How to Get a Nice Car at 18 (Smart Guide) for Young Adults

Getting a nice car at 18 is a big dream for many young people! It can seem hard since you’re just starting, and figuring out how everything works can be tricky. But don’t worry, it’s definitely possible! This guide, How to Get a Nice Car at 18 (Smart Guide), will break down the steps, making it easy to understand. We’ll explore different options, from saving money to financing, so you can drive your dream car sooner. Let’s get started and make your car goals a reality.

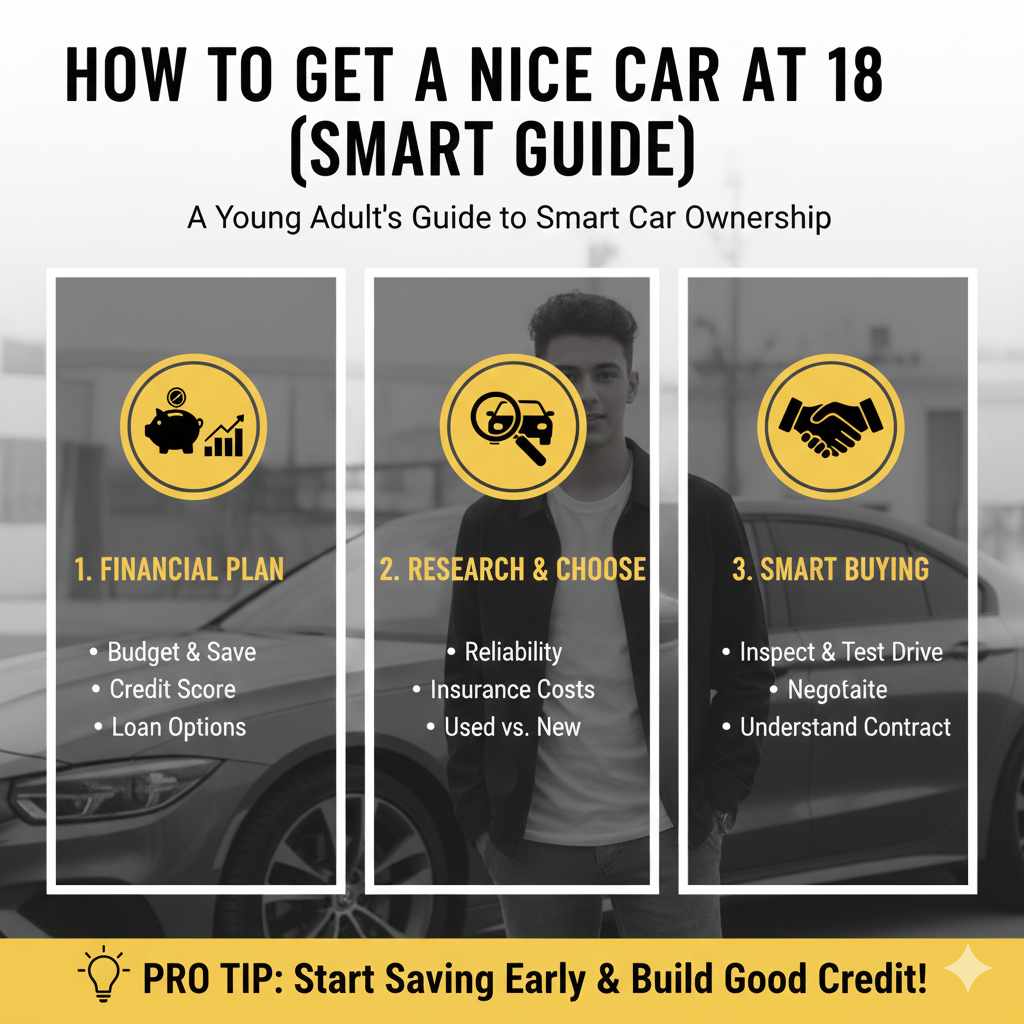

Setting Financial Goals and Saving for a Car

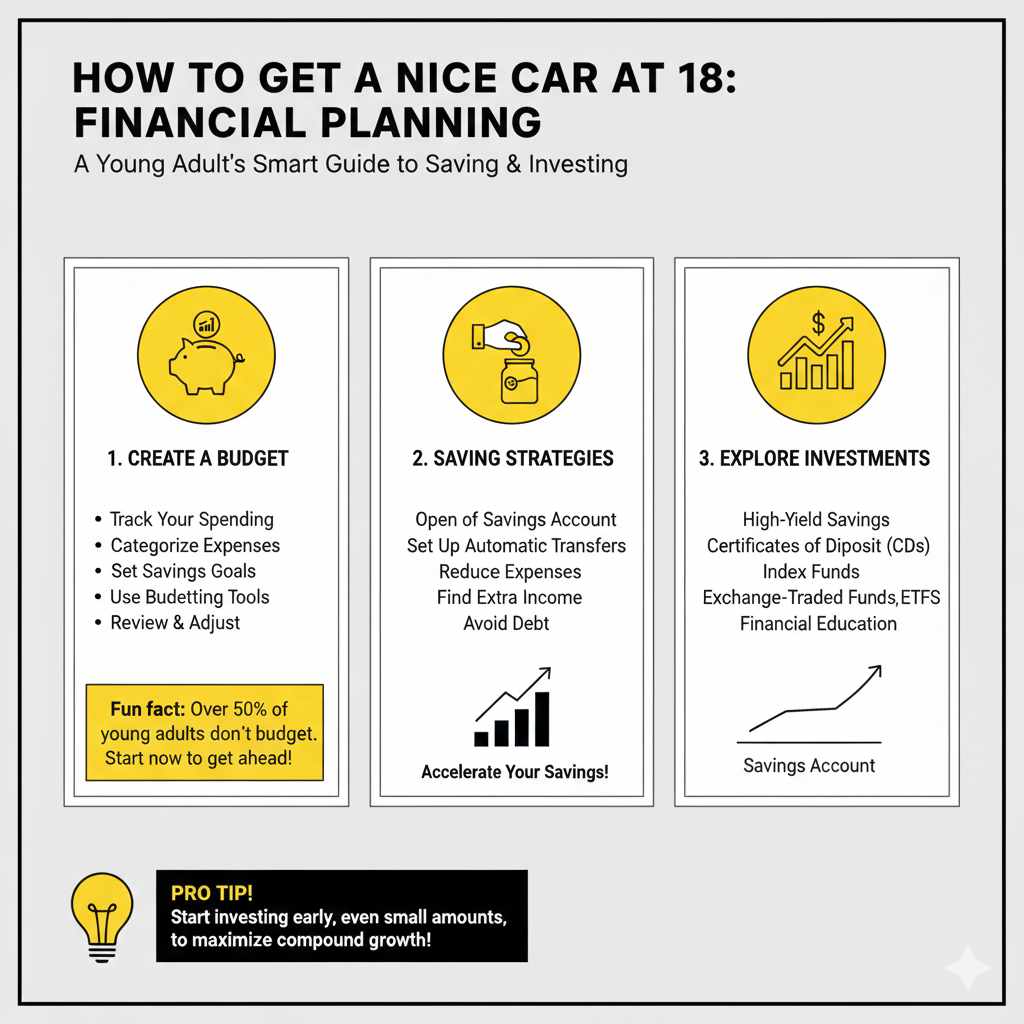

The first step toward owning a nice car at 18 is planning your money. You need to figure out how much you can spend and create a savings plan. This means making a budget to track your income and expenses. Identifying where your money goes each month helps you see where you can cut back to save for your car. Setting realistic goals, like how much you need to save each month, keeps you motivated. Start small, and you’ll soon see your savings grow! You can use various methods to keep track of your income and expenses, such as budgeting apps or simple spreadsheets.

Creating a Budget

Creating a budget might seem difficult, but it’s really about making a plan for your money. Think of it as giving every dollar a job. First, list all your income sources, like your part-time job or allowance. Then, list all your expenses. These can be divided into two main categories: fixed expenses and variable expenses. Fixed expenses are costs that stay the same each month, like a phone bill. Variable expenses change, like spending on entertainment or gas for your current car. By seeing where your money goes, you can make smarter decisions and save more. There are plenty of free budgeting templates and apps available that can help you along the way.

- Track Your Spending: Keep a record of everything you spend money on. This helps you know where your money is going.

- Categorize Expenses: Sort your spending into categories such as housing, food, transportation, and entertainment.

- Set Savings Goals: Decide how much you want to save each month for your car. Make this a priority.

- Use Budgeting Tools: There are many apps and spreadsheets designed to help you budget.

- Review and Adjust: Regularly check your budget and make changes as needed. Life changes, and so should your budget.

Saving Strategies

Once you’ve made a budget, the next step is building your savings. Think of your savings as a separate pot of money dedicated to your car goal. A crucial step is setting up a dedicated savings account. This makes it easier to keep track of your money and helps avoid the temptation to spend it on other things. Consider setting up automatic transfers from your checking account to your savings account each month, even if it’s a small amount. Every little bit helps! Finding ways to boost your income, such as taking on extra work or selling old items, can accelerate your savings progress.

- Open a Savings Account: Choose a bank account specifically for your car savings.

- Set Up Automatic Transfers: Schedule regular transfers from your checking account to your savings account.

- Reduce Expenses: Look for areas where you can cut back on spending. Maybe you can pack your lunch or skip a few streaming services.

- Find Extra Income: Consider part-time jobs, freelancing, or selling things you no longer need.

- Avoid Debt: Try to stay away from unnecessary debt, as it can hinder your savings.

Investment Options for Young People

While savings accounts are a great start, exploring investment options can help your money grow faster. However, as a young person, you will need to consider risks, so only put money in investments you are okay with potentially losing. Simple options include high-yield savings accounts or Certificates of Deposit (CDs), which offer slightly higher interest rates. If you’re okay with some risk, consider investing in the stock market through exchange-traded funds (ETFs) or mutual funds. They offer a simple way to diversify your investments. Remember to research and learn about each option before you invest. Start small, and build your knowledge as you go. For example, ETFs have low costs and can be an effective way to generate returns.

- High-Yield Savings Accounts: These accounts offer better interest rates than regular savings accounts.

- Certificates of Deposit (CDs): CDs lock your money in for a set time but often offer higher interest rates.

- Index Funds: They follow the performance of a specific market index.

- Exchange-Traded Funds (ETFs): ETFs are similar to index funds but can be traded like stocks.

- Financial Education: Learn about investing before you start. There are tons of free resources to learn.

Ways to Finance a Car: Loans and Other Options

Saving up for a car can take time, but there are other ways to get behind the wheel faster. Financing, which involves taking out a car loan, is a common option. The good thing about financing is that you get to use the car while paying it off over time. However, you’ll pay interest, so the car will end up costing more than its original price. You can get loans from banks, credit unions, or dealerships. Another option is a lease, which means you rent the car for a set period. It usually involves lower monthly payments, but you won’t own the car at the end. Understanding these different options is key before making a decision.

Car Loans: How They Work

A car loan is a loan specifically to buy a car. When you get a car loan, you borrow money from a bank, credit union, or dealership. You then pay back the loan in monthly installments over a set period, typically three to seven years. Each payment includes a portion of the original amount (the principal) and interest, which is the cost of borrowing the money. Before you apply for a loan, it’s wise to shop around and compare offers from different lenders. Look at the interest rates, as it directly impacts how much your car will cost overall. You’ll need a good credit score and provide income information to qualify for a loan.

- Shop Around: Compare offers from different lenders to find the best interest rate.

- Check Your Credit Score: A good credit score can help you get a better interest rate.

- Understand Interest Rates: A lower interest rate means you’ll pay less for the car overall.

- Calculate Monthly Payments: Use an online calculator to figure out your monthly payments based on the loan amount, interest rate, and loan term.

- Read the Fine Print: Carefully review the loan terms before you sign anything.

Leasing a Car: Pros and Cons

Leasing a car is another option. When you lease, you essentially rent the car for a set amount of time, usually a few years. At the end of the lease, you must return the car, or you can buy it. Leasing often involves lower monthly payments than buying with a loan. However, you don’t own the car, so you don’t build equity. Also, there are mileage limits, and you’ll have to pay extra if you go over them. Another thing to consider is that the car needs to be in good condition when returned. The upfront costs for a lease, such as down payments, are usually lower. Leasing is an appealing option if you like to drive a new car every few years.

- Lower Monthly Payments: Typically lower than loan payments.

- Drive a New Car: You can regularly drive the newest models.

- No Ownership: You don’t build equity in the car.

- Mileage Limits: You’re limited in how many miles you can drive.

- Return Conditions: You must return the car in good condition.

Choosing Between a Loan and a Lease

The choice between a loan and a lease depends on your situation and goals. If you want to own the car and build equity, a loan is better. You’ll eventually own the car outright. This means you can drive it for as long as you want and sell it later. If you prefer to drive a new car regularly and don’t care about ownership, a lease might be a good choice. Consider how you plan to use the car, how many miles you drive, and how long you want to keep the vehicle. Think about your financial situation and what you’re comfortable paying each month. There is not a single right answer; it’s what makes the most sense for you!

| Feature | Car Loan | Car Lease |

|---|---|---|

| Ownership | You own the car | You do not own the car |

| Monthly Payments | Generally higher | Generally lower |

| Mileage Limits | No limit | Mileage limits apply |

| Flexibility | You can sell the car | You must return the car at the end |

| Long-Term Cost | Potentially lower | Potentially higher |

How to Get a Nice Car at 18: Researching and Purchasing Your Vehicle

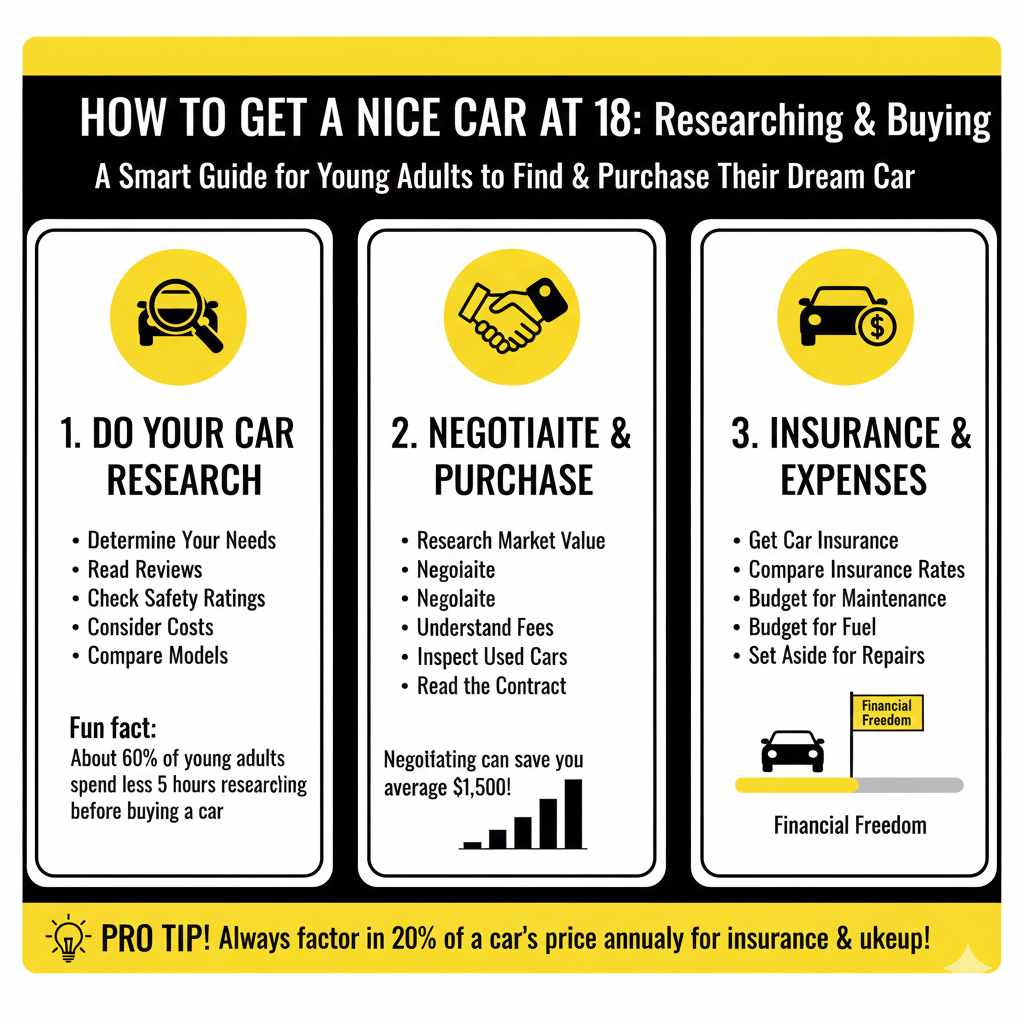

Once you’ve set your finances and decided on a loan or lease, the fun part begins: choosing your car. This involves researching different models, comparing prices, and understanding what you want and need in a vehicle. Decide what features are most important to you, like fuel efficiency, safety features, or technology. Researching different car brands, their reputations, and how reliable they are is key. Websites and magazines provide valuable information and reviews. When you’re ready to buy, you can go to dealerships or explore private sales, each with its pros and cons. Understanding the buying process helps you get the best deal and ensures a good buying experience.

Doing Your Car Research

Before you even step foot in a dealership, do your homework! Start by figuring out your needs and wants. What will you use the car for? What kind of driving do you usually do? Next, look at different models that fit your criteria. Read reviews from trusted sources like Consumer Reports or Edmunds. See what other people say about their experiences. Check the vehicle’s safety ratings from the National Highway Traffic Safety Administration (NHTSA) and the Insurance Institute for Highway Safety (IIHS). Also, consider the cost of ownership, including fuel efficiency, insurance costs, and maintenance. Knowing the true costs helps you make an informed decision and ensures you choose a vehicle that fits your budget.

- Determine Your Needs: Decide what you need the car for (commuting, road trips, etc.).

- Read Reviews: Look at expert and customer reviews to see what others say.

- Check Safety Ratings: Review safety ratings from reputable sources.

- Consider Costs: Research the cost of fuel, insurance, and maintenance.

- Compare Models: Compare different car models to find the best fit for your needs and budget.

Negotiating and Purchasing Your Vehicle

Once you’ve chosen a car, it’s time to purchase. If you’re buying from a dealership, be prepared to negotiate the price. Start by researching the car’s market value, so you know a fair price. Don’t be afraid to make an offer lower than the asking price. Negotiate the price of the car and also any additional fees. Consider your trade-in (if applicable), and ensure you understand the terms of your financing if you’re using it. If buying a used car, have it inspected by a trusted mechanic before you make a purchase. They can check for hidden problems. Take your time, and don’t feel pressured to buy right away. Buying a car is a big decision; do your homework!

- Research Market Value: Know the car’s worth before you negotiate.

- Negotiate: Don’t be afraid to make an offer lower than the asking price.

- Understand Fees: Be sure you understand all fees associated with the purchase.

- Inspect Used Cars: Always have a mechanic inspect a used car.

- Read the Contract: Carefully read all the paperwork before you sign.

Insurance and Ongoing Car Expenses

Buying a car doesn’t end with the purchase; you need insurance and must manage ongoing costs. Car insurance is required to drive legally, and costs vary based on your age, driving record, and the car’s make and model. Get quotes from different insurance companies to find the best rates. You’ll also need to consider other ongoing costs, like fuel, maintenance, and potential repairs. Schedule regular maintenance, such as oil changes and tire rotations, to keep your car running smoothly and avoid problems. Creating a budget that includes these ongoing expenses is essential for keeping your car. Managing these costs ensures a safe and reliable driving experience.

- Get Car Insurance: You must have car insurance to drive.

- Compare Insurance Rates: Get quotes from multiple insurance companies.

- Budget for Fuel: Estimate how much you’ll spend on fuel each month.

- Plan for Maintenance: Schedule regular maintenance to keep your car in good shape.

- Set Aside for Repairs: Budget for unexpected repairs.

Frequently Asked Questions

Question: What’s the best way to start saving for a car?

Answer: The best way to begin is by creating a budget and setting a specific savings goal. Identify all income sources and track your expenses to find ways to reduce spending. Then, consider opening a dedicated savings account and set up automatic transfers. Look for options like high-yield savings accounts that offer better interest rates to make your money grow.

Question: How does my credit score affect getting a car loan?

Answer: Your credit score greatly affects whether you can get a car loan and the interest rate you’ll receive. A good credit score can help you get a lower interest rate, which means you’ll pay less for the car overall. A low credit score might make it harder to get approved or result in a higher interest rate. It’s smart to check your credit report and address any errors before applying for a loan.

Question: What are the pros and cons of leasing a car?

Answer: The pros of leasing include lower monthly payments and the ability to drive a new car every few years. However, you don’t own the car, you’re limited on mileage, and you must maintain the car in good condition. Leasing may also cost more than financing. Leasing is an appealing option if you like driving the latest models and don’t care about ownership. It has different pros and cons.

Question: How can I find the best deal when buying a car?

Answer: Finding the best deal involves research, comparison, and negotiation. Research the market value of the car before you negotiate. Compare prices at different dealerships or consider private sales. Don’t be afraid to negotiate the price and any additional fees, such as financing. Check for promotions or rebates. If buying used, get a mechanic to inspect the car before you purchase.

Question: What are some ongoing costs of owning a car?

Answer: The ongoing costs of owning a car include car insurance, fuel, maintenance, and potential repairs. Insurance costs vary based on your age, the car’s make and model, and your driving record. You’ll need to budget for regular maintenance, like oil changes and tire rotations, to keep your car running smoothly, and create a reserve for unexpected repairs. Fuel costs depend on how much you drive and the car’s fuel efficiency.

Final Thoughts

Getting a nice car at 18 is an achievable goal, and the path involves smart planning and informed choices. First, create a budget and start saving early. Explore different ways to finance a car, like loans or leases, knowing their pros and cons. Research car models and compare prices to find the best fit for your needs and budget. Remember to negotiate, understand all fees, and plan for ongoing costs like insurance and fuel. With careful planning and diligence, you can get the car you want. Embrace the process, learn from your experiences, and celebrate your success when you drive off in your new car! Good luck, and enjoy the drive!