Is A 60 Month Car Loan Bad? Essential Guide

A 60-month car loan isn’t inherently “bad,” but it carries risks and considerations. It means lower monthly payments but more interest paid over time and a higher chance of being upside down on your loan. Carefully weighing the pros and cons against your budget and financial goals is key.

So, you’re looking for a car and exploring your financing options. You’ve probably seen deals for 60-month car loans, and maybe you’re wondering if that’s the best way to go. It’s a common question, and honestly, loan terms can feel a bit confusing. Don’t worry, we’re here to break it all down for you in a way that’s easy to understand. We’ll look at what a 60-month loan means for your wallet, whether it’s a smart move for you, and how to make sure you’re getting the best deal possible. Let’s find out if a 60-month car loan “is a 60 month car loan bad” for your next ride!

What Exactly Is a 60-Month Car Loan?

Simply put, a 60-month car loan is a loan you take out to buy a vehicle that you agree to pay back over a period of five years. That’s 60 payments, spread out monthly.

When you finance a car, the total amount you borrow (the car’s price, plus any fees, minus your down payment) is spread out over a set number of months. The lender also tacks on interest, which is how they make money. The longer your loan term, the more interest you’ll generally end up paying, even if your monthly payments seem smaller.

Understanding Car Loan Terms

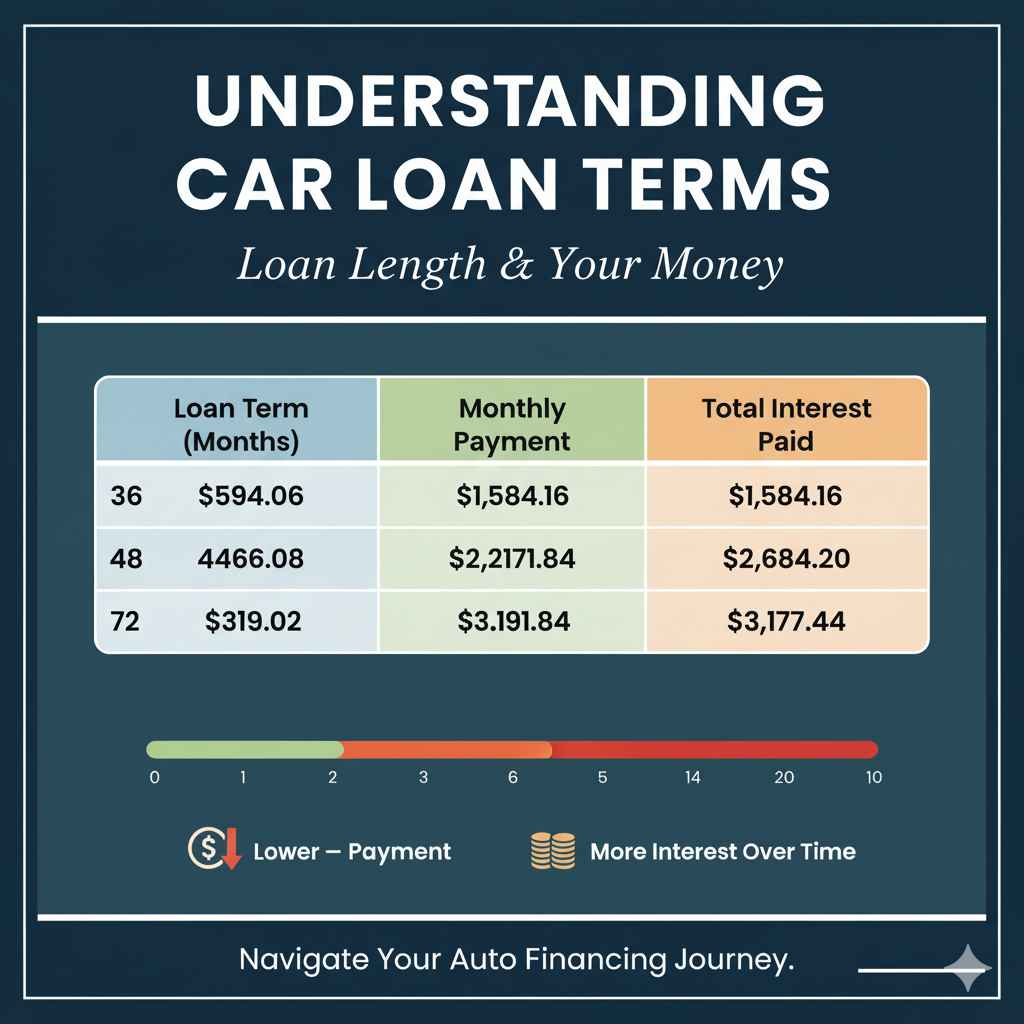

Car loans come in different lengths, often called terms. You might see options for 36 months (3 years), 48 months (4 years), 60 months (5 years), and sometimes even 72 months (6 years) or longer. The term you choose directly impacts how much you pay each month and how much interest you pay over the life of the loan.

Here’s a quick look at how loan terms can affect your payments:

| Loan Term (Months) | Monthly Payment | Total Interest Paid |

|---|---|---|

| 36 | $594.06 | $1,584.16 |

| 48 | $466.08 | $2,171.84 |

| 60 | $378.07 | $2,684.20 |

| 72 | $319.02 | $3,177.44 |

As you can see, the lower monthly payments of a 60-month loan come at the cost of paying more interest over time compared to shorter loan terms. This is an important point to keep in mind when considering your options.

Is a 60-Month Car Loan Bad? The Pros and Cons

The question “is a 60 month car loan bad?” doesn’t have a simple yes or no answer. It really depends on your personal financial situation and goals. Let’s break down the good and not-so-good aspects:

Pros of a 60-Month Car Loan

- Lower Monthly Payments: This is the biggest draw. Spreading the cost of the car over five years means each monthly payment is smaller than it would be with a shorter loan term. This can make a more expensive car or a new car more affordable on a monthly basis, which is great if your budget is tight right now.

- Improved Affordability: For some buyers, a 60-month loan is the only way they can afford the down payment and monthly payments for the car they need. It can open up more vehicle options.

- More Buying Power: With lower monthly payments, you might be able to afford a slightly newer or better-equipped vehicle than you could with a shorter loan term.

Cons of a 60-Month Car Loan

- More Interest Paid Over Time: This is the most significant downside. Because you’re borrowing the money for a longer period, you’ll pay more in total interest. Even a small difference in interest rate can add up over five years. For example, in the table above, you pay over $500 more in interest for a 60-month loan compared to a 48-month loan on the same amount.

- Risk of Being “Upside Down”: “Upside down” means you owe more on the loan than the car is actually worth. Cars depreciate (lose value) the moment they’re driven off the lot. With a longer loan term, your car loses value faster than you pay down the principal loan amount, especially in the early years. If your car is totaled in an accident or you need to sell it early, you might have to pay the difference out of pocket.

- Longer Commitment: You’re committed to making car payments for five years. If your financial situation changes (e.g., job loss, unexpected expenses), a longer loan can be a bigger burden.

- Older Car by the End of the Loan: By the time you’ve made your last payment on a 60-month loan for a new car, the car will be five years old, and it will be that much closer to needing more significant maintenance or repairs.

Who is a 60-Month Car Loan Best For?

A 60-month car loan can be a good option for specific individuals, provided they understand the trade-offs. Here are some scenarios where it might make sense:

People Tight on Monthly Cash Flow

If your priority is to keep your monthly expenses as low as possible, a 60-month loan offers the lowest monthly payment compared to shorter terms for the same price. This can be crucial if you have other significant financial obligations or are just starting out and building your savings.

Buyers of Slightly Older or Used Cars

A 65-72 month loan might be necessary if you’re buying a used car with a higher mileage, as the interest rate might be higher, and the total loan amount could be larger. Some lenders offer longer terms for used cars than others.

Those Planning to Keep Their Car Long-Term

If you’re the type of person who drives a car until it’s well past its prime (say, 10-15 years), then paying a bit more interest over 60 months might not be a dealbreaker. You’re likely to keep the car long enough to pay it off and get plenty of use out of it, minimizing the risk of being upside down when you eventually want to trade it in.

Individuals with Very Strong Credit

If you have an excellent credit score, you’re likely to qualify for the lowest interest rates. This can help mitigate some of the extra interest cost associated with a longer loan term. According to Experian’s State of the Automotive Finance Market report, the average loan term for new cars often hovers around 69 to 70 months, and for used cars, it’s around 66 to 67 months. This indicates a common trend towards longer terms, often facilitated by competitive interest rates for well-qualified buyers.

Buyers Who Will Pay Extra Towards Principal

If you get a 60-month loan but have the discipline to pay a little extra each month, you can significantly reduce the total interest paid and pay off the loan faster. This is a great strategy to get the benefit of lower initial payments while still controlling the total cost.

When to Avoid a 60-Month Loan

Just as there are good reasons to consider a 60-month loan, there are also situations where it’s best to steer clear:

If You Can Afford Shorter Terms

If your budget comfortably allows for 36 or 48-month payments, you’ll save a substantial amount on interest and build equity in your car much faster. This is generally the financially savvier choice.

If You Plan to Trade In Frequently

Drivers who like to get a new car every 2-3 years will almost certainly be upside down on a 60-month loan when it comes time to trade. This means you’ll have to pay that difference out of pocket or roll it into your next loan, trapping you in a cycle of debt.

If You Are Financing an Older or Less Reliable Car

Longer loan terms increase the risk of being upside down. On an older car that’s more prone to needing repairs, this risk is amplified. You don’t want large repair bills piling up on top of a car loan you still owe a lot on.

If the Interest Rate is High

A 60-month loan with a high interest rate is a recipe for paying a massive amount of interest. If you can’t secure a low APR, the extra cost over five years can be significant, making the loan a bad deal.

Tips for Getting the Best Car Loan

No matter the loan term you choose, getting the best possible deal on your car loan is smart. Here’s how:

- Check Your Credit Score: Your credit score is the biggest factor in determining your interest rate. The better your score, the lower the APR you’ll get. You can often check your score for free through your bank or a credit monitoring service. Aim for a score of 700 or above to qualify for the best rates.

- Shop Around for Lenders: Don’t just accept the first loan offer from the dealership. Compare offers from multiple banks, credit unions, and online lenders. Even a small difference in interest rate can save you hundreds or thousands of dollars over the life of a 60-month loan. Use resources like the Consumer Financial Protection Bureau (CFPB) to understand auto loans better.

- Get Pre-Approved: Before you even step onto a car lot, get pre-approved for a loan from your bank or credit union. This gives you a concrete interest rate to compare against dealership offers and strengthens your negotiation position.

- Negotiate the Car’s Price First: Always focus on negotiating the “out the door” price of the car before you discuss financing. Once you agree on the car’s price, then discuss loan terms.

- Consider a Larger Down Payment: A larger down payment reduces the amount you need to borrow. This means lower monthly payments, less interest paid, faster equity building, and a lower chance of being upside down. Aim for at least 20% for a new car and 10% for a used car if possible.

- Pay Extra Towards the Principal: If you have a 60-month loan, try to make extra payments whenever you can. Even an extra $50 or $100 a month can significantly reduce the total interest paid. Make sure to specify that extra payments should go towards the principal.

- Understand All Fees: Be aware of any loan origination fees, late payment fees, or prepayment penalties that might apply.

The Total Cost of Car Ownership

When thinking about a car loan, it’s also important to consider the total cost of owning a car, not just the monthly payment. Beyond the loan, you’ll have expenses like:

- Insurance: This is mandatory and can vary wildly based on your driving record, the car you drive, and where you live.

- Fuel: Gas prices fluctuate, and the fuel efficiency of your car will greatly impact this cost.

- Maintenance: Oil changes, tire rotations, and routine upkeep are essential to keep your car running smoothly.

- Repairs: Unexpected breakdowns can be costly, especially as a car gets older.

- Registration and Taxes: Annual fees to keep your car legally on the road.

A 60-month loan might make a car seem affordable monthly, but if it means sacrificing your ability to save for these other essential costs or an emergency fund, it might not be the best choice. It’s wise to budget for all these things when deciding on a vehicle and loan term.

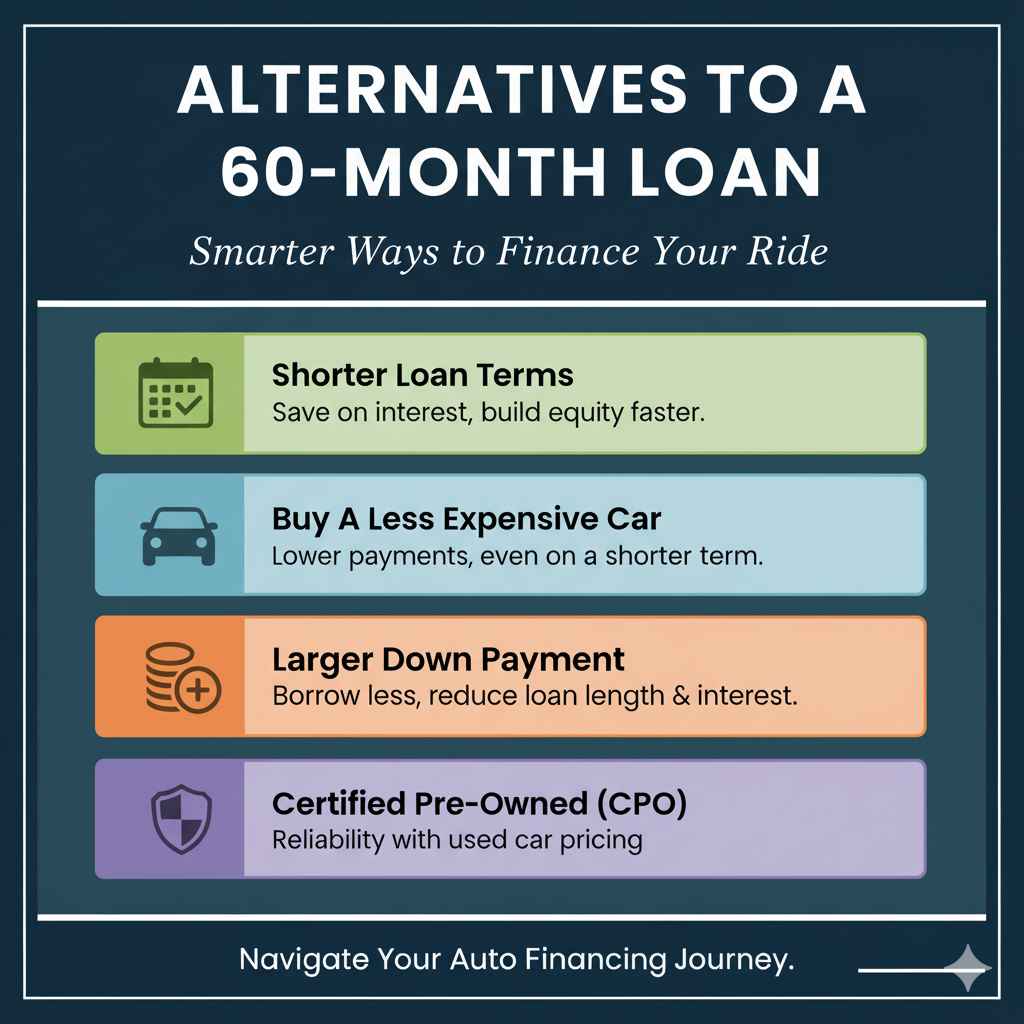

Alternatives to a 60-Month Loan

If a 60-month loan feels a little too long or risky for your situation, consider these alternatives:

- Shorter Loan Terms: As we’ve seen, terms like 36 or 48 months save you money on interest and help you build equity faster.

- Buying a Less Expensive Car: A more affordable car will naturally have lower monthly payments, even on a shorter loan term.

- Saving for a Larger Down Payment: The more you can put down upfront, the less you’ll need to borrow, reducing the loan term and total interest.

- Certified Pre-Owned (CPO) Vehicles: These often come with good warranties and inspection reports, offering a good balance between new car features and used car pricing, sometimes allowing for shorter loan terms.

Frequently Asked Questions About 60-Month Car Loans

Is a 60-month car loan always a bad idea?

No, it’s not always a bad idea. It’s can be a good option if you need lower monthly payments due to budget constraints, but you must understand that you’ll pay more interest, and there’s a higher risk of owing more than the car is worth.

How much more interest will I pay on a 60-month loan?

It depends on the loan amount and interest rate. On a $20,000 loan at 5% APR, a 60-month term costs about $500 more in interest than a 48-month term, and significantly more than a 36-month term.

What is the average car loan term?

The average loan term for new vehicles is typically around 69-70 months, and for used vehicles, it’s around 66-67 months. Many people opt for longer terms to make payments more manageable.

Can I pay off a 60-month loan early?

Yes, most car loans allow you to pay them off early without penalty. Paying extra each month or making a lump sum payment can save you a lot on interest.

What happens if I can’t make my 60-month car payment?

If you miss payments, your lender can repossess your car, severely damage your credit score, and you may still owe money if the car sells for less than you owed.