What Happens If Financed Car Is Stolen: Essential Guide

If your financed car is stolen, you’ll generally need to file a police report and an insurance claim. Your loan agreement still stands, so your lender expects payments until the car is recovered or the insurance payout settles the debt. Understanding your insurance coverage and working closely with your lender and insurer are key.

It’s a terrible feeling to walk out to where you parked your car and find it gone. What if you’re still paying off the loan? This is a common worry for many car owners. Knowing what steps to take can make a stressful situation much more manageable. This guide will walk you through exactly what happens if your financed car is stolen and what you need to do. We’ll cover everything from reporting the theft to dealing with your lender and insurance company.

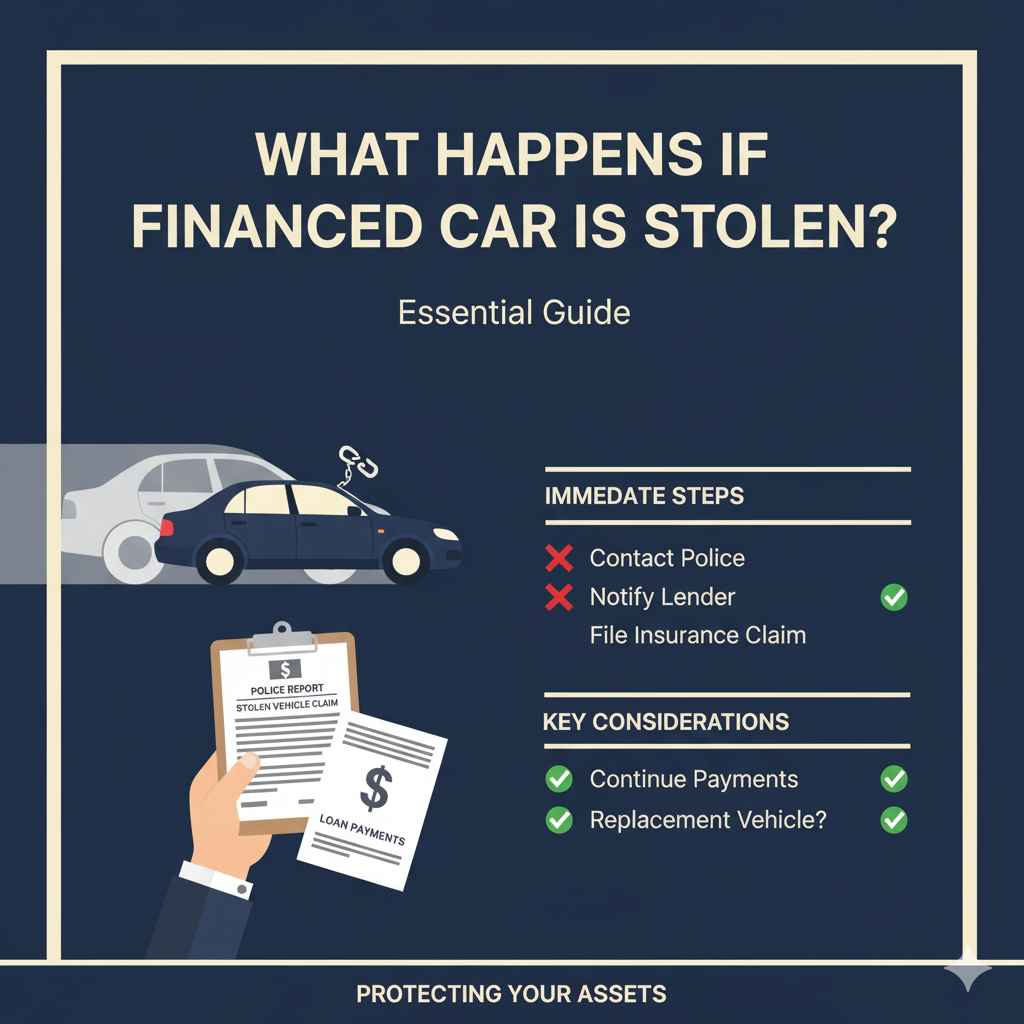

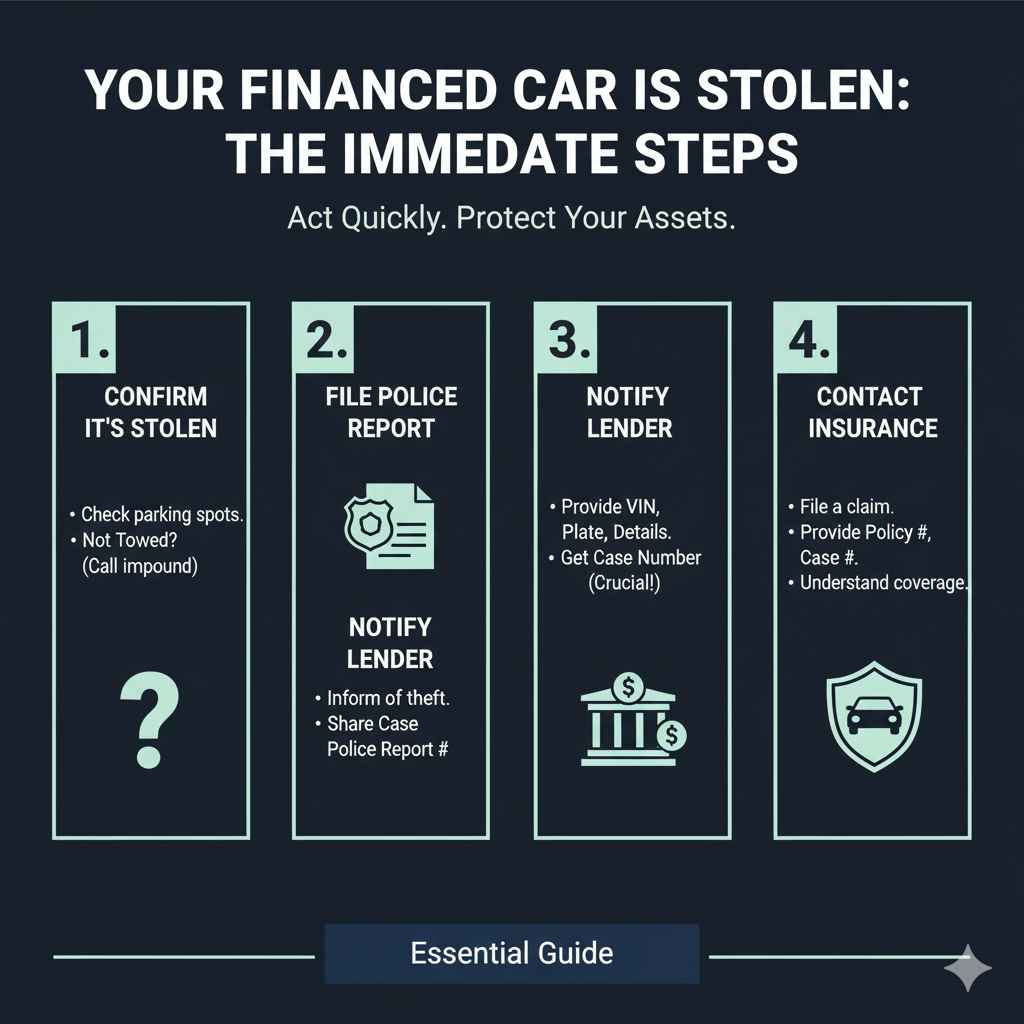

Your Financed Car is Stolen: The Immediate Steps

The moment you realize your car is missing and suspect it’s been stolen, it’s crucial to act quickly and calmly. These first steps are vital for both the recovery of your vehicle and for your insurance and loan responsibilities.

1. Confirm It’s Stolen

Before you call the authorities, be absolutely sure. Is it possible you simply forgot where you parked? Did a family member move it? Double-check your usual parking spots and think about any recent changes. If you’re certain it’s gone and it wasn’t towed legitimately (check with local towing companies or your city’s impound lot), then proceed to the next step.

2. File a Police Report Immediately

This is your absolute first official action. Contact your local police department or sheriff’s office. You’ll need to provide:

Your personal information.

The make, model, year, and color of the car.

The Vehicle Identification Number (VIN) – often found on your registration or insurance documents.

The license plate number.

Any distinguishing marks or features of your car.

The location and time you last saw the vehicle.

Any details about how you suspect it was stolen.

The police will create an official report, which is essential for insurance claims and any future recovery efforts. They will likely enter your car’s information into national databases for stolen vehicles. You’ll receive a case number – keep this handy, as you’ll need it for everything that follows.

3. Notify Your Lender

As soon as you’ve filed the police report, contact your auto loan lender. Inform them that your financed car has been stolen. They need to know what’s happening with the asset they have a lien on. Provide them with your police report case number. They will guide you on their specific procedures and what documentation they require from you.

4. Contact Your Insurance Company

This is critical. Report the theft to your auto insurance provider as soon as possible. You’ll need to give them:

Your policy number.

The police report case number.

All details of the incident.

Your insurance agent will explain your coverage and the claims process. They will likely assign a claims adjuster to your case.

Understanding Your Auto Insurance Coverage

What happens next heavily depends on the type of auto insurance coverage you have. For a stolen car, the most relevant coverage is comprehensive insurance.

What is Comprehensive Insurance?

Comprehensive coverage helps pay for damage to your car that isn’t caused by a collision. This includes theft, vandalism, fire, natural disasters (like hail or floods), and hitting an animal. Most lenders require you to have comprehensive and collision coverage while you’re still paying off the car.

How Comprehensive Coverage Works for Theft

If your financed car is stolen and not recovered, your comprehensive insurance policy should cover its actual cash value (ACV) minus your deductible. The ACV is what the car was worth right before it was stolen. Your insurance payout will go towards satisfying your loan balance.

What if Your Car is Recovered?

If the police recover your car before the insurance company pays out the full value of the loan, the situation changes. The insurance company will typically pay for any damage your car sustained while stolen, up to your comprehensive coverage limit. If there’s no damage, or the damage is minor and you agree to repairs, you might need to get your car back. However, if the car has been significantly damaged or has mileage beyond what you’re comfortable with, you may still have options. Discuss this thoroughly with both your insurance adjuster and your lender.

Your Auto Loan and a Stolen Car

The loan agreement you signed is a contract that is still valid, even if the car is gone. Your lender has a financial interest in the vehicle.

Do You Still Need to Make Payments?

Yes, you generally must continue making your loan payments as scheduled until the debt is resolved. The theft of the car doesn’t automatically erase your loan obligation. Payments are due because the loan covers the financing of the car, not just its physical presence.

What Happens to the Loan Balance?

Car Recovered, Minor Damage: If your car is found and returned to you with minimal damage, you’ll likely resume making payments. The insurance might cover repair costs.

Car Recovered, Major Damage: If the car is recovered but heavily damaged, your insurance will cover the repairs. Once repaired, you’ll resume payments. If the repair costs are deemed too high by the insurer or you, an agreement might be reached to settle the loan with the insurance payout and potentially take a different vehicle or other settlement.

Car Not Recovered: If your car isn’t found, your insurance will pay out the actual cash value of the car to your lender.

The Insurance Payout and Your Lender

When your car is declared a total loss and not recovered, the insurance payout goes directly to the lender.

Payout Equals Loan Balance: If the insurance payout is equal to or more than what you owe, the loan is considered paid off. If there’s any excess money after the loan is satisfied, that money typically comes back to you.

Payout is Less Than Loan Balance: This is where having gap insurance becomes very important. If the actual cash value of your car (what the insurance pays) is less than what you still owe on your loan, you are responsible for paying the difference. This is known as the loan deficiency.

This is where gap insurance (Guaranteed Asset Protection) plays a crucial role. It covers the difference between your insurance payout and the remaining balance on your loan if your car is stolen or declared a total loss. If you don’t have gap insurance, you’ll have to pay this shortfall out of pocket.

Deductibles: What You Need to Pay

When you file a comprehensive claim for a stolen car, you will almost always have to pay a deductible. This is the amount you pay out-of-pocket before your insurance coverage kicks in.

Deductible Amount: This is set in your insurance policy. It could be $500, $1,000, or another amount.

Who Pays Deductible: If your car is stolen and declared a total loss, the insurance company will pay the ACV of the car to the lender minus your deductible. So, if your car’s ACV is $20,000, your loan balance is $18,000, and your deductible is $500, the insurer would pay $18,000 to the lender. Some policies might structure it so the deductible is paid by you directly, or it might be subtracted from the ultimate payout to the lender. Clarify this with your insurer.

If Car is Recovered Damaged: If your car is recovered and has damage, you will pay the deductible to get it repaired under your comprehensive coverage.

Working with Law Enforcement and Recovery Efforts

Law enforcement agencies are your primary allies in recovering stolen vehicles.

The Role of Law Enforcement

Once a police report is filed, your car is entered into national databases. If it’s spotted by law enforcement anywhere in the country, it can be flagged for recovery. The police will then contact you and your lender.

What to Expect if Your Car is Found

Notification: The police will notify you and/or your lender that the car has been recovered.

Location: They will typically impound the vehicle at a secure location.

Inspection: You or your insurance company will likely need to inspect the car to assess any damage.

Retrieval: You or your lender will then arrange to retrieve the car and handle any towing fees or storage charges. These might be covered by insurance depending on your policy.

Authorities use various technologies and databases to track stolen vehicles. The National Insurance Crime Bureau (NICB) works closely with law enforcement to combat vehicle theft. You can learn more about their efforts and resources at NICB.org.

Tips to Protect Your Financed Car from Theft

While no method is foolproof, taking smart precautions can significantly reduce the risk of your financed car being stolen.

Preventative Measures

1. Always Lock Your Doors: It sounds simple, but many thefts occur because a car was left unlocked with the keys inside.

2. Never Leave Keys or Fob Inside: Even if you’re just running in for a minute, take your keys with you.

3. Park in Well-Lit Areas: Thieves prefer to work in the dark and in secluded spots.

4. Be Aware of Your Surroundings: If you see suspicious activity, avoid parking there.

5. Install Anti-Theft Devices:

Alarms: Audible alarms can deter thieves.

Immobilizers: These prevent the engine from starting without the proper key or fob. Many modern cars have these built-in.

Steering Wheel Locks: Highly visible physical deterrents.

GPS Trackers: While not a deterrent, these can greatly increase the chances of recovery if the car is stolen.

6. Don’t Leave Valuables Visible: This can make your car a target for break-ins, which can sometimes escalate to theft.

7. Keep Registration and Insurance Documents Secure: Don’t leave them easily accessible in the car if it’s broken into. Copy them and keep the originals at home in a safe place.

Using these tips can help keep your vehicle safe. For more information on vehicle security, resources like USA.gov offer valuable insights.

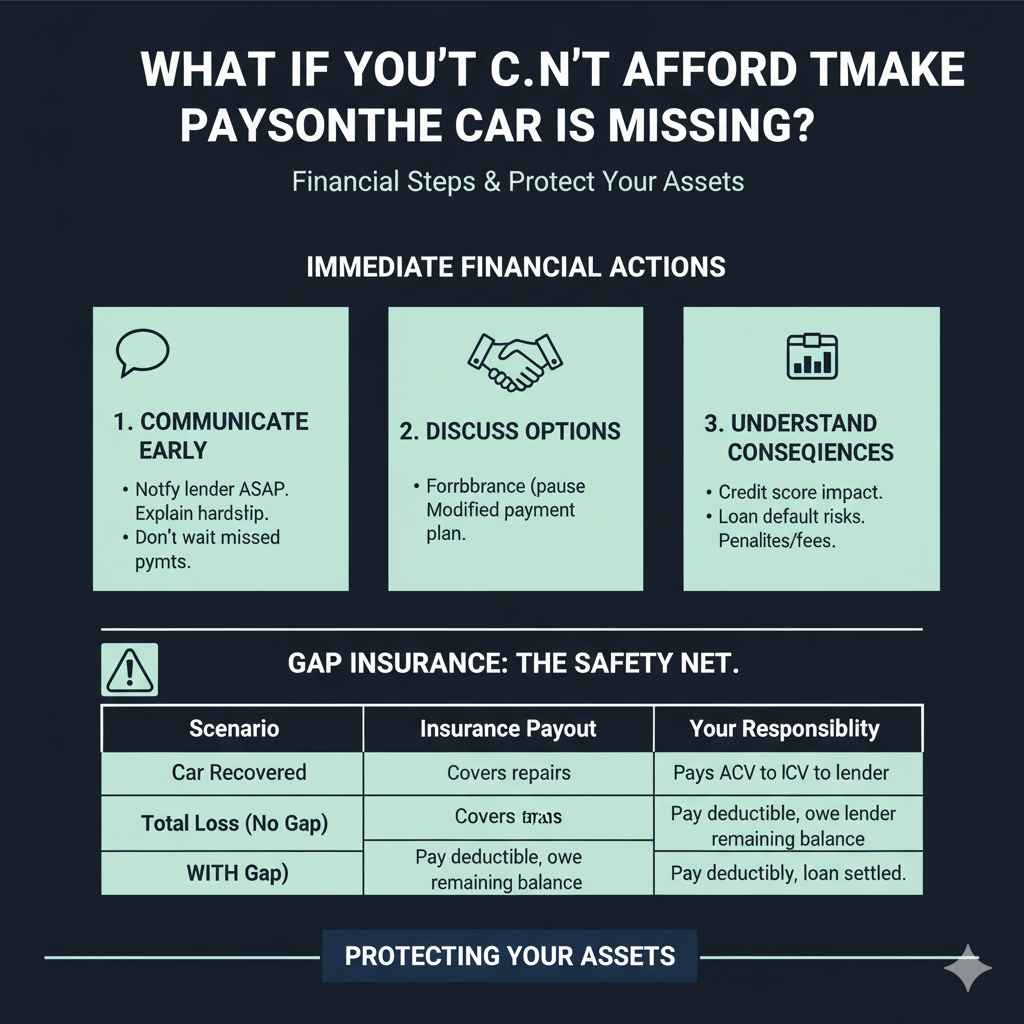

What If You Can’t Afford to Make Payments While the Car is Missing?

This is a challenging but important situation to address. If you’re unable to make loan payments because you’ve lost access to your vehicle and your income, it’s imperative to communicate this with your lender.

Communicate Early and Often: Don’t wait for missed payments. Contact your lender as soon as you know you might face difficulties making payments.

Discuss Forbearance or Payment Plans: Your lender might be willing to offer a temporary pause in payments (forbearance) or a modified payment plan. Explain your situation clearly and honestly.

Understand the Consequences: Missing payments, even when the car is stolen, can negatively impact your credit score. It’s essential to understand the terms of your loan agreement and any potential penalties.

Gap Insurance is Key: Again, gap insurance is crucial here. If the car is unrecoverable and the insurance payout doesn’t cover the loan, the difference is still owed. Without gap insurance, you’ll owe the lender this deficit, and continued non-payment will lead to defaults and potential legal action.

Here’s a look at how the process generally unfolds:

| Scenario | Car Recovered? | Insurance Action | Loan Status | Your Responsibility |

|---|---|---|---|---|

| Car Stolen | Yes, minor damage | Covers repairs (minus deductible) | Continue monthly payments | Pay deductible; resume payments |

| Yes, major damage | Covers repairs (minus deductible) or may declare total loss | Continue monthly payments (or lender/insurer decides) | Pay deductible; resume payments, or negotiate settlement | |

| Car Stolen | No | Pays Actual Cash Value (ACV) to lender | Loan settled by insurance payout | Pay deductible; potential loan deficiency if ACV < loan balance (covered by Gap Ins. if you have it) |

Frequently Asked Questions (FAQs) About Financed Cars Being Stolen

Q1: Do I still owe money on my car loan if it’s stolen?

A1: Yes, you generally continue to owe money on your car loan. The loan is a contract. Your insurance payout will go towards settling the debt, but until then, payments are typically still required.

Q2: What if my car is stolen and never found?

A2: If your car isn’t recovered, your comprehensive insurance will pay its actual cash value to your lender. If that amount doesn’t cover your entire loan balance, you’ll be responsible for paying the difference (the deficiency), unless you have gap insurance.

Q3: Do I need to keep making payments while the police are looking for my car?

A3: Yes, unless your lender explicitly tells you otherwise. It’s best to confirm this directly with them. Continuing to make payments prevents damage to your credit score.

Q4: What is gap insurance and do I need it if my financed car is stolen?

A4: Gap insurance covers the difference between what your insurance pays out (the car’s actual cash value) and what you still owe on your loan if it’s totaled or stolen. It’s highly recommended for financed cars, especially those that depreciate quickly, to avoid owing money after a theft.

Q5: How long does it take for insurance to pay out if my car is stolen?

A5: The timeline varies, but typically it involves a waiting period to see if the car is recovered (often 2-4 weeks). Once it’s declared unrecoverable, the claims process can take several more weeks depending on the insurer and complexity.

Q6: What happens if the insurance payout is more than what I owe on the loan?

A6: If the insurance payout exceeds the remaining loan balance, the lender will receive payment for the full loan amount, and you will receive the remaining surplus money.

Q7: Can I buy a new car while mine is still considered stolen or being processed by insurance?

A7: You can, but it’s advisable to wait until the insurance claim is settled and your loan situation is resolved. Buying a new car before this could complicate finances and insurance coverage.

Conclusion

Losing a financed car to theft is a distressing experience, but knowing the process can help you navigate it more smoothly. The key actions are immediate reporting to the police and your lender, followed by filing an insurance claim. Your comprehensive insurance coverage is designed to mitigate the financial loss, but understanding its limits, deductibles, and the role of gap insurance is vital. Always maintain open communication with your loan provider and insurance company. By staying informed and acting promptly, you can work towards resolving the situation and regaining your financial footing. Remember to explore preventative measures to keep your vehicle safe and secure.