How to Get a Car Loan at 18: Proven Success Secret

Getting a car loan at 18 is achievable by building credit, proving income, and exploring specific lender options. While a cosigner helps, focusing on these personal qualifications can lead to success.

Dreaming of hitting the open road in your own car? At 18, that dream can feel a bit out of reach, especially when loans are involved. Many young drivers wonder if it’s even possible to get a car loan at such a young age. It’s a common hurdle, leaving many feeling stuck. But don’t worry! With the right approach, you can absolutely navigate the process and drive away in your own vehicle. This guide will break down exactly how to make it happen, step-by-step.

Your First Car Loan: Making it Happen at 18

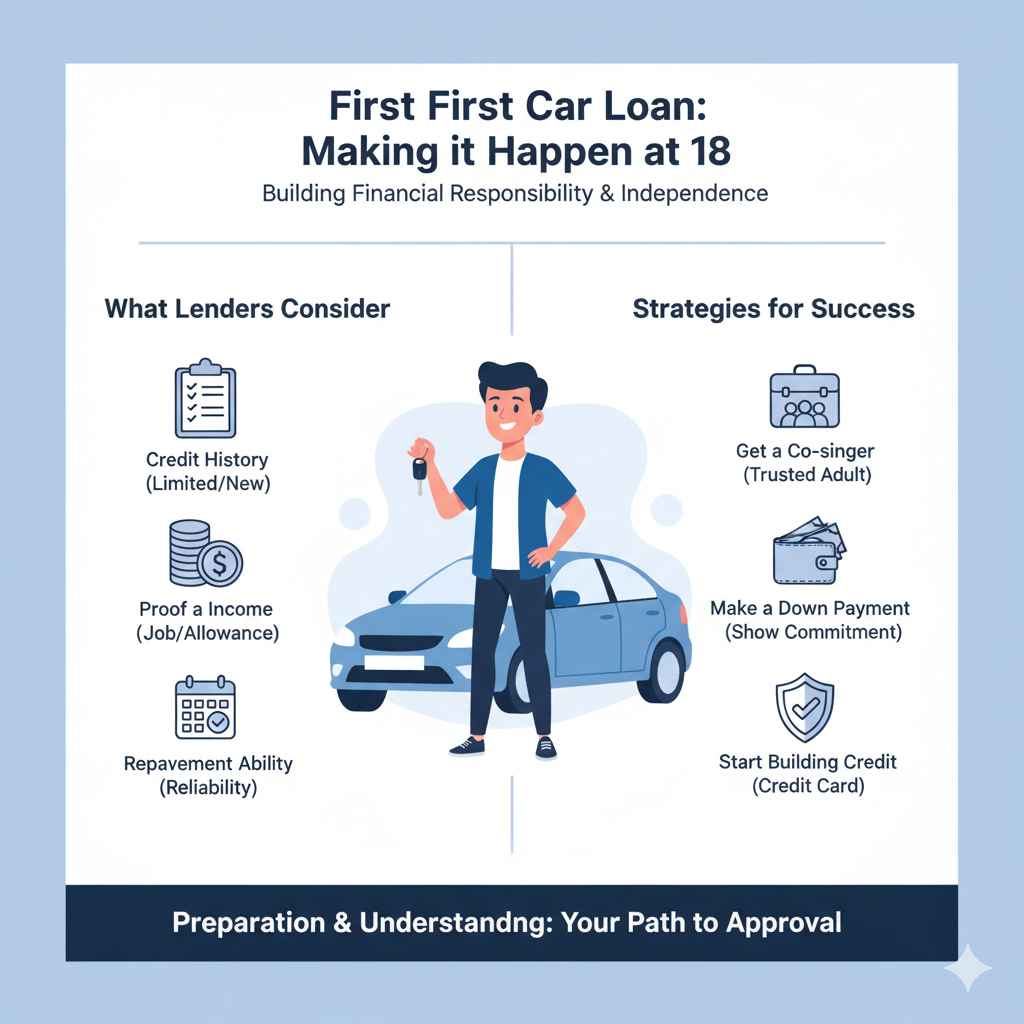

As an automotive guide, I’ve seen firsthand how exciting and, at times, overwhelming the car-buying journey can be for young adults. Getting your first car loan at 18 is a significant step towards independence. It’s not just about buying wheels; it’s about building financial responsibility. Let’s look at what lenders consider and how you can present yourself as a great candidate.

Understanding Car Loans for Young Drivers

When you’re 18, lenders see you as a new entrant into the financial world. This means you likely have a limited credit history, which can make some traditional lenders hesitant. They want to see that you’re a reliable borrower who can make payments on time. The good news is, there are strategies specifically designed to help individuals with less experience secure an auto loan.

The “secret” isn’t really a secret at all; it’s about preparation and understanding the lender’s perspective. By focusing on a few key areas, you can significantly boost your chances of approval.

The Core Pillars of Car Loan Approval at 18

Securing a car loan at 18 hinges on demonstrating your financial readiness. Lenders are looking for a few key indicators. Let’s break down the most important ones:

1. Building and Understanding Your Credit Score

Your credit score is like your financial report card. A higher score tells lenders you’re a responsible borrower. At 18, this might be a blank slate. Here’s how to start building it:

- Secured Credit Card: This is a card where you put down a deposit, which becomes your credit limit. Use it for small, planned purchases and, critically, pay the balance in full every month. This shows consistent, responsible use.

- Being an Authorized User: If a parent or trusted adult has good credit, they can add you as an authorized user on their credit card. Their positive payment history can then reflect on your credit report. Ensure they manage their card responsibly!

- Small Installment Loan: Sometimes, a small loan, like one from a credit union for a few hundred dollars, can help establish a payment history if managed perfectly.

It’s crucial to monitor your credit report. You are entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year through AnnualCreditReport.com. Reviewing it helps you spot errors and understand your progress.

2. Proving Your Income and Employment Stability

Lenders need to know you have a steady stream of income to make loan payments. This is especially important if you don’t have a long credit history.

- Stable Employment: Aim for a job where you’ve been employed for at least six months to a year. Lenders prefer stability.

- Sufficient Income: You need to demonstrate that your income covers your living expenses (rent, food, insurance) plus the car payment and associated costs (gas, maintenance). A common guideline is that your total monthly debt payments, including the new car loan, shouldn’t exceed 40%-50% of your gross monthly income.

- Pay Stubs and Bank Statements: Gather recent pay stubs (usually the last 2-3) and bank statements to verify your income. If you’re self-employed, you might need tax returns.

Sometimes, lenders might request proof of employment directly from your employer, so ensure your workplace can provide that information.

3. Down Payment Power

A down payment is a sum of money you pay upfront towards the car’s purchase price. It reduces the amount you need to borrow, making the loan smaller and less risky for the lender.

- Reduces Loan Amount: A larger down payment means a smaller loan principal, leading to lower monthly payments and less interest paid over time.

- Demonstrates Commitment: It shows the lender you’re serious about the purchase and have saved money, which can also improve your chances of approval.

- Saving Strategies: Start saving early! Look for ways to cut expenses, take on extra work, or even consider selling items you no longer need. Even a few hundred dollars can help.

While not always mandatory, a down payment significantly strengthens your application, especially at 18 without a deep credit history.

4. The Role of a Cosigner (and How to Get a Loan Without One)

A cosigner is someone, usually a parent or relative, who agrees to be legally responsible for the loan if you fail to make payments. They essentially use their good credit history to back your application.

Benefits of a Cosigner:

- Significantly increases your chances of approval.

- May help you secure a lower interest rate.

- Can help you build your own credit history positively if managed well.

How to Get a Car Loan at 18 Without a Cosigner:

This is where the “proven success secret” comes into play for many. Focus intensely on the first three pillars:

- Build Credit Diligently: Start early with a secured card or by being an authorized user well in advance of needing the loan. Aim for a score of 650 or higher, though some lenders may go lower.

- Demonstrate Strong, Stable Income: The more consistent and plentiful your income, the more confident a lender will be.

- Save for a Significant Down Payment: This is perhaps the most impactful strategy. A down payment of 10-20% can make a huge difference.

- Shop Around: Don’t apply everywhere at once, but do compare offers from different types of lenders (see next section).

- Consider “Buy Here, Pay Here” Dealerships (with caution): These dealerships often finance customers directly. They may focus more on your income and ability to pay than your credit score. However, interest rates can be very high, and vehicle quality may vary. It’s a fallback option if other avenues close.

It requires more effort and planning to go it alone, but it’s perfectly achievable!

Where to Apply for a Car Loan at 18

Not all lenders are created equal, and some are more friendly to young applicants than others.

1. Credit Unions

Credit unions are non-profit organizations, and their primary goal is to serve their members. They often offer more flexible terms and competitive rates, especially for younger members. Many have specific programs designed to help young adults build credit. You usually need to become a member by meeting certain criteria (like living in a specific area or working for a particular employer).

The National Credit Union Administration (NCUA) provides information on how credit unions work.

2. Banks

Traditional banks can be a good option, especially if you already have a relationship with them (e.g., a checking or savings account). They have established loan programs but might be stricter with younger applicants without a strong credit history or a cosigner. It’s worth speaking to the personal loan department at your bank during business hours.

3. Online Lenders

Many online lenders specialize in auto loans and may have specific programs for first-time buyers or those with limited credit. They often have quick application processes and can provide pre-approval quickly. Research reputable online lenders and compare their rates and terms carefully. Be wary of lenders who guarantee approval regardless of your credit history or income – this can be a red flag.

4. Dealership Financing (Manufacturer & Independent)

Dealerships can be convenient because they handle the financing on-site. Manufacturer-backed financing (e.g., Toyota Financial Services, Ford Credit) can sometimes have special offers for new cars. Independent dealerships may have their own financing arms or work with various lenders. As mentioned, “Buy Here, Pay Here” dealerships are a specific type to consider with caution.

The Application Process: What to Expect

Once you’ve chosen where to apply, the process is generally straightforward:

- Pre-Approval: It’s often wise to get pre-approved first. This lets you know how much you can borrow and at what interest rate before you even look at cars. It also strengthens your negotiation position.

- Gather Documents: You’ll need proof of identity (driver’s license, state ID), proof of income (pay stubs, bank statements), proof of address (utility bill, lease agreement), and sometimes references.

- Complete Loan Application: Fill out the lender’s application form accurately and honestly.

- Vehicle Information: If you’re applying for a specific car, the lender may need its VIN (Vehicle Identification Number), make, model, and year.

- Review and Sign: If approved, carefully review all the loan terms, including the interest rate (APR), loan term (length of repayment), and any fees. Sign the loan agreement.

Key Terms to Understand

Navigating loan jargon can be confusing. Here are some essential terms:

| Term | Meaning |

|---|---|

| APR (Annual Percentage Rate) | The yearly cost of borrowing money, including interest and fees. It’s the true cost of the loan. |

| Loan Term | The length of time you have to repay the loan (e.g., 36, 48, 60 months). Shorter terms mean higher monthly payments but less interest paid overall. |

| Principal | The actual amount of money you borrow for the car. |

| Interest | The fee a lender charges for lending you money. |

| Down Payment | The upfront cash you pay towards the car’s purchase price. |

| Monthly Payment | The fixed amount you pay each month towards the loan. |

| Collateral | The car itself serves as collateral for the loan. If you don’t pay, the lender can repossess the car. |

Calculating Your Car Payment

Before you apply, it’s smart to get an idea of what your monthly payment might look like. Multiple online auto loan calculators can help. You’ll need to input:

- The total price of the car (or the loan amount you expect to need)

- The estimated APR you might qualify for

- The loan term you’re considering (e.g., 60 months)

For example, borrowing $15,000 at 7% APR for 60 months could result in a monthly payment of roughly $295. Remember to also factor in insurance, gas, and maintenance, which are separate costs of car ownership.

A good resource to play with these numbers is a loan calculator from a reputable financial institution or consumer advocacy group.

Avoid Common Pitfalls

Even with a solid plan, there are traps to watch out for:

- Impulse Buying: Falling in love with a car before knowing your budget or loan terms.

- Focusing Only on Monthly Payment: Lenders sometimes try to sell cars by focusing on low monthly payments, which can be achieved by extending the loan term over many years, costing you far more in interest.

- Ignoring Insurance Costs: Car insurance, especially for young drivers, can be a significant expense. Get insurance quotes before you buy! Many states require minimum coverage, and lenders will likely require comprehensive and collision coverage. For example, the Insurance Information Institute (III) notes that age is a factor in car insurance rates, with younger drivers often paying more.

- Not Reading the Fine Print: Missed payments, late fees, early termination penalties – understand everything before you sign.

Frequently Asked Questions (FAQ)

Q1: Can I get a car loan at 18 with no credit history at all?

A: It’s difficult but not impossible. Your best bet is to find a lender that works with first-time buyers or to have a cosigner. Building some credit beforehand, even just a few months, will help significantly.

Q2: What credit score do I need to get a car loan at 18?

A: Lenders have different requirements. For a standard loan without a cosigner, a score of 650 or higher is generally good. However, some lenders might work with scores in the high 500s or low 600s, often with a higher interest rate or a requirement for a larger down payment.

Q3: How much of a down payment do I need for a car loan at 18?

A: There’s no set rule, and it depends on the lender and the car. However, aim for at least 10% of the car’s price. A larger down payment (20% or more) will significantly improve your chances and get you better terms.

Q4: What’s the difference between a car loan and a personal loan for a car?

A: A car loan is specifically for buying a vehicle and is secured by the car itself (the collateral). A personal loan can be used for anything, including a car, but it’s usually unsecured, meaning it might have a higher interest rate and you’d still need to demonstrate your ability to repay.

Q5: How long will it take to get approved for a car loan?

A: The timeline can vary. Getting pre-approved online can take minutes to a few hours. A full loan approval through a dealership or bank might take a business day or two, especially if they need to verify more information.

Q6: Should I buy a new or used car with my first loan?

A: For a first loan at 18, a used car is often a smarter choice. They are typically less expensive, meaning a smaller loan amount, lower insurance premiums, and less depreciation (the car losing value). This makes it easier to manage payments and build a positive payment history.

Conclusion: Driving Towards Your Independence

Getting a car loan at 18 is a significant milestone that marks the beginning of your independent journey. It requires planning, diligence, and a clear understanding of what lenders look for. By focusing on building good credit, proving your income, saving for a down payment, and knowing where to shop for loans, you can overcome the hurdles that often face young applicants.

Remember, the “secret” is simply smart financial preparation. Take it one step at a time, stay organized, and don’t be afraid to ask questions. You’ve got this! Your hard work in preparing your financial profile will pay off, putting you in the driver’s seat of your own car before you know it.