Can I Sell My Car With Open Claim? Essential Guide

Yes, you can generally sell your car with an open insurance claim, but it can be complicated. Transparency is key. You must inform potential buyers about the open claim and its details. The claim might affect the sale price and the process, so understanding your options and being upfront is crucial for a smooth transaction.

Selling your car can feel like a big task, especially when life throws a curveball like an open insurance claim. Maybe you were in a recent accident, or perhaps there’s a pending claim from a past event. Whatever the reason, the question pops up: “Can I sell my car while this claim is still being processed?” It’s a common concern, and one that can leave you feeling a bit stuck. You want to move on, get rid of the car, and maybe get some cash, but the unresolved claim adds a layer of uncertainty.

Don’t worry, though! This guide is here to break down exactly what you need to know, step-by-step, so you can handle this situation with confidence. We’ll explore your options, explain the potential hurdles, and show you how to navigate the process smoothly.

Understanding Open Insurance Claims and Car Sales

An “open insurance claim” simply means that you’ve reported an incident to your insurance company, and they are in the process of investigating, assessing damages, and potentially issuing a settlement. This could involve anything from a fender-bender to a more significant collision or even theft (though selling a stolen car is a whole different, illegal matter!).

When you decide to sell your car with an open claim, you’re essentially selling a vehicle that has an unresolved financial or legal issue tied to it. This doesn’t automatically make the sale impossible, but it does add some important considerations for both you as the seller and the potential buyer.

Why Transparency is Your Best Friend

The most crucial aspect of selling a car with an open claim is honesty. Trying to hide the fact that there’s an ongoing claim can lead to serious legal trouble and a ruined reputation. Buyers have a right to know the full history of the vehicle they are purchasing. Full disclosure protects you from potential future disputes and ensures a more ethical transaction. Think of it this way: would you want to buy a car without knowing if there was a pending insurance payout or responsibility for damages?

Being upfront about the open claim allows buyers to make an informed decision. They can then decide if they are comfortable proceeding, understand any potential future implications, and negotiate the price accordingly. A transparent seller builds trust, which is invaluable in any sale.

Can You Legally Sell Your Car With an Open Claim?

In most places, the direct answer is yes, you can legally sell your car with an open insurance claim. There isn’t a universal law that forbids the sale of a vehicle simply because an insurance claim is pending. However, the laws and regulations surrounding vehicle sales, especially concerning disclosure, vary by state or country.

The critical factor is disclosure. You are generally obligated to disclose any known material defects or issues that could affect the vehicle’s value or safety. An open insurance claim, especially one related to an accident or significant damage, typically falls into this category.

What Does “Open Claim” Mean for Your Car’s Title?

An open claim itself doesn’t usually affect your car’s title directly. The title is a legal document that proves ownership. However, the outcome of the open claim might: if the claim results in the car being declared a “total loss” by the insurance company, then the title will be branded accordingly (e.g., “salvage” or “rebuilt,” depending on the jurisdiction and subsequent repairs). Selling a car with a branded title has its own set of rules and limitations.

If the claim is for damages that are being repaired, or if liability is still being determined, the title may remain clean. It’s important to understand the status of your claim and how it might impact your vehicle’s paperwork.

Navigating the Sale: Step-by-Step Guide

Selling your car with an open claim requires a bit more diligence than a standard sale. Here’s how to approach it:

Step 1: Understand Your Insurance Claim Status

Before you even think about listing your car, get a clear picture of your insurance claim. Contact your insurance adjuster or review your claim documents. You need to know:

- What is the nature of the claim? (Accident, vandalism, theft recovery, etc.)

- What is the estimated or agreed-upon damage amount?

- Is the car currently drivable?

- What is the insurance company’s assessment of the vehicle’s value (Actual Cash Value – ACV)?

- What is the projected timeline for the claim to be resolved?

- Will the settlement amount be paid directly to you, or to a repair shop?

This information is crucial for transparency and pricing negotiations.

Step 2: Assess Your Car’s Current Condition and Value

Be realistic about your car’s condition. The open claim likely implies some form of damage or incident. Document any visible damage, even if it’s minor. Take clear photos and videos of the car’s current state.

Research your car’s market value. Use resources like Kelley Blue Book (Kelley Blue Book) or Edmunds (Edmunds) to get an estimate. Factor in the open claim and any unrepaired damage, as this will likely reduce the car’s value. Be prepared for buyers to offer less than market value due to the unresolved claim.

Step 3: Inform Potential Buyers (The Disclosure Step)

This is non-negotiable. When you advertise your car or when a potential buyer shows interest, you must disclose the open insurance claim. Be specific:

- State clearly that there is an open insurance claim.

- Explain the reason for the claim (e.g., “involved in a minor accident on [date]”).

- Provide details on the extent of the damage and whether repairs have been made or are planned.

- Mention if the claim has impacted the vehicle’s title (if applicable).

- Most importantly, be honest and transparent.

You can include this information in your online listing description and verbally reiterate it during conversations and viewings. A sample disclosure statement could be: “This vehicle has an open insurance claim due to an incident on [Date]. The current estimated repair cost is [Amount], and the insurance company is still processing the claim. The car is currently [drivable/not drivable] and has [describe visible damage].”

Step 4: Determine Your Selling Strategy

You have a few options depending on your situation and comfort level:

Option A: Sell As-Is, With the Claim Open

This is the most straightforward approach if you need to sell quickly. You sell the car in its current condition, and the buyer takes on the responsibility of dealing with the open claim or its aftermath. This will likely result in a lower sale price.

Option B: Settle the Claim Before Selling

If the claim is for damages and the insurance company has approved a repair amount or a payout for the damages, you could use that settlement to make the repairs before listing the car. Alternatively, if the car is declared a total loss, you’ll receive the Actual Cash Value (ACV) from the insurance company, and they will typically take possession of the vehicle. If you wish to keep the car despite it being declared a “total loss,” you can negotiate to “buy it back” from the insurance company, often for its salvage value. This will result in a salvage title. This process can be complex and might not be worth it if the ACV is low.

Option C: Sell to a Dealership or Wholesaler

Many dealerships and car buying services are equipped to handle vehicles with open claims. They have the resources and expertise to navigate the complexities. However, expect a lower offer compared to selling privately, as they need to factor in their own processing costs and risks. You’ll still need to be transparent about the open claim.

Step 5: Pricing Your Car

As mentioned, an open claim will reduce your car’s market value. Buyers will be wary of potential hidden issues, repair costs, or the hassle of dealing with the claim themselves. Research comparable vehicles (similar make, model, year, mileage) and then adjust your price downwards significantly to account for the open claim and any unrepaired damage.

Consider these factors for pricing:

- The severity of the incident.

- The cost of repairs.

- The title status (clean vs. branded).

- The buyer’s potential burden.

Step 6: The Paperwork and Sale Process

Once you find a buyer:

- Bill of Sale: Create a detailed bill of sale. This document should include the date, buyer’s and seller’s names and addresses, vehicle information (VIN, make, model, year), the agreed-upon sale price, and a clear statement of the vehicle being sold “as-is.” Crucially, include a clause stating that you have disclosed the open insurance claim and its details. Both parties must sign it.

- Title Transfer: You’ll need to transfer the car’s title to the buyer. Ensure your name is on the title as the owner. If there’s a lien on the car, you’ll need to pay it off before you can transfer the title. Check with your local Department of Motor Vehicles (DMV) or equivalent agency for specific title transfer procedures in your area. You can find information on the DMV.org website, which provides helpful state-specific guides.

- Payment: Arrange for secure payment. Avoid personal checks if possible, or wait for them to clear before signing over the title. Cash, cashier’s checks, or secure money transfers are generally preferred.

- Notify Your Insurance Company: Once the sale is complete and the title is transferred, inform your insurance company that you no longer own the vehicle. This will allow you to cancel your insurance policy for that car and avoid any further liability.

Potential Complications and How to Handle Them

Selling a car with an open claim isn’t always straightforward. Here are some common hurdles:

1. Buyer Hesitation

Many buyers will be turned off by the idea of an open claim. They might worry about:

- The extent of hidden damage.

- Their own potential involvement or liability if the claim has broader implications.

- The hassle of dealing with the insurance company or repair process.

- A reduced resale value down the line.

Solution: Be prepared to answer all questions honestly and patiently. Provide any documentation you have regarding the claim. If possible, have an independent mechanic inspect the car to provide a third-party assessment of its condition. Emphasize that you are disclosing everything.

2. Lower Sale Price

Expect to get less money for your car. The open claim is a significant risk factor for any buyer, and they will want compensation for that risk. Market value guides are a starting point, but your actual selling price will reflect the claim’s impact.

Solution: Research the market thoroughly to understand how much similar cars in similar condition sell for. Be realistic about the impact of the claim. If you need to sell quickly, be prepared to accept a lower, but fair, offer.

3. Title Branded as “Salvage” or “Rebuilt”

If the insurance company declares your car a total loss, it will likely receive a “salvage” title. If it’s repaired and inspected, it might get a “rebuilt” title. Selling a car with a branded title is possible but comes with significant challenges and depreciation.

Solution: If the car is branded, you must disclose this. Buyers interested in salvage or rebuilt vehicles are often mechanics or hobbyists looking for projects. You might need to sell to a specialized salvage yard or a buyer comfortable with such titles. A very clear Bill of Sale, detailing the title status, is essential.

4. Outstanding Liens

If you have a loan on the car, the lender (lienholder) has an interest in the vehicle. You cannot sell the car freely if there’s an outstanding loan. The insurance settlement, especially for a total loss, might go directly to the lender first.

Solution: Contact your lender. Understand the payoff amount. If you sell the car privately, the buyer’s payment typically needs to cover the loan balance. You’ll need to coordinate with the lender to release the title after the loan is paid in full. If the car is totaled, the insurance company will usually pay the lienholder directly up to the amount owed. You would then receive any remaining ACV as the owner.

Selling to Different Buyers

Your approach might change slightly depending on who you’re selling to:

Selling to a Private Party

This often yields the highest price but requires the most effort and transparency. You are directly responsible for disclosing all information about the open claim. Buyers might be more hesitant and require more reassurance or inspections.

Selling to a Dealership

Dealerships are professionals. They are accustomed to dealing with various car conditions, including those with open claims. However, they will offer you a wholesale price, which is significantly lower than retail, to cover their potential costs and profit margin. Be upfront about the open claim; they will likely discover it during their own assessment or title search anyway.

Selling to a Car Buying Service (e.g., Carvana, Vroom)

Similar to dealerships, these services offer convenience. You’ll typically start with an online quote. During their inspection, you must disclose the open claim. Their offer might be adjusted based on the claim and the car’s condition. They handle much of the paperwork, but transparency is still key.

Selling for Parts or Scrap

If the car is heavily damaged and the claim implies significant issues, selling it for parts or to a scrap yard might be an option. In this case, the open claim might be less of a concern for the buyer, as they are purchasing based on weight or individual component value. However, you still need to inform your insurance company and complete the title transfer correctly.

Important Considerations: Title Brands and Total Loss

The terms “salvage title” and “total loss” are often related to open insurance claims and are critical for any seller to understand.

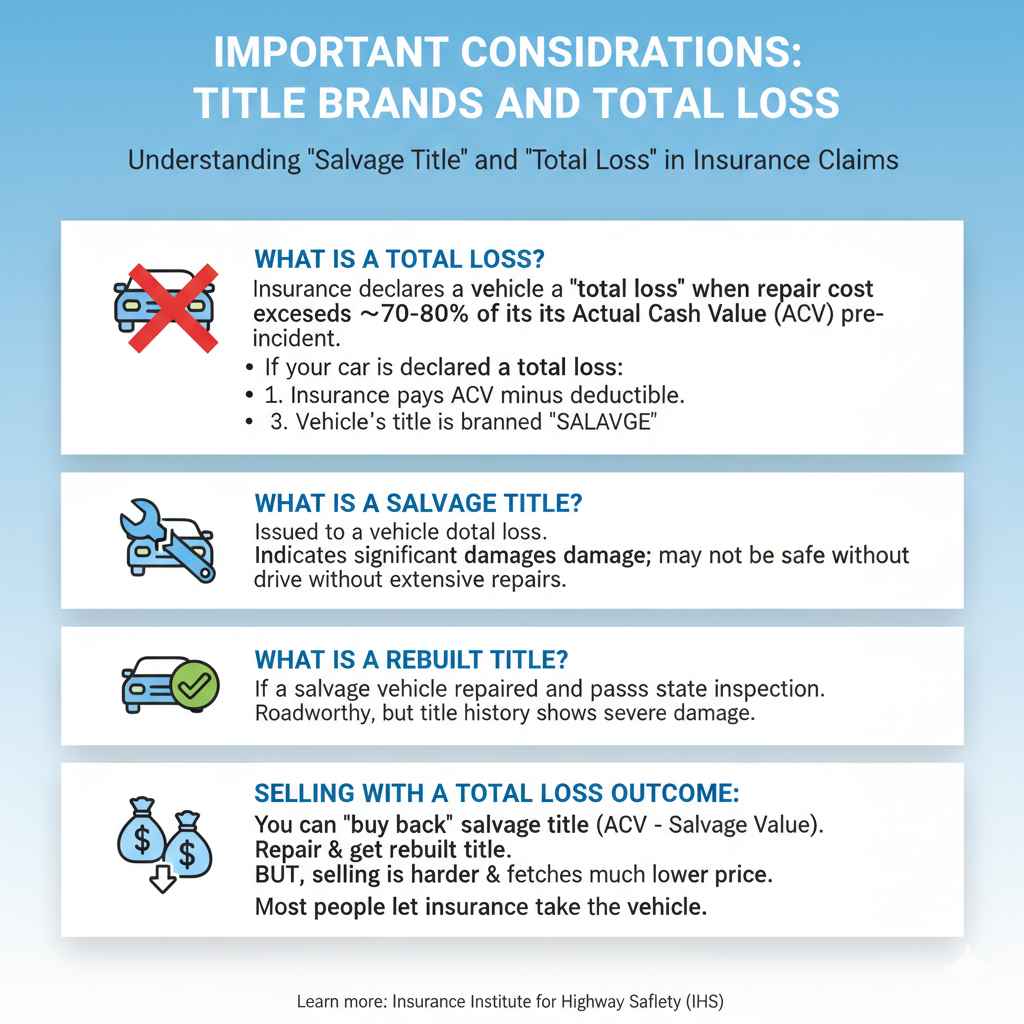

What is a Total Loss?

An insurance company declares a vehicle a “total loss” when the cost to repair the damage exceeds a certain percentage of the vehicle’s Actual Cash Value (ACV) before the incident. This percentage varies by state, but it’s often around 70-80%.

If your car is declared a total loss:

- The insurance company will pay you the ACV of the vehicle, minus your deductible.

- They will then typically take ownership of the damaged vehicle.

- The vehicle’s title will be branded as “salvage.”

What is a Salvage Title?

A salvage title is issued to a vehicle that has been declared a total loss by an insurance company. It indicates that the car has sustained significant damage and may not be safe to drive without extensive repairs.

What is a Rebuilt Title?

If a salvage vehicle is repaired and passes a state inspection, it can be issued a “rebuilt” title. This means it’s roadworthy again, but the title still carries a history of severe damage.

Selling with a total loss outcome: If your car is declared a total loss and you want to keep it, you can negotiate with the insurance company to “buy back” the salvage title. This means you’ll receive the ACV minus the salvage value. While you can then repair it and potentially get a rebuilt title, selling a car with a branded title is significantly harder and fetches a much lower price. Most people choose to let the insurance company take the total loss vehicle. You can learn more about salvage titles from resources like the Insurance Institute for Highway Safety (IIHS).

Frequently Asked Questions (FAQ)

| Question | Answer |

|---|---|

| Do I have to tell a buyer about an open claim? | Yes, absolutely. Honesty and transparency are legally and ethically required. You must disclose any known issues that could affect the vehicle’s value or safety, and an open claim typically falls into that category. |

| Will an open claim stop me from selling my car? | No, it generally won’t stop you from selling your car. However, it will likely make the sale more complicated and potentially reduce the car’s value and the number of interested buyers. |

| Can I get in trouble for not disclosing an open claim? | Yes. If you fail to disclose a known issue like an open claim, you could face legal repercussions from the buyer, especially if they |