Can Someone In A Different State Cosign For A Car: Essential Guide

Yes, it is generally possible for someone in a different state to cosign for a car, but it involves extra steps and careful consideration of state laws and lender requirements. The process requires clear communication, proper documentation, and adherence to specific regulations to ensure a smooth transaction.

Are you looking to buy a car but need a little help with financing? Maybe a trusted friend or family member lives out of state and is willing to be your cosigner. It’s a common question: “Can someone in a different state cosign for a car?” The answer is usually yes, but it’s not as simple as signing a piece of paper next door. This can feel confusing, especially when you’re excited about getting a new ride!

Don’t worry, I’m here to help you navigate this. We’ll break down exactly what’s involved, from understanding the rules to making sure everything is done correctly. By the end of this guide, you’ll know all the essential steps and considerations to make this work smoothly for everyone involved. Let’s get your car buying journey rolling!

Understanding the Role of a Cosigner

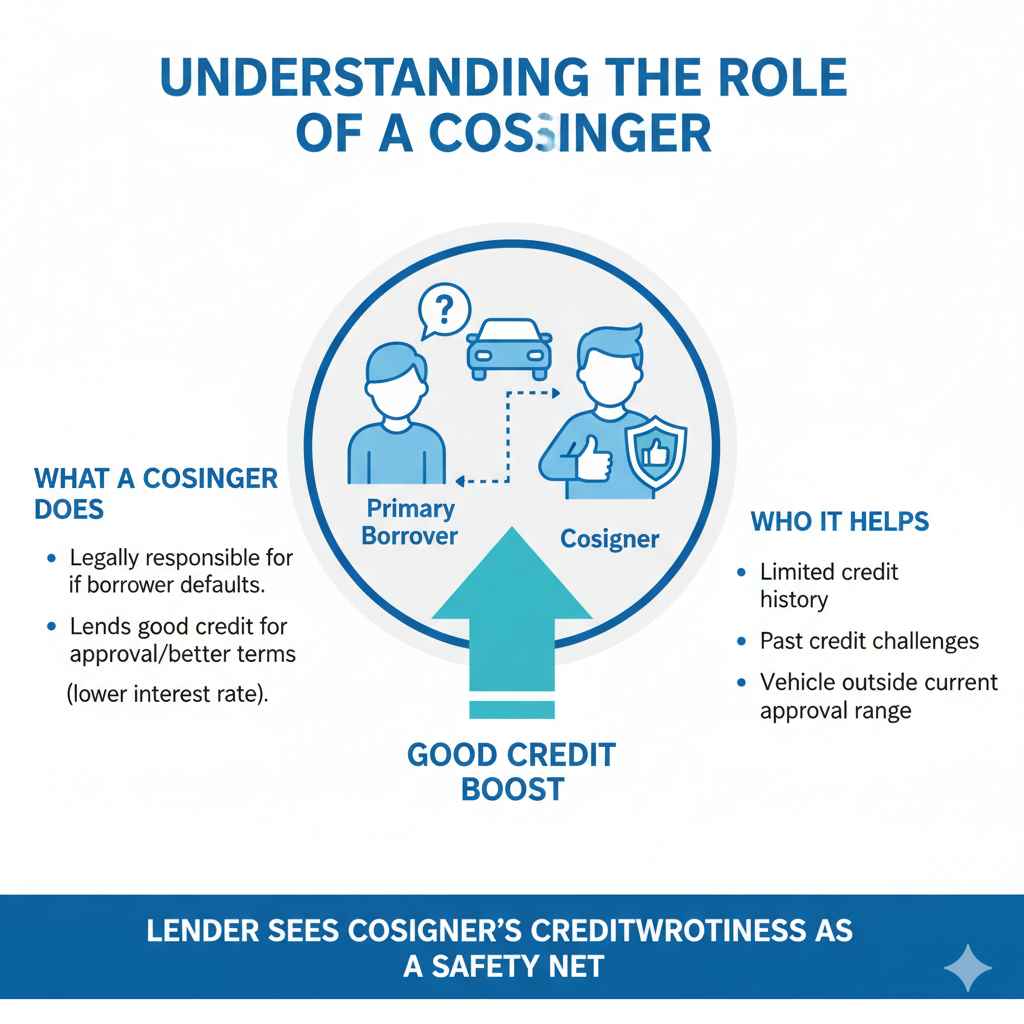

Before we dive into the out-of-state specifics, let’s quickly revisit what a cosigner does. A cosigner, also known as a guarantor, agrees to be legally responsible for a loan if the primary borrower doesn’t pay. They essentially lend you their good credit to help you get approved for a loan or secure better terms, like a lower interest rate.

This is incredibly helpful if you have a limited credit history, past credit challenges, or if you’re looking for a vehicle that might be just outside your current approval range. The lender sees the cosigner’s creditworthiness as a safety net, which increases the chances of your loan being approved.

Can Someone in a Different State Cosign for a Car? The Basics

The straightforward answer is yes, someone in a different state can cosign for a car. However, this process isn’t standardized across every dealership or lender. The feasibility and specific requirements can vary significantly based on a few key factors: the lending institution’s policies, state-specific laws, and the dealership’s willingness to handle the added complexity.

Think of it like this: a cosigner vouches for your ability to repay the loan. For an auto loan, this means their credit score and financial stability are being used to back your application. When they live in another state, the lender needs to be confident that they can legally enforce the loan agreement if needed. This introduces extra layers of verification and paperwork.

Key Factors Influencing Out-of-State Cosigning

Several elements play a crucial role in determining whether an out-of-state cosigner situation will work:

- Lender Policies: This is the biggest factor. Many national lenders are equipped to handle out-of-state cosigners, as they operate across state lines. Local credit unions or smaller banks might have more restrictions. Always ask the lender directly about their policy.

- State Laws: Each state has its own regulations regarding loans, liens, and finance contracts. While a cosigner agreement is generally valid across state lines, the enforcement and requirements might differ. For example, some states have specific disclosure rules for cosigner agreements.

- Dealership Procedures: Some dealerships are more experienced and willing to facilitate out-of-state cosigning than others. A dealership that primarily works with local buyers or lenders might find the process too cumbersome.

- Vehicle Registration and Insurance: This is a significant logistical hurdle. The car will need to be registered and insured, typically in the state where the car will be primarily used and located. The cosigner’s state of residence might have different requirements that need to be managed.

The Process: Step-by-Step for Out-of-State Cosigning

If you’ve confirmed that an out-of-state cosigner is possible, here’s a general walkthrough of what you can expect. This process requires patience and excellent communication between you, the cosigner, the lender, and the dealership.

Step 1: Find a Lender and Dealership Willing to Accommodate

Your first step is to do your homework. Research auto lenders that are known to work with out-of-state cosigners. National banks, large online lenders, and some credit unions often have established procedures for this. Simultaneously, talk to dealerships about their experience with car loans involving cosigners from different states.

Pre-Approval is Key

It’s highly recommended to get pre-approved for a car loan before you start shopping. This allows you to know your budget and interest rate, and it gives you a chance to confirm the lender’s stance on out-of-state cosigners. You can submit the cosigner’s information during the pre-approval process.

Step 2: Gather Necessary Documentation

Both you and your cosigner will need to provide extensive documentation. This is standard for any loan application, but especially crucial when crossing state lines:

-

For the Primary Borrower (You):

- Proof of income (pay stubs, tax returns)

- Proof of employment (letter from employer, W-2s)

- Proof of residency (utility bills, lease agreement)

- Driver’s license and Social Security card

- Completed loan application

-

For the Cosigner (Out-of-State):

- Proof of income (similar to yours)

- Proof of employment (similar to yours)

- Proof of residency in their state (utility bills, etc.)

- Driver’s license and Social Security card from their state

- A signed consent form verifying they understand their cosigner obligations.

- Potentially, they might need to visit the dealership or a notary public.

The lender will provide an exact list, but expecting the above is a good starting point.

It’s important for your cosigner to understand that their personal information will be thoroughly vetted. Lenders will pull their credit report not just to see their score, but also to assess their debt-to-income ratio and overall financial health.

Step 3: The Application and Credit Check

You will fill out the loan application, listing your cosigner. The lender will then perform a credit check on both you and the cosigner. The cosigner’s credit score and history will be heavily weighted in the decision-making process. This is where the out-of-state aspect can introduce a slight delay, as the lender verifies information across different states.

Step 4: Reviewing and Signing the Loan Documents

Once approved, you’ll receive the loan terms. This is a critical stage. The loan contract will clearly outline the responsibilities of both the primary borrower and the cosigner. For an out-of-state cosigner, there are a few crucial points to address:

- Notarization: It’s highly likely that the cosigner’s signature on the loan agreement will need to be notarized. This verifies their identity and ensures they are signing the document willingly. Your cosigner may need to visit a notary public in their state. Some states may require an attorney-in-fact to sign certain documents on behalf of the cosigner if they cannot be present in person. This can be done via a Power of Attorney, which should be drafted carefully and reviewed by legal counsel.

- Remote Signing: Many lenders today offer remote signing options using secure online platforms. This can simplify the process for an out-of-state cosigner, allowing them to e-sign documents after verifying their identity.

- Vehicle Location: The loan agreement often specifies the location where the vehicle will be primarily used and registered. Ensure this matches your state.

The consumer protection laws of the state where the loan is originated usually govern the loan agreement. However, if the cosigner is in a different state, it can sometimes be complicated to determine which state’s laws apply regarding enforcement of the contract terms. Consult the Consumer Financial Protection Bureau (CFPB) for general information on consumer credit rights and laws.

Step 5: Vehicle Purchase and Delivery

Once all documents are signed and the loan is finalized, you can proceed with purchasing the vehicle. The lender will typically fund the dealership directly. You will then arrange for the vehicle’s registration and insurance in your state.

Registration and Insurance Hurdles

This is where the out-of-state cosigner can present the most significant challenge. The car must be legally registered and insured in the state where you live and will drive it. The cosigner’s name might appear on certain loan documents, but they are not the owner. Your name will be on the title (unless specified otherwise, which is rare and complex), and registration and insurance will be tied to your address.

Some states might require the cosigner to technically be a resident of the state where the car is being purchased and registered, even if they aren’t the primary owner. This is where you might encounter roadblocks. Clear communication with your state’s Department of Motor Vehicles (DMV) is essential.

For example, if your cosigner is in California and you are buying a car in Florida, the Florida DMV will follow Florida registration laws. The lender’s requirements are separate from the DMV’s. Most lenders will allow the car to be registered in the primary borrower’s state, but it’s crucial to confirm this with them.

Challenges and Considerations

Navigating an out-of-state cosigning situation comes with its own set of unique challenges:

1. Increased Complexity and Paperwork

As you’ve seen, the process involves more steps, more documents, and more checks to ensure everything is legal and compliant across state lines. Expect these extra steps to add time to the car-buying process.

2. Notarization and Verification Hassles

Getting signatures notarized can be time-consuming if your cosigner has a busy schedule or lives far from a notary. Proof of identity and residency checks can also take longer when dealing with different state records.

3. Lender and Dealership Willingness

Not all lenders or dealerships are set up to handle the logistics of out-of-state cosigning. You might face more rejections or require more effort to find a willing party.

4. Potential for Conflicting State Laws

While contracts are often governed by the originating state’s laws, there can be complexities if issues arise that touch upon the cosigner’s home state laws. This is rare but possible in legal disputes.

5. Impact on Cosigner’s Credit

It’s vital for the cosigner to understand that this loan will appear on their credit report. If you miss payments, it will negatively affect their credit score. This can impact their ability to get credit for themselves in the future.

Benefits of Using an Out-of-State Cosigner

Despite the challenges, there are compelling reasons why you might pursue this route:

- Access to Financing: This is often the primary benefit. It can be your best, or only, option to get approved for a car loan.

- Better Loan Terms: A strong cosigner can help you qualify for a lower interest rate, saving you a significant amount of money over the life of the loan.

- Access to a Wider Range of Vehicles: With an approved loan, you might be able to afford a newer or different type of vehicle than you could on your own.

- Building Credit History: If you make all your payments on time, having a cosigner can help you establish a positive credit history for yourself.

When Might an Out-of-State Cosigner NOT Work?

There are certain situations where it might be exceptionally difficult or impossible to use an out-of-state cosigner:

- Very Strict Lender Policies: Some lenders have a strict “in-state only” policy for cosigners due to the administrative burden.

- Dealership Reluctance: If the dealership isn’t experienced or willing to navigate the complexities, they might refuse to process the loan.

- Specific Loan Types: Some specialized auto loan programs might have unique requirements.

- Cosigner’s Location in a High-Risk State (for Enforcement): In rare cases, a lender might be hesitant if state laws in the cosigner’s residence present significant hurdles for debt collection.

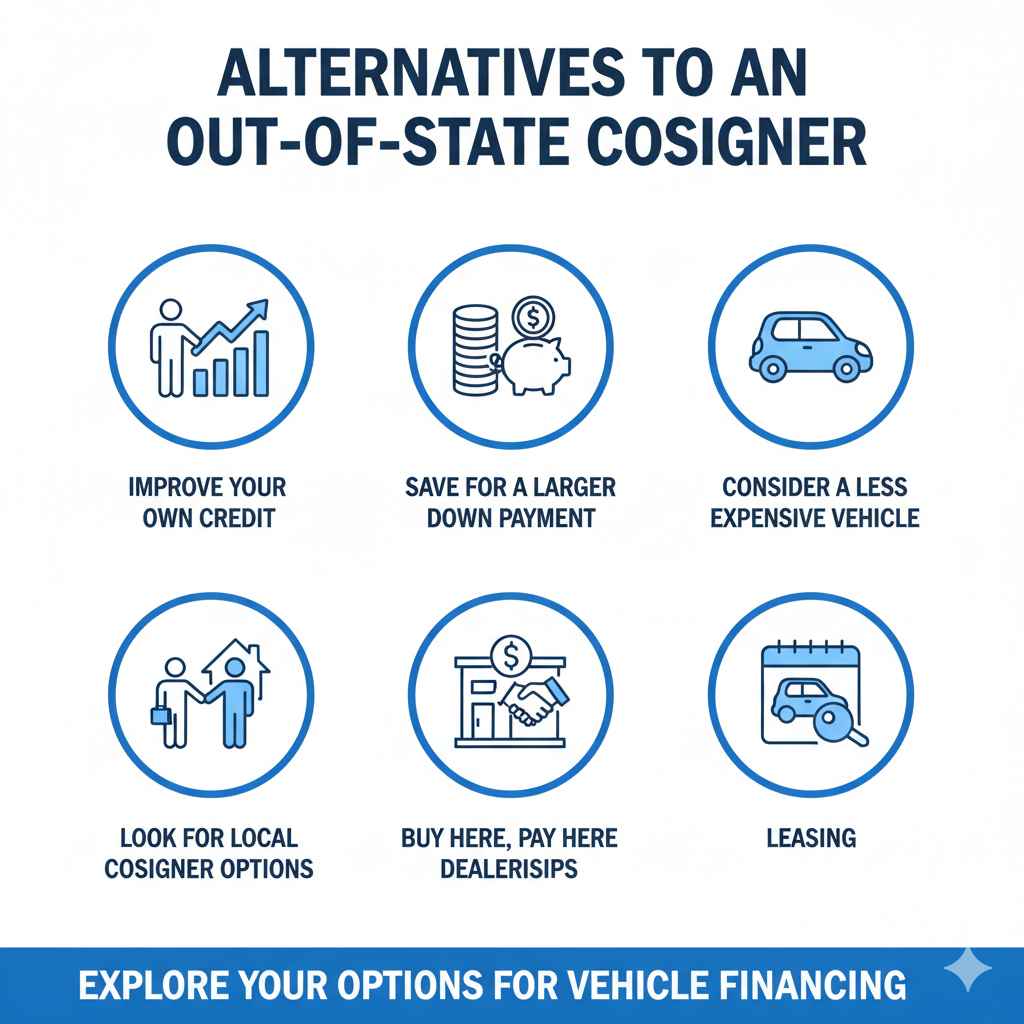

Alternatives to an Out-of-State Cosigner

If the out-of-state cosigner route proves too difficult, don’t despair! Here are some alternatives you can explore:

- Improve Your Own Credit: Focus on building your credit score by paying bills on time, reducing debt, and checking your credit report for errors.

- Save for a Larger Down Payment: A substantial down payment reduces the loan amount, making you a less risky borrower.

- Consider a Less Expensive Vehicle: A lower purchase price means you’ll need less financing, which can be easier to secure.

- Look for Local Cosigner Options: Do you have a friend or family member who lives in your state and has good credit?

- Buy Here, Pay Here Dealerships: These dealerships offer in-house financing, which can be more flexible, though often with higher interest rates.

- Leasing: While not buying, leasing might be an option if your credit is borderline.

Table: Pros and Cons of an Out-of-State Cosigner

Here’s a quick comparison to help you weigh the decision:

| Pros of Out-of-State Cosigner | Cons of Out-of-State Cosigner |

|---|---|

| Access to financing when you might not otherwise qualify. | Increased paperwork and administrative complexity. |

| Potential for lower interest rates and better loan terms. | Lengthier approval and signing process. |

| Allows purchase of a more desirable vehicle. | Not all lenders or dealerships are equipped to handle it. |

| Helps build your own credit history if payments are made on time. | Requires careful coordination and communication across states. |

| Can be a vital stepping stone to vehicle ownership. | Potential for confusion regarding which state laws apply in disputes. |

| Cosigner’s credit is still at risk if you default. |

Frequently Asked Questions (FAQ)

Q1: Will my cosigner have to travel to my state to sign the loan?

Not necessarily. Many lenders offer remote signing options, including e-signatures and secure online portals. However, some might require notarization locally in their state or, in rarer cases, a visit to the dealership. Always confirm the specific process with your lender.

Q2: Can my cosigner in another state be listed on the car’s title?

It is generally not advisable or common for an out-of-state cosigner to be listed on the title. The title usually reflects ownership. A cosigner is a financial guarantor, not an owner. The car will typically be titled in your name, with the loan jointly tied to you and your cosigner.

Q3: What happens if I miss payments and my cosigner is out of state?

The lender will pursue payment from both you and your cosigner. If payments are missed, the lender will report it to the credit bureaus, impacting both your credit scores. The lender can also take legal action to repossess the vehicle and collect the debt, which may involve navigating legal processes in both your state and your cosigner’s state.

Q4: Does the car have to be registered in the cosigner’s state?

No, the car must be registered and insured in the state where the vehicle will be primarily used and reside, which is usually your state. The cosigner’s residency doesn’t dictate the car’s registration if they are not purchasing or residing with the vehicle.

Q5: How long does it typically take for an out-of-state cosigner car loan to be approved?

It can take longer than a standard in-state loan, potentially 2-5 business days or even more, depending on the lender’s process, how quickly documents are submitted, and any additional verification steps required for interstate transactions. Some lenders are faster than others.

Q6: Are there specific states that make out-of-state cosigning harder?

While not a strict rule, states with very consumer-friendly protection laws or complicated lien laws might add layers of complexity. However, most modern lenders are experienced in navigating different state regulations for common transactions like auto loans. The primary challenge is almost always the lender’s specific policy rather than a universally difficult state law.

Conclusion

So, can someone in a different state cosign for a car? The answer is a resounding, yet conditional, yes! While it introduces extra steps like notarization, remote signing, and careful documentation of residency, it’s a perfectly feasible way to secure auto financing. The key lies in thorough research, clear communication with your lender and dealership, and ensuring all parties understand their roles and responsibilities.

By being prepared for the process, gathering all necessary paperwork, and confirming the policies of your chosen finance institution, you can successfully leverage the credit of an out-of-state cosigner.