What is a Booster Seat and Why is it So Important

Rental car insurance typically costs between $30 and $60 per day, depending on the coverage you choose. However, you might already be covered by your personal auto insurance or credit card. Always check your existing policies first to avoid paying for unnecessary protection and save money.

You’ve just landed after a long flight, you’ve found the rental car counter, and you’re so close to starting your vacation. Then, the agent asks the one question that makes everyone pause: “Would you like to purchase our insurance coverage?” Your mind races. Is it a scam? Is it necessary? Why is it so expensive?

Don’t worry, you’re not alone. This is one of the most confusing parts of renting a car. It feels like a high-pressure decision, but it doesn’t have to be. I’m here to walk you through it, step by step. We’ll break down what each type of insurance means, how much it costs, and how you can figure out if you even need it. By the end of this guide, you’ll be able to answer that question with total confidence.

Why Do I Even Need Insurance for a Rental Car?

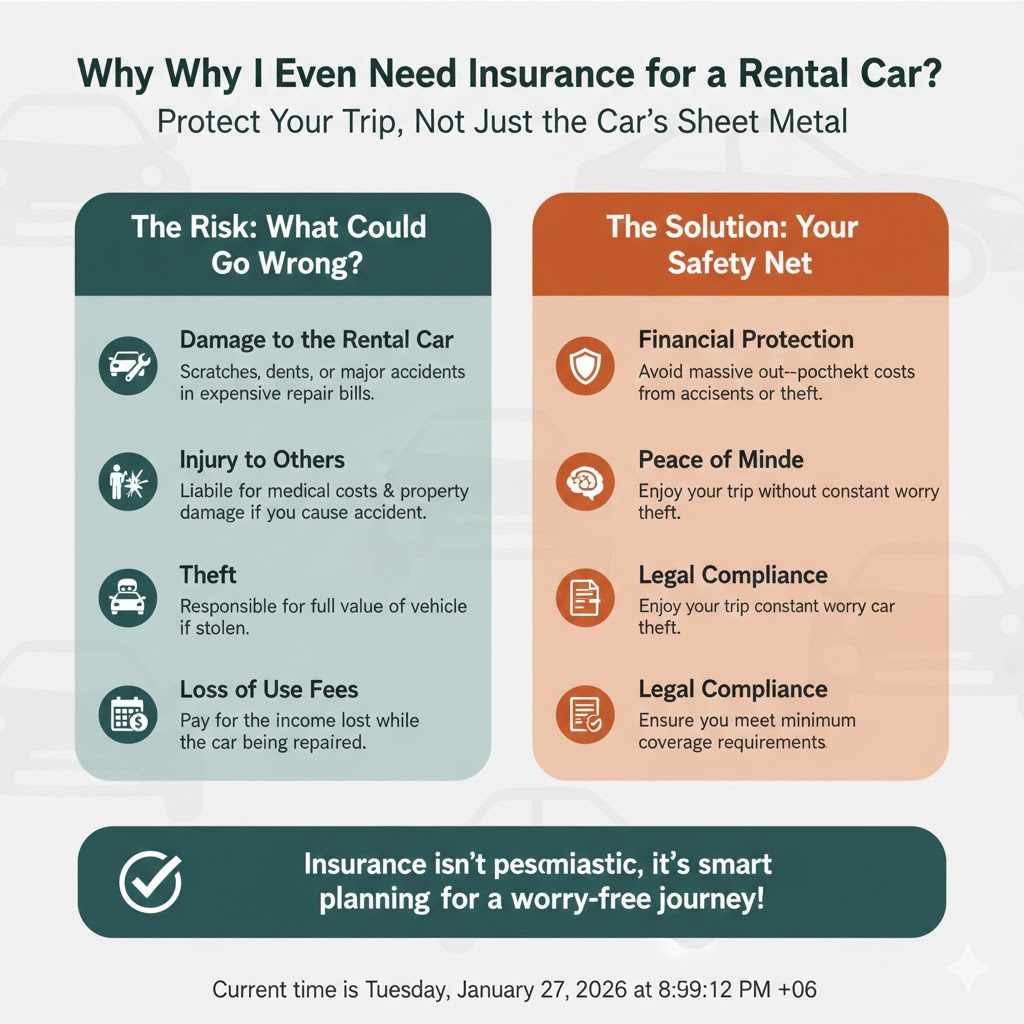

Renting a car feels temporary, so it’s easy to think insurance isn’t a big deal. But when you sign that rental agreement, you’re taking financial responsibility for a vehicle that might be worth $20,000, $30,000, or even more. If something happens—an accident, a theft, or even a small fender bender—you could be on the hook for a lot of money.

Here’s what could go wrong without the right coverage:

- Damage to the Rental Car: Even a minor scratch or dent can lead to hundreds of dollars in repair bills from the rental company.

- Injury to Others: If you cause an accident that injures another person or damages their property, you could be sued for costs that far exceed the value of the car itself.

- Theft: If the rental car is stolen, you would be responsible for its full value.

- Loss of Use Fees: The rental company can charge you for the money it loses while the car is in the repair shop and can’t be rented out.

Having the right insurance isn’t about being pessimistic; it’s about being smart. It’s a safety net that protects your finances and gives you peace of mind so you can enjoy your trip without worry.

Understanding the Types of Rental Car Insurance (The Menu at the Counter)

When you’re at the rental counter, the agent will usually offer you a package of different coverages. It can feel like they’re speaking another language. Let’s translate the four main types of insurance they offer into simple, everyday terms.

1. Collision Damage Waiver (CDW) / Loss Damage Waiver (LDW)

What it is: This is the big one. A Collision Damage Waiver (CDW), often called a Loss Damage Waiver (LDW), is not technically insurance, but it acts like it. If you buy this, the rental company agrees not to hold you responsible if the rental car is damaged or stolen. Without it, you’d have to pay for repairs or the full value of the car out of your own pocket.

Think of it as: “Oops, I Dented the Rental Car” protection. Whether it’s a tiny scratch from a rogue shopping cart or a major collision, this waiver covers the cost of repairs to the car you rented.

2. Liability Insurance (LIS or SLI)

What it is: Liability Insurance protects you from the costs of damage you cause to other people or their property. If you hit another car, a fence, or worse, injure someone in an accident, this coverage helps pay for their medical bills and repair costs. Most states require a minimum amount of liability coverage to drive, but the amounts offered by rental companies are usually much higher than the state minimums.

Think of it as: “Oops, I Dented Someone Else’s Car” protection. This covers your financial responsibility to others, which can often be the most expensive part of an accident.

3. Personal Accident Insurance (PAI)

What it is: This insurance covers medical costs for you and your passengers if you are injured in an accident involving the rental car. It often includes some ambulance and death benefits as well.

Think of it as: “Medical Bills for Me and My Passengers” protection. If you already have good health insurance, you might not need this coverage, as it can be redundant.

4. Personal Effects Coverage (PEC)

What it is: This covers your personal belongings if they are stolen from the rental car. Think laptops, cameras, luggage, and other valuables. There’s usually a limit on how much it will pay out.

Think of it as: “My Stuff Got Stolen” protection. If you have a homeowner’s or renter’s insurance policy, your belongings are often already covered, even when they’re not in your home. It’s a good idea to check your policy.

How Much Is Insurance on a Rental Car? A Cost Breakdown

So, what’s the damage to your wallet? The cost of rental car insurance varies by the rental company, the location, and the type of vehicle you’re renting. However, we can look at some typical price ranges. Here’s a table to make it simple.

| Type of Coverage | What It Covers | Average Cost Per Day |

|---|---|---|

| Collision/Loss Damage Waiver (CDW/LDW) | Damage to or theft of the rental car. | $15 – $30 |

| Liability Insurance (LIS/SLI) | Damage to other people’s property or their medical bills. | $10 – $20 |

| Personal Accident Insurance (PAI) | Medical expenses for you and your passengers. | $3 – $7 |

| Personal Effects Coverage (PEC) | Theft of your personal belongings from the car. | $2 – $5 |

| Full Package (All of the above) | Comprehensive protection from the rental company. | $30 – $60+ |

As you can see, accepting the full insurance package can nearly double the daily cost of your rental! That’s why it’s so important to figure out if you can get this coverage from another source for less money—or for free.

Do You Already Have Coverage? 4 Places to Check Before You Pay

Before you say “yes” at the rental counter, take a few minutes to investigate. You might be surprised to find you already have all the protection you need. Here are the four main places to look.

1. Your Personal Auto Insurance Policy

If you own a car and have personal auto insurance, your policy will often extend to rental cars. This is especially true for rentals within the U.S. and Canada.

- What it usually covers: Your liability coverage (for damage to others) and collision coverage (for damage to the rental car) typically transfer over.

-

What to do: Call your insurance agent before your trip. Don’t just assume you’re covered. Ask these specific questions:

- Does my policy cover rental cars?

- Does my coverage extend to the location I’m traveling to (especially if it’s international)?

- Are there any limits, like the value of the car or the length of the rental period?

- Does my policy cover “loss of use” fees?

- Heads-up: Even if your policy covers the rental, you’ll still have to pay your deductible if you have an accident.

2. Your Credit Card Benefits

This is one of the most valuable—and often overlooked—perks of many major credit cards. Most Visa, Mastercard, American Express, and Discover cards offer some form of rental car insurance as a benefit.

- What it usually covers: Credit card benefits typically provide secondary coverage for collision and theft (CDW/LDW). This means it pays for costs your personal auto insurance doesn’t cover, like your deductible. Some premium travel cards offer primary coverage, which kicks in before your personal insurance.

- What to do: This is crucial! To activate the coverage, you must pay for the entire car rental with that specific credit card. You must also decline the rental company’s CDW/LDW. Call the number on the back of your card or look up your benefits online. The Consumer Financial Protection Bureau offers great advice on this.

- Heads-up: Credit card coverage almost never includes liability, personal accident, or personal effects insurance. It also may not cover certain types of vehicles, like trucks, exotic sports cars, or large vans.

3. Your Travel Insurance Policy

If you purchased a comprehensive travel insurance policy for your trip, it might include rental car coverage. This is more common for international travel. It’s worth checking your policy documents to see what’s included. It could be a great alternative if your personal auto policy or credit card doesn’t cover you abroad.

4. Third-Party Rental Car Insurance Providers

Several companies specialize in selling rental car insurance directly to consumers, often for much less than what the rental companies charge. Companies like Allianz or Bonzah offer policies that you can buy for a specific trip. This can be a good option if you don’t have other coverage or if you want to avoid using your personal insurance and potentially raising your rates after a claim.

A Step-by-Step Guide to Making the Right Choice

Feeling overwhelmed by the options? Let’s put it all together into a simple, four-step plan you can follow before every trip.

Step 1: Check Your Personal Auto PolicyA week or two before you travel, pull out your auto insurance card and call your agent. Ask them directly if your collision and liability coverage extends to rental cars. Make a note of your deductible amount. This is your first and best source of information.Step 2: Review Your Credit Card BenefitsNext, check the benefits of the credit card you plan to use for the rental. Find out if it offers primary or secondary collision coverage. Remember, to use this benefit, you must decline the rental company’s CDW/LDW and pay for the full rental with that card.Step 3: Analyze Your Coverage GapsNow, compare what you have with what you need. Let’s look at a common scenario:You have:– Liability and collision coverage from your personal auto insurance (with a $500 deductible).- Secondary collision coverage from your credit card.Your Gaps:– You are responsible for the $500 deductible in an accident. Your credit card will likely reimburse you for this, but you’ll have to pay it first.- Your personal policy might not cover “loss of use” fees. The credit card might.In this case, you can confidently decline the rental company’s expensive CDW/LDW and Liability coverage. You are already well-protected.Step 4: Decide Based on Your Needs and Risk Tolerance

Your final decision comes down to your situation. Here’s a quick-glance table to help you decide what to do at the counter.

| If Your Situation Is… | Your Best Bet at the Counter |

|---|---|

| You have personal auto insurance that covers rentals AND a credit card with secondary coverage. | Decline the CDW/LDW and Liability. You are likely covered. |

| You don’t own a car and have no personal auto insurance. | Consider buying the rental company’s Liability insurance. Rely on a credit card with primary coverage for CDW/LDW, or buy the waiver. |

| You are renting for business travel. | Check with your employer. They may have a corporate insurance policy that covers you. Do not rely on your personal policy. |

| You are renting internationally. | Your personal auto insurance likely won’t cover you. Rely on a premium credit card with primary coverage or purchase the rental company’s insurance for peace of mind. Some countries require you to buy local insurance. |

| You have a high-deductible auto policy and don’t want the risk. | Consider buying the rental company’s CDW/LDW. It provides zero-deductible coverage and simplifies the claims process if something happens. |

Common Mistakes to Avoid

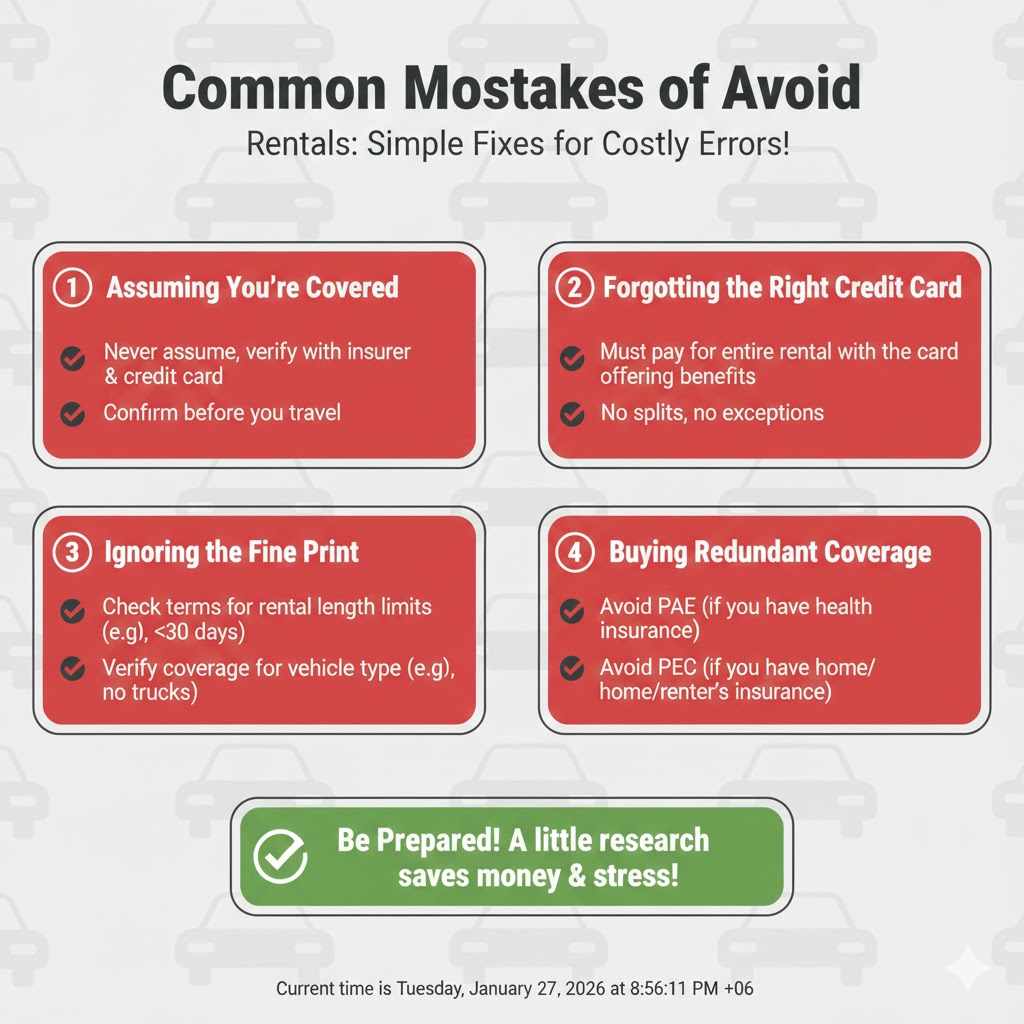

Making the right choice also means avoiding common pitfalls. Keep these mistakes in mind:

- Assuming You’re Covered: Never assume. Always call your insurance agent and credit card company to verify your coverage before you travel.

- Forgetting to Use the Right Credit Card: If you’re relying on your card’s benefits, you must pay for the entire rental with that exact card.

- Ignoring the Fine Print: Your credit card coverage might not apply to long-term rentals (often over 15 or 30 days) or to certain types of vehicles.

- Buying Redundant Coverage: Don’t pay for Personal Accident Insurance if you have good health insurance, or Personal Effects Coverage if you have homeowner’s or renter’s insurance.

- Feeling Pressured at the Counter: Rental agents are often trained to sell you insurance. Stick to your decision. It’s perfectly okay to politely say, “No, thank you, I’m already covered.”

Frequently Asked Questions (FAQ)

What is the cheapest way to insure a rental car?

The cheapest way is to use coverage you already have. Relying on your personal auto insurance policy combined with the collision damage waiver benefit offered by many credit cards is often the most cost-effective option, frequently costing you nothing extra.

Can I use my own car insurance for a rental car?

Yes, in most cases. If you have comprehensive and collision coverage on your personal vehicle, it typically extends to a rental car for personal use within the U.S. and Canada. However, you should always call your insurance provider to confirm the details of your specific policy before you rent.

What happens if I decline all rental car insurance?

If you decline all insurance and you don’t have coverage from another source (like your personal policy or a credit card), you are personally responsible for the full cost of any damage to the rental car, theft of the car, and any damage or injury you cause to others. This could result in tens of thousands of dollars in expenses.

Does my credit card really cover rental car insurance?

Many credit cards offer a Collision Damage Waiver (CDW), but it is not full insurance. It typically covers damage or theft of the rental car but not liability. You must pay for the rental with that card and decline the rental company’s CDW for the benefit to apply. Check if your card offers primary or secondary coverage.

Is the Collision Damage Waiver (CDW) worth it?

The CDW can be worth it if you don’t have any other form of coverage (from personal insurance or a credit card) or if you want total peace of mind with zero deductible. It simplifies the process if there’s an accident, as you can just walk away without dealing with claims or out-of-pocket costs.

How much is liability insurance on a rental car?

Liability insurance from a rental car company, often called Liability Insurance Supplement (LIS) or Supplemental Liability Insurance (SLI), typically costs between $10 and $20 per day. It provides coverage for damages or injuries you cause to other people and their property.

Your Trip, Your Choice, Your Confidence

Navigating the world of rental car insurance can feel like a pop quiz you didn’t study for. But it doesn’t have to be that way. By taking just a little time before your trip to make a couple of phone calls, you can transform from a confused customer into a confident driver.

Remember the simple plan: check your personal auto insurance, check your credit card benefits, and understand the gaps. That’s it. Armed with this knowledge, you can walk up to that rental counter, smile, and know exactly what you need—and what you don’t. You’ll save money, avoid stress, and be able to focus on what really matters: hitting the open road and enjoying your journey.