Minimum Age for Car Insurance Explained

Figuring out when a young driver can get their own car insurance can feel a bit tricky. It’s common for new drivers and their parents to wonder about the rules. Many questions pop up, like “Can I get insurance right when I turn 16?” or “What happens if I don’t have insurance by a certain age?” Don’t worry!

This guide makes the Minimum Age to Get Car Insurance Explained simple and clear. We’ll walk you through everything you need to know, step-by-step, so you can get on the road safely and legally.

Understanding Minimum Age for Car Insurance

The minimum age to get car insurance is a really important topic for new drivers. It’s not about one single number that applies everywhere. Instead, it’s a mix of state laws, insurance company rules, and practical considerations.

For many young people, their 16th birthday might feel like the moment they can drive anywhere, but getting insurance involves more than just having a license. Insurance companies need to assess risk, and younger drivers are generally seen as higher risk. This often means higher premiums and specific requirements.

We’ll break down what this means for you.

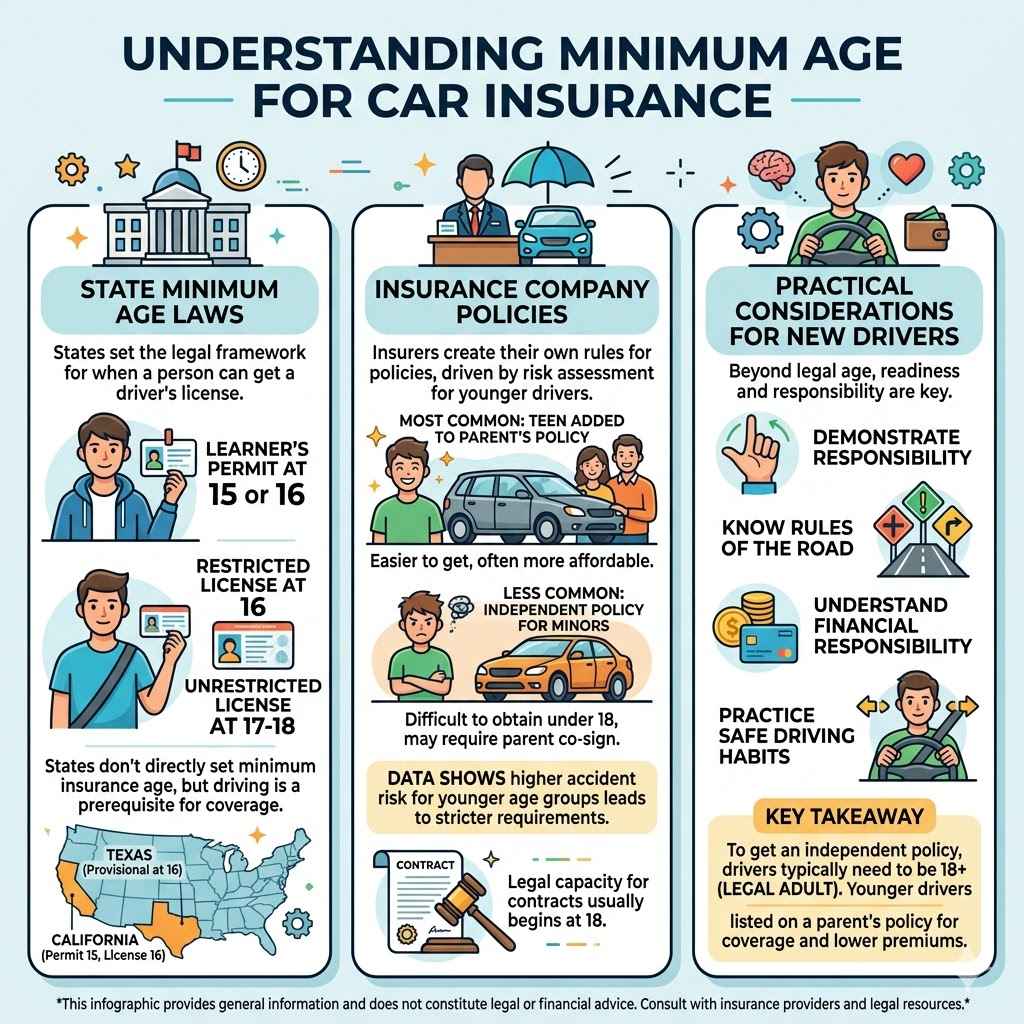

State Minimum Age Laws

Every state has laws about when a person can obtain a driver’s license. This is the first step towards being able to drive a car. However, these state laws do not directly set a minimum age for purchasing car insurance.

Instead, they set the legal framework for who is allowed to operate a vehicle on public roads. For example, some states might allow a learner’s permit at 15 or 16, a restricted license at 16, and an unrestricted license at 17 or 18. The ability to drive legally is a prerequisite for needing insurance, but the insurance itself is governed by different factors.

These state laws are important because they dictate when a person can independently drive. Before a person can be added to a policy or get their own policy, they must be legally permitted to drive. If a state requires a driver to be 16 to get a license, then logically, they cannot get insurance before they are legally allowed to drive.

This creates a baseline for the discussion around the minimum age for car insurance, even if it’s not a direct age limit for the policy itself.

For instance, in Texas, a driver can get a provisional license at 16. This means they can drive alone but with certain restrictions. In California, a driver can get a provisional permit at 15 and a provisional license at 16, also with restrictions.

The age at which these licenses are issued is the starting point for when insurance becomes a necessity and a possibility.

Insurance Company Policies

While states set the driving age, insurance companies have their own rules about when they will issue a policy to a young driver. Most insurance companies will allow a teenager to be added to a parent’s policy as soon as they get their driver’s license. This is often the most common and affordable way for young drivers to get covered.

However, some companies might have their own age thresholds, especially if a young person is trying to get an independent policy.

These company policies are based on their internal risk assessment models. They look at data about accidents, claims, and driving records for different age groups. Younger drivers, especially those under 18, are statistically more likely to be involved in accidents.

Therefore, insurance companies often have stricter requirements or higher rates for this age group. It’s not uncommon for an insurer to require an adult, usually a parent or legal guardian, to co-sign any policy for a driver under 18.

The ability to purchase an independent policy before the age of 18 is rare. This is because insurance contracts are legally binding agreements. Minors, generally considered under 18, may not have the legal capacity to enter into such contracts without adult supervision or consent.

So, even if a 17-year-old has a full license and their own car, they will almost certainly need a parent or guardian to be involved in the insurance process.

Practical Considerations for New Drivers

Beyond legal minimums, there are practical reasons why certain ages are more suitable for getting car insurance. A young driver needs to be responsible and understand the implications of driving. This includes knowing the rules of the road, practicing safe driving habits, and understanding the financial responsibility that comes with owning and operating a vehicle.

Insurance is a major part of that financial responsibility.

For a young person to get their own insurance policy, they typically need to be a legal adult (18 years or older in most places). Before that age, they are usually listed as a driver on a parent or guardian’s policy. This arrangement ensures that there is an adult legally responsible for the policy and any potential claims.

It also often results in lower premiums because the young driver is associated with a more experienced driver’s record.

Consider the scenario where a 16-year-old gets their license and wants to drive the family car. They are not likely to get their own policy. Instead, they will be added to their parents’ auto insurance.

If they buy their own car, the parents would still likely need to be involved in obtaining insurance for that car, especially if the teen is under 18. This practical aspect is key to a smooth and legal driving experience.

Adding a Teen Driver to Your Policy

When a teenager gets their driver’s license, one of the first things parents do is figure out how to get them covered by insurance. The most straightforward way is by adding them to an existing family auto insurance policy. This process is generally simpler than setting up a new, independent policy.

It also often proves to be more cost-effective, as insurance companies tend to offer discounts for multiple vehicles and drivers under one household. We’ll explore how this works and what you need to know.

How to Add a Driver

Adding a young driver to your insurance policy is usually a call or a few clicks away. You’ll need to contact your insurance provider and inform them that your teenager has obtained a driver’s license. They will ask for the teenager’s name, date of birth, and driver’s license number.

The insurance company will then update your policy to include this new driver.

The key information they will need includes the driver’s license number, date of birth, and often details about their driving experience, if any. Your insurer will then determine how this addition affects your premium. It’s important to be upfront and provide accurate information to avoid any issues with coverage later on.

Most insurance companies have dedicated teams or online portals to handle these policy updates.

For instance, if you have a policy with State Farm, you can usually do this by logging into your online account, using their mobile app, or by speaking directly with your agent. They will guide you through the necessary steps to get your new driver officially added to your coverage. The same process generally applies to other major insurers like GEICO, Progressive, or Allstate.

Impact on Premiums

Adding a young, inexperienced driver to your policy will almost always increase your premium. This is because young drivers, particularly teenagers, are statistically at a higher risk of being involved in accidents. Insurance companies price their policies based on risk, and this added risk translates to higher costs.

However, the increase can vary significantly based on several factors.

These factors include the number of vehicles on the policy, the type of coverage you have, the driving record of the young driver (if they’ve had any previous permits or supervised driving experience), and the location where the vehicle is primarily garaged. Good student discounts, driver’s education discounts, and defensive driving course discounts can sometimes help offset the increased cost.

Let’s consider a sample scenario: A family’s annual premium for two cars and two adult drivers might be $2,000. Upon adding a 16-year-old licensed driver, the premium could increase by anywhere from 30% to 80%, potentially raising it to $2,600-$3,600 or more, depending on the insurer and other factors. This highlights the significant financial impact of adding a young driver.

Coverage Options for Teen Drivers

When adding a teen driver, you’ll need to decide what level of coverage is appropriate. Generally, you’ll extend your existing coverage levels to them. This typically includes liability coverage (bodily injury and property damage), which pays for damages you cause to others if you’re at fault in an accident.

Comprehensive and collision coverage, which pay for damage to your vehicle, are also often included.

It’s important to review your policy details carefully. You want to ensure that your teen driver has adequate protection. If they will be driving a car that is financed or leased, comprehensive and collision coverage will likely be required by the lender or leasing company.

Even if they drive an older car that you own outright, these coverages can be valuable to protect your investment.

For example, if your teen driver is involved in an accident and causes significant damage to another vehicle or injures someone, the liability coverage on your policy will help pay for those costs. Without sufficient liability coverage, you could be held personally responsible for damages exceeding your policy limits, which could have severe financial consequences. Therefore, ensuring robust coverage for your teen is a wise decision.

Independent Car Insurance Policies

While most young drivers start on a parent’s policy, some may eventually seek to obtain their own independent car insurance. This usually happens when a young person moves out on their own, purchases a car solely in their name, or simply prefers to manage their own insurance. However, getting an independent policy before the age of 18 is very uncommon due to legal contractual limitations.

The process and considerations differ significantly from being a listed driver on a family policy.

Eligibility for Independent Policies

Generally, an individual must be a legal adult, typically 18 years or older, to enter into a legally binding contract for an independent car insurance policy. Insurance companies require the policyholder to have the legal capacity to sign contracts, pay premiums, and be held responsible for the terms of the policy. For individuals under 18, this legal capacity is usually lacking.

Therefore, a 16-year-old or 17-year-old with a valid driver’s license will almost always need a parent or legal guardian to co-sign their policy or be listed as a primary insured on a household policy. If a young adult turns 18, they can then explore getting their own policy, often by setting up a new policy entirely, rather than just being added to a parent’s. This involves a more thorough underwriting process by the insurance company.

Consider a 19-year-old who has moved to a different city for college and bought their own car. They would likely need to obtain an independent insurance policy in their name. They would need to shop around for quotes from various insurance companies, providing details about their driving history, the vehicle they own, and their address.

This is a distinct process from being a named driver on their parents’ policy.

Factors Affecting Premiums for Young Adults

For young adults (18-25 years old) seeking independent policies, premiums are typically much higher compared to older, more experienced drivers. This is primarily due to statistical data indicating a higher likelihood of accidents and claims within this age group. Several factors influence these premiums:

Driving Record: A clean driving record with no accidents or traffic violations is crucial. Any past incidents will significantly increase premiums. For example, a speeding ticket could add hundreds of dollars to an annual premium.

Vehicle Type: The make, model, safety features, and cost of repair for the vehicle all impact insurance rates. Sports cars or vehicles with high theft rates are more expensive to insure. A sensible sedan like a Toyota Camry will usually cost less to insure than a Ford Mustang.

Location: Where the car is garaged plays a big role. Urban areas with higher rates of theft, vandalism, and accidents often have higher insurance costs than rural areas. Premiums in New York City will generally be higher than in a small town in Nebraska.

Coverage Levels: The amount of coverage chosen (liability limits, deductibles for comprehensive and collision) directly affects the premium. Higher coverage limits and lower deductibles mean higher costs.

Credit Score: In many states, insurance companies use credit-based insurance scores to help determine premiums. A lower credit score can lead to higher insurance rates.

For instance, a 20-year-old male in Chicago driving a 2020 Honda Civic, with no prior accidents, might pay upwards of $3,000-$4,000 annually for a full coverage independent policy. The same driver in a rural area with a clean record driving a less expensive car might pay closer to $1,500-$2,000. The difference is substantial and driven by these influencing factors.

Shopping for Independent Policies

When a young adult is ready for their own policy, shopping around is essential to find the best rates and coverage. They should gather necessary information, including their driver’s license, vehicle information (VIN, make, model, year), and details about their driving history. They will then need to get quotes from multiple insurance companies.

It’s important to compare quotes apples-to-apples, ensuring that the coverage levels, deductibles, and policy limits are the same for each quote. This allows for a true comparison of pricing. Young adults should also inquire about any discounts they might be eligible for.

These can include good student discounts (if still in school), discounts for completing defensive driving courses, or discounts for installing anti-theft devices.

A realistic scenario involves a 22-year-old recent graduate who has just moved into their own apartment. They need insurance for their car. They could get quotes from GEICO, Progressive, Allstate, and USAA (if eligible).

By comparing quotes, they might find that one company offers a better rate for the same coverage, perhaps due to a specific discount they qualify for or a more favorable risk assessment for that demographic in that particular area. This diligent shopping can save them hundreds of dollars annually.

When Can You Legally Drive and Insure a Car?

The ability to legally drive a car and the ability to insure a car are closely linked but not always the same age. The legal driving age is determined by state laws, which set minimum ages for obtaining learner’s permits, provisional licenses, and full driver’s licenses. The minimum age to get car insurance is more nuanced, involving both these legal driving ages and insurance company policies.

Learner’s Permits and Supervised Driving

Most states allow individuals to obtain a learner’s permit at age 15 or 16. This permit allows them to drive a vehicle but only when accompanied by a licensed adult, usually over the age of 21 or 25, seated in the front passenger seat. During this supervised driving period, the learner is covered by the supervising adult’s auto insurance policy.

This is a critical phase where the new driver gains essential experience. The insurance coverage during this time is provided through the existing policy of the adult supervising them. It’s crucial for the supervising adult to ensure their policy is up-to-date and has adequate liability coverage.

The learner is essentially an extension of the policyholder while under supervision. This allows them to practice safely and legally before obtaining a full license.

For example, a 15-year-old in Pennsylvania can get a learner’s permit. While driving with their parent or guardian, they are covered under the parent’s auto insurance. This ensures that if an accident occurs during this supervised practice, there is insurance protection in place.

The permit holder is not getting their own insurance; they are covered by someone else’s policy.

Provisional and Restricted Licenses

Once a driver reaches a certain age, typically 16 or 17, they may be eligible for a provisional or restricted driver’s license. These licenses allow young drivers to drive independently but often come with limitations, such as restrictions on nighttime driving, the number of passengers allowed, or the types of roads they can use. At this stage, the young driver is usually added as a named insured to a parent’s or guardian’s policy.

Adding a teen with a provisional license to a policy is a standard practice. The insurance company is aware that this driver now operates a vehicle on their own, albeit with some restrictions. The premium will reflect this increased risk compared to a learner’s permit holder who is always supervised.

The legal ability to drive without constant adult supervision triggers the need for this formal addition to an insurance policy.

In California, a 16-year-old can obtain a provisional driver’s license after holding a permit for at least six months and completing a driver education program. This allows them to drive alone but with restrictions on driving between 11 p.m. and 5 a.m.

and carrying passengers under 20 without an adult present. They would be added to their parents’ insurance policy at this point.

Full Unrestricted Licenses

The age at which a driver can obtain a full, unrestricted driver’s license varies by state, often being 17 or 18. Once a driver has this unrestricted license, they have the full privileges of operating a vehicle without the limitations associated with provisional licenses. If they are still living at home and driving a family car, they will remain on the parents’ policy.

If they are living independently and own their own car, they can then pursue an independent insurance policy.

The transition to an unrestricted license signifies a greater level of independence and responsibility. For insurance purposes, while they are still considered young drivers and premiums will be high, they meet the legal and contractual requirements to hold their own policy. This is the point where the Minimum Age to Get Car Insurance Explained truly comes into play for independent adult drivers.

For instance, an 18-year-old in New York can obtain an unrestricted junior license. If this individual has their own car and lives apart from their parents, they can now legally contract for their own insurance. They would shop for policies in their name, with rates influenced by their age, driving history, vehicle, and location.

This marks a significant step towards full adult responsibility on the road.

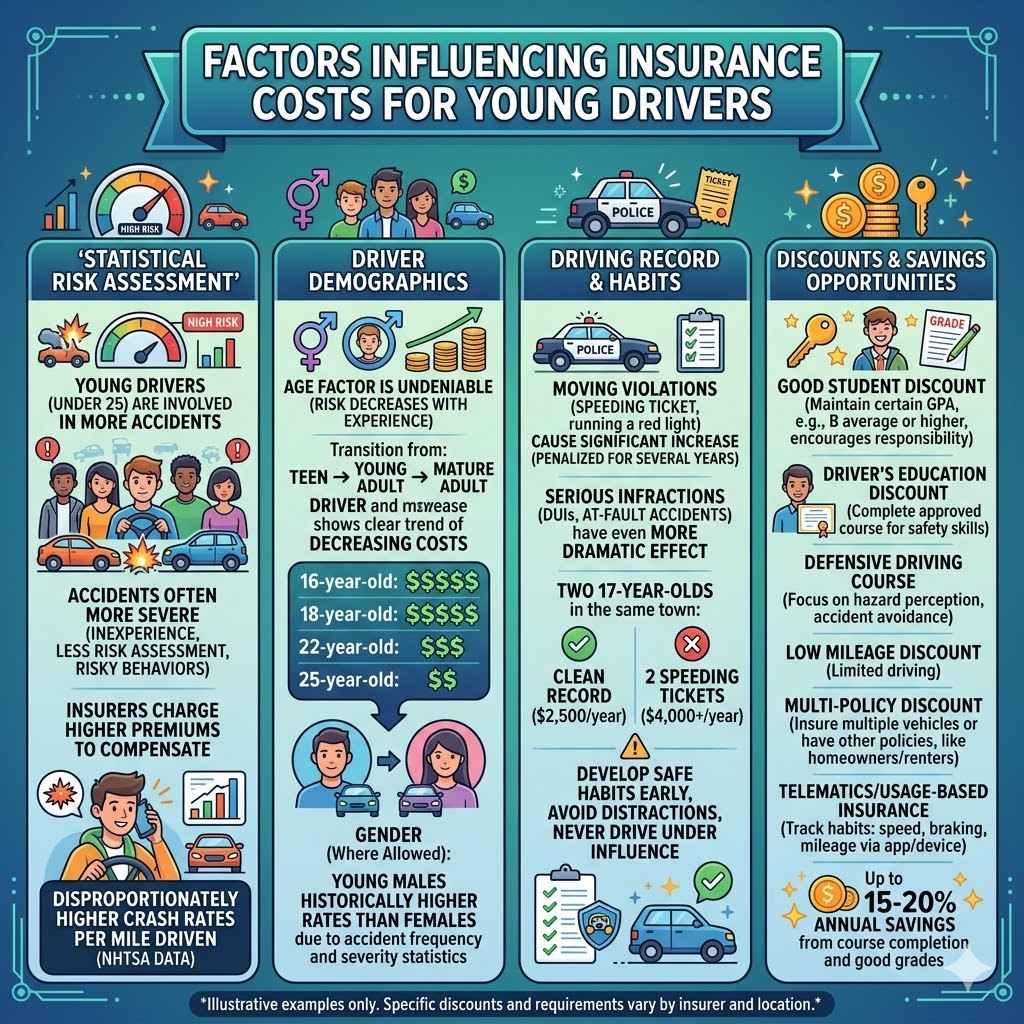

Factors Influencing Insurance Costs for Young Drivers

The cost of car insurance for young drivers is significantly higher than for older, more experienced drivers. This premium difference is rooted in statistical data that highlights a greater risk associated with younger individuals behind the wheel. Several key factors contribute to these elevated costs, and understanding them can help young drivers and their families make informed decisions.

Statistical Risk Assessment

Insurance companies use extensive data to assess risk. Studies consistently show that drivers under the age of 25, and especially teenagers, are involved in more car accidents. These accidents are often more severe due to inexperience, less developed risk assessment skills, and a higher propensity for risky behaviors.

This statistical reality means that insurers charge higher premiums to compensate for the increased likelihood and potential cost of claims from this demographic.

For example, the National Highway Traffic Safety Administration (NHTSA) data often shows that young drivers have disproportionately higher crash rates per mile driven. While this can vary by age and gender, the general trend is clear: younger drivers are a higher risk. Insurance companies use these statistics to calculate the base rates for different age groups before applying other individual factors.

In 2021, drivers aged 16-19 were involved in a significant percentage of fatal crashes, despite making up a smaller portion of the overall driving population. This statistic underscores the elevated risk factor that insurance companies consider. Therefore, it is not surprising that insurance premiums reflect this reality.

Driver Demographics

Certain demographic factors, such as age and gender, play a role in how insurance companies calculate premiums for young drivers. Historically, young male drivers have been charged higher rates than young female drivers because statistics have shown them to be involved in more serious and frequent accidents. However, some states have begun to limit or prohibit the use of gender in determining insurance rates due to fairness concerns.

Regardless of gender-based pricing, the age factor itself is undeniable. The risk associated with a 16-year-old driver is generally higher than that of a 22-year-old, even with similar driving records. As drivers get older and accumulate more experience, the statistical risk decreases, leading to lower premiums.

The transition from teen to young adult and then to mature adult driver shows a clear trend of decreasing insurance costs.

Consider this: a 16-year-old male might face a higher premium than a 16-year-old female in states where gender is still a pricing factor. However, both will likely pay substantially more than an 18-year-old, who in turn will pay more than a 25-year-old. The impact of age on insurance cost is profound and gradual.

Driving Record and Habits

A young driver’s driving record is arguably one of the most critical factors influencing their insurance costs. Even a single moving violation, such as a speeding ticket or a citation for running a red light, can cause a significant increase in premiums for several years. More serious infractions, like DUIs or at-fault accidents, will have an even more dramatic and lasting effect.

Insurance companies offer discounts for good driving records. Conversely, they penalize drivers with a history of violations. Developing safe driving habits early on, such as obeying speed limits, avoiding distractions, and never driving under the influence, is crucial not only for safety but also for keeping insurance costs manageable.

Practicing defensive driving techniques can also help mitigate risks and potentially lead to discounts.

A sample scenario could involve two 17-year-old drivers living in the same town, driving similar cars. One has a clean record, while the other has received two speeding tickets in the past year. The driver with the clean record might pay $2,500 annually for insurance, while the one with tickets could see their premium jump to $4,000 or more.

This illustrates the direct financial consequence of poor driving habits.

Discounts and Savings Opportunities

Fortunately, there are several ways young drivers and their families can work to reduce car insurance costs. Insurance companies offer various discounts that can make coverage more affordable:

Good Student Discount: Many insurers offer discounts to high school or college students who maintain a certain GPA (often a B average or higher). This encourages academic achievement and assumes that responsible students are also responsible drivers.

Driver’s Education Discount: Completing an approved driver’s education course can often qualify a young driver for a discount. These courses teach valuable safety skills and road awareness.

Defensive Driving Course: Taking and passing a state-approved defensive driving course can sometimes lead to a discount. These courses focus on hazard perception and accident avoidance techniques.

Low Mileage Discount: If a young driver doesn’t drive very often (e.g., only drives to school on days when public transport isn’t available, or their car is rarely used), they may qualify for a discount based on limited mileage.

Multi-Policy Discount: Insuring multiple vehicles or having other policies with the same insurance company (like homeowners or renters insurance) can often result in discounts.

Telematics/Usage-Based Insurance: Some companies offer programs where a device or app tracks driving habits (speed, braking, mileage, time of day). Safe driving can lead to significant discounts.

For example, a family might find that by having their 17-year-old complete a recognized defensive driving course and maintaining a B average in school, they can shave off up to 15-20% from the annual premium increase associated with adding the teen. This saving could amount to several hundred dollars per year, making a noticeable difference in overall insurance costs.

Frequently Asked Questions

Question: What is the absolute minimum age to get car insurance?

Answer: There isn’t a single, universal minimum age. It depends on state laws for driving and insurance company policies. Generally, you must be a legal adult (usually 18) to get an independent policy, but you can be added to a parent’s policy as soon as you get your driver’s license, often at 16.

Question: Can a 16-year-old get their own car insurance policy?

Answer: In most cases, no. A 16-year-old typically cannot enter into a legal contract for their own insurance policy. They will usually be added to a parent or guardian’s policy until they reach the age of 18.

Question: Does a learner’s permit count for insurance?

Answer: Yes, when you have a learner’s permit and are driving supervised, you are covered by the insurance policy of the adult supervising you.

Question: How does adding a teen driver affect car insurance costs?

Answer: Adding a teen driver almost always increases insurance costs because they are statistically seen as higher risk. The increase depends on the insurer, the teen’s record, and the coverage chosen.

Question: Are there ways to make car insurance cheaper for young drivers?

Answer: Yes, several discounts can help. These include good student discounts, driver’s education completion, defensive driving courses, and sometimes usage-based insurance programs that monitor safe driving habits.

Summary

The minimum age to get car insurance isn’t a fixed number but rather a combination of state driving laws and insurance company rules. You can usually be added to a parent’s policy as soon as you get your driver’s license, often around age 16. To have your own independent policy, you generally need to be 18.

Shopping around, asking for discounts, and maintaining a good driving record are key to managing costs.