Is 642 a Good Credit Score for a Car Loan? Essential Guide

Is 642 a good credit score for a car loan? While not perfect, a 642 credit score is considered fair and can often qualify you for a car loan. However, expect higher interest rates and potentially less favorable terms compared to those with excellent credit. This guide will help you understand your options and how to improve your chances of approval.

Getting a car loan can feel like a big step, especially when you’re not sure where you stand with your credit score. If you’ve looked into it and seen a 642 score, you might be wondering if that’s “good enough.” It’s a common question, and frankly, it can be a bit confusing with all the different numbers and ranges out there. The good news is, a 642 credit score isn’t the end of the road for your car-buying dreams.

It falls into the “fair” credit category, meaning you can likely get approved for a loan, but it might come with some strings attached, like higher interest rates. Don’t worry, though! We’re going to break down exactly what a 642 credit score means for securing a car loan, what to expect, and most importantly, how you can make the process smoother and potentially save money. We’ll cover everything from understanding credit score ranges to finding the right lender and even strategies to boost your score for future opportunities.

Understanding Credit Scores and Car Loans

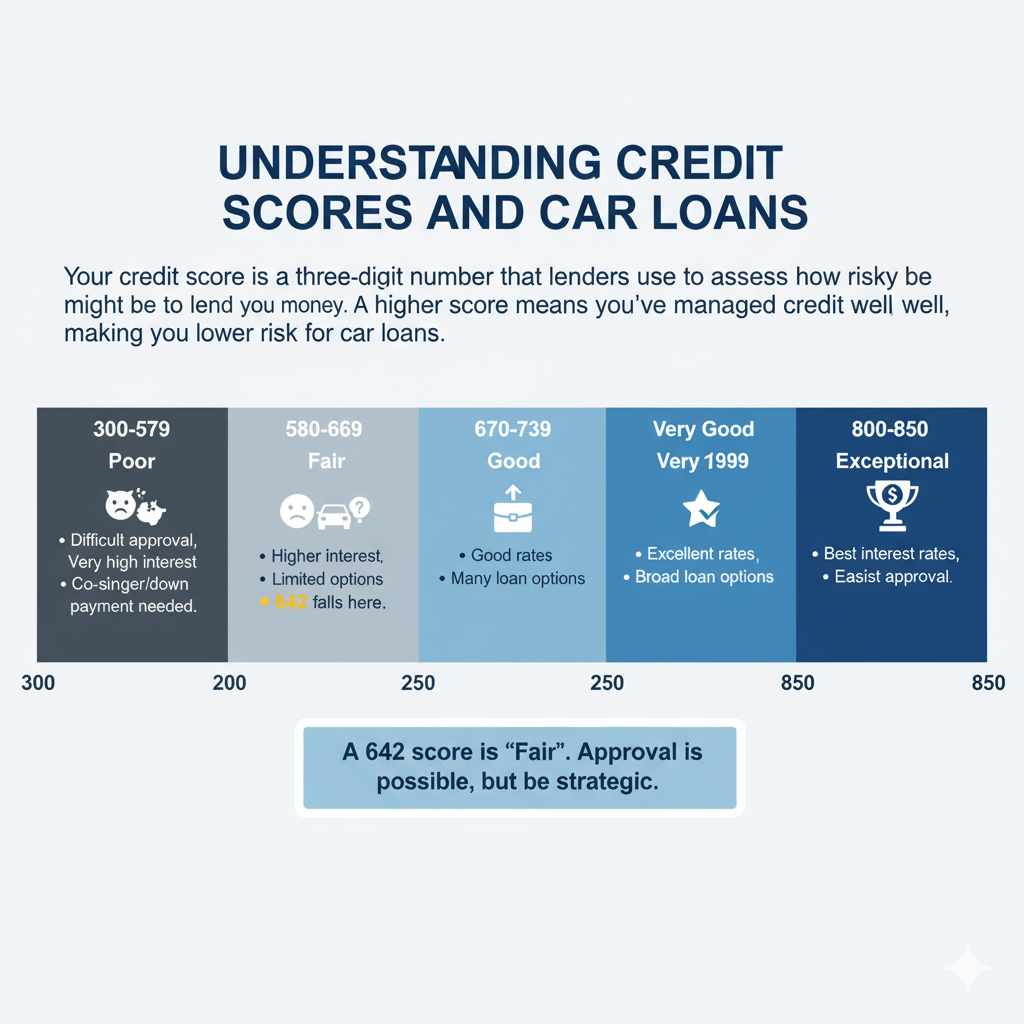

Your credit score is a three-digit number that lenders use to assess how risky it might be to lend you money. Think of it like a financial report card. A higher score generally means you’ve managed credit well in the past, making you a lower risk to lenders. For car loans, this score is a big factor in whether you get approved and what kind of interest rate you’ll pay.

Credit scores typically range from 300 to 850. Lenders often group these scores into categories to make decisions easier:

| Credit Score Range | Category | Implications for Car Loans |

|---|---|---|

| 800-850 | Exceptional | Best interest rates, easiest approval. |

| 740-799 | Very Good | Excellent rates, broad loan options. |

| 670-739 | Good | Good rates, many loan options available. |

| 580-669 | Fair | Higher interest rates, more limited options, possibly requiring a co-signer or larger down payment. This is where a 642 score typically falls. |

| 300-579 | Poor | Difficult approval, very high interest rates, often requires a co-signer or a significant down payment, or a subprime lender. |

As you can see from the table, a 642 credit score lands squarely in the “Fair” category. This isn’t ideal, but it’s a significant step above “Poor” credit. It means lenders see you as someone who has had some credit challenges, whether it’s late payments, high credit utilization, or other issues, but you’re not considered an extremely high risk. You’re in a position where approval is possible, but you’ll need to be strategic.

Is 642 a “Good” Score for a Car Loan Specifically?

To directly answer your question: is 642 a good credit score for a car loan? It’s a borderline score. It’s not considered “good” in the sense of securing the best possible rates and terms, but it’s often good enough to get approved. Many lenders have specific programs designed for buyers with fair credit. However, the interest rates you’ll be offered will reflect the increased risk perceived by the lender. This means your monthly payments might be higher, and the total amount of interest you pay over the life of the loan could be substantial compared to someone with a score in the 700s.

The key takeaway here is that while 642 might not get you the “gold star” treatment from lenders, it doesn’t close the door on getting a car. It simply means you’ll need to do your homework, compare offers carefully, and potentially work a little harder to get the best deal possible for your situation.

What to Expect with a 642 Credit Score for a Car Loan

When you apply for a car loan with a 642 credit score, here’s what you should generally expect. Understanding these factors upfront can help you prepare and manage your expectations.

Interest Rates (APR)

This is likely the most significant impact. With a fair credit score, you’ll probably be offered a higher Annual Percentage Rate (APR) than someone with good or excellent credit. A higher APR means you pay more interest on the loan. For example, a 5-year loan of $20,000 with a 5% APR might have a monthly payment of about $377. The same loan at 12% APR would cost about $445 per month, a significant difference over time. The Consumer Financial Protection Bureau (CFPB) offers resources to understand auto loan terms.

Loan Approval Odds

Approval is possible, but not guaranteed. It depends heavily on the specific lender and their risk tolerance. Some lenders specialize in subprime auto loans (loans for borrowers with lower credit scores) and may be more willing to approve your application, but usually at higher rates. Others might require additional security, such as a co-signer or a larger down payment, to mitigate their risk.

Down Payment Requirements

Lenders often ask for a larger down payment from borrowers with fair credit. This reduces the loan amount and minimizes the lender’s risk if you were to default. The exact amount can vary, but budgeting for a larger upfront payment is wise.

Loan Terms and Amount

You might find that the loan terms are less flexible. Lenders may offer shorter loan terms to get their money back sooner, or they might cap the amount you can borrow. It’s also possible the lender will only approve you for a loan on a less expensive vehicle than you might have hoped for.

Co-signer or Dealer Financing

To improve your chances of approval and potentially secure a better rate, you might consider bringing a co-signer with good credit onto the loan. Alternatively, dealership financing (also known as dealer financing or indirect lending) can sometimes be more flexible, as dealerships work with various lenders, including those who cater to a wider range of credit scores.

Factors Lenders Consider Beyond Your Score

While your credit score is a primary factor, lenders don’t look at it in isolation. They also consider other elements to get a fuller picture of your financial health and your ability to repay the loan.

- Income and Employment Stability: Lenders want to see that you have a steady income to make your monthly payments. Proof of employment and income (like pay stubs or tax returns) are usually required. A stable work history, especially in the same industry or with the same employer, is reassuring.

- Debt-to-Income Ratio (DTI): This is the percentage of your gross monthly income that goes toward paying your monthly debt obligations. Lenders prefer a lower DTI, as it indicates you have more disposable income available to handle new loan payments.

- Loan-to-Value Ratio (LTV): This compares the loan amount to the value of the car you’re buying. A lower LTV (meaning you’re borrowing less relative to the car’s worth, often achieved with a larger down payment) can make a lender more comfortable.

- Payment History on Previous Loans: Even with a 642 score, if your credit report shows a history of on-time payments on other loans (like personal loans or mortgages), it can help offset some of the concerns associated with a fair score.

- Trade-in Value: If you’re trading in an existing vehicle, its trade-in value can act as an additional form of down payment, reducing the overall loan amount and potentially improving your LTV.

How to Improve Your Chances of Getting Approved with a 642 Credit Score

Even with a fair credit score, there are proactive steps you can take to increase your likelihood of getting approved for a car loan and potentially get better terms.

1. Get Pre-Approved from Multiple Lenders

Don’t just walk into a dealership and apply for financing. Research and apply for pre-approval from banks, credit unions, and online lenders before you shop for a car. This allows you to compare offers and see what APRs and terms you qualify for. Credit unions, in particular, often offer competitive rates. Applying for pre-approval from multiple lenders within a short period (usually 14-45 days, depending on the credit scoring model) is typically treated as a single inquiry, minimizing the impact on your credit score. You can leverage this information to negotiate with the dealership’s finance department.

You can find reputable lenders through resources like the National Credit Union Administration (NCUA) for credit unions or by researching banks known for auto lending. Some online lenders even have tools that allow you to check your pre-approval odds without a hard credit pull.

2. Boost Your Down Payment

A larger down payment is one of the most effective ways to improve your loan approval odds and secure a better interest rate. It shows the lender you are serious about the purchase and reduces their risk. Aim for at least 10-20% of the car’s price, though more is always better. Even an extra $500-$1000 can make a difference. Consider saving a bit longer, selling an unused item, or using a tax refund if possible.

3. Consider a Co-signer

If you have a trusted friend or family member with a strong credit history (e.g., a score above 700), ask them if they would be willing to co-sign your car loan. A co-signer agrees to be legally responsible for the loan if you fail to make payments. This can significantly increase your chances of approval and may help you qualify for a lower interest rate. However, be aware that a co-signer’s credit score will be affected if payments are missed, and it puts a strain on your relationship if things go wrong. Ensure open communication and a solid repayment plan are in place.

4. Shop for Cars Within Your Budget

It’s easy to get caught up in wanting a specific car, but it’s crucial to be realistic about what you can afford. With a fair credit score, you’ll likely be paying more interest. Calculate your total monthly car expenses, including loan payment, insurance, gas, and maintenance, and choose a vehicle that fits comfortably within your budget. Focus on reliable, fuel-efficient models that have lower insurance costs. Websites like Edmunds can help you estimate car costs and loan payments.

5. Prepare Necessary Documentation

Having all your paperwork in order can speed up the loan process and show lenders you are organized and prepared. Gather the following:

- Proof of income (recent pay stubs, W-2 forms, tax returns)

- Proof of address (utility bills, lease agreements)

- Valid driver’s license

- Vehicle information (if you’ve already chosen one)

- Insurance information (most lenders and dealerships will require proof of insurance before finalizing the loan)

6. Improve Your Credit Score for Future Loans

While you’re applying for a loan now, use this as an opportunity to improve your credit for even better deals in the future. Focus on these fundamental credit-building habits:

- Pay all bills on time: Payment history is the most significant factor in your credit score. Set up autopay or reminders.

- Reduce credit utilization: Keep the amount of credit you use well below your credit limits. Aim to keep your credit utilization ratio below 30%, ideally below 10%.

- Don’t open too many new accounts at once: Each new credit application can slightly lower your score temporarily.

- Check your credit report for errors: You are entitled to a free credit report annually from each of the three major credit bureaus (Equifax, Experian, and TransUnion) at AnnualCreditReport.com. Dispute any inaccuracies.

Making consistent, positive financial decisions now will benefit you in the long run.

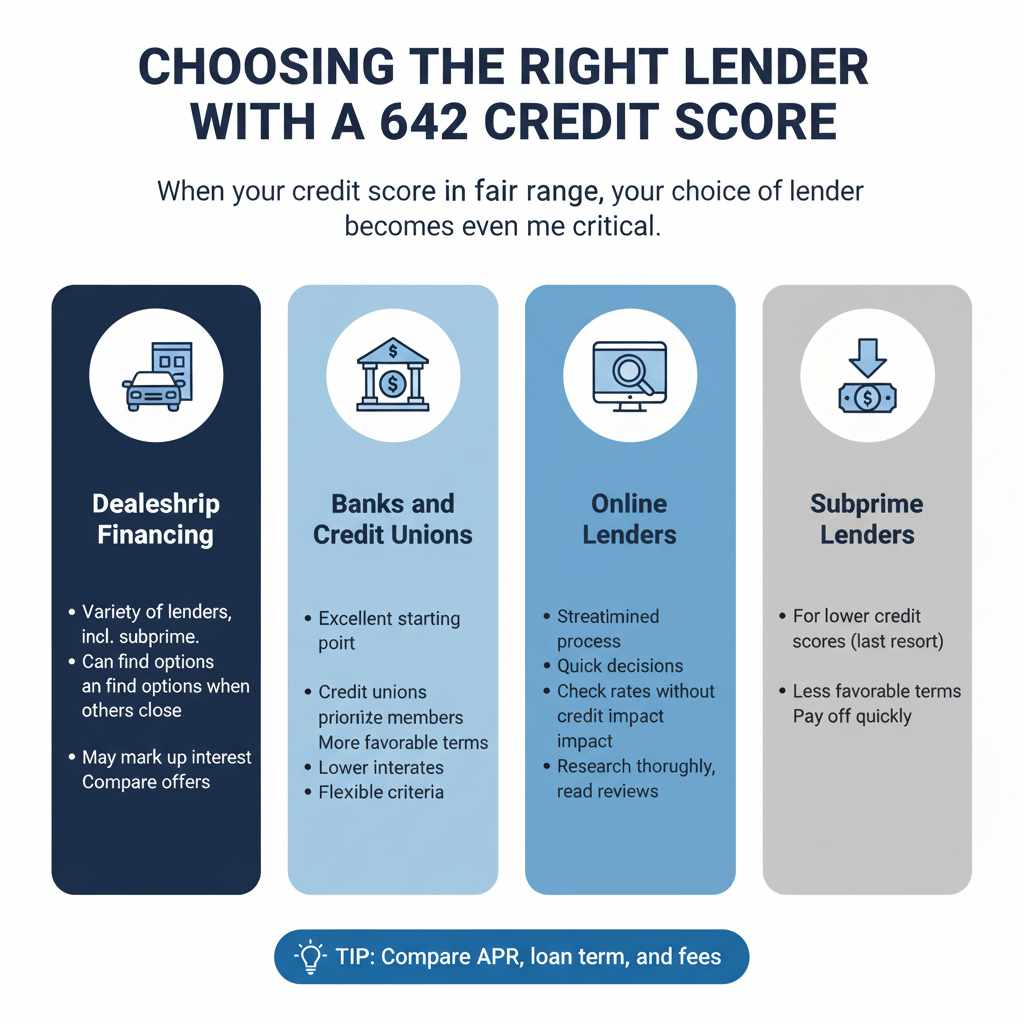

Choosing the Right Lender with a 642 Credit Score

When your credit score is in the fair range, your choice of lender becomes even more critical. Not all lenders are created equal, especially when it comes to working with borrowers who have fair credit.

Dealership Financing

Dealerships have established relationships with a variety of lenders, including those who specialize in subprime auto loans. They can often find options when other avenues might seem closed. However, dealerships can sometimes mark up interest rates to make a profit on the financing itself. Always compare dealership offers against pre-approved offers from other sources.

Banks and Credit Unions

Traditional banks and especially credit unions are excellent places to start. Credit unions, in particular, are member-owned and often prioritize helping their members, which can translate into more favorable loan terms, even for those with fair credit. Their approval criteria might be more flexible, and their interest rates can be lower than what a dealership might offer. It’s worth checking if you are eligible to join a local credit union.

Online Lenders

Numerous online lenders offer auto loans, and many have specific programs for borrowers with fair credit. These lenders often have streamlined application processes and can provide quick decisions. Some offer tools to check your potential rates without impacting your credit score. Be sure to research online lenders thoroughly, read reviews, and understand all their fees and terms before committing.

Subprime Lenders

These lenders specifically cater to borrowers with lower credit scores. While they are often the most accessible option for those with scores like 642, they typically come with the highest interest rates and less favorable loan terms. Use these as a last resort if other options fall through, and try to pay off the loan as quickly as possible to minimize the excess interest paid.

Tip: When comparing loan offers, focus on the APR (Annual Percentage Rate), the loan term (length of the loan), and any fees associated with the loan.

Improving Your Credit Score Specifically for Car Loans

While you prepare to apply for a car loan, you might also be thinking about improving your credit score in the short term. Here are a few focused strategies:

1. Pay Down High Credit Card Balances

Your credit utilization ratio is a major component of your FICO score. If you have credit cards with high balances, paying them down significantly can boost your score within a billing cycle. For example, if you have a credit card with a $10,000 limit and a $5,000 balance (50% utilization), reducing that balance to $1,000 (10% utilization) can have a substantial positive impact on your score.

2. Become an Authorized User

If you have a trusted family member with excellent credit, they could add you as an authorized user to one of their credit cards. This means you get to have a card with their account number, but they remain responsible for payments. If they have a well-managed account (long history, low utilization, on-time payments), this can positively reflect on your credit report. However, ensure they are responsible and that the issuer reports authorized user activity to the credit bureaus.

3. Consider a Secured Credit Card

If your credit is fair due to a lack of credit history or past issues, a secured credit card is an excellent tool. You make a security deposit upfront (typically $200-$500), which becomes your credit limit. Use this card for small, everyday purchases and pay it off in full every month. Responsible use of a secured credit card is reported to credit bureaus and can help build a positive credit history over time.

4. Avoid New Credit Inquiries (Unless Pre-Approved)

While you’re in the car loan application process, try to avoid opening new credit accounts for anything else. Every hard credit inquiry associated with a new loan or credit card application can temporarily lower your score. Focus on the auto loan applications and pre-approvals during this crucial period.

Navigating the Car Buying Process with a 642 Score

Once you’ve got your financing options in sight, it’s time to think about the car itself. Here’s how to approach car shopping with a fair credit score:

Focus on Value, Not Just Flash

With higher interest rates potentially on the table, stretching your budget for a luxury or high-performance vehicle might lead to unmanageable monthly payments and a lot of interest paid. Prioritize reliable, fuel-efficient, and less expensive vehicles.