Why Interest Rates Are Higher for Used Cars

It can feel tricky when you’re trying to figure out why interest rates seem higher for used cars. Many people find this topic confusing when they first look into it. This is totally normal and we’re here to make it easy.

We’ll walk you through it step by step, so you know exactly what’s going on. Get ready to learn everything you need to know to feel confident about your car buying decisions.

Understanding Used Car Interest Rates

This section will explain the core reasons behind the difference in interest rates between new and used cars. We’ll explore the fundamental principles that lenders consider when setting these rates. Understanding these factors is key to grasping why used car loans often come with higher financial costs.

This knowledge empowers you to make smarter decisions when looking for a vehicle.

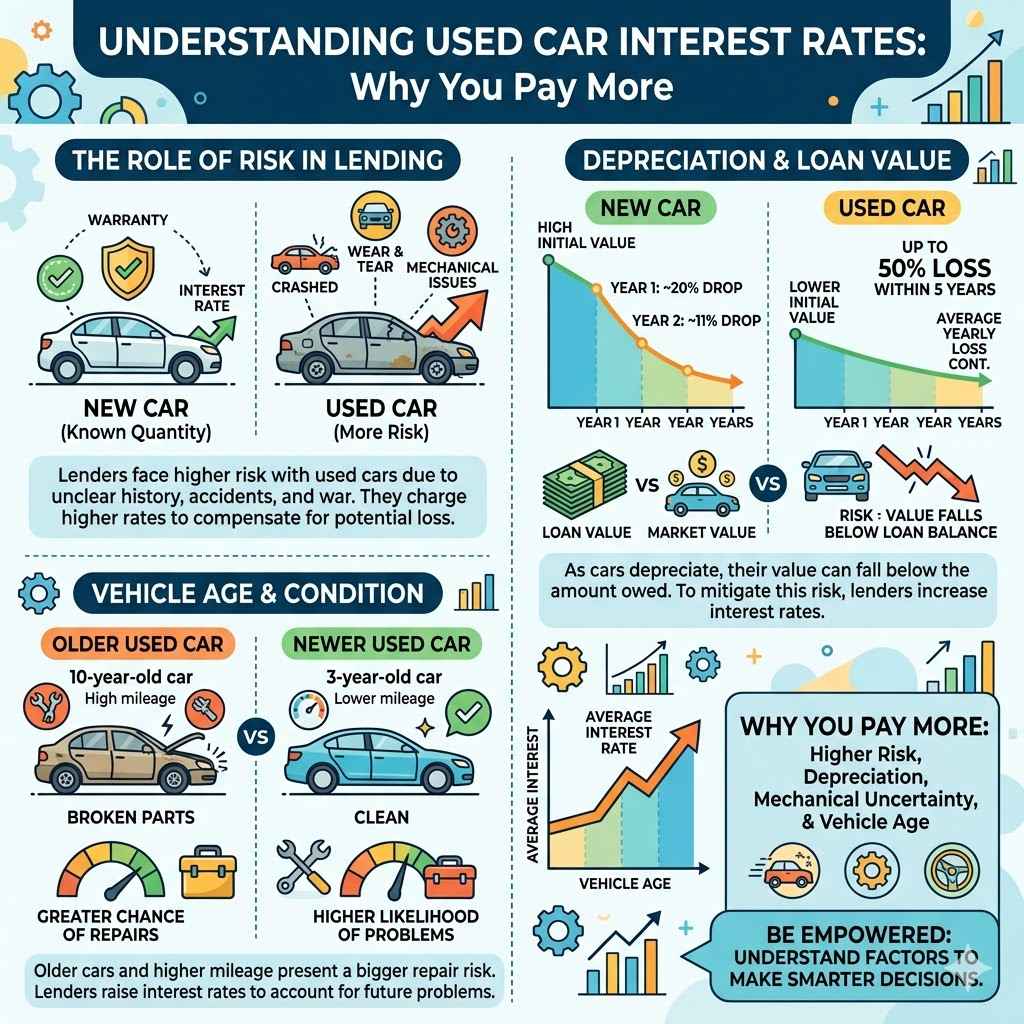

The Role of Risk in Lending

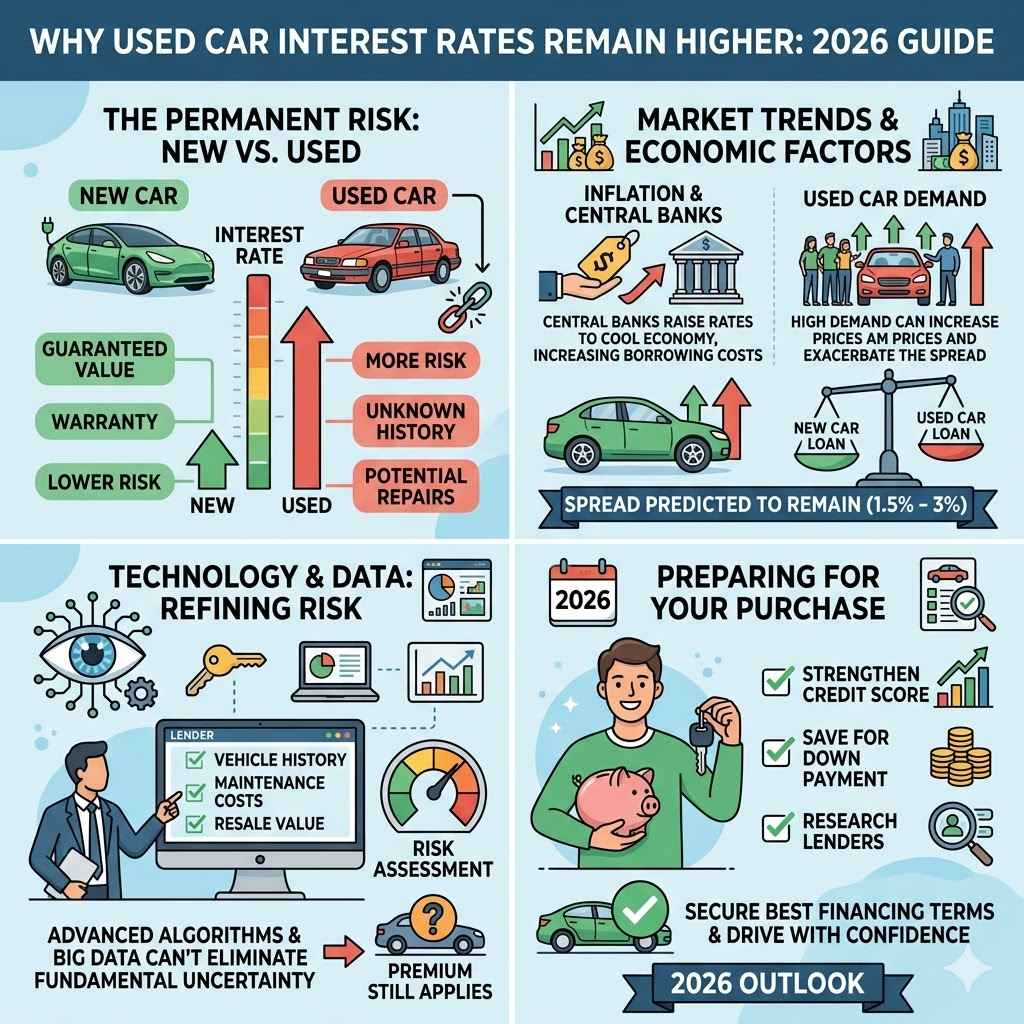

Lenders look at the potential for losing money when they offer loans. This is called risk. When lending money for a used car, there’s generally more risk for the lender compared to a brand new car.

A new car is a known quantity with a full warranty. A used car, however, has a history that isn’t always perfectly clear. This history can include past accidents, wear and tear, and potential mechanical issues that might arise sooner than with a new vehicle.

Because of this increased risk, lenders charge a higher interest rate. They do this to protect themselves against the possibility that the car might not hold its value as well as expected, or that it might require unexpected repairs that the borrower can’t afford. The higher interest rate acts as compensation for the lender taking on this greater chance of financial loss.

It’s a way for them to ensure they still make a profit even if things don’t go perfectly with the loan.

Think of it like this: if you were to lend a friend a brand new tool, you’d feel pretty confident it would work well for a long time. If you lent them an older, well-used tool, you might worry it could break soon. You’d probably ask for a little extra back to cover that worry.

That’s similar to how lenders view used cars.

Depreciation and Loan Value

Cars lose value over time, a process called depreciation. New cars depreciate the fastest in their first few years. However, even used cars continue to depreciate.

Lenders are concerned about the loan-to-value ratio, or LTV. This ratio compares how much you’re borrowing to how much the car is actually worth.

If a used car depreciates quickly, its market value can drop below the amount owed on the loan. This creates a situation where the lender is owed more money than the car is worth. If the borrower stops paying, the lender might not be able to recover all their money by selling the car.

This is a significant risk. To offset this, they charge a higher interest rate on used car loans. The higher rate helps the lender recoup potential losses more quickly.

For example, a car that’s five years old might lose 10% of its value in the next year. A brand new car might lose 20% in its first year, but it starts from a much higher initial value. The risk for the lender is that the older car’s value is already lower, making it more susceptible to falling below the outstanding loan balance with continued depreciation.

This makes lenders cautious.

Statistical data often shows that the average depreciation for a car in its first year can be around 20%, and up to 50% within the first five years. For used cars, the rate of depreciation slows down but continues. This sustained loss of value is a primary driver for higher interest rates on these vehicles.

Vehicle Age and Condition

The age and general condition of a used car play a big part in the interest rate offered. Older cars, or those with higher mileage, are generally seen as having a greater chance of needing repairs. This is because their mechanical parts have been used more and are closer to the end of their lifespan.

A lender might look at a car’s age and decide it’s more likely to break down. If a car breaks down, it might not be worth as much, and the borrower might have trouble making payments if they also have repair bills. To compensate for this increased likelihood of mechanical issues and associated risks, lenders increase the interest rate.

They are essentially pricing in the potential for future problems.

For instance, a 10-year-old car with 150,000 miles will likely have a higher interest rate than a 3-year-old car with 30,000 miles. This is a direct reflection of the perceived risk associated with the older vehicle’s condition and potential for future maintenance costs. Lenders use vehicle history reports and inspections to help assess this risk, but age and mileage are strong indicators.

A report from the automotive industry indicated that vehicles over seven years old, on average, tend to have a 1.5% higher interest rate compared to vehicles between one and three years old when financed through a traditional auto loan. This shows a clear correlation between vehicle age and the cost of borrowing.

Factors Influencing Used Car Loan Rates

Beyond the car itself, several other factors related to the loan and the borrower can affect interest rates. These elements combine with the inherent risks of lending on a used vehicle to determine the final rate you’ll be offered. Understanding these components helps you see the full picture of what goes into setting an interest rate.

Credit Score of the Borrower

Your credit score is one of the most significant factors lenders consider when deciding on an interest rate for any loan, including used car loans. A credit score is a number that represents how likely you are to repay borrowed money. It’s based on your history of paying bills, how much debt you have, and other financial behaviors.

If you have a high credit score (generally 700 or above), it signals to lenders that you are a reliable borrower who pays debts on time. This reduces their risk. Therefore, you’ll likely qualify for lower interest rates.

Conversely, if you have a lower credit score, lenders see you as a higher risk. They might believe you’re more likely to miss payments or default on the loan. To compensate for this increased risk, they will charge you a higher interest rate.

For example, someone with excellent credit might get an interest rate of 5% on a used car loan, while someone with poor credit might be offered 15% or more. This difference can amount to thousands of dollars in extra interest paid over the life of the loan. It’s crucial to know your credit score before you start looking for a car loan.

According to recent industry data, borrowers with credit scores above 740 typically receive interest rates that are 2-3% lower than those with scores between 660 and 739. For scores below 600, interest rates can be 5-8% higher than the national average for used car loans.

Loan Term and Amount

The length of the loan, known as the loan term, and the total amount you borrow also influence the interest rate. Longer loan terms generally mean you pay interest over a more extended period, which can lead to paying more interest overall, even if the annual rate seems reasonable. Lenders sometimes offer slightly higher rates for longer terms because there’s more time for economic conditions to change or for unforeseen issues to arise with the borrower or the vehicle.

Similarly, very large loan amounts can sometimes carry slightly higher rates due to the increased capital at risk for the lender. Conversely, smaller loan amounts might also see slightly higher rates because the lender’s profit margin is smaller, and they need to make that profit worth their effort. However, the impact of the loan term is often more pronounced than the loan amount on the interest rate.

Let’s consider two scenarios for a $15,000 used car loan. A 36-month loan at 7% interest would have a monthly payment around $466 and a total interest cost of about $1,656. A 72-month loan at 8% interest would have a monthly payment around $259 but a total interest cost of about $3,648.

The longer term results in a significantly higher total interest payment due to the extended period of paying interest.

Down Payment Size

The size of your down payment is another critical factor. A larger down payment reduces the amount you need to borrow, which lowers the loan-to-value (LTV) ratio. As mentioned earlier, a lower LTV is less risky for the lender.

When you put more money down, you’re showing the lender you’re more committed to the purchase and you have equity in the vehicle from the start.

This reduced risk often translates into a lower interest rate. Lenders see a substantial down payment as a sign of financial responsibility and a buffer against depreciation. It means that even if the car loses some value, you’re less likely to owe more than the car is worth.

This can make lenders more comfortable offering you a better rate.

For example, if you are buying a $20,000 car and make a 20% down payment ($4,000), you’re only financing $16,000. This $16,000 loan will likely have a lower interest rate than if you made only a 5% down payment ($1,000) and financed $19,000. The difference in risk for the lender is substantial.

A study found that buyers who put down 20% or more on a used car loan often qualified for rates that were up to 0.5% to 1% lower than those who made smaller down payments, especially when financing through dealerships.

Why Are Interest Rates Higher for Used Cars? 2026 Guide Implications

This section directly addresses the core question of why interest rates are higher for used cars and how this understanding impacts your car buying plans, particularly looking ahead. It synthesizes the previous points to provide a clear perspective on the financial landscape of purchasing pre-owned vehicles. This knowledge is essential for planning effectively for future car acquisitions.

The Lender’s Perspective

From a lender’s viewpoint, offering a loan for a used car presents a more complex risk profile than a loan for a new vehicle. New cars come with manufacturer warranties, standardized production quality, and predictable depreciation curves, especially in their initial years. This predictability allows lenders to forecast potential outcomes with greater accuracy.

Used cars, however, are a different story. Their past maintenance history might be incomplete, they carry the mark of previous use and potential wear and tear, and their future reliability is less certain. The risk of unexpected mechanical failures increases with age and mileage, which can lead to expensive repairs for the owner and, potentially, loan defaults if the owner cannot afford both.

Additionally, the resale value of used cars can be more volatile. Market demand, accident history, and even cosmetic condition can significantly impact how much a used car is worth at any given time. If the car’s value drops below the outstanding loan balance, the lender faces a loss if they have to repossess and sell the vehicle.

To account for these elevated risks, lenders charge higher interest rates. This higher rate is a form of compensation for taking on this greater financial uncertainty.

Consider a scenario where a used car loan is approved for a vehicle that is five years old. The lender anticipates that this car has already experienced significant depreciation and is more prone to needing repairs than a new car. They factor in the possibility that the car’s market value might decline faster than expected or that the borrower may face unexpected repair costs.

This leads them to set a higher interest rate to cover these potential downsides and ensure profitability.

The Impact on Buyers

For buyers, higher interest rates on used cars translate directly into higher monthly payments and a greater total cost of ownership over the life of the loan. This means that when comparing the total expense of buying a new car versus a used car, the interest paid on a used car loan can be substantial. Buyers need to factor this into their budget planning.

For example, a $20,000 loan for a new car at 6% interest over 60 months would have a monthly payment of about $387 and a total interest cost of roughly $3,220. The same $20,000 loan for a used car at 9% interest over 60 months would have a monthly payment of about $415 and a total interest cost of around $4,900. The difference of nearly $1,700 in interest can be significant for a buyer’s finances.

This financial reality highlights the importance of shopping around for the best interest rates, negotiating terms, and understanding all the associated costs. Buyers should be aware that the sticker price of a used car is not the only expense; the interest accrued over the loan period is a major component of the overall cost. Thorough research and preparation are key to mitigating the impact of these higher rates.

A 2023 survey revealed that approximately 70% of used car buyers finance their purchases. Of those, the average interest rate was noted to be around 8.5%, which is significantly higher than the average rate for new car loans at that time, typically falling between 4.5% and 5.5%. This gap underscores the financial implications for consumers.

Strategies for Lowering Used Car Loan Rates

Despite the general trend of higher rates for used cars, buyers can employ several strategies to secure more favorable terms. These strategies focus on reducing the perceived risk for lenders and demonstrating financial responsibility. By taking proactive steps, you can potentially lower the interest rate you are offered.

Improve Your Credit Score Before Applying. A strong credit score is your most powerful tool for getting lower interest rates. Focus on paying all bills on time, reducing outstanding debt, and avoiding opening too many new credit accounts before applying for a car loan. A few months of diligent credit management can make a significant difference.

For instance, if your credit score is currently 640, and you manage to raise it to 680 through consistent on-time payments and debt reduction, you might see your potential interest rate drop by 1-2%. This can save you hundreds, if not thousands, of dollars over the loan’s duration.

Make a Larger Down Payment. As discussed, a substantial down payment reduces the loan-to-value ratio, making the loan less risky for the lender. Aim for at least 20% down if possible. This not only lowers your monthly payments but can also signal to lenders that you are financially stable and serious about the purchase, potentially leading to a better rate.

Imagine buying a $15,000 car. A 10% down payment ($1,500) means financing $13,500. A 20% down payment ($3,000) means financing $12,000.

The loan for $12,000 is less risky for the lender, and you might receive an interest rate that’s 0.5% to 1% lower than what you’d get for the $13,500 loan.

Shop Around for Lenders. Don’t accept the first loan offer you receive, especially from the dealership. Compare rates from multiple sources, including banks, credit unions, and online lenders. Each lender has different risk appetites and pricing models, so you might find a much better rate by simply comparing offers. Even a small difference in interest rate can save you a lot of money.

For example, Lender A might offer 8% on a used car loan, while Lender B offers 7.2%, and Lender C offers 6.8%. By obtaining quotes from all three, you could potentially save hundreds of dollars in interest over a typical loan term. It pays to do your homework and get multiple pre-approvals.

Consider Shorter Loan Terms. While a shorter loan term means higher monthly payments, it generally results in a lower overall interest rate and less total interest paid. If your budget allows for the higher monthly payments, opting for a shorter term can be a financially sound decision in the long run, reducing the amount of time the lender is exposed to risk.

A $15,000 loan at 7% interest would cost about $291 per month for a 60-month term, with total interest of $2,460. The same loan at 7% for a 48-month term would cost about $350 per month, but the total interest would be only $1,800. You pay more each month but save significantly on total interest.

Looking Ahead: Why Are Interest Rates Higher for Used Cars? 2026 Guide

As we project towards 2026, the fundamental reasons why interest rates are higher for used cars are expected to remain consistent. Lenders will continue to assess risk based on depreciation, vehicle age and condition, and borrower creditworthiness. The economic climate, inflation, and the Federal Reserve’s monetary policies will influence overall interest rate trends, but the inherent differences between new and used vehicles in terms of risk will likely persist.

Market Trends and Economic Factors

Economic factors such as inflation, interest rate policies set by central banks, and overall consumer confidence significantly impact auto loan rates for both new and used cars. When inflation is high, central banks often raise interest rates to cool down the economy, which consequently increases the cost of borrowing across the board. This means that even the base rate for used cars, which is already higher due to risk factors, could climb.

Market demand for used cars also plays a role. If demand is very high, especially if it outstrips the supply of new vehicles, lenders might see less risk as the cars are more likely to maintain value. However, supply chain issues that impact new car production can also drive up demand and prices for used cars, potentially creating a more competitive lending environment for these vehicles as well.

The automotive market is dynamic. For example, during periods of high demand for used cars, such as those experienced post-pandemic due to new car shortages, interest rates for used vehicles could see upward pressure due to increased competition among buyers and sustained lender demand for borrowers. This indicates that market forces can exacerbate the existing rate differences.

A recent analysis from financial forecasting firms suggests that by 2026, while overall interest rates might stabilize or adjust based on economic conditions, the spread between new and used car loan rates is predicted to remain. This spread is generally expected to be between 1.5% and 3% higher for used vehicles, reflecting the ongoing assessment of risk by financial institutions.

The Role of Technology and Data

Technology and the increased availability of data are helping lenders refine their risk assessments. Advanced algorithms can analyze vast amounts of information on vehicle history, repair costs, resale values, and driver behavior to provide more precise risk profiles for both vehicles and borrowers. While this could theoretically lead to more accurate pricing, it doesn’t eliminate the fundamental risks associated with used vehicles.

For instance, sophisticated vehicle history reporting services and predictive analytics allow lenders to better understand the potential future maintenance needs of specific makes and models. This data might help them differentiate more finely between high-risk and lower-risk used vehicles, potentially leading to more tailored rates within the used car segment.

However, even with advanced data, the inherent uncertainty of a pre-owned asset means that a premium will likely continue to be charged. The technological advancements primarily serve to quantify and manage the existing risks rather than eliminate them. This means that while pricing might become more nuanced, the general principle of higher rates for used cars is likely to endure.

The automotive finance industry is increasingly adopting AI-driven credit scoring models. These models can process more variables than traditional methods, offering a potentially more granular view of borrower risk. While promising, the core factors driving used car loan rates—depreciation and potential for wear and tear—remain dominant in these models.

Preparing for Your Next Used Car Purchase

To best prepare for purchasing a used car in the coming years, focus on strengthening your financial position. Work on improving your credit score, saving for a larger down payment, and researching lenders to find the most competitive rates. Understanding the “Why Are Interest Rates Higher for Used Cars?

2026 Guide” principles allows you to approach your car purchase with informed expectations and strategies.

By being a well-prepared and informed buyer, you can navigate the used car market more effectively and secure the best possible financing terms. This proactive approach will help you save money and drive away with confidence in your purchase, knowing you’ve made a smart financial decision.

Frequently Asked Questions

Question: Are interest rates for used cars always higher than for new cars?

Answer: Generally, yes. Lenders perceive used cars as higher risk due to depreciation, potential wear and tear, and less predictable maintenance needs. This higher risk typically leads to higher interest rates compared to new cars.

Question: Can I get a good interest rate on a used car if I have bad credit?

Answer: It can be challenging, but not impossible. Lenders see bad credit as high risk. You might face very high interest rates or may need a co-signer.

Focusing on improving your credit score is the best long-term strategy.

Question: How much of a down payment is considered “large” for a used car loan?

Answer: A down payment of 20% or more is generally considered large. It significantly reduces the loan-to-value ratio, lowering the risk for the lender and potentially earning you a better interest rate.

Question: Should I get pre-approved for a used car loan before visiting a dealership?

Answer: Absolutely. Getting pre-approved from a bank or credit union gives you a baseline interest rate and loan amount. This empowers you to negotiate better terms with the dealership and avoid impulse decisions.

Question: Will the interest rates for used cars go down in the future?

Answer: Overall interest rate trends depend on economic factors. While rates might fluctuate, the underlying reasons for used cars having higher rates than new cars—like depreciation and risk—are likely to remain, meaning a gap will probably persist.

Summary

Higher interest rates for used cars stem from increased lender risk due to depreciation, vehicle age, and condition. Your credit score, down payment, and loan term also play significant roles. By understanding these factors and preparing financially, you can secure better loan terms for your next used vehicle purchase.