitimate practices. By understanding what a CPN is, acquiring one through ethical means!