How to Hide Your Car: Essential Guide

Hiding your car from repossession involves strategic parking, using private property, altering appearance, and understanding legal routes. This guide offers safe, legal methods to temporarily secure your vehicle while you resolve financial issues. Always prioritize communication with your lender.

It can be a stressful situation when you’re trying to avoid having your car repossessed. Life happens, and sometimes payments become difficult. You might be wondering, “How can I keep my car safe for a little while if I’m facing repossession?” It’s a common worry, and thankfully, there are sensible, legal ways to temporarily protect your vehicle. This guide will walk you through simple, effective steps to help you understand your options and give you peace of mind. We’ll cover practical tips to help you keep your car safe while you work on resolving the underlying issues.

Understanding Repossession and Your Rights

Before we dive into how to hide your car, it’s important to understand what repossession is and what rights you have. Repossession, in the context of car loans, happens when you fail to make your loan payments. The lender has the legal right to take back the vehicle because it serves as collateral for the loan. However, there are specific laws and regulations about how and when a lender can repossess a car. These laws vary by state, but generally, lenders cannot breach the peace during repossession, meaning they can’t use force, break into your garage, or threaten you.

Knowing your lender’s policy and your state’s laws can empower you. Many lenders prefer to work with borrowers rather than repossess a vehicle. Open communication is often the best first step. If you anticipate missing a payment or are already behind, contact your lender immediately to discuss possible solutions like payment plans, deferrals, or loan modifications. Even if you are looking into temporary measures to hide your car, understanding the legal framework is crucial to ensure you are not breaking any laws yourself.

For accurate information specific to your situation, consult with a legal aid society or a consumer protection agency. The Consumer Financial Protection Bureau (CFPB) is an excellent resource for understanding your rights and financial regulations.

Why Might Someone Need to Hide Their Car?

The primary reason someone searches for “how to hide your car from repossession” is the fear of losing their transportation. A car is often essential for daily life: getting to work, taking children to school, attending medical appointments, and running errands. Losing your car can create significant disruptions and financial hardship.

Other reasons might include:

- Temporary Financial Hardship: Facing unexpected job loss, medical bills, or other financial emergencies.

- Negotiating with Lender: Needing a short period to gather funds to catch up on payments or negotiate a new payment plan.

- Avoiding Further Damage: Wanting to prevent the car from being repossessed while exploring options to keep it long-term.

- Protecting a Vehicle with High Equity: If you owe significantly less on your car than its market value, repossession could mean losing that equity.

It’s important to remember that while these methods can offer temporary relief, they are not long-term solutions. The underlying financial issue needs to be addressed for a lasting resolution.

Legal and Ethical Considerations

Before you start strategizing, it’s vital to tread carefully and legally. While the goal is to temporarily secure your vehicle, actively evading a lender in a way that involves deception or illegal actions can have serious consequences. Most repossession laws are designed to balance the lender’s right to collateral with the borrower’s need for a vehicle and protection from harassment.

Here are some key points to keep in mind:

- No Tampering: Never tamper with your car’s Vehicle Identification Number (VIN) or license plates. This is illegal and can lead to criminal charges.

- No Damage: Do not damage the vehicle to make it “unappealing” to a repossessor.

- No Concealing with False Information: Do not provide false information about your location or the vehicle’s whereabouts to the lender or their agents.

- Lender’s Rights: Lenders can and will often use skip tracing techniques, GPS data (if installed and agreed to in your loan contract), and surveillance to locate repossessed vehicles.

The goal should be to temporarily park your car in a secure location, not to outright disappear with it. This guide focuses on legitimate, non-deceptive strategies.

Effective Strategies for Hiding Your Car

When considering how to hide your car from repossession, the key is to place it where it is not easily visible or accessible to repo agents. This requires thought and strategic planning. Here are several methods:

1. Utilize Private Property

The most straightforward and legal approach is to park your car on private property where repossession agents cannot easily access it without permission or a court order. This includes:

- Your Garage: If you have a garage, this is your best bet. Park your car inside and keep the garage door closed. This physically obstructs access and hides the vehicle from view.

- A Friend’s or Family Member’s Property: Ask a trusted friend or family member if you can park your car at their residence. Ensure they have a private driveway or a suitable parking spot, preferably out of public view.

- Business Property (with permission): If you have a close relationship with a business owner, you might be able to arrange parking on their private lot, especially if it’s not heavily trafficked or is secured after hours. Always get explicit permission.

Important Note: Parking on a public street, even in front of your house, is generally not a viable long-term strategy. Repo agents regularly patrol public areas. If the car is visible and accessible, it can be repossessed.

2. Park in an Apartment Complex or Gated Community

If you live in an apartment or a gated community with assigned parking or a resident-only lot, parking your car in your designated spot can provide a layer of security. Residents often know each other’s vehicles, and unauthorized cars can draw attention. Gated communities add an extra barrier for repossession agents.

Caveat: Some apartment complexes or HOAs have towing services for unauthorized vehicles, so parking in your own assigned or permitted spot is crucial. Also, be aware if your car is equipped with a GPS tracker linked to the lender, as this can override location-based security.

3. Utilize Storage Units

A secure storage unit facility can be an excellent place to temporarily store your vehicle. Many facilities offer covered or enclosed units that will completely hide your car. This provides a high level of security and keeps the car out of sight.

Considerations:

- Cost: Renting a storage unit incurs additional monthly expenses.

- Access: Ensure the facility allows vehicle storage and that you can access the unit when needed.

- Security: Choose a facility with good security measures like fencing, lighting, and surveillance.

4. Park in a Less Obvious Location

For short-term needs or if other options are limited, consider parking in a location that is not immediately suspicious but still conceals the vehicle. This could include:

- Behind your house if not visible from the street.

- In a large, rarely visited parking lot (e.g., a remote section of a large mall during off-hours, a community park at an odd time). However, be aware that some private lots have surveillance and towing policies.

- In a dense wooded area on private land (with permission). This is highly dependent on location and accessibility and carries risks of damage from nature.

Risk Assessment: These less conventional methods carry higher risks. Repo agents are skilled at finding vehicles, and abandoning a car in a remote location could make it vulnerable to vandalism, theft, or damage, leading to bigger problems.

5. Alter Appearance Subtly

While you should never tamper with the car’s VIN or plates, a few subtle alterations can sometimes deter immediate identification. Be cautious with these and ensure they are not illegal.

- Cover the Vehicle: A generic car cover can obscure the make and model. Ensure it isn’t overly conspicuous.

- Park with Other Similar Vehicles: If you can park your car amongst many other similar cars (e.g., in a large parking garage), it might be harder to single out initially.

Important Warning: Making the car look abandoned or highly suspicious might attract unwanted attention from law enforcement rather than deterring a repo agent. Stick to simple concealment.

What NOT to Do When Trying to Hide Your Car

It’s just as important to know what actions could backfire or create legal trouble for you. Avoiding these pitfalls is key to protecting yourself and your vehicle.

- Do NOT park on public streets for extended periods. Repo agents frequently patrol these areas, and your car can be easily spotted.

- Do NOT park in your driveway if it’s visible from the street. While it’s private property, if it’s easily accessible and visible, it’s still a target.

- Do NOT disable or tamper with GPS tracking devices. Many modern car loans include GPS trackers. Tampering can violate your loan agreement and give the lender grounds for immediate repossession.

- Do NOT lie to your lender or repo agents. Providing false information can have legal repercussions.

- Do NOT physically block or prevent repossession. Interfering with a repossession agent can lead to arrest and charges.

- Do NOT attempt to hide the car in a way that compromises its safety or attracts attention (e.g., in a hazardous or highly visible but unusual location).

Tools and Resources That Might Help

While the focus is on parking strategies, other resources can aid in managing the situation.

For Understanding Your Loan and Rights:

- Your Loan Agreement: Reread your contract carefully. It will outline terms, conditions, and actions related to default and repossession.

- Lender Communication: Keep a log of all conversations, including dates, times, names, and what was discussed.

- State Consumer Protection Agencies: These agencies can provide information on local laws and consumer rights.

- Legal Aid Societies: If you qualify, they can offer free or low-cost legal advice.

- Credit Counseling Agencies: Reputable non-profit credit counselors can help you create a budget and explore debt management options.

For Securing Your Vehicle (Temporary):

- car cover: A basic, neutral-colored car cover can obscure identification. Ensure it’s secured properly so it doesn’t blow off.

- Storage Unit Rental: Facilities offering vehicle storage.

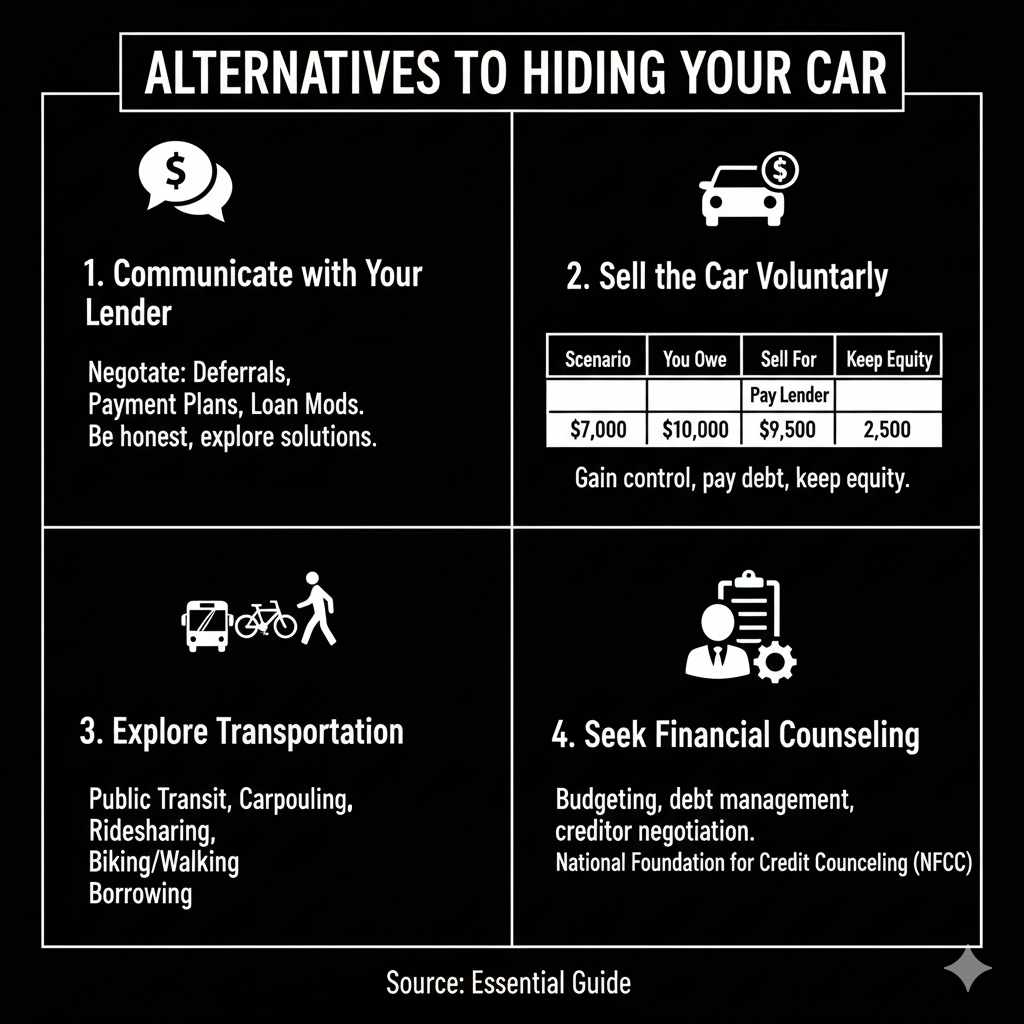

Alternatives to Hiding Your Car

Hiding your car is a temporary measure. The best long-term solution is to address the financial issues that led to the risk of repossession. Here are some proactive alternatives:

1. Communicate with Your Lender

This is by far the most crucial step. Lenders want to get paid and often prefer to work out a solution than go through the costly process of repossession. They might offer:

- Forbearance or Deferment: Temporarily pausing or postponing payments.

- Payment Plan Adjustments: Spreading missed payments over a longer period.

- Loan Modification: Changing the terms of your loan to make payments more manageable.

The sooner you contact them, the more options you are likely to have. Be honest about your situation.

2. Sell the Car Voluntarily

If you owe less than the car is worth, selling it yourself might be a good option. You can use the proceeds to pay off the loan and keep any remaining equity. This gives you control over the sale and ensures you get the best possible price. You can then arrange alternative transportation.

Example Scenario:

| Item | Details |

|---|---|

| Loan Balance | $7,000 |

| Car Market Value | $10,000 |

| Sale Price (estimated) | $9,500 |

| Payment to Lender | $7,000 |

| Equity Remaining | $2,500 |

In this case, selling the car allows you to keep $2,500 and avoid repossession. You would then need to secure other transportation.

3. Explore Transportation Alternatives

If you decide that keeping the car is not feasible, or if you must temporarily remove it from your possession, start planning for alternative transportation. This could include:

- Public Transportation: Buses, trains, subways.

- Carpooling: Arranging rides with colleagues, friends, or family.

- Ridesharing Services: Uber, Lyft, etc. (for essential trips).

- Biking or Walking: For shorter distances.

- Borrowing a Vehicle: From a friend or family member.

4. Seek Financial Counseling

A credit counselor can assess your overall financial situation, help you create a budget, and negotiate with creditors. They can provide strategies for managing debt and improving your financial health, which is crucial for preventing future issues like car repossession.

Organizations like the National Foundation for Credit Counseling (NFCC) offer resources to find accredited counselors.

Frequently Asked Questions (FAQ)

Q1: Can a repo agent tow my car from my garage?

Generally, no. Repossession agents are legally prohibited from breaking into private property, including your garage, or causing damage to do so. They cannot use force or breach personal property boundaries. However, if your car is parked in an accessible driveway, they can tow it.

Q2: What if my car has a GPS tracker?

Many modern car loans include GPS tracking devices. If your car has one, the lender can track its location, which can make hiding it very difficult. Tampering with or disabling these devices is typically a violation of your loan agreement and can lead to immediate repossession.

Q3: How long can I hide my car?

Hiding your car is a temporary measure. It does not resolve the underlying debt. While you might temporarily avoid repossession, it’s essential to use this time to work with your lender or find a permanent solution. Prolonged evasion can lead to more severe actions from the lender.

Q4: Will hiding my car make my repossession shorter?

No, typically the opposite is true. If your car is repossessed, and you had to go to great lengths to hide it, the lender may charge you additional fees for the increased difficulty and time spent locating it. These fees are often added to your outstanding debt.

Q5: What happens after a car is repossessed?

After repossession, the lender will usually sell the car, often at an auction. If the sale price doesn’t cover the remaining loan balance plus any repossession costs, you will likely owe the lender the difference (a deficiency balance). You may also have a grace period to “reinstate” the loan or buy back the car, depending on your loan terms and state laws.

Q6: Can I get my car back if it’s repossessed?

In many cases, yes, you can get your car back. This usually involves paying the full outstanding loan balance, plus allrepo fees and costs, or “reinstating” the loan, which typically means paying the overdue payments plus fees. The exact process and availability depend on your contract and state laws.

Conclusion

Facing potential car repossession is a challenging situation, but understanding your options can make a significant difference. This guide has provided practical, beginner-friendly advice on how to temporarily hide your car from repossession agents, emphasizing legal and ethical considerations throughout. Remember, the aim of these strategies is to buy you time to address the root issue—your loan payments. The most effective and recommended path forward is always open communication with your lender. Explore options like payment plans, loan modifications, or, if necessary, voluntarily selling the car to avoid further financial complications. By taking proactive steps and seeking reliable resources, you can navigate this difficult period with greater confidence and work towards a stable financial future.