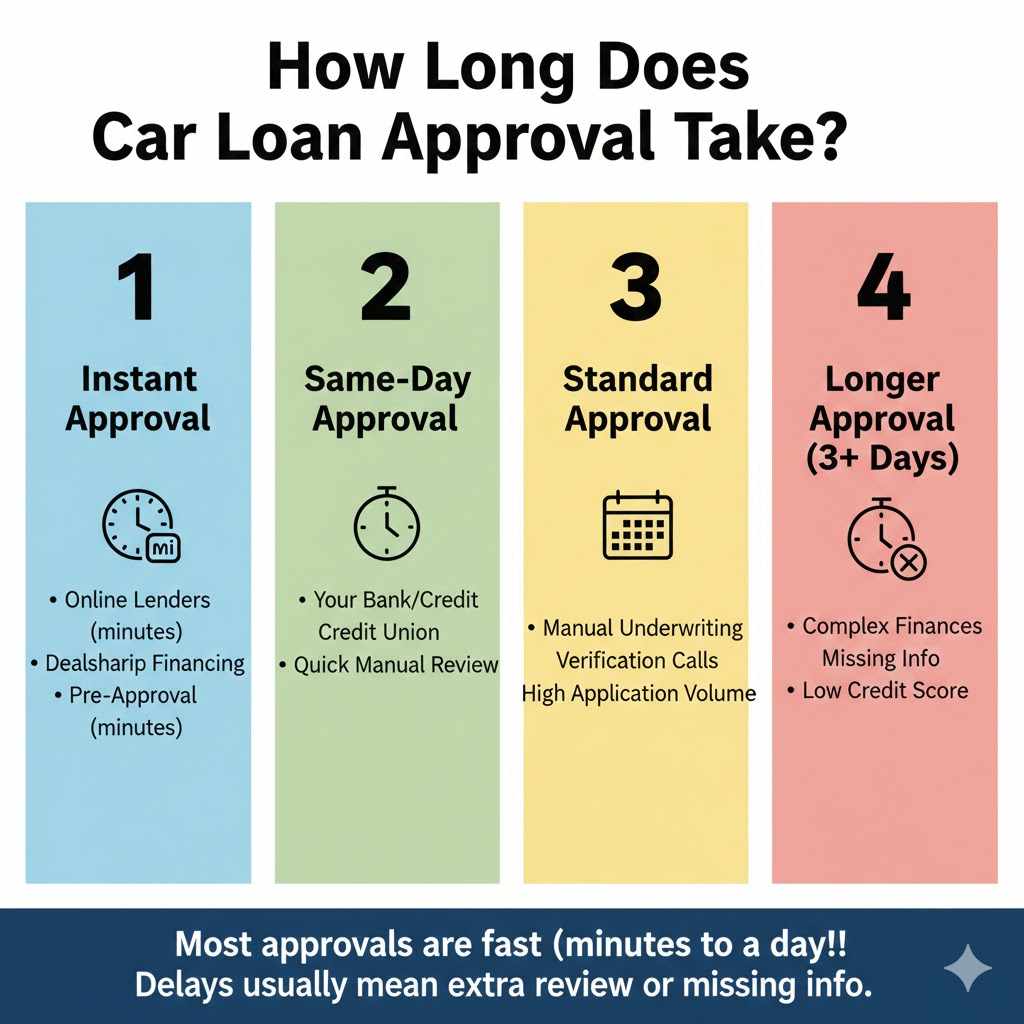

How Long Does It Take to Get a Car Loan Approved? The Full Timeline

Getting a car loan approved can take anywhere from a few minutes to several business days. Online lenders and dealerships often provide instant pre-approvals, while traditional banks or credit unions might take 1-3 business days. Your credit score, application accuracy, and the lender you choose are the biggest factors influencing your approval time.

Waiting for a car loan approval can feel like watching paint dry. You’ve found the perfect car, you’re excited to get behind the wheel, but a big question mark is hanging over your head. Will the loan go through? How long will this take? It’s a common worry, and it can add a lot of stress to an otherwise exciting experience.

Don’t worry, I’m here to help clear things up. My name is Md Meraj, and I’m here to make car ownership simple and stress-free. We’re going to break down the car loan approval process together. You’ll learn exactly what affects the timeline, what lenders are looking for, and the best secrets to speed everything up. By the end of this guide, you’ll feel confident and ready to get your approval as fast as possible.

The biggest question on everyone’s mind is simple: how long is the wait? The answer isn’t a single number, because it depends heavily on where you apply and how prepared you are. Let’s break down the typical timelines you can expect.

Instant Approval (Minutes to an Hour)

Yes, it’s possible to get approved almost instantly! This lightning-fast turnaround is most common in a few specific scenarios:

- Online Lenders: Many online-only financial institutions use sophisticated algorithms to review your application. If you have a strong credit score and a straightforward financial profile, their automated systems can give you a “yes” or “no” in minutes.

- Dealership Financing: Car dealerships have direct relationships with multiple lenders. When you apply through them, their finance manager sends your application to their network. For buyers with good credit, offers can start rolling in before you’ve even finished your test drive.

- Pre-Approval: This is your secret weapon. Getting pre-approved online from a bank or credit union before you even visit a dealership often results in an instant decision. This tells you exactly how much you can borrow and shows the dealer you’re a serious buyer.

Same-Day Approval (1 to 8 Hours)

Sometimes, the process takes a few hours. This is very common and still considered a fast approval. This usually happens when:

- You apply at your own bank or credit union. If you have a long-standing relationship with a financial institution, they can quickly review your history with them. Applying early on a business day increases your chances of a same-day answer.

- Your application needs a quick manual review. Maybe one number on your application needs a second look, or the loan amount is slightly higher than their automatic approval threshold. A loan officer will briefly review it and can often give you an answer within the business day.

Standard Approval (1 to 3 Business Days)

This is the most traditional timeframe, especially when dealing with banks or credit unions where you are not currently a member. An approval that takes a couple of days is not a bad sign! It just means a human is carefully reviewing your file. Here’s why it can take this long:

- Manual Underwriting: A loan officer, or “underwriter,” is personally reviewing your credit report, income documents, and debt-to-income ratio. They are making sure you can comfortably afford the payments.

- Verification Calls: The lender might need to call your employer to verify your job and income, which can take time depending on when they can reach the right person.

- High Application Volume: If you apply during a busy season (like a holiday sales event), the lender may simply have a backlog of applications to get through.

Longer Approval (More Than 3 Days)

If you find yourself waiting for more than a few days, it’s usually due to a specific issue. This is less common, but it’s good to know the potential causes:

- Complex Financial Situation: If you are self-employed, have variable income, or have a unique credit history, lenders will take extra time to understand your finances.

- Missing or Incorrect Information: This is the most common reason for a long delay. If you forget to submit a pay stub or enter your Social Security number incorrectly, the process comes to a halt until you fix it.

- Low Credit Score: Lenders who specialize in subprime loans (for borrowers with poor credit) often have a more intensive review process to assess the risk.

The 4 Key Factors That Speed Up (or Slow Down) Your Approval

Understanding what lenders look for is the key to a fast approval. Think of it like a checklist. The more boxes you can tick ahead of time, the smoother the road will be. Let’s look at the four biggest factors.

1. Your Credit Score: The Most Important Number

Your credit score is a three-digit number that tells lenders how responsibly you’ve handled debt in the past. A higher score means you are a lower risk, which makes lenders much more eager to approve you quickly.

- Excellent Credit (720+): You are a lender’s dream. You can expect fast, often instant, approvals and the best interest rates.

- Good Credit (690-719): You are still in a great position. Approvals are typically fast, usually same-day or within 24 hours.

- Fair Credit (630-689): Lenders will take a closer look. They will want to verify your income and employment more carefully. Approval might take 1-3 days.

- Poor Credit (Below 630): Approval will take longer. The lender needs to do a deep dive into your financial situation to see if you can handle the loan. It’s still possible to get approved, but expect the process to take several days.

It’s a great idea to know your score before you apply. You can get a free copy of your credit report from all three major bureaus at the official government-authorized site, AnnualCreditReport.com.

2. Your Application’s Accuracy and Completeness

This might sound simple, but it is the number one cause of preventable delays. A small typo in your address or a mistake in your income figures can flag your application for a manual review. Before you hit “submit,” double-check and even triple-check every single field. Make sure your name matches your ID exactly, your address is correct, and all numbers are accurate.

3. The Lender You Choose

Not all lenders are created equal when it comes to speed. Where you apply makes a huge difference in the approval timeline.

| Lender Type | Typical Approval Time | Best For |

|---|---|---|

| Online Lenders | Minutes to a few hours | Speed, convenience, and comparing rates easily. |

| Car Dealerships | Minutes to a few hours | One-stop shopping and convenience, especially for those with good credit. |

| Credit Unions | Same day to 2 business days | Members looking for great customer service and competitive rates. |

| Large National Banks | 1 to 3 business days | Existing customers who value the security of a large institution. |

4. Your Overall Financial Health

Lenders look at more than just your credit score. They want to see a complete picture of your financial stability. Two key metrics they consider are:

- Income Stability: Lenders love to see a steady job history. If you’ve been at your current job for two years or more, it gives them confidence. If you’ve changed jobs recently or have inconsistent income, they may ask for more documentation, slowing things down.

- Debt-to-Income (DTI) Ratio: This sounds complicated, but it’s simple. It’s the percentage of your gross monthly income that goes toward paying your monthly debts (rent/mortgage, credit card payments, other loans). For example, if you earn $4,000 a month and your total debt payments are $1,600, your DTI is 40%. Most lenders prefer a DTI below 43% for a quick approval. The Consumer Financial Protection Bureau offers great tools to help you understand your DTI.

Your 5-Step Checklist for a Lightning-Fast Car Loan Approval

Want to get that “approved” message as fast as possible? Follow this simple checklist. Preparation is your best friend in this process.

- Know Your Credit Score Before You Start. Don’t walk into the process blind. Check your credit score and report a few weeks before you plan to apply. This gives you time to spot and dispute any errors that could be hurting your score and causing delays.

- Gather All Your Documents in One Place. Nothing slows down an application like a missing document. Have digital and physical copies of everything you’ll need ready to go. This shows the lender you are organized and serious.

- Get Pre-Approved Before You Go to the Dealership. This is the ultimate pro tip. Applying for pre-approval from your bank, credit union, or an online lender accomplishes two things. First, it gives you a firm budget to work with. Second, you walk into the dealership with financing already secured. This turns you into a “cash buyer” in their eyes, simplifying the negotiation and speeding up the final paperwork immensely.

- Fill Out the Application Perfectly. Take your time. Sit down without distractions and fill out every field carefully. Use your documents to ensure every number for your income, address, and employment history is 100% correct.

- Apply at the Right Time. If you’re applying with a bank or credit union, do it on a weekday morning. This gives the loan officers a full business day to review your file. Applying late on a Friday afternoon, especially before a holiday weekend, is the surest way to guarantee you’ll be waiting until next week for an answer.

Essential Documents Checklist

Having these documents ready will prevent delays. Lenders need to verify who you are, how much you earn, and where you live.

| Document | Why You Need It |

|---|---|

| Proof of Identity | A valid driver’s license, state ID, or passport. This is non-negotiable. |

| Proof of Income | Your last two to three pay stubs. If you’re self-employed, you’ll need the last two years of tax returns and recent bank statements. |

| Proof of Residence | A recent utility bill (gas, electric, water) or bank statement with your name and current address on it. |

| Vehicle Information | If you’ve already picked out a car, have the purchase agreement or buyer’s order. It should include the car’s VIN, year, make, model, and price. |

| Proof of Insurance | You’ll need to show you have car insurance before you can drive off the lot. Have your insurance card or policy declaration page handy. |

Frequently Asked Questions About Car Loan Approvals

1. Can I get a car loan approved on the weekend?

Yes, it’s possible, especially through a car dealership. Dealership finance offices are open on weekends and work with lenders who have automated systems or weekend staff. However, if you apply directly to a traditional bank or credit union on a Saturday, you will likely have to wait until Monday for a final decision.

2. What’s the difference between pre-qualification and pre-approval?

Pre-qualification is a quick estimate of what you might be able to borrow, based on self-reported information and usually a soft credit check (which doesn’t affect your score). Pre-approval is a much more serious offer. It involves a formal application and a hard credit inquiry, resulting in a conditional commitment from the lender to give you a loan up to a certain amount.

3. Does applying for a car loan hurt my credit score?

When you formally apply for a loan, the lender performs a “hard inquiry” on your credit report, which can cause your score to dip by a few points temporarily. However, credit scoring models understand that people shop around for the best rate. Multiple auto loan inquiries made within a short period (usually 14-45 days) are typically treated as a single inquiry, minimizing the impact on your score.

4. How can I get a car loan approved with bad credit?

It’s more challenging but definitely possible. To improve your chances, save up for a larger down payment (20% or more is ideal), as this reduces the lender’s risk. Look for lenders who specialize in subprime auto loans, and consider asking a trusted family member or friend with good credit to co-sign the loan for you. Be prepared for a higher interest rate.

5. What does “conditionally approved” mean?

Conditional approval is great news! It means the lender has reviewed your credit and financial profile and has agreed to give you the loan, provided you meet a few final conditions. Typically, these conditions are just submitting your final documents for verification, like your most recent pay stub or proof of insurance for the new car. Once you provide these items, the approval becomes final.

6. Is it better to get financing through the dealership or my own bank?

It’s best to do both! Get a pre-approval from your own bank or a trusted online lender first. This gives you a baseline interest rate to compare against. Then, let the dealership see if they can beat that rate. This creates competition for your business and ensures you get the best possible deal.

You’re in the Driver’s Seat

Navigating the car loan process doesn’t have to be a long, anxious wait. As you can see, the time it takes to get approved is largely within your control. The secret isn’t about luck; it’s about preparation. By understanding your credit, gathering your documents, and choosing the right lender, you can significantly speed up the timeline.

Remember the key steps: check your credit, get your paperwork in order, and secure a pre-approval before you start shopping. This simple strategy puts you in a position of power. You’ll walk into the dealership not as someone asking for a loan, but as a confident, prepared buyer ready to make a smart deal.

So take a deep breath. You have the knowledge and the tools to make this process smooth and fast. You’re ready to get that approval and, most importantly, get on the road in your new car.