What Happens If You Surrender a Non-Running Car in Chapter 13?

Figuring out what to do with a car that doesn’t run when you’re in Chapter 13 bankruptcy can feel a bit tricky. Many people wonder, What Happens If You Surrender a Non-Running Car in Chapter 13? It’s a common question, especially if you’re new to this process. Don’t worry, though! This guide is here to make it super simple. We’ll walk through everything step-by-step. First, let’s look at why this situation comes up and how it affects your bankruptcy plan.

Understanding Non-Running Car Surrender in Chapter 13

When you file for Chapter 13 bankruptcy, you create a repayment plan to catch up on debts over three to five years. This plan often involves dealing with secured debts, like car loans. If your car isn’t running, it might seem like a simple item to get rid of, but there are specific rules to follow. Understanding these rules is key to a smooth Chapter 13 process. This section will lay out the basics of why surrendering a non-running car might be your best option and what that actually means in terms of your bankruptcy.

Why Surrender a Non-Running Car?

There are several good reasons why you might decide to surrender a non-running car during your Chapter 13 bankruptcy. One of the main drivers is cost. Keeping a car that doesn’t run means you still have to pay for insurance and storage, even if it’s just sitting there. These costs add up and take money away from your bankruptcy repayment plan. If the car is old, has major mechanical issues, and isn’t worth fixing, it might be more financially smart to let it go.

Another reason is that the loan balance on the car might be much higher than its actual market value, especially if it’s not in running condition. If the car isn’t running, its value is significantly less, and trying to keep it might not make financial sense in the long run. Surrendering it means you hand the car back to the lender, and the remaining debt might be treated differently within your Chapter 13 plan.

Sometimes, the car might simply be a burden. If it’s costing you money to maintain or store and you don’t have the funds or desire to repair it, surrendering it can lighten your financial load. This allows you to focus your resources on other more pressing debts and your Chapter 13 plan.

The Legal Process of Surrender

When you decide to surrender a non-running car in Chapter 13, it’s not just a matter of leaving the keys somewhere. You must inform your bankruptcy trustee and the court of your intention. This is typically done by listing the car and its secured loan in your bankruptcy petition. If you want to surrender the vehicle, you will generally indicate this intention to the lender and the trustee.

The lender will then arrange to repossess the car. Since it’s not running, you might need to coordinate with the lender on how and where they can pick it up. This is different from a running car where the lender might simply come and take it. The bankruptcy court needs to be aware of this action, and your trustee will oversee the process.

After the car is repossessed, the lender will usually sell it at an auction. The sale price will then be applied to your outstanding loan balance. Any remaining amount owed on the loan after the sale is called a deficiency balance. How this deficiency balance is handled is a critical part of what happens next in your Chapter 13 case.

Impact on Your Chapter 13 Plan

Surrendering a non-running car can affect your Chapter 13 repayment plan in a few ways. Firstly, it removes the monthly car payment from your budget, which can free up money. This extra money can then be redirected to other debts or used to increase payments to unsecured creditors.

However, as mentioned, there might be a deficiency balance left after the car is sold. The treatment of this deficiency balance depends on your specific Chapter 13 plan and how it’s structured. In some cases, the deficiency might be treated as an unsecured debt, meaning it gets paid a small percentage over the life of your plan. In other situations, it might need to be addressed differently, especially if the car was considered “necessary” for your household.

It’s important that your attorney clearly communicates your intentions regarding the car to the lender and the trustee. Any miscommunication can lead to problems, such as the lender trying to repossess the car after you thought it was already surrendered and accounted for. Your bankruptcy attorney will guide you through these steps to ensure everything is handled correctly.

What Happens to the Loan Balance After Surrender?

Once you surrender a non-running car, the journey of its loan doesn’t end there. The lender will take steps to recover as much of the remaining debt as possible. This process has several stages, and understanding each one is important to know what financial impact it will have on your Chapter 13 bankruptcy. The key thing to remember is that surrender is not always the end of your obligation for the loan amount.

Car Repossession and Sale

After you officially surrender the car to the lender, they will typically arrange for it to be repossessed. Since the car is non-running, this might involve special towing services. The lender then becomes responsible for getting the vehicle from your possession.

Once the lender has the car, they will usually attempt to sell it. This is often done through an auction. The goal of the sale is to get as much money as possible for the vehicle to reduce the outstanding loan balance. The price the car sells for at auction is a crucial factor in determining the next steps.

The reality is that a non-running car often sells for much less than a working vehicle. This is because potential buyers will have to factor in the cost of repairs. This lower sale price directly impacts the amount of debt that remains.

The Deficiency Balance Explained

The term “deficiency balance” is very important here. It refers to the difference between the amount you still owed on the car loan and the amount the lender received when they sold the car. For example, if you owed $10,000 on the loan and the lender sold the non-running car for $2,000, you would have a $8,000 deficiency balance.

This deficiency balance is a debt that you may still be responsible for. In many cases, this remaining debt is treated as an unsecured debt within your Chapter 13 bankruptcy. This means it falls into the same category as credit card debts or medical bills that don’t have collateral attached to them.

Your Chapter 13 plan will outline how these unsecured debts are paid. Often, unsecured creditors receive only a small percentage of what they are owed over the course of the plan. The exact percentage depends on your income, expenses, and the total amount of your unsecured debts.

Discharging the Deficiency in Chapter 13

The good news is that Chapter 13 bankruptcy is designed to help you manage and discharge debts. The deficiency balance from the surrendered non-running car can often be included in your Chapter 13 plan.

During your Chapter 13 case, your attorney will work with the trustee and the court to ensure the deficiency is properly handled. If your plan pays off all your secured debts and a certain percentage of your unsecured debts, the remaining deficiency balance can be discharged at the end of your Chapter 13 plan. This means you would no longer owe that money.

However, if your Chapter 13 plan is set up to pay unsecured creditors 100% of their debt, then the full deficiency balance would need to be paid. This is why it is so important to have a well-structured Chapter 13 plan that accounts for all potential outcomes, including car repossession and resulting deficiencies.

Alternatives to Surrendering a Non-Running Car

While surrendering a non-running car is a common and often practical choice in Chapter 13, it’s not always the only option. Sometimes, people might want to keep their car, even if it’s not currently running. In such cases, there are specific strategies that can be employed within the Chapter 13 framework. Exploring these alternatives can help you make the best decision for your financial situation.

Repairing the Car Before Surrender

One alternative is to repair the car before surrendering it. If the cost of repairs is less than the deficiency balance you would likely incur, and if the car is essential for your transportation needs, this might be a viable option. You would use funds outside of your Chapter 13 plan to make these repairs.

After the car is repaired and running, you could then continue making your loan payments as originally planned or work with your lender on a modification if needed. It’s crucial to discuss this strategy with your bankruptcy attorney. They can help you evaluate the costs versus the benefits and ensure that this decision aligns with the goals of your Chapter 13 plan.

If you decide to keep the car after repairs, you would continue making your regular car payments as part of your Chapter 13 plan. The value of the car would still be considered, and the loan would remain a secured debt. This option generally makes sense only if the car is necessary and the repair costs are manageable.

Redeeming the Car

Another option is to “redeem” the car. Redemption in bankruptcy means paying the lender the current market value of the car in a lump sum. This allows you to keep the car and receive a clear title, free and clear of the original loan.

However, redemption typically requires you to have the funds available for a lump-sum payment, which can be challenging for individuals filing for Chapter 13 bankruptcy. If you can obtain the money through savings or a personal loan (though loans might be restricted during bankruptcy), this could be a way to keep the car.

The redemption value is usually based on the car’s actual cash value (ACV) at the time of filing for bankruptcy, not the outstanding loan balance. This can be a significant advantage if you owe much more than the car is worth. This process would involve filing a motion with the court and getting approval.

Modifying the Loan Terms

In some Chapter 13 cases, it might be possible to modify the terms of your car loan. This is often referred to as a “cramdown.” If you’ve had the car for at least 910 days (about 2.5 years) before filing bankruptcy, and if the loan balance is higher than the car’s value, you might be able to reduce the principal loan amount to the car’s current market value.

This means you would then pay back the reduced principal amount, plus interest, over the life of your Chapter 13 plan. This can significantly lower your monthly payments and the total amount you repay. However, not all car loans are eligible for cramdowns, and there are specific rules that must be met. Your bankruptcy attorney will be able to determine if your loan qualifies for this option.

Even if the car is not running, if you choose to keep it via redemption or loan modification, you will still be responsible for its repair and maintenance costs. These costs must be factored into your overall budget and Chapter 13 plan.

How Your Chapter 13 Trustee Handles the Car

Your Chapter 13 trustee plays a vital role in overseeing your bankruptcy case, and this includes handling secured assets like cars. The trustee’s job is to ensure that your bankruptcy plan is fair to your creditors and that you are complying with all court orders and bankruptcy laws. When it comes to a non-running car you decide to surrender, the trustee’s involvement is crucial for proper execution.

The Trustee’s Role in Surrender

When you indicate your intention to surrender a non-running car, the trustee is informed. They will review your bankruptcy documents to confirm that the car and its associated loan are properly listed. The trustee will also verify that your intention to surrender aligns with the terms of your proposed Chapter 13 plan.

The trustee acts as an intermediary between you, the lender, and the court. They ensure that the repossession process is handled correctly and that the lender provides proper documentation, such as a notice of sale and the final deficiency balance. The trustee’s oversight helps prevent any misunderstandings or disputes between you and the lender.

If the car is a joint asset or if there are other complexities involved, the trustee will work to resolve them. Their goal is to ensure that all assets and debts are accounted for accurately within your bankruptcy estate.

Ensuring Proper Documentation

Accurate documentation is paramount in any bankruptcy case. When you surrender a non-running car, your trustee will require proof that the lender has repossessed the vehicle and that it has been sold. This typically involves the lender providing a “repossession and sale notice” or similar documents.

These documents will detail the date of repossession, the sale date, the sale price, and the resulting deficiency balance. The trustee will review these documents to ensure they are accurate and complete. If there are any discrepancies, the trustee will work to resolve them before finalizing the accounting for that asset.

Proper documentation also helps protect you. It serves as evidence that you have complied with your obligations regarding the surrendered car, especially in relation to the deficiency balance. Without this documentation, the lender could potentially try to claim the full amount of the loan was still owed.

Calculating the Deficiency and Its Impact

Once the car has been sold and the deficiency calculated, the trustee will incorporate this information into your Chapter 13 plan. As previously mentioned, this deficiency is typically treated as an unsecured debt. The trustee, along with your attorney, will work to determine how much of this unsecured debt will be paid over the duration of your plan.

The trustee’s calculation will factor in your income, your necessary expenses, and the total amount of unsecured debt you have. For example, if your plan proposes to pay unsecured creditors 10% of their claims, the deficiency balance will be reduced by 90% upon completion of your plan.

The trustee’s office manages the distribution of funds to creditors according to the approved Chapter 13 plan. They will ensure that any payments made towards the deficiency balance are recorded and that the final discharge at the end of your plan correctly reflects any remaining debt that has been discharged.

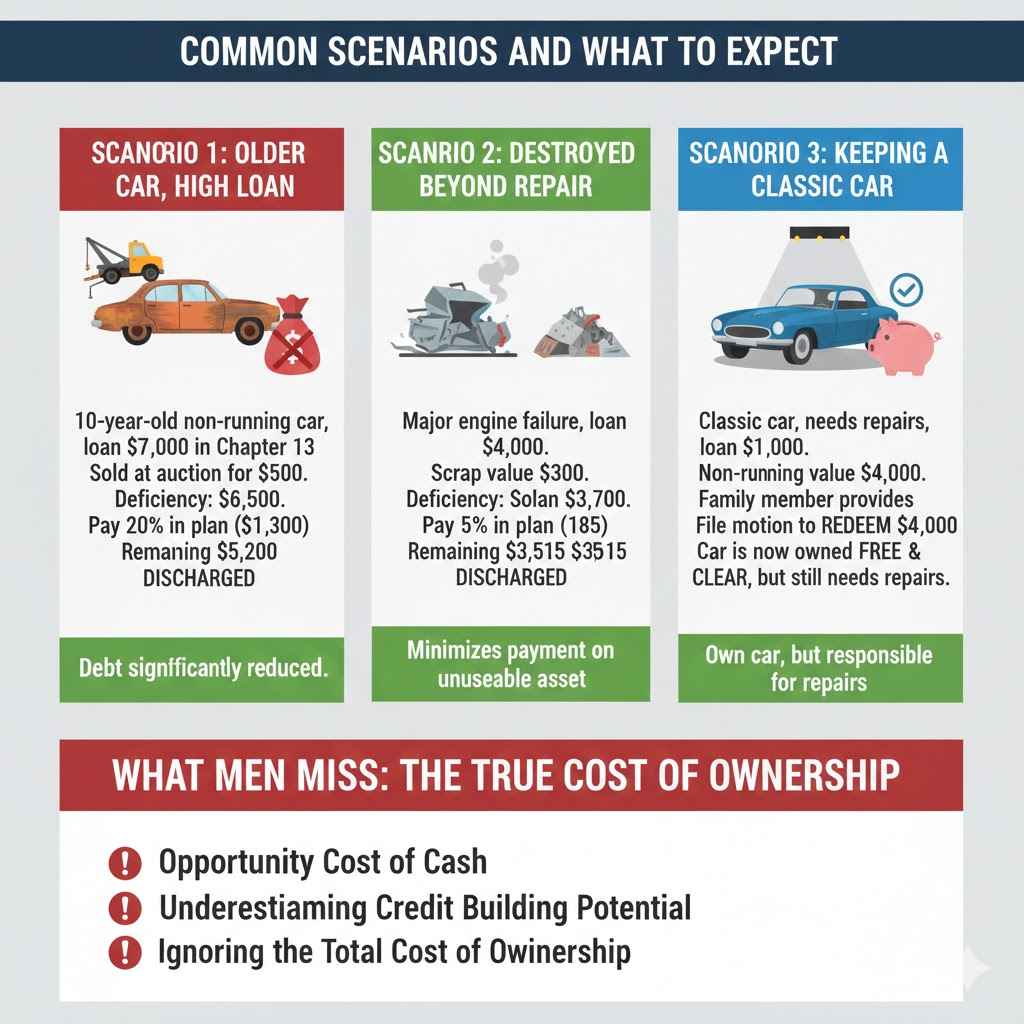

Common Scenarios and What To Expect

Understanding how these situations play out in real life can make the process much clearer. Here are a few examples of what might happen when you surrender a non-running car in Chapter 13. These scenarios highlight the importance of communication and following the correct procedures.

Scenario 1 The Car is Older with High Loan Balance

Imagine you have a ten-year-old car that hasn’t been running for six months. You still owe $7,000 on the car loan. You decide to surrender the car in your Chapter 13 bankruptcy. The lender repossesses it and sells it at auction for $500.

This creates a deficiency balance of $6,500 ($7,000 – $500). In your Chapter 13 plan, you are paying unsecured creditors 20% of what they are owed. Your bankruptcy attorney informs the trustee and the lender. Over your 5-year plan, you will pay $1,300 towards this deficiency ($6,500 * 20%). At the end of your plan, the remaining $5,200 is discharged.

Scenario 2 The Car is Collapsed Beyond Repair

You have a car that has suffered a major engine failure, making it completely irreparable without costing more than a new car. The loan balance is $4,000, and you estimate its scrap value is around $300. You file for Chapter 13 and decide to surrender it.

The lender repossesses and sells it for $300, resulting in a $3,700 deficiency. Your Chapter 13 plan is a “means test” plan, meaning you pay unsecured creditors the minimum possible, perhaps 5%. Over the plan, you pay $185 towards the deficiency ($3,700 * 5%). The rest is discharged.

Scenario 3 Keeping a Non-Running Classic Car

Consider a situation where you have a classic car that you want to keep, even though it needs extensive repairs and is not currently running. The loan balance is $10,000, and its current non-running value is $4,000. You manage to secure a $4,000 lump sum from a family member to redeem the car.

You file a motion with the bankruptcy court to redeem the car for its current value of $4,000. The court approves the motion. You pay the $4,000 lump sum to the lender. You now own the car free and clear of the loan, but you still have the responsibility and cost of repairing it. This option is only feasible if you can access the funds for redemption.

Frequently Asked Questions

Question: Do I have to list a non-running car in my Chapter 13 filing?

Answer: Yes, absolutely. You must list all your assets and debts in your Chapter 13 bankruptcy petition, including any vehicles, even if they are not running. Failing to list an asset can have serious consequences.

Question: Can the lender still repossess my non-running car if I list it for surrender?

Answer: Once you officially list the car for surrender and the lender is notified and agrees, they will proceed with repossession. The bankruptcy court’s approval and the trustee’s oversight ensure this process is handled correctly and according to bankruptcy law.

Question: What happens if the car sells for more than I owe?

Answer: If, by some chance, the car sells for more than you owe on the loan, the excess money usually goes back into your bankruptcy estate. Your Chapter 13 trustee will then distribute this surplus according to your plan, potentially to other creditors.

Question: Will surrendering a non-running car hurt my credit score?

Answer: Surrendering a car is a voluntary repossession, which will negatively impact your credit score. However, Chapter 13 bankruptcy itself already has a significant impact on your credit. The goal of bankruptcy is to help you achieve financial fresh start.

Question: Can I sell a non-running car myself before surrendering it in Chapter 13?

Answer: You generally cannot sell assets in a Chapter 13 case without court permission. If you wish to sell the car, you must file a motion with the bankruptcy court requesting permission to do so. Your attorney will guide you through this process.

Final Thoughts

When you surrender a non-running car in Chapter 13, the lender repossesses and sells it. The resulting debt difference, or deficiency, becomes an unsecured debt. This deficiency is then typically managed and potentially discharged through your Chapter 13 repayment plan. This ensures you can move forward without the burden of a non-functional vehicle and its associated loan.