Can You Be Denied A Car Loan After Pre-Approval? Essential Guide

Yes, you absolutely can be denied a car loan even after receiving pre-approval. Pre-approval is a conditional go-ahead, not a final guarantee. Several factors can change between your pre-approval and the final loan decision, leading to denial. This guide will explain why and what you can do to prevent it.

Getting pre-approved for a car loan feels like a massive step forward, doesn’t it? It’s exciting to know you have a potential budget lined up for your dream car. But what happens if, after all that excitement, you’re told “no” at the dealership? It’s a frustrating situation, and thankfully, more common than you might think. This guide is here to break down exactly why this can happen and what steps you can take to keep your car-buying dream alive. We’ll walk through the process, making it easy to understand, so you can drive away with confidence.

Understanding Car Loan Pre-Approval

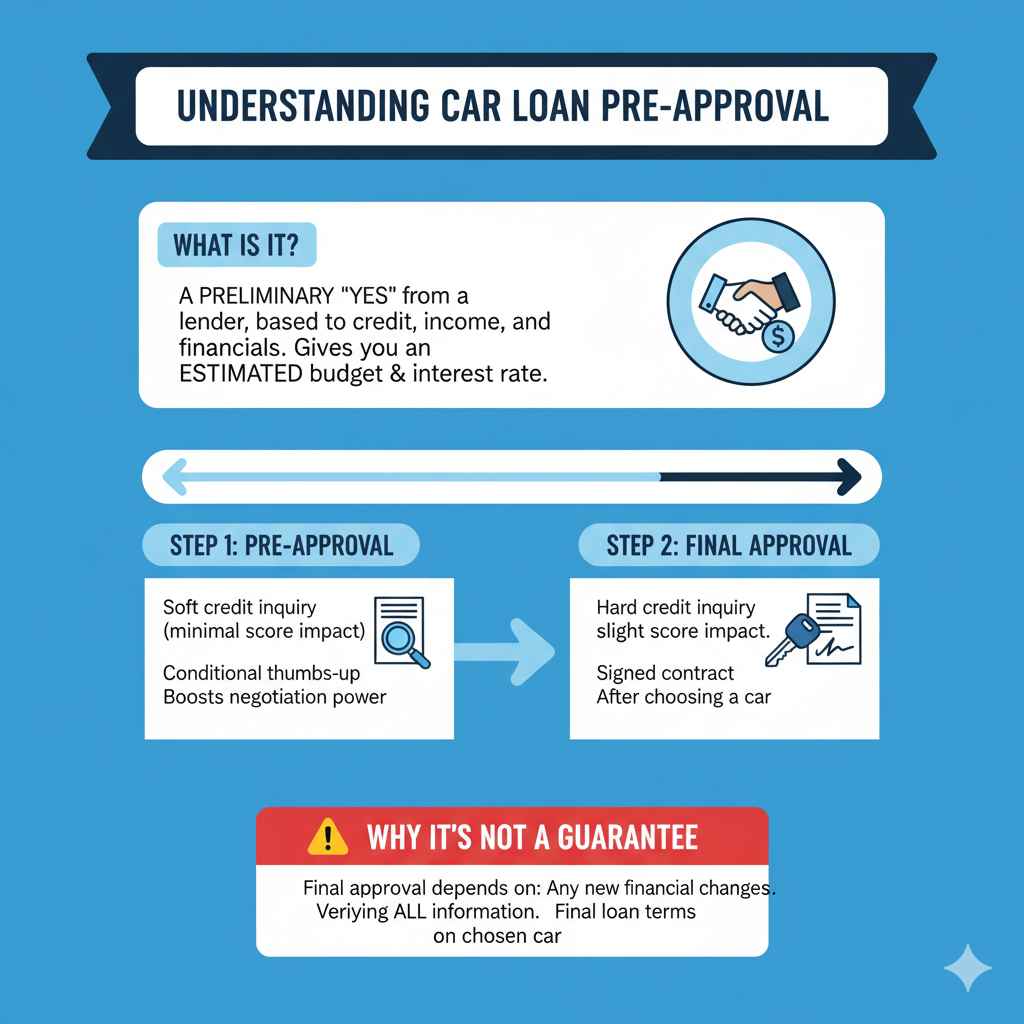

So, what exactly is car loan pre-approval? Think of it as a lender giving you a preliminary “yes” based on the financial information you provide upfront. They’ll look at your credit history, income, and other financial details to estimate how much they might be willing to lend you and at what general interest rate. It’s a fantastic tool because it gives you a solid understanding of your budget before you even set foot on a car lot.

This initial step shows dealerships you’re a serious buyer and can help you negotiate from a stronger position. However, it’s important to remember that pre-approval isn’t the same as final loan approval. It’s more like a conditional thumbs-up, not a signed contract. The real work begins after you find the car you love!

Why Pre-Approval Isn’t a Guarantee

Here’s the crucial part: a lot can happen between your initial pre-approval and driving off the lot with your new car. The lender’s initial assessment is based on the information you provided at that specific moment. If any new information comes to light, or circumstances change, it can impact the final decision. Understanding these potential pitfalls is key to navigating the car buying process smoothly.

Common Reasons for Car Loan Denial After Pre-Approval

Even with a pre-approval letter in hand, lenders have the final say. If something changes or was overlooked, your loan could be denied. Let’s look at the most frequent reasons this happens, so you can be prepared and avoid these common traps.

1. Changes in Your Financial Situation

Your financial health is the biggest factor in loan approval. If anything significant changes between your pre-approval and the final paperwork, it can cause trouble. Lenders want to see stability.

- Job Loss or Income Reduction: If you lose your job, have your hours cut, or your income decreases significantly, lenders see this as a higher risk. Your ability to repay the loan is directly tied to your income.

- New Debt: Taking on new loans, opening new credit cards and maxing them out, or even large purchases on existing credit cards can increase your debt-to-income ratio, making you appear more financially strained.

- Missed Payments on Other Debts: If you miss payments on existing loans or credit cards after getting pre-approved, this will hurt your credit score and send up red flags for the lender.

2. Issues with the Vehicle Itself

Sometimes, the car you choose can be the reason for denial, even if your finances look good.

- Vehicle Age or Mileage: Lenders often have limits on how old a car can be or how many miles it can have for them to finance it. Older cars or those with very high mileage are seen as riskier investments.

- Vehicle Value: If the car’s market value is significantly lower than the loan amount you’re requesting, the lender might be hesitant. They risk not being able to recover their investment if you default. This is especially true for unique or highly modified vehicles.

- Title Issues: A car with a salvage title, flood damage, or other problematic history might be automatically disqualified, regardless of its price.

3. Discrepancies in Information Provided

Honesty and accuracy are crucial throughout the loan application process. Any inaccuracies could lead to denial.

- Misrepresented Income or Employment: If the details you provided during pre-approval don’t match up with what the lender verifies during the final underwriting process, it can be seen as a serious issue.

- Incomplete Application: Missing information or failing to provide all necessary documents promptly can delay the process and, in some cases, lead to denial.

- Errors on Credit Report: While you should have checked your credit before pre-approval, sometimes new errors can appear, or previously unknown negative information might surface during the deeper dive.

4. Lender-Specific Requirements or Changes

Each lender has its own set of rules and risk tolerance. What one lender approves, another might not.

- Loan-to-Value Ratio (LTV): Lenders have limits on how much they’ll lend compared to the car’s value. If your down payment is too small for the car you’ve picked, you might exceed their LTV threshold.

- Changes in Lender Policies: Lenders can change their lending criteria or risk appetite based on economic conditions. A loan that was potentially approvable yesterday might be rejected today if the lender tightens its policies.

- Inability to Verify Information: If the lender can’t independently verify details like your employment or address, they may deny the loan to mitigate risk.

5. Credit Score Drop

Your credit score is a snapshot of your creditworthiness. While pre-approval is based on your score at that moment, a significant drop can kill the deal.

- New Credit Inquiries: Applying for multiple new credit lines (like credit cards or other loans) between pre-approval and final approval can lower your score.

- Late Payments: As mentioned earlier, any late payments on existing accounts will negatively impact your score.

- Increased Credit Card Balances: Using more of your available credit can also bring your score down.

Key Differences: Pre-Approval vs. Final Approval

It’s vital to understand that pre-approval and final approval are distinct stages. Pre-approval is the initial screening, while final approval is the deep dive.

Pre-Approval: This is typically a conditional commitment from a lender. They’ve reviewed your credit report, credit score, and basic financial information (like income and employment). They provide an estimated loan amount, interest rate, and term based on this initial assessment. It’s a good indicator of what you might qualify for but is not a guaranteed loan.

Final Loan Approval: This is the binding commitment from the lender. It happens after you’ve selected a specific vehicle and the lender has completed a thorough underwriting process. This includes:

- Verification of all financial documents (pay stubs, bank statements, tax returns).

- Appraisal or verification of the chosen vehicle’s value and condition.

- A final review of your credit report.

- Verification of employment and residence.

If any of these elements don’t meet the lender’s criteria at this later stage, the loan can be denied.

How to Prevent Denial After Pre-Approval

Don’t let the possibility of denial discourage you! With the right approach, you can significantly increase your chances of a smooth transaction from pre-approval to final sign-off.

1. Maintain Your Financial Stability

The most critical step is to keep your financial picture as stable as possible after getting pre-approved.

- Avoid New Debt: Resist the urge to open new credit cards or take out other loans. If you need to make a large purchase, consider if it can wait until after the car loan is finalized.

- Pay Bills on Time: Ensure all your existing bills (credit cards, other loans, utilities) are paid on schedule. Even one missed payment can have a devastating effect.

- Keep Credit Utilization Low: Try not to use a large percentage of your available credit. If you can pay down some credit card balances, even better.

2. Be Transparent and Accurate

Honesty is the best policy, especially when dealing with lenders.

- Provide Correct Information: Double-check all details you give to the lender. Ensure your income, employment history, and address are accurate.

- Submit Documents Promptly: When the lender requests verification documents (like pay stubs or bank statements), provide them as quickly as possible. Delays can sometimes lead to the lender rescinding their offer.

3. Choose Your Vehicle Wisely

The car you select plays a significant role. Work with your pre-approval amount as a guide, but also consider these vehicle-specific factors.

- Stick to Reputable Sellers: Buying from a well-established dealership often means the vehicles have gone through more rigorous checks.

- Research Vehicle Value: Use resources like Kelley Blue Book (KBB) or the National Automobile Dealers Association (NADA) Guides to understand the fair market value of the car you’re interested in. Kelley Blue Book is a great place to start.

- Check Vehicle History Reports: Always get a CarFax or AutoCheck report to uncover any hidden issues like accidents or title problems.

- Consider LTV: Be aware of the Loan-to-Value ratio. If you’re buying a car that’s priced above its market value or you have a small down payment, you might be pushing the Lender’s LTV limits. A larger down payment can help here.

4. Understand Lender Requirements

Don’t be afraid to ask questions and understand the specifics of your pre-approval offer.

- Ask About Vehicle Restrictions: Inquire if the lender has any restrictions on vehicle age, mileage, or type.

- Clarify LTV Policies: Understand their maximum Loan-to-Value ratio.

- Know the Expiration Date: Pre-approvals usually have an expiration date. Make sure you’re aware of it and aim to complete your purchase within that timeframe.

5. Review Your Credit Report

Before you even apply for pre-approval, and certainly after, examine your credit report for errors.

- Get Free Reports: You are entitled to one free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) every year at AnnualCreditReport.com.

- Dispute Errors: If you find any inaccuracies, dispute them immediately with the credit bureau. Addressing them can boost your score and prevent unexpected issues.

What to Do If Your Car Loan Is Denied

It’s never ideal, but if you find yourself denied, don’t panic. There are always steps you can take. First, find out exactly why the loan was denied.

1. Ask for the Specific Reason

Contact the lender and politely ask for the precise reason for the denial. They are often required by law to provide this information, especially concerning credit. Understanding the “why” is the first step to finding a solution.

2. Address the Underlying Issue

Once you know the reason, you can work on fixing it.

- Credit Score Issues: If your credit score dropped or was lower than expected, focus on improving it. Pay down debt, make on-time payments, and avoid new credit inquiries. You can also check your credit report for errors and dispute them.

- Income/Debt Ratio: If your debt-to-income ratio is too high, you might need to reduce existing debt or increase your income. Alternatively, you could look for a less expensive vehicle.

- Vehicle Issues: If the problem was the car itself (age, value, title), you’ll need to look for a different vehicle that meets the lender’s criteria.

3. Reapply or Seek Other Lenders

Depending on the reason for denial, you might be able to reapply after addressing the issue. Or, you can explore other financing options.

- Subprime Lenders: If your credit is the main issue, subprime auto lenders specialize in working with borrowers who have lower credit scores. Be prepared for higher interest rates.

- Dealership Financing: Many dealerships have relationships with multiple lenders and can help you find financing, even if your credit isn’t perfect.

- Credit Unions: Credit unions often offer competitive rates and may be more flexible with their lending criteria than large banks.

- Co-signer: If you have a friend or family member with good credit who is willing to co-sign the loan, this can significantly improve your chances of approval. However, remember that a co-signer is equally responsible for the debt.

4. Consider a Smaller Loan or Down Payment

Sometimes, adjusting the loan amount can make a difference. If you can increase your down payment or look for a less expensive car, this can lower the overall risk for the lender and potentially lead to approval.

Impact on Your Credit Score

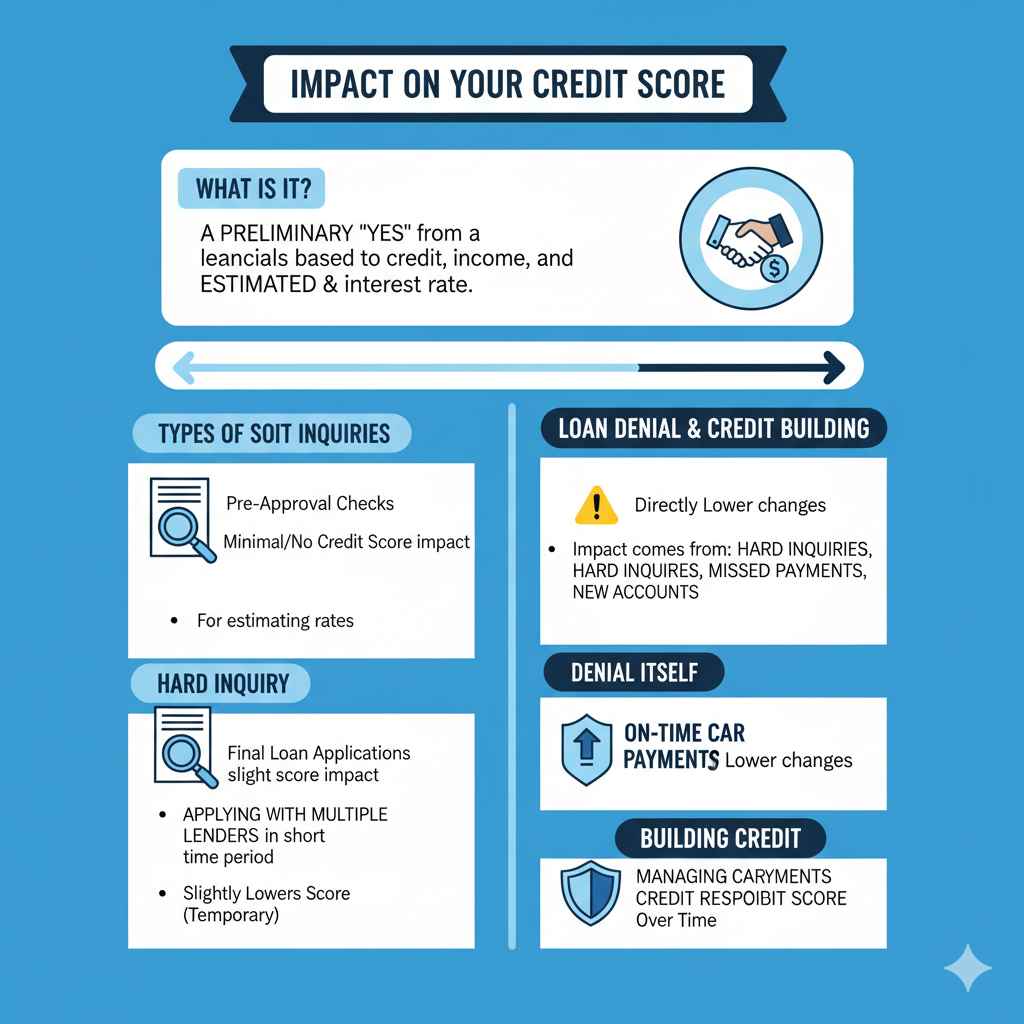

It’s good to know how the loan process affects your credit. Applying for pre-approval often involves a “soft inquiry,” which doesn’t typically impact your credit score. However, when a lender does a full credit check for final approval (a “hard inquiry”) or if you apply with multiple lenders in a short period for different options, it can slightly lower your score.

A car loan denial itself generally doesn’t directly lower your credit score. The reduction comes from the hard inquiries and potentially from opening new accounts or missed payments that contributed to the denial. The good news is that responsible handling of a car loan, including on-time payments, will help build your credit over time.

FAQ: Can You Be Denied a Car Loan After Pre-Approval?

Here are answers to some common questions about this topic:

Q1: What is the difference between pre-qualification and pre-approval for a car loan?

A1: Pre-qualification is a quick estimate based on self-reported information, usually without a credit check, giving you a rough idea of what you might borrow. Pre-approval involves a lender checking your credit report and financial details, making it a more solid, though still conditional, indication of loan approval.

Q2: How long is a car loan pre-approval typically valid for?

A2: Pre-approvals usually last between 30 to 90 days. It’s best to confirm the exact validity period with your lender, as it can vary.

Q3: If I get pre-approved, does that mean I’m guaranteed to get the loan?

A3: No, not at all. Pre-approval is a conditional commitment. The final approval depends on a thorough review of the specific car you choose, verification of your financial information, and your financial situation remaining stable until the loan is finalized.

Q4: Can a lender withdraw a pre-approval offer?

A4: Yes, a lender can withdraw a pre-approval offer if your financial situation changes negatively (e.g., job loss, new debt) or if there are significant discrepancies in the information you provided that are discovered during the final underwriting process.

Q5: What happens if the car I want costs more than my pre-approval amount?

A5: If the car’s price, plus taxes and fees, exceeds your pre-approval limit, you’ll need to either increase your down payment, negotiate the car’s price, find a less expensive vehicle, or seek financing for the difference from another source.

Q6: Should I wait to get pre-approved until I find the exact car I want?

A6: It’s generally better to get pre-approved first. This gives you a clear budget and shows dealerships you are a serious buyer. Once pre-approved, you can then use that knowledge to find a vehicle that fits within your approved loan amount and meets lender criteria.

Conclusion

Navigating the car loan process can feel complex, but understanding the steps involved is key to success. While car loan pre-approval is a valuable tool that gives you a strong starting point and a clear budget, it’s never a final guarantee. By staying vigilant about your financial health, being transparent with lenders, choosing your vehicle wisely, and knowing the potential pitfalls, you can significantly reduce the risk of denial after pre-approval.

Remember, if you do encounter a denial, don’t get discouraged. Seek to understand the exact reason, address the underlying issue, and explore alternative lenders or options like a co-signer. With careful planning and informed decisions, you’ll be well on your way to driving home in your new car. Happy car hunting!