Should I Finance Or Pay Cash For A Car: The Genius Answer

Paying cash for a car is often the cheapest option because you avoid interest payments. However, financing is the smarter choice if it allows you to keep your savings for emergencies, invest your cash for a higher return, or secure a very low (or 0%) interest rate. The “genius” answer depends entirely on your financial situation and goals.

Deciding how to pay for your next car can feel like a huge test. One voice in your head says, “Pay cash! Avoid debt!” while another whispers, “Finance it! Keep your money safe!” It’s a common puzzle, and honestly, it can be really stressful. You just want to make the smart choice without regretting it later.

Don’t worry, I’m here to help you solve this puzzle. As your friendly auto guide, I’ll break it down into simple, easy-to-understand pieces. We’ll look at the good and bad of both options, and by the end, you’ll feel confident knowing exactly which path is right for you. Let’s find your genius answer together.

Walking onto a car lot is exciting, but the excitement can quickly turn to confusion when it comes time to talk money. The big question looms: Should you write a check for the full amount or sign up for monthly payments? There’s no single magic answer that works for everyone. The best choice is deeply personal and depends on your money, your goals, and your comfort level with debt. In this guide, we’ll explore both sides so you can drive off the lot with peace of mind.

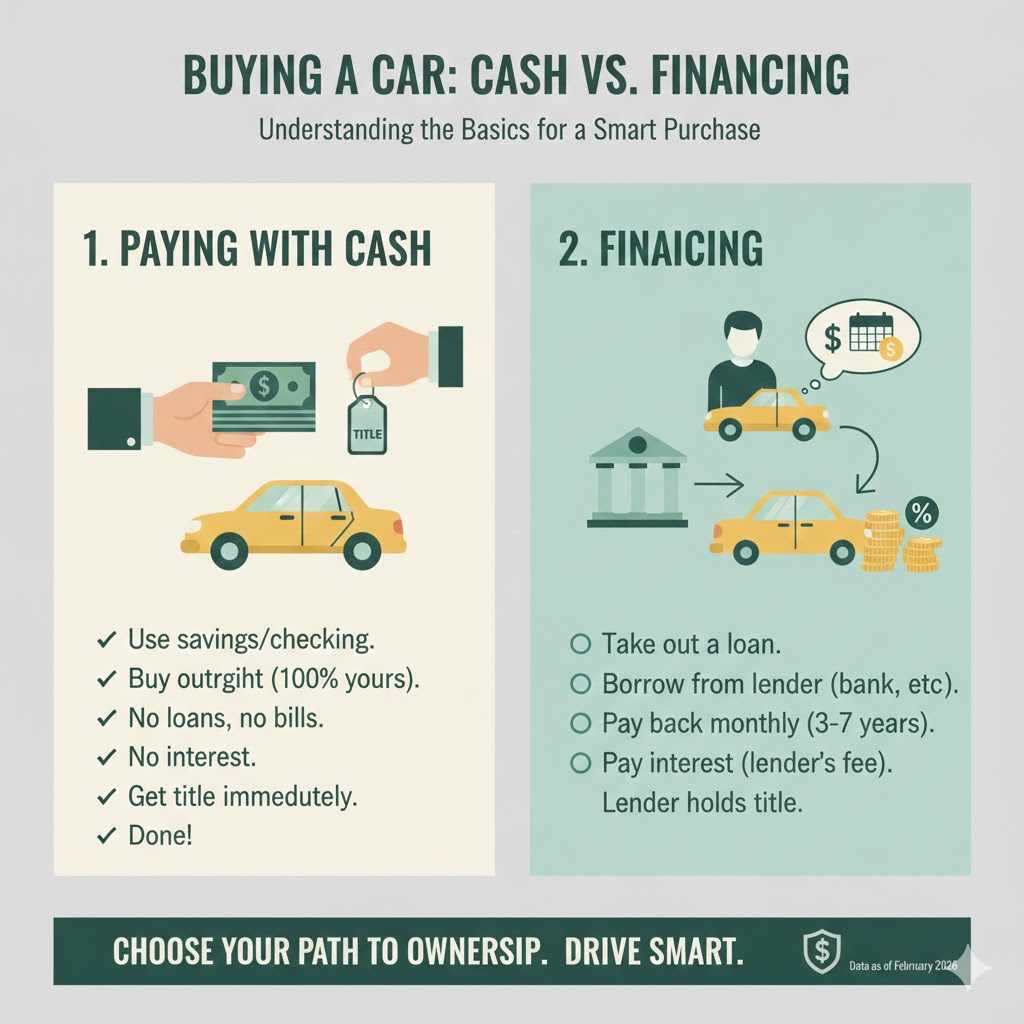

Understanding the Basics: Cash vs. Financing

Before we dive deep, let’s make sure we’re on the same page. These terms can sound complicated, but they’re actually very simple.

What Does Paying with Cash Mean?

Paying with cash is exactly what it sounds like. You use money from your savings or checking account to buy the car outright. You write a check, hand over a cashier’s check, or do a wire transfer, and the car is 100% yours. There are no loans, no monthly bills, and no interest to worry about. You get the title immediately, and the transaction is done.

What Does Financing Mean?

Financing means you’re taking out a loan to buy the car. You borrow money from a lender, like a bank, credit union, or the dealership’s finance company. You then pay that money back over a set period of time (the “term”), usually between 3 to 7 years, in monthly installments. In addition to paying back the loan amount, you also pay interest, which is the lender’s fee for letting you borrow their money.

The Case for Paying Cash: When It Makes Sense

The idea of owning your car free and clear from day one is very appealing. For many people, paying with cash is the simplest and most financially sound way to buy a vehicle. Let’s look at why.

The Big Benefits of Paying with Cash

- No Debt: This is the biggest win. You won’t have a car payment hanging over your head every month. That frees up your monthly budget for other things, like saving, investing, or just having a little more fun.

- Zero Interest Costs: When you finance, you always pay more than the car’s sticker price because of interest. Paying with cash means the price you see is the price you pay. Over the life of a loan, this can save you hundreds or even thousands of dollars.

- Simpler Buying Process: Buying with cash is straightforward. You don’t have to fill out loan applications, wait for credit approvals, or read through pages of loan agreements. You just agree on a price and make the payment.

- True Ownership: The car is yours, period. You hold the title, not the bank. This means you can sell it whenever you want without having to deal with a lender. You also have more flexibility with insurance, as lenders often require more expensive coverage (like comprehensive and collision).

When Paying Cash is the Smartest Move

Paying cash is a fantastic option if you find yourself in one of these situations:

- You have plenty of savings. You can afford to buy the car without wiping out your emergency fund. A good rule of thumb is to have at least 3-6 months of living expenses saved up AFTER you buy the car.

- You’re buying a less expensive, used car. If you’re buying a car for $5,000 or $10,000, it’s often much smarter to pay cash than to take out a small loan that might come with higher interest rates.

- You want to live a debt-free lifestyle. For some people, the peace of mind that comes with having no debt is priceless.

- Your credit isn’t great. If you have a low credit score, you’ll likely face very high interest rates on a loan, making financing extremely expensive. In this case, saving up to pay cash is a much better financial decision.

The Downsides of Paying with Cash

While paying cash sounds perfect, it does have a few potential drawbacks to consider.

- It can drain your savings. Tying up a large sum of money in a car (which is a depreciating asset, meaning it loses value over time) can be risky. If an unexpected emergency happens, you might not have the cash on hand to cover it.

- Opportunity Cost: This is a big one. The money you use to buy a car could have been used for something else, like investing in the stock market, which could potentially earn you a return. If the interest rate on a car loan is very low, you might actually make more money by investing your cash and financing the car instead.

- It might limit your car options. If you only have $15,000 in cash saved, you’re limited to cars at or below that price. Financing might allow you to get a newer, safer, or more reliable vehicle that you need, even if you don’t have the full amount upfront.

The Case for Financing: When It’s a Better Option

Financing a car is incredibly common, and for good reason. It makes car ownership accessible to almost everyone and can sometimes be a strategic financial move, even for people who have the cash.

Why Financing Can Be a Genius Move

- Keeps Your Cash Liquid: Your savings stay in your bank account, ready for emergencies, opportunities, or other important life goals like a down payment on a house. This financial flexibility can be a lifesaver.

- Allows You to Afford a Better Car: Financing can bridge the gap between the car you can afford with cash and the car you really need. This might mean a newer model with better safety features, improved fuel efficiency, or a factory warranty, which can save you money on repairs down the road.

- Builds Your Credit History: If you make all your payments on time, a car loan can be a great way to build or improve your credit score. A strong credit history is essential for getting good rates on future loans, like a mortgage.

- Access to Low-Interest Deals: Sometimes, car manufacturers offer promotional financing deals with incredibly low or even 0% APR (Annual Percentage Rate). In these cases, you’re borrowing money for free! It makes little financial sense to pay cash when you can use the lender’s money at no cost and keep your own cash invested.

When Financing is the Right Call

Financing might be your best bet under these circumstances:

- You qualify for a low interest rate. If you have a great credit score, you could get a loan with an interest rate lower than the rate of inflation or what you could earn by investing.

- You don’t want to touch your emergency fund. Your financial safety net is more important than avoiding a car loan.

- You are disciplined with your budget. You know you can comfortably afford the monthly payment without straining your finances.

- The dealership is offering a special 0% or near-0% APR deal. This is a clear signal to consider financing.

The Pitfalls of Financing to Watch Out For

Financing isn’t without its risks. Here’s what you need to be cautious about:

- It Costs More in the Long Run: Unless you get a 0% APR deal, you will always pay more than the car’s purchase price due to interest.

- Risk of Being “Underwater”: Cars lose value quickly. It’s possible to owe more on your loan than the car is actually worth, especially in the first couple of years. This is called being “underwater” or having “negative equity.” It can be a big problem if you need to sell the car or if it gets totaled in an accident.

- Temptation to Overspend: Focusing on a low monthly payment can trick you into buying a more expensive car than you can truly afford. Always look at the total cost of the car, including interest.

- Long Loan Terms: A 6- or 7-year (72- or 84-month) loan will have a lower monthly payment, but you’ll pay significantly more in interest over time. You could also still be making payments when the car starts needing expensive repairs.

Let’s Do the Math: A Simple Comparison

Numbers often make the decision clearer. Let’s imagine you’re buying a car for $25,000. Here’s how the costs could break down.

| Metric | Paying Cash | Financing |

|---|---|---|

| Car Price | $25,000 | $25,000 |

| Loan Terms | N/A | 60 months (5 years) at 6% APR |

| Monthly Payment | $0 | $483 |

| Total Interest Paid | $0 | $3,998 |

| Total Cost of Car | $25,000 | $28,998 |

In this example, financing costs you almost $4,000 extra. That seems like an easy win for cash, right? But now, let’s consider opportunity cost. What if you took that $25,000 and invested it instead, earning an average return of 8% per year? Over those same 5 years, your investment could grow to be worth over $36,700. In that scenario, you would have come out way ahead by financing the car.

The “Genius” Answer: A Hybrid Approach?

What if you don’t have to choose one extreme or the other? For many people, the smartest move is a middle ground: making a large down payment and financing the rest.

A down payment is the amount of cash you pay upfront. By putting down a significant amount—say, 20% or more of the car’s price—you get the best of both worlds:

- You borrow less money. This immediately reduces your monthly payment and the total interest you’ll pay.

- You avoid being “underwater.” A large down payment gives you instant equity in the car, protecting you if you need to sell it early on.

- You may get a better interest rate. Lenders see a large down payment as a sign that you are a lower-risk borrower, and they may offer you more favorable loan terms.

- You keep cash in the bank. You still have a healthy savings account for emergencies and other goals.

This balanced strategy minimizes risk while preserving your financial flexibility, making it a truly “genius” answer for many car buyers.

Key Factors to Help You Decide

To find your perfect answer, you need to look at your personal situation. Grab a piece of paper and think honestly about these five factors.

| Factor | What to Consider |

|---|---|

| Your Financial Health | Do you have a fully funded emergency fund (3-6 months of expenses)? Is your job stable? Don’t even think about paying cash if it leaves you without a safety net. The Consumer Financial Protection Bureau has great resources for building your savings. |

| Your Credit Score | Check your score for free. A score above 720 will likely get you good interest rates, making financing more attractive. A score below 650 might mean high rates, pushing you toward paying cash. |

| Current Interest Rates | What are the average auto loan rates right now? Are there any manufacturer deals for 0% APR? A low-rate environment makes financing a much better deal. |

| The Type of Car | Are you buying a brand new $50,000 car or a reliable $8,000 used car? It’s much easier and often wiser to pay cash for the less expensive vehicle. |

| Your Personal Goals & Philosophy | What’s more important to you? Being completely debt-free, or having more cash on hand for investments and flexibility? There’s no wrong answer here—it’s about what helps you sleep at night. |

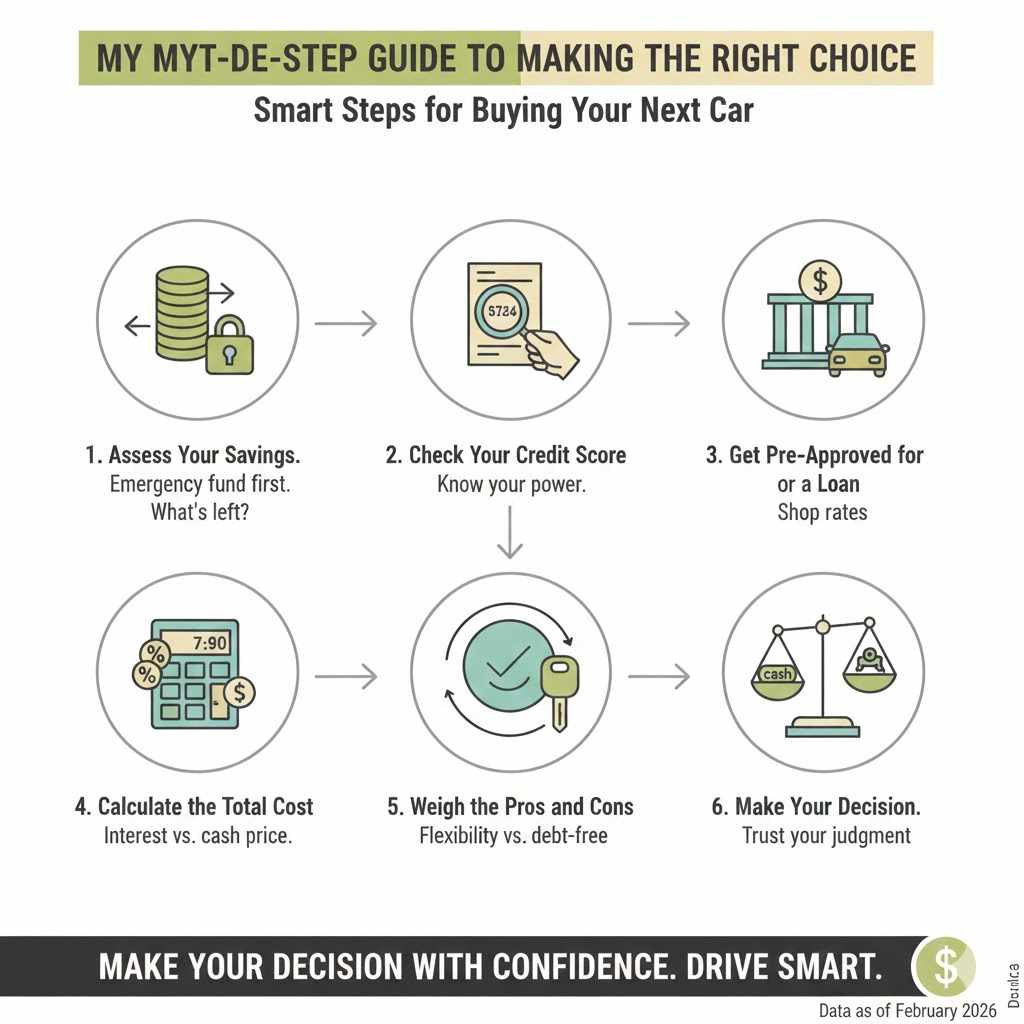

My Step-by-Step Guide to Making the Right Choice

Feeling a little overwhelmed? Don’t be. Just follow these simple steps to make a decision you can feel great about.

- Assess Your Savings. First, calculate how much you need for a 3-6 month emergency fund. Set that money aside mentally—it’s not for the car. What’s left over is your potential “car cash.”

- Check Your Credit Score. Use a free service like Credit Karma or check with your bank or credit card company. Knowing your score gives you power.

- Get Pre-Approved for a Loan. Before you even visit a dealership, apply for a car loan at your local bank or credit union. They often have better rates. This will tell you exactly what interest rate you qualify for, so you can do the math accurately.

- Calculate the Total Cost. Use an online auto loan calculator to see how much you’d pay in total interest for the car you want. Compare that to the cash price.

- Weigh the Pros and Cons for YOU. Look at your calculations and the key factors from the section above. Is the extra cost of financing worth the financial flexibility it provides you? Or is the peace of mind of being debt-free more valuable?

- Make Your Decision with Confidence. By now, you’ve done your homework. You know your numbers and your priorities. Trust your judgment and make the choice that best fits your life.

Frequently Asked Questions (FAQ)

Is it ever a good idea to drain my savings to pay cash for a car?

Almost never. Your emergency fund is your most important financial tool. It protects you from unexpected job loss, medical bills, or home repairs. Depleting it for a car puts you in a very risky position. Always prioritize your financial safety net first.

Can I build my credit score by financing a car?

Yes, absolutely. An auto loan is a type of installment loan. Making your payments on time, every time, is a powerful way to show lenders that you are a responsible borrower, which can significantly boost your credit score over the life of the loan.

What is a good interest rate for a car loan?

This changes with the economy, but generally, a “good” rate for someone with excellent credit (760+) might be between 4% and 7%. A rate below 3% is excellent, and a 0% APR deal is unbeatable. Rates can go much higher (10%+) for those with lower credit scores.

What is “opportunity cost” when buying a car?

Opportunity cost is the potential gain you miss out on when you choose one option over another. In this case, it’s the money you could have earned by investing your cash instead of using it to buy a car. If your investments can earn 8% and a car loan costs you 5%, you come out ahead by financing.

Does paying cash give me more negotiating power at the dealership?

Not as much as it used to. In the past, “cash was king.” Today, dealerships often make a significant portion of their profit from arranging financing. While they are happy to take your cash, a buyer who is pre-approved for a loan is just as strong. The best negotiating tool is being prepared and willing to walk away.

What happens if I can’t make my car payments?

If you start missing payments, the lender will report it to the credit bureaus, which will seriously damage your credit score. If you continue to miss payments, the lender can legally repossess (take back) the vehicle. It’s crucial to only take on a loan payment that you are confident you can afford.

Conclusion: Your Road to a Smart Car Purchase

So, what is the genius answer to the finance versus cash debate? The genius answer is the one that is right for you. It’s not about what your friend did or what a radio host shouts about. It’s about looking honestly at your savings, your credit, your income, and your goals.

For some, the freedom of a paid-off car is the ultimate prize. For others, the strategic flexibility of keeping cash invested while using a low-interest loan is the smarter financial play. And for many, the balanced, hybrid approach of a large down payment is the perfect compromise.

You now have all the tools and knowledge you need to make this decision. By thinking it through and following the steps we’ve laid out, you’re no longer guessing. You’re making an informed, confident choice that will benefit you for years to come. Now go out there and get the right car, the right way.