Can I Lose House? Essential Legal Guide

Can I Lose My House Due to an At-Fault Car Accident? A Simplified Legal Guide for Car Owners.

The short answer is yes, you potentially could face losing your house due to an at-fault car accident, but it’s not a common or easy outcome for most people. Understanding your insurance coverage and legal options is key to protecting your home.

Car troubles can be stressful enough. The last thing anyone wants to worry about is whether a mistake on the road could put their home at risk. It’s a scary thought, isn’t it? Many people wonder, “If I cause an accident, can my house be taken away from me?” This guide is here to break down the legal side of things in a way that’s easy to understand. We’ll walk through how car accidents and your home ownership connect, what protections you likely have, and what steps you can take to keep your house safe.

Understanding Your Liability After an At-Fault Accident

When you’re found to be at fault for a car accident, you’re legally responsible for the damages and injuries caused. This is called “liability.” Your liability isn’t just limited to what happens at the scene of the accident; it can extend to the financial costs of repairs, medical bills, lost wages, pain and suffering, and more. The severity of the accident plays a huge role here. A minor fender-bender is very different from a serious crash with significant injuries.

The legal system aims to compensate those who were harmed. If the costs from an accident you caused are substantial, creditors or injured parties may try to recover their losses from your assets. Your home is often considered one of the most valuable assets you own. This is where the worry about losing your house can come from. But don’t panic just yet; there are several layers of protection in place, primarily through car insurance.

The Crucial Role of Car Insurance

Car insurance is your first and most important line of defense against overwhelming financial consequences from an accident. It’s designed specifically to cover the costs of damages and injuries you might cause to others when you’re at fault. Think of it as a shield protecting your personal assets, like your home.

There are different types of coverage that are relevant here:

- Bodily Injury Liability Coverage: This pays for medical expenses, lost wages, and pain and suffering of other people if you cause an accident that injures them.

- Property Damage Liability Coverage: This covers the cost of repairing or replacing property that you damage in an accident, such as other vehicles, fences, or buildings.

In most places, carrying a minimum amount of liability insurance is legally required by the state. This is often referred to as “state minimums.” However, these minimums can be quite low and might not cover the full cost of a serious accident. If the damages exceed your insurance policy limits, the injured party could potentially pursue your other assets.

Why State Minimums Might Not Be Enough

State minimum liability coverage is a basic level of protection solely to meet legal requirements. Let’s look at a table to illustrate how quickly costs can add up compared to minimum coverage:

| Type of Damage | Potential Cost | Example State Minimum Coverage (Varies by state) | Risk if Coverage is Exceeded |

|---|---|---|---|

| Medical Bills for One Seriously Injured Person | $50,000 – $100,000+ | $25,000 (Bodily Injury per person) | Could pursue other assets, including your home. |

| Multiple Injuries and Property Damage | $150,000 – $300,000+ | $50,000 (Bodily Injury per accident, $25,000 Property Damage) | Significant risk of asset seizure. |

| Catastrophic Injury/Multiple Fatalities | $500,000 – $1,000,000+ | (State minimums are rarely sufficient) | Very high likelihood of lawsuits and asset pursuit. |

As you can see, even a moderately serious accident can quickly surpass the state minimums. This is why many insurance experts and legal professionals advise carrying higher levels of liability coverage than what is legally required.

Umbrella Insurance: An Extra Layer of Protection

For car owners who want enhanced protection beyond their standard auto policy, an umbrella insurance policy is a smart option. This type of insurance provides additional liability coverage that kicks in after the limits of your auto or homeowner’s insurance policies have been exhausted. It’s called “umbrella” because it sits over your other policies, extending your coverage like a protective umbrella.

An umbrella policy typically starts with $1 million in coverage and can go much higher. It’s generally quite affordable for the significant peace of mind it offers. For many, especially those with substantial assets, it’s an essential investment to safeguard their home.

When Can Someone Go After Your Home?

If the damages from an accident you caused significantly exceed your insurance coverage, the injured party (or their insurance company, if they have to pay out a claim for you) can pursue legal action to recover their losses. This process usually involves filing a lawsuit.

If the lawsuit is successful and a judgment is entered against you for an amount more than your insurance covers, the creditor may seek to collect this judgment from your assets. This could involve:

- Wage Garnishment: A portion of your paycheck is directly sent to the creditor.

- Bank Levy: Funds from your bank accounts can be seized.

- Property Liens: A lien can be placed on your home. This means you cannot sell or refinance your house without paying off the lien first.

- Forced Sale of Assets: In some extreme cases, a court could order the sale of your assets, including your home, to satisfy the debt.

This is the scenario where you could, in theory, lose your house. However, legal systems and specific state laws often have protections in place to prevent individuals from being left completely homeless.

State Homestead Exemptions: Protecting Your Primary Residence

Most states have laws known as “homestead exemptions.” These laws protect a certain amount of equity in your primary residence from being seized by creditors to satisfy debts. Your primary residence is defined as the home where you live most of the time.

The amount of equity protected varies greatly by state. Some states offer very generous exemptions, protecting tens or even hundreds of thousands of dollars, while others offer more limited protection. It’s crucial to understand the homestead exemption laws in your specific state.

For example, some states have unlimited homestead exemptions, making it nearly impossible to lose your home to satisfy unsecured debts or judgments from an accident if your equity is below a certain (or no) threshold. Others have dollar limits. If the debt owed is larger than your homestead exemption, the remaining amount could still be at risk.

You can find information on your state’s homestead exemption by searching online for “[Your State Name] homestead exemption laws.” Look for resources from official government websites, such as state legislature sites or judicial branch pages.

Understanding Equity

Equity is the difference between the market value of your home and the amount you still owe on your mortgage. For example, if your home is worth $300,000 and you owe $100,000 on your mortgage, you have $200,000 in equity.

Equity = Home’s Current Market Value – Outstanding Mortgage Balance

If your home’s equity is less than the amount of the judgment against you and also less than your state’s homestead exemption, your home is likely protected. If your equity exceeds the homestead exemption, the amount of equity above the exemption limit could potentially be targeted by creditors.

Procedures and Legal Processes Involved

Losing your house isn’t a simple or quick process. If a creditor seeks to seize your home, they must typically go through a legal process:

- Obtain a Judgment: The creditor must first win a lawsuit against you and get a court order (a judgment) stating that you owe them a specific amount of money.

- Collection Efforts: With a judgment in hand, the creditor can then ask the court for permission to collect on that debt.

- Filing a Lien: They might file a judgment lien against your property. This is a public record that attaches your debt to your home.

- Foreclosure Proceedings: If the debt remains unpaid and the lien is in place, the creditor may initiate foreclosure proceedings, which is the legal process by which a lender or creditor can take possession of your property to satisfy a debt.

Throughout this process, you have legal rights. You would be notified of any lawsuits and have the opportunity to defend yourself in court. Consulting with an attorney is highly recommended if you find yourself in this situation.

Steps to Protect Your Home

The best way to protect your home from potential claims arising from an at-fault car accident is to be proactive. Here are the key steps:

1. Secure Adequate Car Insurance Coverage

This is the most critical step. Review your current auto insurance policy and consider increasing your liability limits. While state minimums are the legal floor, they are often insufficient for serious accidents. Aim for coverage that provides a comfortable buffer above the minimums, such as $100,000/$300,000 bodily injury liability and $100,000 property damage liability, or even higher.

Many insurance agents can help you find a policy that balances strong coverage with affordability. Don’t be afraid to shop around and get quotes from different insurance companies.

2. Consider an Umbrella Policy

If you have significant assets, own a home, or simply want maximum protection, an umbrella policy is an excellent investment. It provides an additional layer of liability coverage for a relatively low cost. It’s a small price to pay for security against devastating financial loss that could jeopardize your home.

3. Understand Your State’s Laws

Familiarize yourself with your state’s specific insurance requirements, homestead exemption laws, and any other asset protection statutes. Knowing your rights and the protections available can empower you to make better decisions.

4. Maintain Your Vehicle and Drive Safely

While this might seem obvious, reducing the likelihood of accidents in the first place is the ultimate form of protection. Regular maintenance ensures your car is safe to operate, and defensive driving practices minimize risks. The fewer accidents you are involved in, the lower your risk of liability.

5. Consult a Legal Professional

If you are ever involved in a serious accident or are concerned about potential legal ramifications, seeking advice from a qualified attorney is wise. An attorney specializing in personal injury or debt collection can explain your specific situation and options.

Common Misconceptions About Losing Your Home

There are several myths surrounding losing your home due to a car accident. Let’s clear a few up:

-

Myth: Any car accident will automatically put my house at risk.

Reality: This is rarely true, especially with adequate insurance. Most accidents are covered by insurance, and home equity protections like homestead exemptions make it very difficult to seize a primary residence.

-

Myth: If I don’t have insurance, they can take my house immediately.

Reality: Driving without insurance is illegal and exposes you to significant personal liability. However, even then, a creditor must go through full legal proceedings to obtain a judgment and attempt to seize assets. It’s not an automatic process, but the risk is extremely high.

-

Myth: My homeowner’s insurance will cover car accident damages.

Reality: Homeowner’s insurance generally does not cover damages arising from operating a vehicle. That’s the role of auto insurance and potentially umbrella insurance.

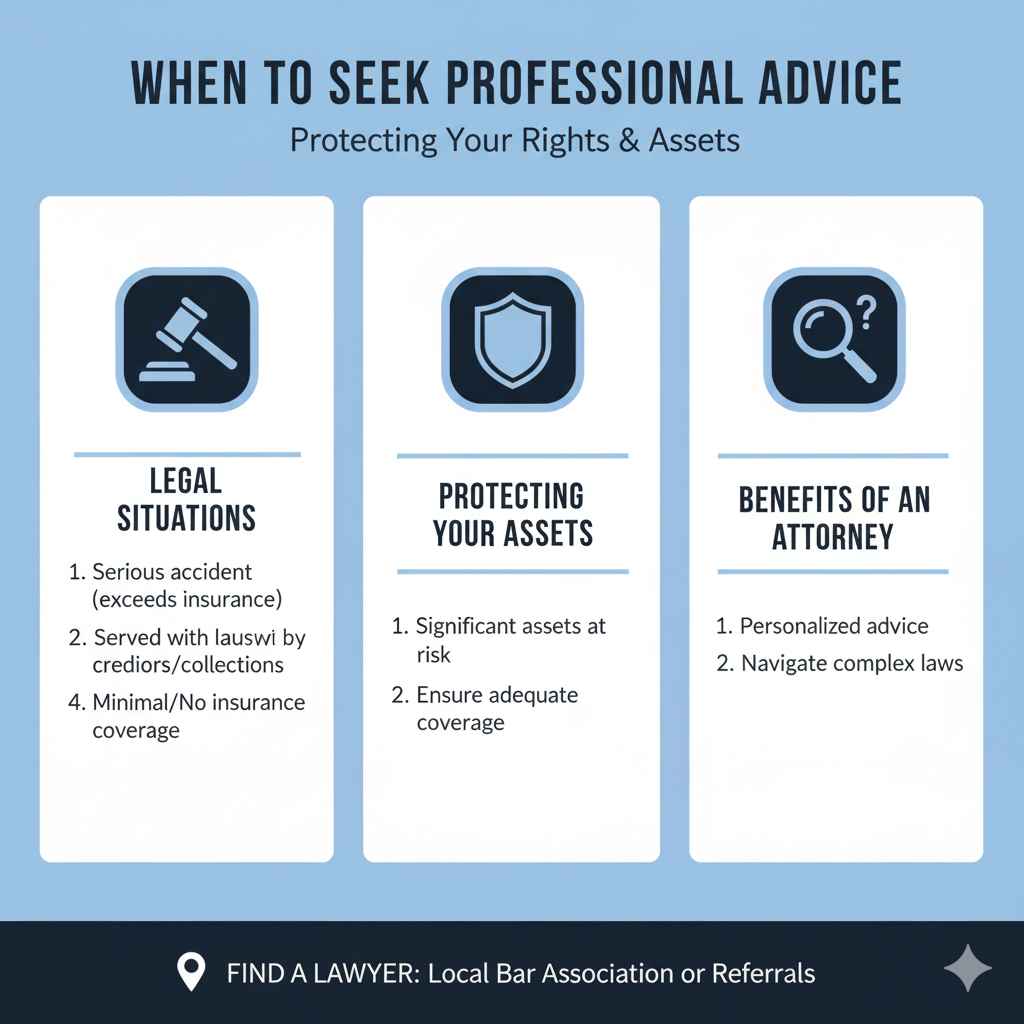

When to Seek Professional Advice

You should strongly consider consulting with an attorney if:

- You were involved in a serious accident where injuries or damages could potentially exceed your insurance limits.

- You have been served with a lawsuit related to a car accident.

- You are being contacted by creditors or collection agencies regarding an accident debt.

- You have minimal or no car insurance coverage.

- You have significant assets and want to ensure they are protected.

An attorney can offer personalized advice and help you navigate complex legal situations. You can find legal professionals through your local bar association or by asking for referrals from trusted sources.

Frequently Asked Questions (FAQs)

Q1: What is the main way an at-fault car accident could lead to losing my house?

A1: If the damages from an accident you caused are much higher than your car insurance coverage, the injured party could sue you. If they win a judgment, they might try to collect it by forcing the sale of your assets, including your home, after all other attempts fail.

Q2: How important is it to have more than the state minimum car insurance?

A2: It’s very important. State minimums are often too low to cover significant medical bills or property damage. Higher liability limits provide a crucial financial safety net that helps protect your personal assets like your house.

Q3: What is an umbrella policy, and do I need one?

A3: An umbrella policy provides extra liability coverage above your standard auto and homeowner’s policies. You might consider one if you have substantial assets, own a home, or want an extra layer of protection against very large claims.

Q4: Will my home be protected even if I owe a lot of money after an accident?

A4: Your home may be protected to some extent by your state’s homestead exemption laws, which shield a certain amount of your home’s equity from creditors. However, if your equity exceeds the exemption amount, the excess could be at risk.

Q5: What is the legal process someone goes through to take my house?

A5: They must first win a lawsuit and obtain a court judgment against you. Then, they can ask the court to allow them to place a lien on your property or force its sale to satisfy the debt. This is a lengthy legal process.

Q6: What’s the best first step to take to protect my home?

A6: The best first step is to ensure you have adequate car insurance with high enough liability limits to reasonably cover potential damages from an accident. Consider adding an umbrella policy for extra security.

Conclusion

Worrying about losing your house due to a car accident can be a significant stressor, but understanding the legal landscape and your insurance protections can bring immense relief. While it’s technically possible for your house to be at risk if you cause a severe accident and your insurance coverage is insufficient, it’s a scenario that is often mitigated by robust insurance policies and state-specific asset protection laws like homestead exemptions.

Your primary defense is carrying sufficient car insurance, including high liability limits and potentially an umbrella policy. By being proactive, staying informed about legal protections, and driving safely, you can significantly reduce the risk and gain the confidence that your home is well-protected. Remember, taking action with your insurance is the most powerful step you can take to safeguard your most valuable asset.