Do I Need Insurance for a Loaner Car? Essential Guide

Yes, you generally need insurance for a loaner car, though your existing auto insurance policy might cover it. Understanding who is responsible and what your policy covers is key to avoiding out-of-pocket expenses if an accident occurs with a temporary vehicle.

Getting Back on Track: Your Essential Guide to Loaner Car Insurance

When your car is in the shop for repairs, getting a loaner car can feel like a lifesaver. It means you can keep moving and handle your daily life without too much disruption. But a common question pops up: “Do I need insurance for this temporary ride?” It’s normal to feel a bit unsure, especially when dealing with unfamiliar situations. The good news is, understanding loaner car insurance is simpler than you might think. This guide will walk you through everything you need to know, making sure you’re covered and confident while driving that temporary vehicle.

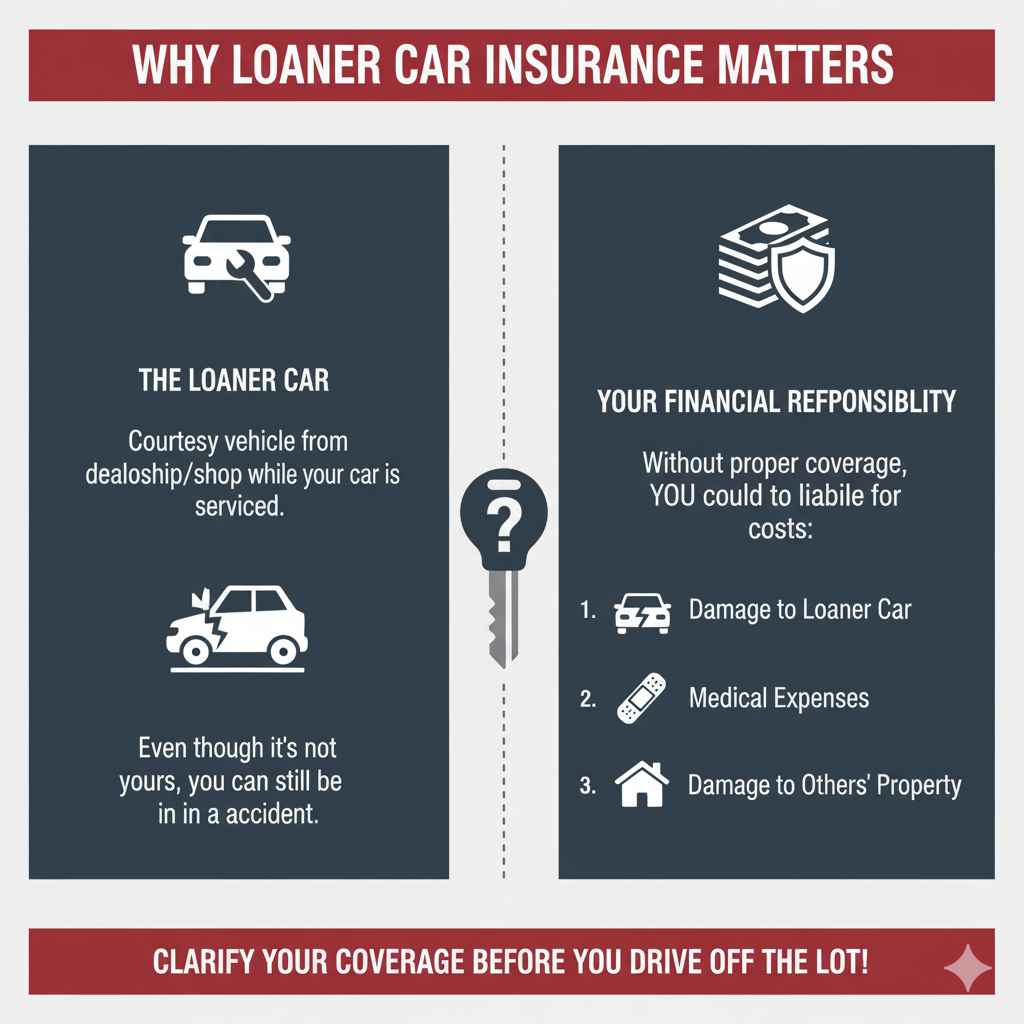

Why Loaner Car Insurance Matters

When your car is being serviced or repaired, the dealership or repair shop might offer you a loaner vehicle. This is a courtesy to help you stay mobile. While it’s a convenient service, it’s crucial to remember that this car, even though it’s not yours, can still be involved in an accident. In such a case, someone needs to be financially responsible for any damages or injuries. This is where understanding insurance comes into play.

Without proper coverage, you could be liable for significant costs if something happens to the loaner car or if you cause damage to another vehicle or property. This could include repair bills for the loaner, medical expenses for anyone injured, and costs associated with damage to other people’s property. It’s a situation no one wants to face, which is why clarifying your insurance status before you drive off the lot is so important.

Your Existing Auto Insurance Policy: The First Line of Defense

Many drivers assume their personal auto insurance policy will automatically cover them when they drive a loaner car. In most cases, this is true, but it’s not an automatic guarantee for every situation. Your personal auto insurance policy is designed to follow you, the driver, with your policy’s coverage limits and deductibles applying to the vehicle you are driving, whether it’s your own car or a temporary one.

Your policy typically covers:

Liability Coverage: This helps pay for bodily injury and property damage to others if you are involved in an accident and it’s your fault.

Collision Coverage: This helps pay for damage to the loaner car if it’s damaged in a collision, up to your policy limits and after you pay your deductible.

Comprehensive Coverage: This helps pay for damage to the loaner car that isn’t caused by a collision, like theft or vandalism, again, up to your policy limits and after your deductible.

However, it’s essential to verify this with your insurance provider. Different policies have different terms, and specific exclusions might apply. For instance, if you have a very basic liability-only policy, it may not extend to cover damage to the loaner vehicle itself.

What to Ask Your Insurance Provider

Before you even pick up the loaner car, it’s a smart move to have a quick chat with your insurance company. Here are some key questions to ask:

Does my current auto insurance policy extend coverage to temporary or substitute vehicles, such as loaner cars?

What are my coverage limits for liability, collision, and comprehensive when driving a loaner car? Are they the same as my personal vehicle?

What is my deductible for claims involving a loaner car?

Are there any specific exclusions in my policy that would prevent coverage for a loaner car?

If I typically don’t have collision or comprehensive coverage on my own vehicle, will it be applied to the loaner for damage to that vehicle?

What documentation do I need to keep from the repair shop and my insurance company in case of an incident?

Asking these questions upfront can save you a lot of stress and potential financial headaches down the road.

The Dealership’s Insurance: What It Covers (And What It Doesn’t)

Dealerships and repair shops that provide loaner cars typically have their own insurance policies. However, these policies are usually designed to be secondary to your personal insurance. This means they often act as a backstop if your own insurance isn’t sufficient or doesn’t apply.

Dealership insurance might cover:

Excess Damage: If the damage to the loaner car exceeds your personal insurance limits or your ability to pay your deductible.

Uninsured/Underinsured Scenarios: If you don’t have adequate personal insurance.

Third-Party Claims: In some cases, if your insurance denies your claim or if you cause damage to others and your policy has lapsed.

It’s important to understand that the dealership’s insurance is not a free pass. They will likely expect you to cover damages up to your personal policy’s deductible, and if your policy doesn’t cover certain types of damage, you could be held responsible for the full cost. Always clarify this with the dealership before driving away.

When Your Insurance Might Not Cover a Loaner Car

While your personal insurance usually extends to loaner cars, there are a few scenarios where it might not:

Policy Exclusions: Your policy might have specific clauses that exclude coverage for rental or loaner vehicles, especially if you don’t carry comprehensive and collision coverage on your own car.

Driver Restrictions: If you have specific restrictions on your policy (e.g., if you’ve added an excluded driver), these could apply to a loaner car as well.

Commercial Use: If you plan to use the loaner car for business purposes, your personal auto insurance likely won’t cover it. Personal auto insurance is for personal use only.

Geographic Limitations: Some policies have limitations on where you can drive a covered vehicle. If the loaner car will be driven outside these limits, coverage might be void.

Notifying Your Insurer: Failing to inform your insurer that you are driving a loaner car might lead to issues if a claim arises, though many policies automatically extend coverage. It’s always best to check.

Out-of-State or International Rental: While less common for standard loaner agreements, if you were to rent a car instead of getting a loaner and drive it far from home or overseas, specific policy endorsements might be needed.

The Dangers of Driving Without Insurance on a Loaner Car

Driving a loaner car without adequate insurance is a risky proposition. If an accident occurs, you could face several serious consequences:

Financial Ruin: You could be personally responsible for the full cost of repairing the loaner car, which can easily run into thousands of dollars. Imagine the bill for a new bumper, fender, or even major structural damage on a late-model vehicle!

Liability for Damages to Others: If you cause an accident that damages another vehicle or injures someone, you will be liable for those costs. Without insurance, these expenses can quickly escalate into tens or hundreds of thousands of dollars.

Medical Bills: If anyone involved in an accident is injured, you could be responsible for their medical expenses, which can be astronomical.

Legal Troubles: Beyond financial responsibility, you could also face legal action, including lawsuits and potentially even criminal charges depending on the severity of the incident and your state’s laws.

Damage to Your Reputation: A significant accident can have long-term impacts, affecting your ability to get insurance in the future and potentially even impacting your credit score.

Can You Purchase Temporary Insurance (a Waiver)?

Sometimes, dealerships will offer you a Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW) for the loaner car. This is essentially a type of insurance offered by the rental company or dealership that waives your responsibility for damage to the vehicle.

What it covers: Typically covers damage to the loaner car itself, often with a deductible.

What it usually doesn’t cover: It rarely covers damage to other vehicles, property, or any injuries you might cause to others. This is why it’s crucial to have your own liability insurance.

Cost: These waivers can add a daily fee to your loaner car arrangement.

Value: If your personal insurance doesn’t cover damage to the loaner vehicle, or if you want to avoid your deductible, a CDW/LDW can be valuable. However, with comprehensive and collision coverage on your own policy, it’s often redundant and an unnecessary expense.

Always read the fine print of any waiver you consider purchasing. Understand exactly what it covers and what it excludes, and compare its cost and benefits to your existing insurance.

How to Get Covered: Steps to Take

Navigating the world of loaner car insurance can seem daunting, but it doesn’t have to be. Follow these steps to ensure you’re covered:

1. Understand Your Current Policy: Before you need a loaner, familiarize yourself with your auto insurance policy. Pay attention to sections on rental cars or substitute vehicles. If it’s unclear, call your insurance agent.

2. Contact Your Insurance Provider: As soon as you know you’ll be getting a loaner car, call your insurance company. Confirm that your policy extends coverage and understand the specifics (deductibles, limits, exclusions). Get this confirmation in writing if possible.

3. Talk to the Dealership/Repair Shop: When you arrange for the loaner car, ask them about their insurance policy and what they expect from you. Inquire about any waivers they offer and their cost.

4. Document Everything: Make sure you have all necessary documents, including your driver’s license, insurance card, and the loaner car agreement from the dealership, which should detail the car’s VIN, mileage, and any pre-existing damage.

5. Inspect the Loaner Car: Before driving off, thoroughly inspect the loaner car for any existing damage (scratches, dents, interior wear). Document any issues with photos or videos and ensure they are noted on the loaner agreement. This protects you from being blamed for pre-existing damage.

6. Drive Carefully and Responsibly: Treat the loaner car with the same care and respect you would your own vehicle. Obey all traffic laws and avoid risky driving behaviors.

Protecting Yourself: Best Practices Checklist

Here’s a quick checklist to keep you on the safe side:

Confirm your personal auto insurance covers loaner cars.

Understand your deductibles and coverage limits for a loaner.

Ask the dealership about their insurance and any waivers offered.

Read any loaner car agreement thoroughly before signing.

Inspect the loaner car for damage and document it.

Keep copies of all relevant documents handy.

Drive cautiously and adhere to traffic laws.

Understanding Deductibles on Loaner Cars

Your deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. When you have a loaner car and an accident occurs that your insurance covers, your deductible will apply. For example, if you have a $500 deductible and the damage to the loaner car costs $3,000 to repair, you would pay $500, and your insurance would pay the remaining $2,500.

If the dealership offers a Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW), it might allow you to waive your deductible for damage occurring to the loaner vehicle. However, these waivers often have their own fees and exclusions.

Important Note: Your deductible only applies to damage to the vehicle you are driving that is covered by your policy. It does not apply to liability claims where you are being sued for damage you caused to others.

What About Your Credit Score?

If you cause damage to a loaner car and don’t have insurance or adequate coverage, you could be held personally liable for the repair costs. If you are unable to pay these costs, the repair shop or dealership might turn the debt over to a collection agency. Unpaid collections can significantly harm your credit score, making it harder to get loans, rent an apartment, or even get certain jobs in the future.

Conversely, if your insurance company pays for damages, and you have a deductible, paying that deductible on time will not negatively impact your credit. However, if you have a history of claims, especially at-fault accidents, this can sometimes lead to increased premiums or even difficulty getting insured in the future.

Temporary Car Insurance Options

In rare cases, if your personal insurance doesn’t extend to loaner cars, or if you have very limited coverage, getting temporary insurance might be an option. However, for standard loaner situations, this is usually unnecessary and quite expensive. Dealerships might offer a form of supplemental liability insurance or damage waiver.

A more reliable approach is to proactively ensure your primary auto insurance policy is comprehensive enough to cover situations like driving a loaner. If you consistently find yourself in situations where you lack adequate coverage for temporary vehicles, it might be time to re-evaluate your current auto insurance policy with your agent. For instance, ensuring you have full comprehensive and collision coverage on your primary vehicle often provides the necessary protection for loaners.

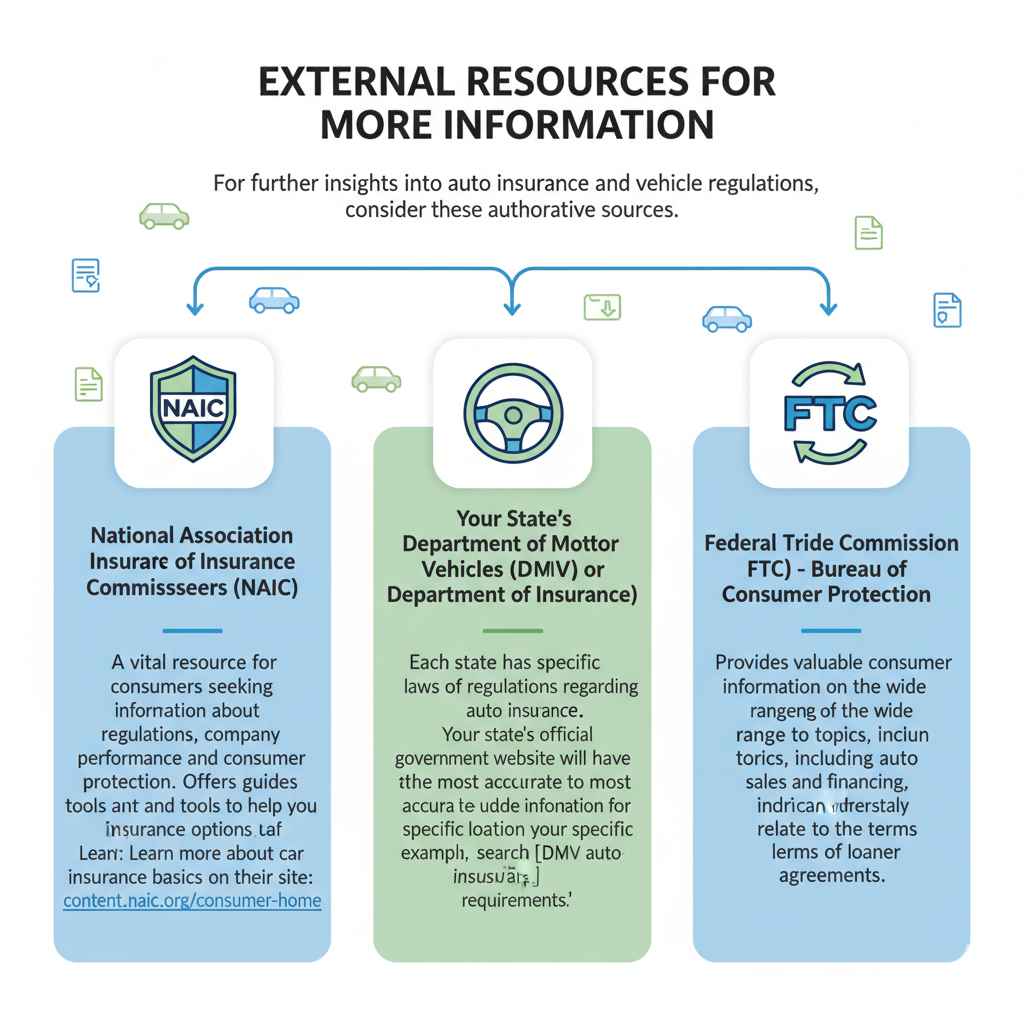

External Resources for More Information

For further insights into auto insurance and vehicle regulations, consider these authoritative sources:

National Association of Insurance Commissioners (NAIC): The NAIC is a vital resource for consumers seeking information about insurance regulations, company performance, and consumer protection. Their website offers guides and tools to help you understand your insurance options. You can learn more about car insurance basics on their site: https://content.naic.org/consumer-home

Your State’s Department of Motor Vehicles (DMV) or Department of Insurance: Each state has specific laws and regulations regarding auto insurance. Your state’s official government website will have the most accurate and up-to-date information for your specific location. For example, searching “[Your State] DMV auto insurance requirements” will lead you to official resources.

Federal Trade Commission (FTC) – Bureau of Consumer Protection: The FTC provides valuable consumer information on a wide range of topics, including auto sales and financing, which can indirectly relate to the terms of loaner agreements. Their aim is to protect consumers from unfair or deceptive business practices: https://www.consumer.ftc.gov/

Frequently Asked Questions (FAQ)

Q1: Will my personal car insurance cover a loaner car?

A1: In most cases, yes. Your personal auto insurance policy typically extends to cover you when you’re driving temporary vehicles like loaner cars, provided you are driving them with the owner’s permission and for personal use. However, it’s crucial to confirm this with your insurance provider and understand your specific policy’s terms, deductibles, and coverage limits.

Q2: What if I don’t have comprehensive and collision coverage on my own car?

A2: If your personal policy only includes liability coverage, it will likely cover damages you cause to others in a loaner car, but it won’t cover damage to the loaner vehicle itself. In this situation, you would be responsible for the cost of repairs to the loaner unless you purchase a damage waiver from the dealership.

Q3: What’s the difference between a CDW/LDW and my own insurance?

A3: A Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW) is offered by dealerships or rental agencies. It typically covers only damage to the specific vehicle you are borrowing, often with a deductible paid to the dealership. Your personal insurance is a broader contract that usually includes liability coverage for damage to others, and potentially collision/comprehensive for damage to the borrowed vehicle, subject to your policy’s terms and deductibles.

Q4: Do I need to tell my insurance company I’m getting a loaner car?

A4: While many policies automatically extend coverage, it’s always best practice to inform your insurance company that you will be driving a loaner car. This ensures there are no surprises if a claim arises and allows you to confirm your coverage details. Some policies might require notification.

Q5: What should I do if I get into an accident in a loaner car?

A5: Treat it like any other accident. Ensure everyone is safe, call emergency services if necessary, exchange information with any other drivers involved, and notify the police. Then, contact your insurance company immediately to report the incident. Also, inform the dealership or repair shop that provided the loaner car as soon as possible.

Q6: Can the dealership charge me for damages if my insurance doesn’t fully cover it?

A6: Yes. If the damages exceed your insurance coverage limits or if your policy doesn’t cover certain types of damage, you can be held financially responsible for the remaining costs. This is why understanding your policy limits and having adequate coverage is essential.

Q7: Do my insurance deductibles apply to a loaner car?

A7: Yes, if your personal insurance covers the damage to the loaner car, your standard deductibles for collision and comprehensive coverage will apply. You will be responsible for paying these amounts before your insurance pays the rest of the covered damages.

Conclusion: Drive with Confidence

Navigating the road with a loaner car is a temporary necessity for most drivers. Understanding your insurance coverage is key to handling this situation with confidence and avoiding unexpected financial burdens. By taking a few proactive steps—confirming your policy with your insurer, understanding the dealership’s terms, and documenting everything—you can ensure that your temporary wheels are just as covered as your everyday drive.

Remember, your aim is always to be prepared. A little bit of knowledge goes a long way in protecting you and your finances. So, when you pick up that loaner car, you can do so with peace of mind, knowing you’re equipped with the right information to keep you safe and sound on the road. Happy driving!