Can I Transfer My Car Loan to My Business? Essential Guide

Yes, you can often transfer your car loan to your business, but it’s not a simple switch. It involves refinancing the loan in your business’s name, which requires lender approval and meeting specific business credit and vehicle usage requirements. Doing so can offer tax benefits and simplify company expenses.

Navigating your finances can sometimes feel like a puzzle, and when you use your car for your business, you might wonder if you can simplify things by putting that car loan under your company’s name. It’s a common question for many business owners who find their personal auto loan intertwined with their professional driving. The good news is, it’s often possible! This guide will make it clear and easy to understand how you can transfer your personal car loan to your business, covering what you need to know every step of the way.

Let’s get started on making your business’s financial picture a little smoother.

Why Consider Transferring Your Car Loan to Your Business?

Using your personal vehicle for business purposes is incredibly common. Whether you’re a consultant, a salesperson, a contractor, or run a delivery service, your car is likely an essential tool for your livelihood. When the loan for that vital vehicle is in your personal name, it can create a few headaches. Transferring the car loan to your business can be a smart move for several good reasons.

Tax Benefits

One of the biggest draws for business owners is the potential for tax advantages. When a car loan is officially a business expense, the interest paid on that loan can often be deducted. This can lower your overall taxable income. Additionally, other car-related expenses become easier to track and deduct. Making the car a business asset can open doors to claiming mileage, maintenance, insurance, and depreciation as business write-offs, potentially saving you a significant amount of money come tax season.

Simplified Record-Keeping

Juggling personal and business finances separately is crucial for accurate accounting and tax preparation. If your car is both your personal ride and your business workhorse, having a personal loan for it can muddy the waters. By transferring the loan to your business, you clearly designate the vehicle as a business asset. This makes it much easier to track all expenses related to the car, from loan payments to fuel and repairs, all under one business umbrella. This clarity is a lifesaver when it comes time to file your taxes or present your business’s financial health.

Improved Business Credit

Taking out loans in your business’s name and managing them responsibly is a fantastic way to build your company’s credit history. A strong business credit score can be invaluable for securing future financing, such as loans for equipment, expansion, or even other vehicles. By transferring the car loan, you’re essentially establishing a positive payment history for your business, which can pave the way for greater financial opportunities down the road.

Potential for Better Interest Rates (Sometimes)

While not always the case, depending on your business’s financial standing and your personal credit before the transfer, your business might qualify for more favorable interest rates. Lenders often assess business loans differently than personal ones, considering factors like your business’s revenue, cash flow, and overall financial stability. If your business is doing well, you might be able to refinance your car loan at a lower rate than you originally secured personally.

Is Transferring Your Car Loan to Your Business Always Possible?

While the idea of transferring your car loan to your business is appealing, it’s important to understand that it’s not a guaranteed process. Several factors come into play, and lenders have specific criteria you’ll need to meet. It’s more accurately described as refinancing the loan in your business’s name rather than a direct transfer.

Here’s what typically needs to happen:

Lender Approval is Key: The most critical step is getting approval from a lender. You can’t just move a loan from one entity to another without going through a formal application process.

Business Structure Matters: The type of business you have (sole proprietorship, LLC, S-corp, etc.) will influence how the loan is handled. Some structures might make the process simpler than others.

Vehicle Usage Requirements: Lenders will want to ensure the vehicle is primarily used for business purposes. If the car is mostly for personal use, they may not approve the loan transfer.

Your Business’s Financial Health: Your business will need to demonstrate its ability to repay the loan. This means showing strong financials, a healthy cash flow, and good credit history for the business itself.

How to Transfer Your Car Loan to Your Business: A Step-by-Step Approach

Ready to make the move? Here’s a breakdown of the process, designed to be easy to follow.

Step 1: Assess Your Eligibility and Business Needs

Before you talk to any lenders, take a good look at your situation.

Business Use Percentage: Honestly evaluate how much you use the car for business. Most lenders require a significant majority of usage (often 50% or more) to be for business purposes. Keep records of your mileage if you haven’t already.

Business Financials: Gather your business’s financial statements. This includes profit and loss statements, balance sheets, and bank statements. You’ll need to show you have the capacity to manage this new debt.

Business Credit Score: If your business has been operating for a while, check its credit score. A good score will significantly help your application. If your business is new, you might be relying more on your personal credit, depending on the lender and business structure.

Personal vs. Business Loan: Understand the difference. A personal loan is tied to your individual credit. A business loan is tied to your business’s credit and financial health.

Step 2: Gather Necessary Documentation

Lenders will need proof of your business’s legitimacy and financial standing. Be prepared with:

Business Legal Documents: Articles of Incorporation, Operating Agreement, Partnership Agreement, or Sole Proprietorship registration.

Business Financial Records: Recent tax returns (business and personal), bank statements (business and personal), profit and loss statements, and balance sheets.

Vehicle Information: Details about the car, including its make, model, year, VIN, and your current loan payoff amount. You’ll also need proof of ownership or title.

Proof of Business Use: Mileage logs, invoices, or receipts that demonstrate how the vehicle is used for business.

Step 3: Research Lenders and Loan Options

You’ll need to find a lender that offers business auto loans. Don’t just go with the first one you find.

Banks and Credit Unions: Your existing business bank or a local credit union might be good places to start. They often have established relationships with local businesses.

Online Business Lenders: Many online platforms specialize in business loans, including auto loans for vehicles. These can sometimes offer faster approvals and more flexible terms.

Specialized Auto Lenders: Some lenders focus specifically on auto financing for businesses.

Compare Rates and Terms: Look at the Annual Percentage Rate (APR), loan term, fees, and any prepayment penalties. A lower APR and reasonable fees will save you money in the long run.

Consider Refinancing: If your business is being approved for a loan, it’s essentially a refinance. You’re paying off your personal loan with the new business loan.

Step 4: Apply for the Business Auto Loan

Once you’ve chosen a lender and have all your documents in order, it’s time to apply.

Complete the Application: Fill out the lender’s application form accurately and completely. Be prepared to provide detailed information about your business, its finances, and yourself as the owner.

Submit Documentation: Upload or submit all the required documents. Double-check that everything is clear and legible.

Professionalism Counts: Present your business in the best possible light. A well-organized application and clear financial records make a strong impression.

Step 5: Underwriting and Approval Process

The lender will now review your application and documentation.

Credit Checks: They will check your business credit score and potentially your personal credit score, especially if you have a newer business or are required to personally guarantee the loan.

Financial Review: They’ll scrutinize your financial statements to assess your business’s repayment ability.

Vehicle Valuation: The lender may also appraise the vehicle to confirm its value and ensure it aligns with the loan amount. You can get an idea of your car’s value through resources like Kelley Blue Book (KBB) or NADA Guides.

Loan Offer: If approved, you’ll receive a loan offer detailing the terms and conditions. Review this offer carefully.

Step 6: Finalize the New Loan and Pay Off the Old One

If you accept the loan offer, it’s time to close the deal.

Sign Loan Documents: You’ll sign the paperwork for the new business auto loan.

Lender Pays Off Original Loan: The new lender will typically disburse the funds directly to your old lender to pay off your personal car loan in full.

Update Title and Registration (If Necessary): Depending on your state and the lender’s requirements, you might need to update the vehicle’s title and registration to reflect the new lienholder (the business lender). This is a crucial step to ensure the vehicle is officially a business asset with the proper security for the new loan.

Step 7: Adjust Your Business Accounting

With the loan successfully transferred, make sure your accounting reflects the change.

Record New Loan Payments: Ensure that all future loan payments are recorded as business expenses.

Track Deductible Interest: Keep track of the interest paid on the new business loan, as this is likely tax-deductible.

Consult Your Accountant: It’s always a good idea to discuss these changes with your accountant to ensure you’re maximizing tax benefits and complying with all regulations.

Key Considerations and Potential Pitfalls

While transferring a car loan to your business can offer many benefits, it’s not without its challenges. Being aware of these can help you navigate the process smoothly.

Personal Guarantee: Many lenders, especially for newer or smaller businesses, will require a personal guarantee. This means that if the business defaults on the loan, you are personally responsible for repaying it. This is a common practice and doesn’t negate the benefits of the loan being a business expense.

Credit Score Impact:

Applying for a new loan will involve a hard credit inquiry, which can temporarily lower your credit score. This is a standard part of any loan application process. If your business is relatively new and you haven’t established business credit, the lender might heavily rely on your personal credit history, impacting it directly.

LTV Ratio (Loan-to-Value): Lenders will assess the car’s current value against the loan amount. If you owe more on the loan than the car is worth (being “upside down”), it might be harder to get approved or you may need to bring cash to the table to bridge the gap. You can check the car’s value using resources like Edmunds.

Increased Business Debt:

Adding a car loan increases your business’s overall debt load. Ensure that your business can comfortably handle the monthly payments without straining its cash flow. Lenders will look at your debt-to-income ratio for the business.

Insurance Needs: Once the loan is transferred to the business, you may need to adjust your auto insurance policy. You might need commercial auto insurance or a commercial rider on your existing policy, as business use often carries different risks than personal use. Check out resources from the Small Business Administration (SBA on Business Insurance) for guidance.

Impact on Personal Credit:

If the loan is fully transferred and paid off by the business, it will be removed from your personal credit report as a liability. However, if you provide a personal guarantee, the loan might still appear on your personal credit report as a contingent liability.

Tools and Resources to Help You

Navigating this process might seem daunting, but there are resources available to assist you.

Business Financial Software

Software like QuickBooks, Xero, or Wave can help you organize your business’s financial records. This makes it easier to generate the profit and loss statements and balance sheets lenders will require. Proper bookkeeping is vital for demonstrating financial health.

Credit Monitoring Services

Services that allow you to monitor your business credit score can be very helpful. Many also offer alerts for significant changes or new inquiries on your business credit report.

Accountant or Financial Advisor

A good accountant or financial advisor can offer invaluable advice on structuring your finances, understanding tax implications, and preparing for loan applications. They can help you present your business’s financial picture in the best possible light.

Online Loan Calculators

Before applying, use online loan calculators to estimate monthly payments based on different loan amounts, interest rates, and terms. This helps you understand the financial commitment and compare offers from various lenders.

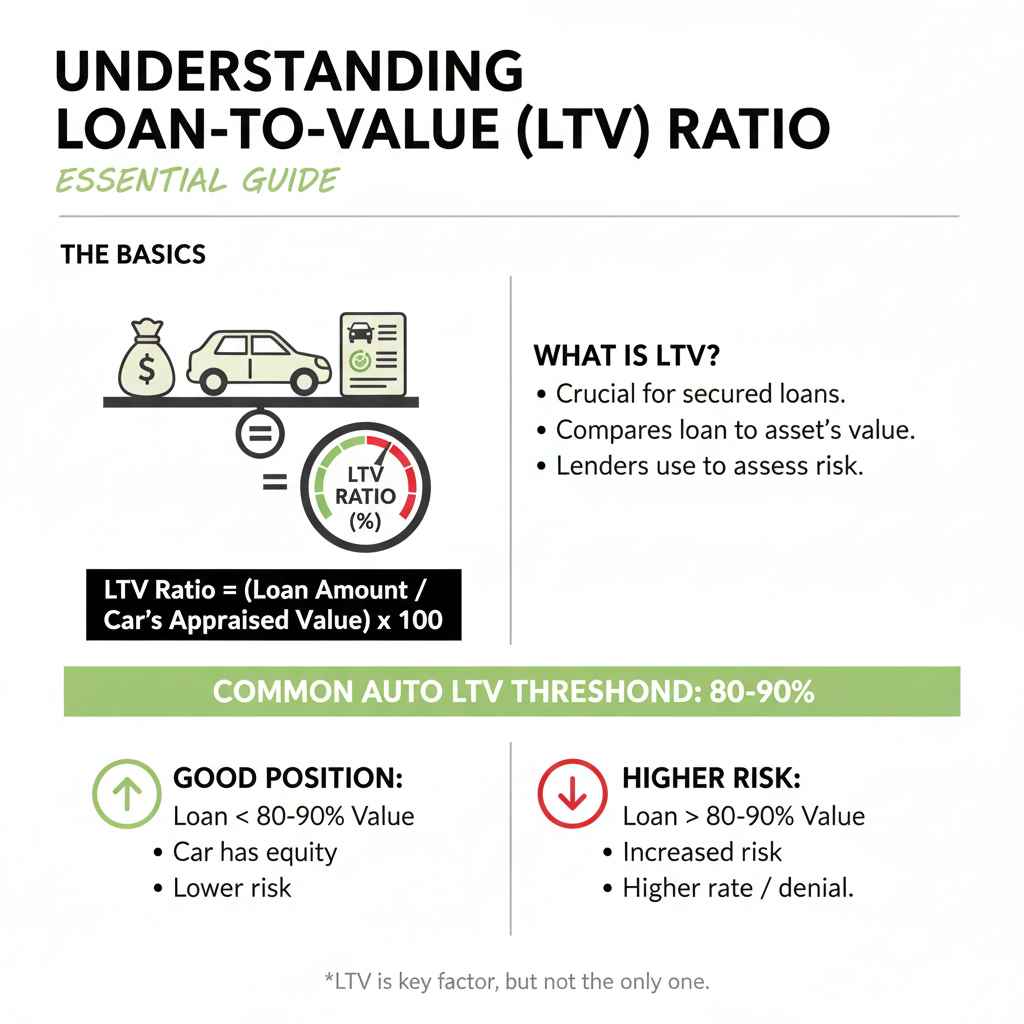

Understanding Loan-to-Value (LTV) Ratio

The Loan-to-Value (LTV) ratio is a crucial metric lenders use when considering any loan secured by an asset, like your car. It compares the amount of the loan to the appraised value of the asset itself.

A common LTV threshold for auto loans is around 80-90%. This means the lender is typically willing to finance up to 80-90% of the car’s value.

If your Loan Balance is LESS than 80-90% of the Car’s Value: You’re in a good position. The car has enough equity to secure the loan comfortably.

If your Loan Balance is MORE than 80-90% of the Car’s Value: You might be considered a higher risk. The lender might require a larger down payment, a higher interest rate, or deny the loan altogether.

If you owe MORE than the car is worth (Negative Equity): You will almost certainly need to pay the difference between the loan payoff amount and the car’s value in cash to complete the refinance into a business loan.

Understanding your car’s current market value is therefore essential. You can get estimates from reputable sources:

| Source | Website/Type of Resource | What They Offer |

|---|---|---|

| Kelley Blue Book | kbb.com | Used car values, trade-in values, private party sale values |

| Edmunds | edmunds.com | Car appraisals, estimated market value |

| NADA Guides | nadaguides.com/Cars | Wholesale and retail values for vehicles |

Having this information handy will help you gauge your eligibility before approaching lenders.

Common Misconceptions About Business Auto Loans

It’s easy to get caught up in what seems like a simple process, but there are some common myths that can cause confusion. Clearing these up ensures you’re making informed decisions.

Myth 1: It’s Just a Paperwork Shuffle: Many people think you can just fill out a form and the loan is transferred. In reality, it’s a full loan refinancing process requiring credit checks, financial reviews, and lender approval.

Myth 2: My Personal Loan Automatically Becomes a Business Expense: Unless you go through the official refinancing process, your personal loan payments are not automatically deductible for your business.

Myth 3: All Business Loans Require a Perfect Business Credit Score: While a strong business credit score helps, many lenders will also consider your personal credit history, especially for small businesses. Some lenders even specialize in working with businesses that have limited credit history.

* Myth 4: I Can’t Transfer the Loan if the Car is Older: Age and mileage can affect the car’s value, but many lenders will finance business auto loans for older vehicles, provided the LTV ratio is favorable and the business can afford the payments.

Frequently Asked Questions (FAQ)

Can I transfer my car loan to my business if I’m a sole proprietor?

Yes, sole proprietors can often transfer their car loan to their business. In this structure, your personal and business finances are closely linked. You’ll still go through a refinancing process, and the lender will assess both your personal creditworthiness and your business’s income generated from the vehicle’s use. Making the loan a business expense helps in clearly separating your business finances for tax purposes.

What if my car is used by both myself and employees for business?

If your car is used by you and other employees for business, this actually strengthens the case for it being a business vehicle. You’ll need to clearly document the business usage by all parties. This might involve detailed mileage logs for everyone using the car for work-related activities to demonstrate significant business use.

How much of the car’s value can a business loan cover?

This depends on the lender and involves the Loan-to-Value (LTV) ratio. Generally, lenders will finance up to 80-90% of the car’s current market value.