Is 642 A Good Credit Score For Car Loan: Essential Guide

A 642 credit score is considered fair for a car loan. You can likely get approved, but expect higher interest rates than someone with excellent credit. Focusing on improving your score before applying can save you significant money over the life of the loan.

Hey there, fellow drivers! Md Meraj here. Thinking about a new set of wheels or maybe a reliable upgrade? One of the biggest bumps in the road to owning a car is often securing a loan. And if you’ve seen that magic number, “642,” pop up when checking your credit, you’re probably wondering: “Is 642 a good credit score for a car loan?” It’s a totally valid question, and it can feel a bit confusing. But don’t worry, we’re going to break it down together, nice and easy. We’ll look at what a 642 score really means for getting that car and what smart steps you can take to drive away happy. Let’s make car ownership a smooth ride!

Understanding Your Credit Score: What’s 642 Really Mean?

Think of your credit score as your financial report card. Lenders like banks and dealerships look at it to decide if they should lend you money, like for a car loan. Generally, credit scores range from 300 to 850. The higher the score, the less risky you appear to lenders. A score of 642 falls into the “fair” or sometimes “average” category. This means you’re not at the very top, but you’re also not at the bottom. It’s a score that tells lenders you’ve had some credit history, probably paid some bills on time, but might have had a few hiccups along the way.

For a car loan, a 642 score puts you in a position where approval is possible. It’s not a guaranteed “no,” but it’s also not a guaranteed “yes” with the best terms. Lenders will look at your score, but they’ll also consider other things like your income, how stable your job is, and how much you’re looking to borrow compared to your income (this is called your debt-to-income ratio).

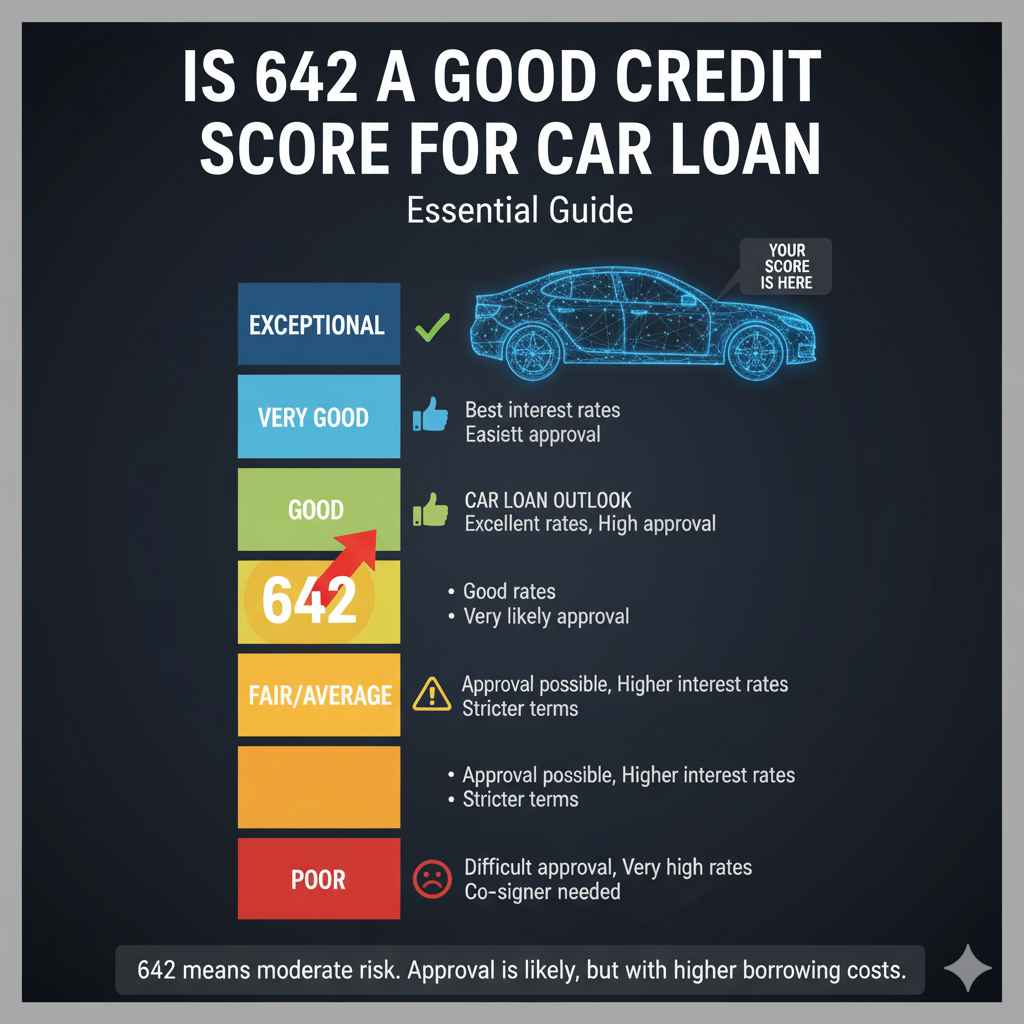

Credit Score Ranges and Car Loan Implications

It helps to see where 642 sits compared to other credit score levels. Different lenders might have slightly different definitions, but here’s a general idea:

| Credit Score Range | Category | Car Loan Outlook |

|---|---|---|

| 800-850 | Exceptional | Best interest rates, easiest approval. |

| 740-799 | Very Good | Excellent interest rates, high approval chances. |

| 670-739 | Good | Good interest rates, very likely approval. |

| 580-669 | Fair/Average | Approval possible, but with higher interest rates and possibly stricter terms. 642 falls here. |

| 300-579 | Poor | Difficult approval, very high interest rates, might require a co-signer or a very large down payment. |

As you can see, your 642 score lands you squarely in the “Fair/Average” zone. This means lenders view you as having a moderate risk. They’re willing to lend, but they’ll want to be compensated for that risk through higher interest rates. This is the most crucial thing to understand: while you can likely get a car loan with a 642, the cost of borrowing will be higher than for someone with a score in the ‘Good’ or ‘Excellent’ ranges.

What Affects Your Credit Score?

Before we dive into improving your situation, it’s helpful to know what makes your credit score tick. Understanding these factors can empower you to make better financial decisions:

- Payment History: This is the biggest factor! Do you pay your bills on time, every time? Late payments can drag your score down.

- Credit Utilization: This is the amount of credit you’re using compared to your total available credit. Keeping this low (ideally below 30%) is good.

- Length of Credit History: The longer you’ve had credit accounts open and managed them responsibly, generally the better.

- Credit Mix: Having a mix of credit types (like credit cards, installment loans) can be positive, showing you can manage different kinds of debt.

- New Credit: Opening too many new accounts in a short period can temporarily lower your score.

For someone with a 642, one or more of these areas might need a little attention. Maybe there were a few missed payments in the past, or perhaps your credit card balances are a bit high.

Can You Get a Car Loan with a 642 Credit Score?

Yes, you absolutely can! The key phrase here is “can,” not “will get the best deal.” Many dealerships and lenders specialize in working with borrowers who have fair credit. They understand that life happens, and not everyone has a perfect credit history. You’ll likely find that direct lenders (banks, credit unions) and dealership financing (often called “Buy Here, Pay Here” or working with subprime lenders) are options.

However, it’s important to be prepared for what this means:

- Higher Interest Rates: This is the most common consequence. The Annual Percentage Rate (APR) you’re offered will be higher, meaning you’ll pay more in interest over the loan term.

- Shorter Loan Terms: Lenders might offer shorter repayment periods to reduce their risk, which means higher monthly payments.

- Larger Down Payment: You might be asked to put down a larger amount of money upfront.

- Limited Vehicle Choices: Some dealerships might steer you towards older or less expensive vehicles, as they represent less risk for the lender.

For instance, imagine two people buying the same $20,000 car over five years.

Person A (Excellent Credit, 4% APR): Monthly payment ~$368, Total interest ~$2,100.

Person B (Fair Credit, 12% APR): Monthly payment ~$445, Total interest ~$6,700.

That’s a significant difference in total cost!

Strategies to Improve Your Chances (and Save Money!)

While a 642 score can get you a car loan, it’s always a good idea to try and improve it, even just a little, before you apply. Even a small boost can lead to better loan terms and save you hundreds or even thousands of dollars. Here’s how you can boost your score:

1. Check Your Credit Reports for Errors

This is a crucial first step. Sometimes, your score might be lower than it should be because of mistakes on your credit report. You’re entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year through AnnualCreditReport.com. Review them carefully for any inaccuracies, such as accounts that aren’t yours, incorrect payment statuses, or outdated negative information. If you find errors, dispute them immediately. The Consumer Financial Protection Bureau (CFPB) has excellent resources on how to do this.

2. Pay Down Credit Card Balances

As mentioned, credit utilization is a big deal. If your credit cards have high balances, paying them down – aiming for under 30% of your credit limit – can significantly improve your score. For example, if you have a card with a $10,000 limit and a $7,000 balance, paying it down to $3,000 or less will make a difference.

3. Make All Payments On Time, Going Forward

This can’t be stressed enough. Every single payment you make from now on should be on time. If you tend to forget, set up automatic payments or use calendar reminders. Even one or two late payments can knock points off your score, while consistent on-time payments are the bedrock of a good score.

4. Avoid Opening New Credit Accounts Unnecessarily

While improving your credit mix can be good, applying for several new credit cards or loans right before applying for a car loan can actually hurt your score temporarily due to the hard inquiries. Focus on managing the credit you have responsibly.

5. Consider a Secured Credit Card or Credit-Builder Loan

If you have limited credit history or want to actively rebuild, these tools can be very effective. A secured credit card requires a deposit, which becomes your credit limit. Paying it off on time builds positive credit history. A credit-builder loan is a small loan where the money is held by the lender and released to you after you make all the payments.

Getting Pre-Approved for a Car Loan

This is a smart move for anyone, but especially with a 642 credit score. Pre-approval means you apply for a loan with a bank or credit union before you go to the dealership. You’ll find out how much you can borrow and at what interest rate. This gives you:

- Bargaining Power: You know your financial limit, so you won’t be swayed by a salesperson focused on monthly payments rather than the total price.

- Realistic Expectations: You’ll know what kind of car you can afford.

- A Better Rate: The rate you get from a bank or credit union might be better than what a dealership can offer, especially if they work with subprime lenders.

When you go to the dealership, you can tell them, “I’m pre-approved for X amount at Y interest rate from my bank.” They can then try to beat that offer, or you can simply use it as your guide. Always compare the dealership’s financing offer to your pre-approval offer.

Navigating Dealership Financing with a 642 Score

Dealerships are often the go-to for car loans, and they work with many different lenders, including those who specialize in subprime loans (for borrowers with lower credit scores). Here’s what to expect and how to handle it:

1. The Application Process

You’ll fill out a loan application. The dealership will submit this to various lenders to see who will approve you and at what terms. With a 642 score, you might get approved by a subprime lender. These lenders often have higher interest rates to offset the risk. You might also be asked for a larger down payment. Some dealerships might even offer in-house financing, sometimes called “Buy Here, Pay Here” (BHPH). With BHPH, the dealership is your lender, and you make payments directly to them. These can be flexible but often come with the highest rates and strictest terms. Always read the contract carefully.

2. Negotiating Terms

Once you have an offer, don’t just accept it. Remember your pre-approval, if you got one. Even if you didn’t, shop around if you have time. If the dealership’s offer is higher than your pre-approval, ask them if they can match or beat it. If they can’t, you can still take the loan from your bank or credit union. Don’t let them pressure you into accepting unfavorable terms.

3. The Importance of a Down Payment

As we’ve touched on, a larger down payment can make a big difference when your credit score is in the fair range. It reduces the amount you need to borrow, which lowers the lender’s risk. This can help you secure a loan, potentially at a slightly better interest rate, and it also means you’ll owe less on the car from day one. Even putting down an extra $500 or $1,000 can be beneficial. Saving up for a bigger down payment is often well worth the wait.

What to Look Out For (Red Flags)

When you’re looking for a car loan with a 642 score, some deals might seem too good to be true, or simply confusing. Be aware of these potential red flags:

- Extremely High Interest Rates: While rates will be higher, look out for rates that seem excessively high, perhaps well above what others with similar scores might see.

- Excessive Fees: Check for hidden fees in the loan agreement, such as loan origination fees, dealer prep fees (that you shouldn’t be paying for), or mark-ups that aren’t justified.

- “Guaranteed Approval” Claims: While many places work with fair credit, “guaranteed approval” often comes with very high costs. Always read the fine print.

- Longer Loan Terms for Lower Payments: A common tactic is to extend the loan term to make monthly payments seem affordable. However, this significantly increases the total amount of interest you pay over time. For example, a $20,000 loan at 10% APR might be $425/month for 5 years, but extended to 7 years, it drops to ~$325/month, but you pay thousands more in interest.

- Pressure Tactics: If a salesperson is pushing you to sign immediately without giving you time to think or compare, that’s a warning sign.

Always remember that you have the right to walk away if a deal doesn’t feel right or if the terms are too unfavorable.

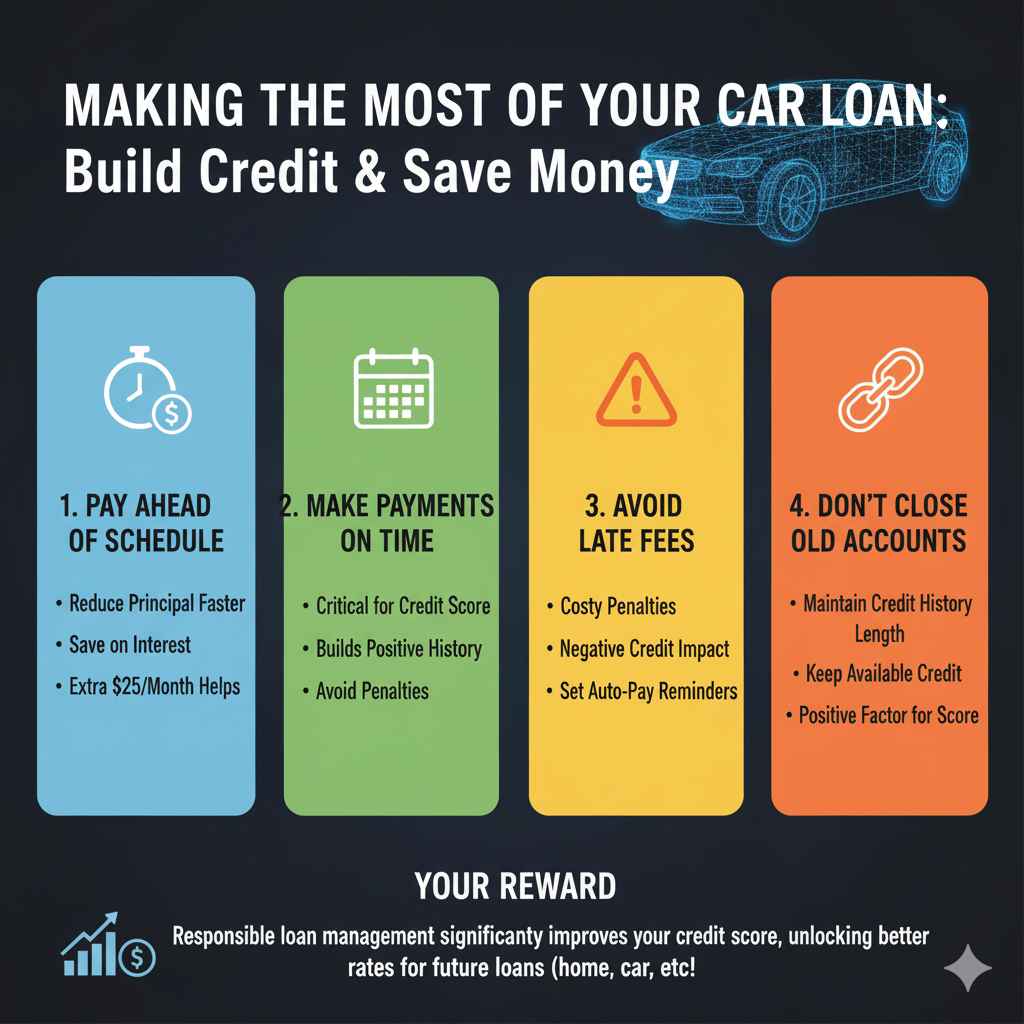

Making the Most of Your Car Loan

Once you secure your car loan with a 642 credit score, your mission doesn’t end there. The best way to use this loan to your advantage for the future is to treat it as an opportunity to rebuild your credit:

- Pay Ahead of Schedule: Whenever possible, pay more than the minimum payment. Even an extra $25 or $50 can chip away at the principal faster.

- Make All Payments On Time: This is critical. Consistent, on-time payments are the single best way to improve your credit score over time.

- Avoid Late Fees: Late fees not only cost you money but can also be reported to credit bureaus, negatively impacting your score.

- Don’t Close Old Accounts Hastily: Once you eventually pay off your car loan, resist the urge to close that account if it was a new one used for building credit. The length of your credit history and your available credit can be positive factors.

By managing your car loan responsibly, you can significantly improve your credit score over the next few years, opening doors for better loan terms on future purchases, like a home or even another car.

Frequently Asked Questions (FAQs)

Q1: Is a 642 credit score too low for a car loan?

No, a 642 credit score is generally considered ‘fair’ and is not too low for a car loan. You can likely get approved for a loan, but you may face higher interest rates and stricter terms compared to those with higher credit scores.

Q2: What kind of interest rate can I expect with a 642 credit score?

Expect interest rates to be higher than average. While rates fluctuate, someone with excellent credit might get 4-6% APR, a fair credit score like 642 could see rates ranging from 10% to 18% or even higher, depending on the lender and market conditions. It’s vital to shop around.

Q3: How much down payment might I need for a car loan with a 642 score?

Lenders may ask for a larger down payment to reduce their risk. While it varies, be prepared to put down anywhere from 10% to 20% or more of the vehicle’s price. A bigger down payment can also help you qualify for better loan terms.

Q4: What are the risks of taking a car loan with a 642 credit score?

The main risks are higher borrowing costs due to elevated interest rates, potentially shorter loan terms leading to higher monthly payments, and possibly a more limited selection of vehicles to choose from. You also risk further damaging your credit if you struggle to make payments.

Q5: Can I improve my credit score before applying for a car loan?

Yes! Even a few months can make a difference. Focus on paying down credit card debt, ensuring all payments are on time, and checking your credit report for errors. Aim to get your credit utilization below 30%.

Q6: Should I get pre-approved at my bank or credit union, or go straight to the dealership?

It’s highly recommended to get pre-approved at your bank or credit union first. This gives you a benchmark interest rate and loan amount. You can then use this offer as leverage at the dealership to see if they can beat it, or simply choose the best offer you receive.