Cash vs Financing Cars What Men Miss

Figuring out how to pay for a car can feel tricky. Many folks wonder if buying with cash is better than getting a loan. This is a common question, and What Most Men Get Wrong About Cash vs Financing Cars is something many people struggle with.

It’s easy to get confused by all the numbers and options. But don’t worry! This guide breaks it down simply.

We’ll walk through each step so you can make the best choice for your wallet. Let’s get started and clear things up.

Cash vs Financing Cars Making the Smart Choice

Deciding whether to pay cash or finance a car purchase is a big financial decision. Many people jump into this without fully thinking it through, leading to mistakes that can cost them money. This section looks at why this choice is so important and what people often overlook.

Understanding the pros and cons of each method will help you avoid common pitfalls. It’s about looking beyond just the monthly payment to see the whole financial picture. We will explore the core differences and why they matter for your budget.

The Allure of Paying Cash

Paying cash for a car means you own it outright from day one. There are no monthly loan payments hanging over your head. This can bring a great sense of financial freedom and peace of mind.

You avoid paying any interest, which can add up to thousands of dollars on a car loan. Also, your credit score isn’t directly involved in the purchase itself, so there’s no risk of damaging it by missing payments.

When you pay cash, the car is yours free and clear. This means you don’t have to worry about repossession if you hit a rough patch financially. It’s a straightforward transaction.

The price you agree on is the total you pay for the vehicle. This simplicity is very appealing to many car buyers.

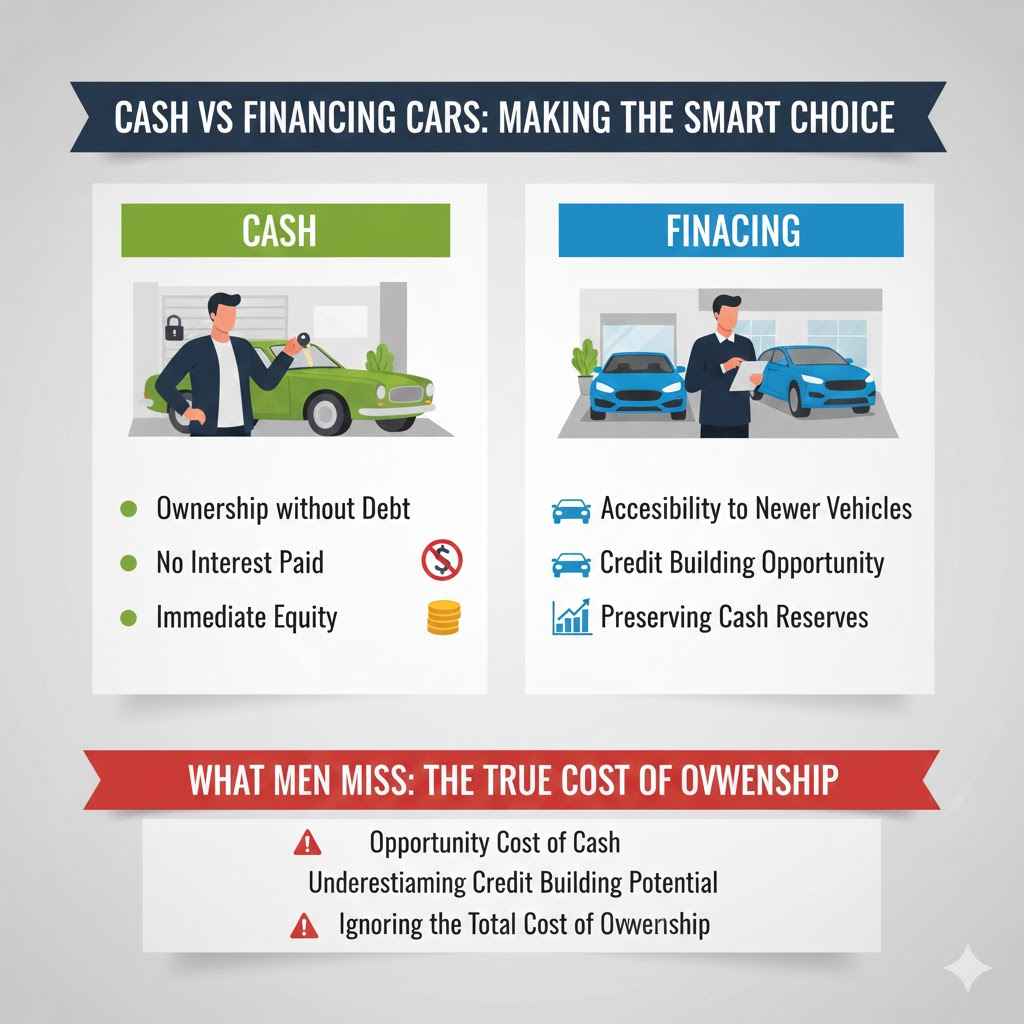

Ownership without Debt: Owning a car outright means you are completely free from any car loan obligations. This can feel very liberating and remove a significant monthly expense from your budget. It allows you to redirect funds you would have spent on payments towards other financial goals, like savings or investments. The feeling of not owing anyone for your vehicle is a powerful motivator for many people.

No Interest Paid: The biggest financial advantage of paying cash is avoiding interest charges. Car loans typically come with interest rates that can increase the total cost of the car significantly over the life of the loan. By paying cash, you pay only the sticker price, saving potentially thousands of dollars that would have gone to the lender. This makes the car truly yours without any hidden financial costs over time.

Immediate Equity: When you pay cash, you immediately have equity in your vehicle. This means the car’s value is entirely yours. If you decide to sell it later, the entire sale price is profit. This is different from financing, where a portion of your payment goes towards interest, and you might owe more than the car is worth in the early stages of the loan, a situation known as being upside down.

The Case for Financing a Car

Financing a car allows you to drive a new vehicle without needing the full purchase price upfront. This is especially helpful if you need a car now but don’t have a large sum of cash available. Auto loans often come with competitive interest rates, and making timely payments can actually help build or improve your credit history.

This can be beneficial for future loans like mortgages.

Financing also spreads the cost over several years. This makes the monthly payments more manageable than trying to save the entire amount. You can often afford a more reliable or newer model when you finance.

It also frees up your cash for other important things like emergency funds or investments. The key is to find a loan with a good interest rate and affordable monthly payments.

Accessibility to Newer Vehicles: Financing makes it possible to afford newer, more reliable cars that you might not be able to buy with cash. This can mean access to better safety features, improved fuel efficiency, and modern technology. For families or individuals who rely heavily on their vehicle, this access can be invaluable, offering peace of mind and better performance.

Credit Building Opportunity: Making consistent, on-time payments for an auto loan can significantly boost your credit score. A good credit score is essential for many financial milestones, such as getting approved for a mortgage, securing lower insurance rates, or even renting an apartment. This can be a strategic financial move for those looking to improve their financial standing.

Preserving Cash Reserves: Financing allows you to keep your savings intact. This is crucial for maintaining an emergency fund to cover unexpected expenses like medical bills or job loss. It also means you can invest your cash in assets that might yield a higher return than the interest rate on your car loan. This financial flexibility can be a smart strategy for overall financial health.

Common Misconceptions and What Men Often Miss

A significant number of people, often men, tend to focus too much on the immediate ownership aspect of paying cash. They might overlook the long-term financial implications or the opportunity cost of tying up a large sum of money. This is a key area where What Most Men Get Wrong About Cash vs Financing Cars becomes apparent.

The idea of “owning it outright” can be so strong that they don’t consider if financing could actually be the more financially astute decision in the long run. This might involve missing out on better investment returns or not building credit history.

Another common oversight is underestimating the power of good credit. Some may believe that if they have the cash, credit history doesn’t matter. However, building a solid credit profile through responsible loan management can lead to significant savings on future borrowing, such as mortgages or other large purchases.

This missed opportunity to leverage credit can be a costly mistake.

Opportunity Cost of Cash: Many focus only on the total price of the car and the fact that paying cash means no interest. They fail to consider what else that money could be doing. Investing that large sum in stocks, bonds, or other ventures could potentially yield returns that far exceed the interest they would have paid on a car loan. This missed growth is a major oversight.

Underestimating Credit Building Potential: Some believe that having cash negates the need to build credit. This is a mistake. Responsible use of an auto loan, with timely payments, is one of the simplest ways to establish or improve a credit score. A strong credit score can lead to lower interest rates on mortgages, credit cards, and other important loans in the future, saving much more money than the car loan itself.

Ignoring the Total Cost of Ownership: Beyond the purchase price, people sometimes forget about insurance, maintenance, and depreciation. While paying cash avoids loan interest, it doesn’t eliminate these other costs. Financing might allow for a newer, more fuel-efficient car that has lower running costs, potentially offsetting some of the interest paid. The total picture matters.

Exploring the Financial Mechanics Cash vs. Financing

This section delves into the nuts and bolts of how cash purchases and car financing actually work from a financial perspective. We’ll break down the numbers involved, looking at interest rates, depreciation, and how each payment method impacts your overall wealth. Understanding these mechanics is key to making an informed decision that benefits your personal finances in the long term.

It’s about more than just the sticker price; it’s about the financial journey of owning a car.

The True Cost of Paying Cash

When you pay cash for a car, the immediate cost is straightforward: the agreed-upon purchase price. However, the “true” cost involves more than just that number. The biggest factor is the opportunity cost.

If you have $30,000 in savings and use it all to buy a car, that $30,000 is no longer earning interest in a savings account or potentially growing in the stock market. This lost potential return is a significant, though often unseen, cost of paying cash.

For instance, if that $30,000 could have earned an average of 5% per year in an investment, over five years, that’s $7,500 in potential earnings lost. While this is a simplified example, it illustrates the concept. Also, while you avoid loan interest, the car still depreciates in value.

You bear the full brunt of this depreciation immediately as your cash is tied up in a depreciating asset.

Depreciation and Cash Purchases

Depreciation is the decrease in a car’s value over time. When you pay cash, you feel the impact of depreciation directly. The moment you drive off the lot, the car is worth less than what you paid.

If you bought a car for $25,000 cash and it depreciates by 20% in the first year, its value drops by $5,000. You’ve spent $25,000 of your hard-earned money, and your asset is now worth only $20,000.

This is a sunk cost – money you’ve spent that you can’t get back. While all cars depreciate, paying cash means your entire purchase price is subject to this loss from day one. If you had financed, a portion of your payments would be going towards interest, but the depreciation impact on your cash outflow would be spread over time.

It’s a different way of feeling the pinch of value loss.

The Power of Investing Your Cash Instead

Imagine you have $20,000 cash to buy a car. If you choose to finance with a loan that has a 4% interest rate, your monthly payments might be manageable. That $20,000 cash could be invested.

Let’s say it’s invested in a diversified stock market index fund that historically returns an average of 8% per year. After five years, that $20,000 could grow to over $29,000.

Meanwhile, your car loan payments are fixed. The interest paid on the loan might be around $2,000-$3,000 over five years. In this scenario, you’ve used your cash to potentially gain around $9,000, while only paying a few thousand in interest for the car.

This makes financing the more financially rewarding choice in this example. The key is earning more on your investment than you pay in loan interest.

Understanding Financing Terms and Interest Rates

When you finance a car, you agree to a loan with a specific principal amount, an interest rate, and a repayment term (the number of months you’ll make payments). The interest rate is arguably the most critical component. It’s expressed as an annual percentage rate (APR).

A lower APR means you pay less in interest over the life of the loan.

Loan terms can vary, typically from 36 months (3 years) to 72 months (6 years) or even longer. A shorter term means higher monthly payments but less total interest paid. A longer term means lower monthly payments but significantly more interest paid overall.

It’s a trade-off between immediate affordability and long-term cost.

Annual Percentage Rate APR Explained

The Annual Percentage Rate, or APR, is the yearly cost of borrowing money, including fees. For car loans, it’s the primary figure you’ll see advertised. A 3% APR is much better than a 7% APR.

Even a small difference in APR can add up to thousands of dollars over the life of a car loan. For example, a $25,000 loan at 4% APR for 60 months will have a total interest cost of about $2,600.

The same $25,000 loan at 8% APR for 60 months would cost around $5,400 in interest. That’s an extra $2,800! Lenders calculate your APR based on your credit score, the loan term, the car’s age and value, and market conditions.

Always compare APRs from multiple lenders to ensure you’re getting the best deal. Don’t just look at the monthly payment; look at the APR and the total amount financed.

Loan Term Lengths and Total Interest Paid

The length of your loan term directly impacts how much you pay in interest. A shorter term means your monthly payments are higher, but you pay off the loan faster and therefore pay less interest in total. A longer term reduces your monthly payments, making the car more affordable on a month-to-month basis.

However, you end up paying more interest over the entire duration of the loan.

Let’s look at a $20,000 loan at 5% APR:

| Loan Term (Months) | Monthly Payment | Total Interest Paid | Total Cost |

|---|---|---|---|

| 36 | $594.13 | $1,588.68 | $21,588.68 |

| 48 | $466.21 | $2,188.08 | $22,188.08 |

| 60 | $377.88 | $2,672.80 | $22,672.80 |

| 72 | $318.03 | $3,178.16 | $23,178.16 |

As you can see, extending the loan term by 36 months (from 36 to 72) increases the total interest paid by over $1,500. This highlights why shorter terms are generally better if your budget allows.

The Impact on Your Credit Score

Choosing to finance a car can have a significant positive impact on your credit score, provided you make your payments on time. An auto loan is a form of installment credit, which is a key factor in credit scoring. Regularly paying down the loan demonstrates to credit bureaus that you are a responsible borrower.

However, if you miss payments or default on the loan, it can severely damage your credit score. This can make it harder and more expensive to borrow money for other things in the future, like a house or even other loans. Therefore, careful consideration of your ability to make monthly payments is paramount.

Building Credit Through Auto Loans

For individuals looking to establish or improve their credit history, an auto loan can be an excellent tool. When you secure financing and consistently make your monthly payments on time, this positive payment history is reported to the major credit bureaus (Equifax, Experian, and TransUnion). This builds a track record of responsible credit management.

For example, someone with no credit history might take out an auto loan. After making 24 on-time payments, their credit report will show this positive activity, gradually increasing their credit score. This can open doors to better credit card offers, lower interest rates on future loans, and generally improve their financial profile.

It’s a tangible way to prove creditworthiness.

Risks of Financing for Credit

While financing can build credit, it also carries risks if not managed properly. Late payments are reported to credit bureaus and can drastically lower your credit score. A single late payment can have a negative impact, and multiple late payments can be devastating.

This makes it harder to get approved for loans or credit cards in the future, and you may face higher interest rates.

Defaulting on the loan, meaning failing to make payments for an extended period, can lead to the lender repossessing the car. This severe negative mark on your credit report can stay with you for seven years or more, making future borrowing very challenging and expensive. It’s crucial to only finance if you are confident you can manage the monthly payments.

Real-Life Scenarios and Practical Advice

Understanding the theory behind cash versus financing is one thing, but seeing how it plays out in real life can make it much clearer. This section uses examples to illustrate the financial outcomes of different choices. We’ll look at a few scenarios to help you apply this knowledge to your own situation and make the best decision for your financial future.

Scenario 1 The Saver vs. The Investor

Meet Alex and Ben, both looking to buy a $25,000 car. They have the same financial situation otherwise: good jobs and a stable income.

Alex: The Saver

Alex has $25,000 saved and decides to pay cash for the car. He wants the peace of mind of owning it outright and avoids any loan interest. Alex puts the full $25,000 into his car.

His cash savings are now depleted.

Ben: The Investor

Ben also has $25,000 saved. He decides to finance the car. He puts down $5,000 and finances the remaining $20,000 at a 4% APR for 60 months.

His monthly payment is about $377.88. Ben keeps his remaining $20,000 in a diversified investment account that he expects to grow at an average of 7% annually.

After five years:

Alex has a $25,000 car (now worth less due to depreciation, let’s say $15,000) and no cash savings from his original car fund. He paid $25,000 upfront.

Ben has paid about $2,673 in interest for his car loan. His car is also worth about $15,000. However, his initial $20,000 investment has grown to approximately $28,142 (assuming a 7% annual return compounded). So, he has gained about $8,142 from his investment while also having the car.

In this scenario, Ben, the investor, is financially ahead by over $8,000 compared to Alex, the saver, after accounting for the car’s value and investment gains versus loan interest. This shows how the opportunity cost of cash can be significant.

Scenario 2 Building Credit with a Modest Loan

Sarah is a young professional with a limited credit history. She needs a reliable car and wants to improve her credit score.

She finds a car for $18,000. She has $5,000 saved for a down payment and decides to finance the remaining $13,000.

She secures a loan with a 6% APR for 60 months. Her monthly payments are around $253.

Over the next five years:

Sarah makes all her payments on time. Her credit score, which was in the mid-600s, steadily increases.

By the end of the loan term, her credit score is in the high 700s.

She has paid approximately $2,180 in interest for the car loan.

Sarah’s decision to finance, despite having enough cash to buy the car outright, served her goal of building credit. The increased credit score she achieved will likely save her more money in the long run when she needs to take out a mortgage or other loans. She wisely chose a loan term and payment she could comfortably afford.

Advice for Navigating Your Decision

Here’s some practical advice to help you make the best choice for your car purchase:

Calculate the Opportunity Cost: If you’re considering paying cash, ask yourself what else you could do with that money. Could investing it earn you more than the interest you’d pay on a loan? Use online calculators to compare potential investment returns with loan interest costs. Don’t just think about what you save in interest; think about what you could gain elsewhere.

Shop for Loans Before Visiting Dealerships: Get pre-approved for an auto loan from your bank, credit union, or online lenders before you even start looking at cars. This gives you a benchmark for the interest rate you should be aiming for and strengthens your negotiation position. Dealerships often mark up interest rates, so knowing your pre-approved rate is crucial.

Understand All Fees and Charges: When financing, read all loan documents carefully. Understand not just the APR but also any origination fees, late fees, or prepayment penalties. Some loans allow you to pay them off early without penalty, which is ideal if you want to accelerate your payments. Clarity on all costs is essential for avoiding surprises.

Consider Your Financial Goals: Is your priority to be debt-free, or is it to grow your wealth and improve your credit score? If being debt-free is paramount, and you have the cash, paying in full makes sense. If growing wealth and improving credit are more important, financing with a low APR might be the better strategy, especially if you have an investment plan for your cash.

What Most Men Get Wrong About Cash vs Financing Cars Final Thoughts

Many people focus solely on avoiding loan interest when buying a car. They miss that financing can build credit and that invested cash can grow more than loan interest costs. Making an informed choice requires looking at the whole financial picture, not just immediate ownership.

Frequently Asked Questions

Question: Is it always better to pay cash for a car

Answer: Not always. While paying cash avoids interest, financing can help build your credit score, and investing your cash could potentially earn more than the loan interest. It depends on your financial goals and ability to invest or manage credit responsibly.

Question: How much should I put down on a car loan

Answer: Putting down a larger down payment reduces the amount you need to finance, leading to lower monthly payments and less interest paid. A common recommendation is at least 10-20%, but more is always better if it doesn’t deplete your emergency fund.

Question: Can financing a car hurt my credit score

Answer: Yes, if you miss payments or default. However, making all your payments on time can significantly improve your credit score. It’s a tool that can be used for good or ill depending on how you manage it.

Question: What is a good APR for a car loan

Answer: A “good” APR varies with market conditions and your creditworthiness, but generally, lower is better. Rates below 5% are considered very good for qualified buyers, while rates above 8% might be considered high.

Question: Should I use my savings to pay cash for a car

Answer: Only if you have a substantial emergency fund remaining. Depleting your savings entirely for a car leaves you vulnerable to unexpected expenses. It’s often wiser to finance a portion if it means keeping your emergency savings intact.

Summary

When choosing between cash and financing for a car, remember that What Most Men Get Wrong About Cash vs Financing Cars often involves overlooking the potential benefits of financing. It’s not just about avoiding interest; it’s about strategic financial planning. By comparing opportunity costs, understanding loan terms, and considering your credit-building goals, you can make the smartest decision for your money.