Will Paying off My Car Loan Boost Your Credit Score?

Have you ever wondered if paying off your car loan could give your credit score a boost? You’re not alone.

Many people grapple with the nuances of credit scores and how their financial decisions impact them. The idea of finally freeing yourself from monthly car payments is enticing, but will it actually help or hurt your credit score? Understanding this could be the key to unlocking better financial opportunities for you.

Imagine the freedom of not having a car loan hanging over your head. Picture the possibilities of what you could do with that extra cash each month. But before you make that final payment, it’s crucial to consider how it will affect your credit score. This isn’t just about numbers; it’s about your financial future. Dive deeper into this topic to discover how your credit score could change and what steps you can take to ensure it moves in the right direction. Your financial health is at stake, and understanding this dynamic could be the game-changer you need.

Impact Of Car Loan On Credit Score

Car loans play a significant rolein your credit history. They show you can manage debt. Lenders see this as a positive sign. A car loan is a type of installment loan. It adds variety to your credit mix. A good mix can improve your score. Paying on time helps your credit score. Late payments can hurt it. Consistent payments show responsibility. This builds trust with lenders.

Payment historyis crucial for your credit score. It makes up 35% of your score. Paying your car loan on time is important. Each timely payment boosts your score. Late payments can lower it. The longer you pay on time, the better. Your score reflects your payment habits. A higher score means better loan options. Keep track of your due dates. Avoid missing payments to protect your score.

Credit: www.experian.com

Benefits Of Paying Off A Car Loan

Paying off a car loan reduces your overall debt. This improves your debt-to-income ratio. Lenders like when you owe less. It shows you can manage money well. Your monthly payments decrease. You have more money to save or spend. This can help when applying for new loans. Lenders may offer better interest rates. You seem less risky to them. Your finances look healthier.

Paying off the car loan impacts credit utilization positively. High balances can hurt your score. Lower balances boost it. You seem responsible with credit. Using less credit is good. It shows you don’t rely on borrowed money. Credit utilization is a big part of your credit score. Keeping it low helps your score grow. Lenders trust you more.

Potential Drawbacks Of Early Payoff

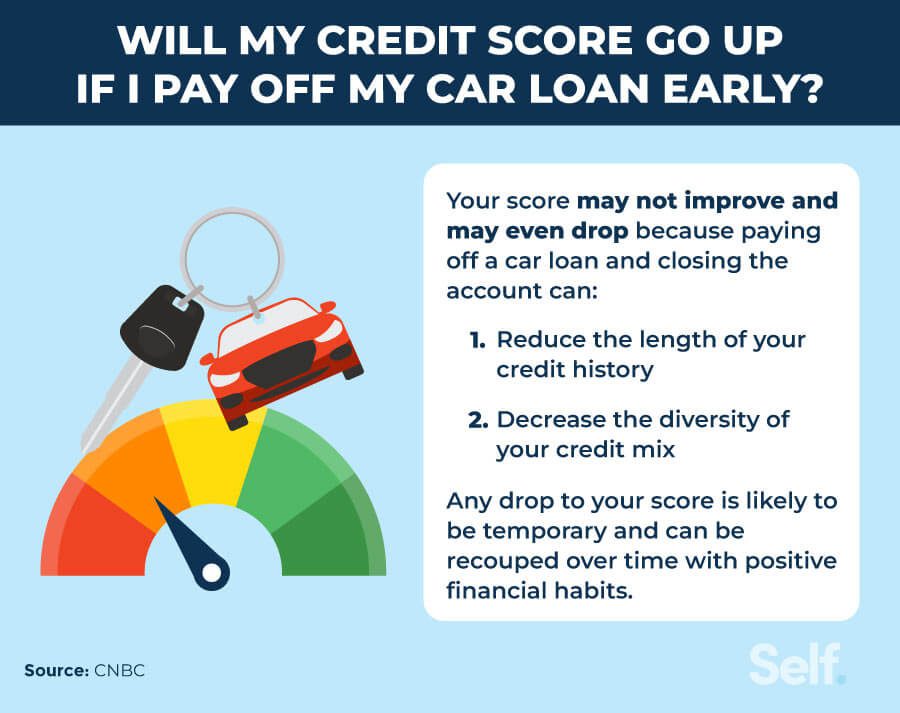

Paying off a car loan early might not boost your credit score. Your credit scoremight drop a little. This happens because of the closed account impact. When you pay off a loan, the account closes. Closed accounts can affect your score. Open accounts show active credit use. Credit agencies prefer this.

Closed Account Impact

Closed accounts are not as active as open ones. Your score could go down. This drop might be small but noticeable. Keeping the account open shows you use credit. This is important for your score. An open loan shows regular payments.

Effect On Credit Mix

Credit mix is part of your score. It looks at different types of credit. Loans, credit cards, and mortgages are examples. Paying off a car loan changes your mix. A balanced mix helps your score. Removing a loan changes this balance. Your score might see a small dip. Keep your credit healthy by diversifying.

:max_bytes(150000):strip_icc()/are-personal-loans-bad-your-credit-score.asp_FINAL-44664c5b7c6b4d73b8ddc4699d545722.png)

Credit: www.investopedia.com

Strategies For Boosting Credit Score

Paying bills on time is crucial. Late payments can hurt your credit score. Try setting up automatic payments. This helps avoid missing due dates. Keeping reminders can also be helpful. Always pay at least the minimum amount due. Paying more than the minimum can be better. It shows you handle debts well.

Having different types of credit helps. Credit cards, loans, and mortgages are examples. A mix shows lenders you can manage different debts. This can boost your score. Ensure you don’t have too much debt. Too many loans can be risky. Keep balances low on credit cards. This reflects good financial habits. It also shows you are responsible with money.

Alternatives To Early Loan Payoff

Refinancing a car loan can be a good choice. This means getting a new loan with a lower rate. It can help you save money. It might also reduce monthly payments. With lower payments, you can manage your budget better. Sometimes, refinancing can extend the loan term. But be careful, it might cost more over time. Compare different refinancing offers. Choose the one that suits your needs the best.

Making partial payments is another option. Pay a bit more than the monthly amount. This reduces your loan balance faster. It can save you money on interest. Partial payments can also shorten the loan term. But make sure to check with your lender first. Some lenders might charge a fee for extra payments. Always check your budget before making extra payments.

Monitoring Credit Score Changes

Credit monitoring tools help track your credit score. These tools send alerts for changes. They also show your credit report details. This makes it easy to see what affects your score. Regular updates can help you understand your credit better. Alerts come when new accounts open or payments are late. This helps you react quickly to changes. It’s important to check your score often. This keeps you informed about your credit health.

Credit reports show your financial history. They list your debts and payments. On-time payments improve your credit score. Late payments can lower it. The report includes your credit card balances. It also shows any loans you have. High balances can hurt your score. Paying off loans can help improve it. Always check your report for errors. Mistakes can affect your credit score. Fix errors to keep your score accurate.

Frequently Asked Questions

Why Did My Credit Score Drop 100 Points After Paying Off My Car?

Paying off your car might reduce credit mix and active accounts, impacting your score. Closed accounts might lower your score temporarily.

Does Paying Off A Car Loan Boost Credit Score?

Paying off a car loan can boost your credit score. It reduces your debt-to-income ratio and shows financial responsibility. However, credit score impacts vary based on your credit history and other outstanding debts. It’s important to maintain other good credit habits to see a significant increase.

How Soon Will Credit Score Improve After Loan Payoff?

Your credit score might improve within a few months after paying off your car loan. Credit reporting agencies update your credit report monthly. The impact on your score can vary based on your credit profile. Consistent on-time payments and low credit utilization are key for improvement.

Can Paying Off A Loan Hurt My Credit Score?

Paying off a loan might temporarily lower your credit score. Closing an account can affect your credit mix and length of credit history. However, the impact is usually minor and short-term. Maintaining other positive credit behaviors will help your score recover and potentially increase over time.

Conclusion

Paying off your car loan can boost your credit score. It shows you’re responsible with debt. But, it might not always cause a big jump. Your credit mix and history also matter. Keep other debts low and pay bills on time.

Check your credit report regularly. This helps you spot any errors. Remember, building credit takes time. Patience and consistency are key. Aim for a balanced approach to managing your credit. A well-maintained credit profile opens more financial doors in the future.

Keep learning and stay informed. You’ll see improvements over time.