Does Car Insurance Cover Repairs: Your Essential Guide

Your car insurance likely covers repairs, but only under very specific circumstances. It’s not a free pass for all fixes. This guide breaks down exactly what your policy might pay for, helping you understand when to file a claim and what to expect.

Hey there, fellow drivers! Ever had that sinking feeling when you hear a strange noise from your car, or worse, after a fender bender? You instantly wonder, “Will my car insurance company help me pay for this?” It’s a super common question, and honestly, a little confusing. Dealing with car troubles is stressful enough without the added worry about repair bills. But don’t sweat it! I’m here to break down exactly how your car insurance works when it comes to repairs. We’ll shed some light on what your policy covers, what it doesn’t, and how to make sense of it all. Get ready to feel more confident about your car insurance and what it can do for you.

Understanding Your Car Insurance and Repairs: The Basics

Think of your car insurance as a safety net. It’s designed to protect you financially when unexpected, specific events happen to your vehicle. It’s not typically a magic wand that fixes any old wear and tear or routine maintenance. The key is understanding the different types of coverage you have and how they apply to repairs.

What is Car Insurance Really For?

At its core, car insurance is a contract between you and an insurance company. You pay a regular premium, and in return, the insurer agrees to cover certain financial losses related to your car in exchange for that premium. These losses usually stem from accidents, theft, or other covered perils.

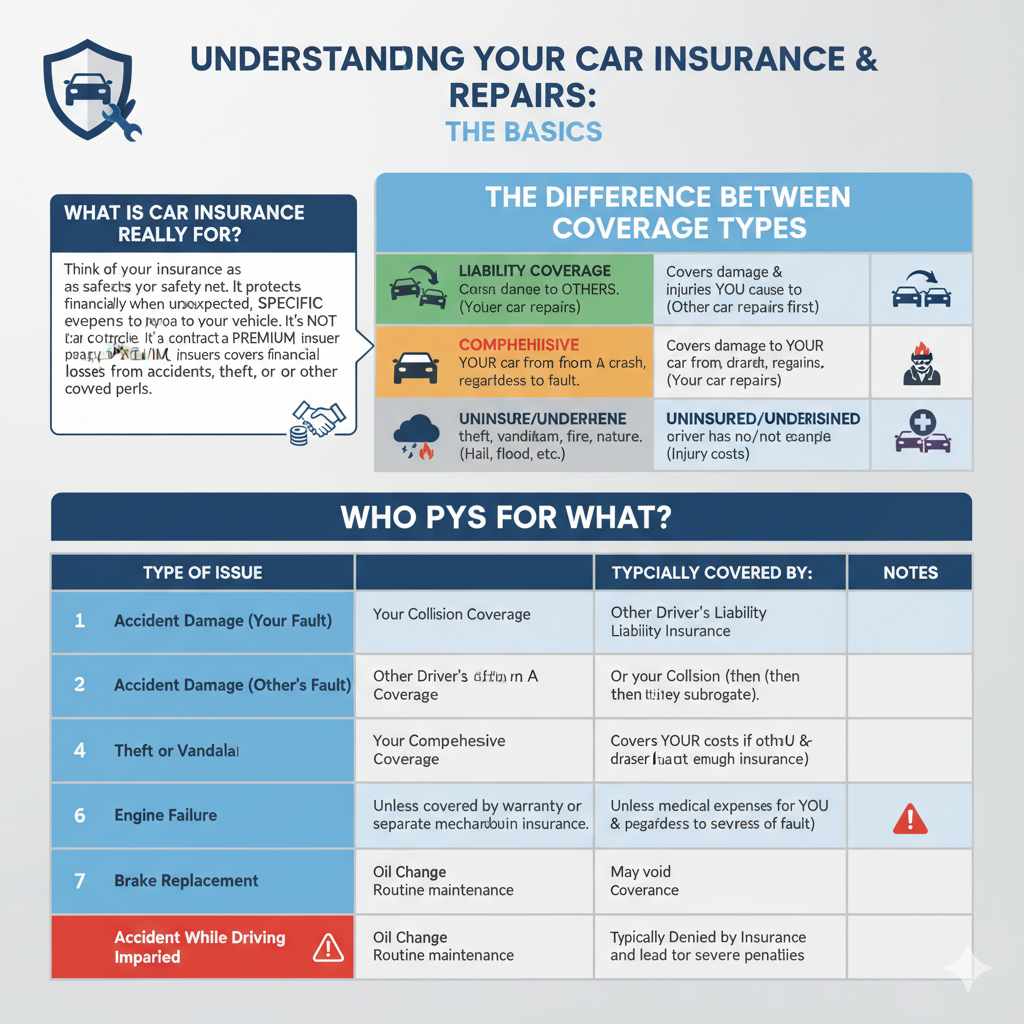

The Difference Between Coverage Types

Not all car insurance policies are the same. The types of coverage you choose directly determine what kind of repairs can be paid for by your insurance. Here’s a quick look at the main players:

- Liability Coverage: This is your legal minimum in most places. It covers damage and injuries you cause to other people or their property in an accident. So, if you’re at fault, your liability coverage would pay to fix the other car, not yours.

- Collision Coverage: This is the coverage that often comes to mind for repairs after an accident. Collision coverage helps pay to repair or replace your car if it’s damaged in a crash with another vehicle or object, regardless of who is at fault.

- Comprehensive Coverage: Think of this as “other than collision” damage. Comprehensive coverage helps pay for damage to your car from things like theft, vandalism, fire, falling objects, or natural disasters (like hail or floods).

- Uninsured/Underinsured Motorist Coverage: This helps cover your costs if you’re in an accident with a driver who has no insurance or not enough insurance to cover your damages.

- Medical Payments Coverage (MedPay) or Personal Injury Protection (PIP): These cover medical expenses for you and your passengers, regardless of fault. They don’t cover car repairs directly but handle injury costs.

When Does Car Insurance Actually Cover Repairs?

This is the big question! Your car insurance typically steps in to cover your car’s repairs in these main situations:

1. After an Accident (Collision Coverage)

If you’re involved in a collision, your collision coverage is what you’ll likely rely on. This applies whether you hit another car, a lamppost, a fence, or even if you roll your vehicle. The important thing to remember here is that it covers damage to your car from the accident itself.

- At-Fault Accidents: If the accident is determined to be your fault, your collision coverage will pay for your car’s repairs, minus your deductible.

- Not-at-Fault Accidents: Even if the other driver caused the accident, your collision coverage can still be used to get your car repaired quickly. Your insurance company will then try to recover that money from the other driver’s insurance (this is called subrogation). Alternatively, if the other driver has insurance, you might file a claim directly with their insurer.

2. Damage from Non-Collision Events (Comprehensive Coverage)

Life throws curveballs, and sometimes, they involve your car! If your car is damaged by something other than a crash, your comprehensive coverage is usually the hero.

- Theft: If your car is stolen and damaged during the theft, or if it’s recovered but damaged, comprehensive coverage can help.

- Vandalism: Unfortunately, sometimes cars are targets for malicious damage. Comprehensive coverage would help fix things like broken windows or scratched paint.

- Fire: If your car catches fire, this coverage can help with the repairs or replacement.

- Natural Disasters: Damage from events like hail, floods, falling trees, or strong winds are typically covered.

- Animal Collisions: Hitting a deer or another animal often falls under comprehensive coverage, rather than collision.

3. When Repairs Are Due to a Specific Covered Event

It’s crucial to grasp that insurance covers damage from a sudden and accidental event. It’s not for gradual wear and tear or maintenance.

When Does Car Insurance NOT Cover Repairs?

This is just as important as knowing what is covered. Many common car issues are unfortunately not covered by standard auto insurance policies.

1. Routine Maintenance and Wear and Tear

Your insurance policy is not designed to be a car maintenance fund. Things like:

- Oil changes

- Brake pad replacements

- Tire rotations

- Engine tune-ups

- Battery replacements due to age

- Worn-out parts

These are all the responsibility of the car owner. They are expected upkeep for owning a vehicle.

2. Mechanical Breakdowns

If your engine suddenly gives out, your transmission fails, or your alternator dies, these are mechanical breakdowns. Unless you have a separate mechanical breakdown insurance policy (which is rare and often limited) or a manufacturer’s warranty still active, your standard car insurance will not cover these repairs.

3. Pre-existing Damage

Insurance companies won’t cover damage that existed before you got your policy or damage that occurred but wasn’t reported. They want to cover new incidents.

4. Intentional Damage

If you intentionally damage your own vehicle, your insurance won’t cover it. This is also true if the damage is caused by someone you know intentionally.

5. Driving Under the Influence (DUI/DWI)

If you cause an accident while driving under the influence of alcohol or drugs, your insurance company may deny your claim or significantly increase your premium afterwards. Many policies have exclusions for this. Check out resources from the National Highway Traffic Safety Administration (NHTSA) for more on the dangers and consequences of impaired driving.

6. Racing, Speed Contests, or Illicit Activities

Using your car for illegal street racing or participating in any illegal activity typically voids your insurance coverage.

7. Neglect or Lack of Maintenance

If a problem arises because you’ve clearly neglected your car’s maintenance (e.g., an engine seizing because you never checked the oil), the insurance company may deny the claim.

Understanding Your Deductible

When you do have a covered repair claim, you’ll likely encounter a “deductible.” This is the amount of money you agree to pay out-of-pocket before your insurance company starts paying for a covered loss.

For example, if you have a $500 deductible and your car needs $3,000 worth of collision repairs after an accident, you’ll pay the first $500, and your insurance company will cover the remaining $2,500 (subject to policy limits).

Choosing Your Deductible

You usually get to choose your deductible amount when you buy your policy. Common deductible amounts are $250, $500, $1,000, or even higher. Generally, a higher deductible means a lower premium, and a lower deductible means a higher premium.

Pro Tip: Make sure you can comfortably afford to pay your deductible if you need to file a claim. It’s wise to have this amount accessible in an emergency fund.

How to File a Claim for Repairs

If you’ve had an incident that you believe is covered by your insurance and requires repairs, here’s a general idea of how to proceed:

1. Safety First!

Immediately ensure everyone is safe. If there are injuries, call emergency services. If the accident is blocking traffic or poses a danger, try to move vehicles to a safe location if possible and safe to do so. If not, call the police.

2. Document Everything

Take photos or videos of the damage from multiple angles. If it’s an accident, exchange insurance information, names, and contact details with other parties involved. Get witness information if possible.

3. Contact Your Insurance Company

Report the incident to your insurance company as soon as possible. Most insurers have a claims department you can call, or you can file a claim through their website or mobile app. You’ll need to provide details about the incident, your vehicle, and any damage.

4. Claim Assessment

The insurance company will assign an adjuster to your claim. They will likely inspect the damage to your vehicle, either in person or sometimes through photos you provide. An adjuster’s role is to assess the damage, determine if it’s covered by your policy, and estimate the cost of repairs.

5. Repair Process

Once the claim is approved and the estimate is agreed upon, you’ll typically have a few options for repairs:

- Use a Shop in the Insurer’s Network: Many insurance companies have a network of preferred repair shops. These shops often have pre-negotiated rates and streamlined processes.

- Choose Your Own Repair Shop: You generally have the right to choose where your car is repaired. If you choose a shop not in the insurer’s network, the insurance company will still pay for the covered repairs, but there might be a different process for payment or getting estimates.

Your insurance company will usually pay the repair shop directly, minus your deductible, if you use an in-network facility. If you choose your own shop, they might pay you directly, or you might pay the shop and then get reimbursed by your insurer.

Can Extended Warranties or GAP Insurance Help?

While not standard car insurance, it’s worth mentioning two other types of protection that can assist with repair-related costs in specific situations:

Extended Warranties (or Service Contracts)

These are contracts purchased separately that cover repairs for mechanical breakdowns for a set period or mileage after your manufacturer’s warranty expires. They are not insurance and work on a different principle. They are generally for mechanical failures, not accident damage. Always read the fine print carefully to understand what is covered and what isn’t.

For more information on vehicle service contracts, you can consult resources from the Federal Trade Commission (FTC).

GAP Insurance (Guaranteed Asset Protection)

If your car is totaled in an accident and you owe more on your car loan or lease than the car is worth, GAP insurance covers the difference. This isn’t for routine repairs but for covering that financial gap if your car needs to be replaced after a major incident.

Making Smart Decisions About Your Insurance and Repairs

Understanding your policy is the first step to making smart decisions. Here are some tips:

- Read Your Policy: Don’t just file it away. Take the time to understand what coverages you have and what your deductibles are.

- Regularly Review Your Coverage: As your car ages or your financial situation changes, you might need to adjust your coverage. For example, if your car is older and not worth much, you might consider dropping collision and comprehensive coverage to save money on premiums.

- Maintain Your Vehicle: Preventative maintenance can save you a lot of money and hassle in the long run. It also shows your insurance company you’re a responsible owner.

- Understand the Value of Your Car: Knowing your car’s actual cash value (ACV) helps you understand potential payouts if it’s ever totaled.

- Don’t File Minor Claims: Filing too many claims, especially for minor damage, can lead to increased premiums or even non-renewal from your insurer. Assess if the repair cost is close to or less than your deductible and potential premium increases before filing.

Who Pays for What? A Comparison Table

To make it super clear, let’s look at a simple comparison of who typically pays for different car issues:

| Type of Issue | Typically Covered By: | Notes |

|---|---|---|

| Accident Damage (Your Fault) | Your Collision Coverage | You pay your deductible first. |

| Accident Damage (Other’s Fault) | Other Driver’s Liability Insurance | Or your Collision Coverage (then they subrogate). |

| Theft or Vandalism | Your Comprehensive Coverage | You pay your deductible first. |

| Hail or Flood Damage | Your Comprehensive Coverage | You pay your deductible first. |

| Engine Failure | Owner (out-of-pocket) | Unless covered by warranty or separate mechanical breakdown insurance. |

| Oil Change | Owner (out-of-pocket) | Routine maintenance. |

| Brake Replacement | Owner (out-of-pocket) | Routine maintenance. |

| Accident While Driving Impaired | Typically Denied by Insurance | May void coverage and lead to severe penalties. |

Frequently Asked Questions (FAQ)

Q1: Does car insurance cover dents and scratches?

A: Your car insurance may cover dents and scratches if they are the result of a covered event like an accident (covered by collision) or vandalism/falling objects (covered by comprehensive). It won’t cover dents and scratches from everyday wear and tear or minor scuffs. You’ll also need to consider your deductible.

Q2: What if my car’s engine blows up? Does insurance pay for that?

A: Generally, no. An engine failure is considered a mechanical breakdown, which is not covered by standard auto insurance. This is usually the owner’s responsibility unless the car is still under a manufacturer’s warranty or you have purchased separate mechanical breakdown insurance.

Q3: If someone hits my car and drives away (hit-and-run), what happens?

A: If the other driver is identified, their liability insurance would cover your repairs. If the driver is never found, your collision coverage would typically pay for your car’s repairs, assuming you have it. Your deductible would apply. In some states, your Uninsured Motorist Property Damage coverage might also apply.

Q4: Do I have to use a specific repair shop recommended by my insurance company?

A: No, you typically do not have to use a repair shop recommended by your insurance company. You have the right to choose your own mechanic. However, using a shop within the insurer’s network can sometimes streamline the process and ensure they have a direct billing relationship.

Q5: How does insurance know how much to pay for repairs?

A: The insurance company assigns an adjuster who inspects the damage and creates an estimate for repairs based on labor rates and parts costs in your area. They often use specialized software for this. If you disagree with the estimate, you can ask for a second opinion or present estimates from your chosen mechanic.

Q6: What happens if my car is damaged by a tree falling on it during a storm?

A: Damage from falling trees during a storm is typically covered by your comprehensive insurance coverage. You would report this as a comprehensive claim, and your deductible would apply.

Conclusion

Navigating car insurance and repairs can feel like a puzzle, but understanding the basics makes all the difference. Remember, your car insurance is a vital tool designed to protect you from significant financial losses due to specific, unexpected events like accidents, theft, or severe weather. It’s not a blanket policy to cover any repair your car might need, especially not routine maintenance or mechanical failures.

By knowing the difference between your collision, comprehensive, and liability coverages, understanding your deductible, and knowing when to file a claim, you can confidently manage your vehicle’s upkeep and unexpected hiccups.