Banks That Give Loans For Branded Title Cars Near You

Finding the right bank for a car loan can feel tricky sometimes, especially when you have a branded title. Many people run into problems because they don’t know where to start looking. It can seem like a big puzzle.

But don’t worry! This guide makes it simple. We will walk you through everything step by step.

Get ready to learn how to find the Banks That Give Loans for Branded Title Cars Near You with ease.

Finding Banks That Offer Branded Title Car Loans

This section helps you understand how to locate financial institutions that are open to lending for cars with branded titles. It’s important to know that not all banks have the same rules. Some are more flexible than others, especially when a car’s history isn’t perfect.

We will cover the types of lenders to look for and how they assess these loans differently. This knowledge is your first step to getting approved.

What Is A Branded Title?

A branded title means a vehicle has a history that’s flagged on its title document. This can happen for several reasons. The most common reasons include the car being in a major accident, flood damage, or theft recovery.

It could also be salvaged and rebuilt. This history doesn’t automatically mean the car is unsafe, but it does affect its value and how lenders see it.

When a car has a branded title, it’s considered a higher risk by many lenders. This is because the car’s market value is usually lower than a similar car with a clean title. Lenders worry that if you can’t pay back the loan, they might not get their money back by selling the car.

Why Are Branded Title Loans Challenging?

The main reason finding banks that lend for branded titles is tough is risk assessment. Traditional banks often have strict policies against lending on these vehicles. Their algorithms and loan officers might automatically reject applications for cars with a salvage or rebuilt title.

They prefer clear titles because they are easier to value and resell.

This doesn’t mean it’s impossible. It just means you need to look in the right places. You’ll likely need to explore options beyond the big national banks.

Credit unions and specialized auto loan companies are often more willing to work with borrowers who have branded title vehicles. They might have different ways of looking at the car’s condition and your financial situation.

Where To Start Your Search

Your search for Banks That Give Loans for Branded Title Cars Near You should begin with local institutions. Credit unions are often a great starting point. They are member-owned and tend to be more flexible with loan terms.

They often look at the overall financial health of their members rather than just a car’s title status.

Another good place to check is online lenders that specialize in subprime auto loans. These lenders are accustomed to working with borrowers who have less-than-perfect credit or are looking to finance vehicles with less common situations, like branded titles. Do your research to find reputable online lenders.

Understanding Loan Requirements For Branded Titles

Once you know where to look, it’s important to understand what these lenders will be asking for. Getting a loan for a branded title car often involves more scrutiny. Lenders want to ensure they are still making a sound investment.

We will break down the common requirements, from down payments to inspections. This will help you prepare your application and know what to expect.

Down Payment Requirements

Most lenders will require a larger down payment for a branded title car loan than for a clean title loan. This is to reduce their risk. A bigger down payment means you owe less money, and the lender has less to lose if you default.

You might see requirements for 10% to 25% of the car’s price as a down payment, sometimes even more.

Saving up for a substantial down payment is crucial. It shows the lender you are serious about the purchase and can financially commit. It also helps lower your monthly payments and the total interest you pay over the life of the loan.

If you can’t afford a large down payment, it might be harder to get approved.

Vehicle Inspections And Appraisals

Lenders often require a thorough inspection or appraisal of the branded title vehicle. This is to verify its current condition and safety. An independent mechanic’s report might be necessary.

The lender wants to make sure the repairs done after the branding event were done correctly and that the car is roadworthy.

This inspection is not just for the lender; it’s a vital step for you as a buyer too. It can uncover hidden problems that might not be obvious. A clean inspection report from a trusted mechanic can boost your chances of loan approval.

It provides objective evidence that the car is in good shape despite its history.

Credit Score And Financial History

While some lenders specialize in branded titles, your credit score and financial history still play a big role. A higher credit score generally means you are a lower risk, making it easier to get approved and secure better interest rates. Lenders will look at your credit reports to see your payment history, any past bankruptcies, and your debt-to-income ratio.

If your credit score is lower, you might still find options, but expect higher interest rates and potentially stricter terms. Some lenders might focus more on your current income and job stability to offset a lower credit score. It’s always a good idea to check your credit report before applying for a loan.

This helps you understand where you stand and address any errors.

Loan To Value Ratios

Lenders use Loan-to-Value (LTV) ratios to determine how much they are willing to lend. This is the ratio of the loan amount to the car’s value. For branded title cars, LTV ratios are typically lower than for clean title cars.

The lender wants to ensure the loan amount doesn’t exceed a certain percentage of the car’s reduced market value.

For example, a lender might offer an LTV of 80% for a clean title car but only 60% or 70% for a branded title car. This means if the car is valued at $10,000, the lender might only be willing to loan $6,000 to $7,000, requiring you to cover the rest with a down payment.

Types Of Lenders For Branded Title Auto Loans

Understanding the different types of financial institutions that might approve loans for branded titles can save you a lot of time and effort. Not all lenders are created equal, and some are much more suited to this specific need. We will explore the pros and cons of each, helping you decide where to focus your search for Banks That Give Loans for Branded Title Cars Near You.

Credit Unions

Credit unions are non-profit organizations owned by their members. They often have more flexible lending policies than large national banks. Because they are focused on serving their members, they may be more willing to consider individual circumstances, including loans for branded title vehicles.

Their decision-making process can be more personal. Loan officers might take the time to understand your situation, your credit history, and the specific car you’re interested in. This human touch can be invaluable when seeking non-traditional auto loans.

Many credit unions also offer competitive interest rates and lower fees.

Online Lenders

The rise of online lending has opened up new avenues for borrowers. Many online lenders specialize in auto loans, including those for vehicles with branded titles. These lenders often have streamlined application processes that can be completed entirely online.

They can also be quicker with approvals and funding.

However, it’s crucial to research online lenders thoroughly. Look for established companies with good reviews and transparent terms. Some online lenders might have higher interest rates to compensate for the higher risk.

It’s important to compare offers from several different online sources.

Dealership Financing

Some car dealerships have their own financing departments or work with a network of lenders who specialize in subprime or branded title loans. This can be a convenient option because you can often handle the car purchase and financing all in one place. However, dealership financing can sometimes come with higher interest rates or fees.

It’s important to be aware that dealerships may have incentives to approve loans, which can sometimes lead to less favorable terms for you. Always compare any dealership financing offer with pre-approved loans from other lenders, like credit unions or online companies, to ensure you’re getting the best deal.

Specialty Auto Loan Companies

There are companies that specifically focus on providing auto loans for buyers who might not qualify through traditional channels. This includes buyers looking for branded title cars or those with less-than-perfect credit. These companies understand the unique challenges of the used car market and are structured to handle them.

These lenders often have extensive experience in assessing the value and risk associated with branded title vehicles. They may employ specialized appraisal methods and work with experienced inspectors. While they offer a vital service, it’s important to scrutinize their interest rates and fees to ensure they are reasonable for the risk involved.

Banks That Give Loans for Branded Title Cars Near You

When searching for Banks That Give Loans for Branded Title Cars Near You, focus on local banks and credit unions first. These institutions might have more flexibility and a better understanding of the local market. They might also be more willing to meet with you in person to discuss your specific needs and the vehicle you want to finance.

Don’t limit yourself to the big national banks. Smaller, community-focused banks and credit unions are often your best bet. They can provide a more personalized experience and might be more open to considering applications that a larger institution would automatically reject.

A quick online search for “credit unions near me” or “local banks car loans” can be a good starting point.

Tips For Securing A Branded Title Car Loan

Getting approved for a branded title car loan requires a bit of preparation and smart strategy. By following some key tips, you can significantly improve your chances of success. This section will provide actionable advice to help you prepare your application and negotiate the best possible terms for your loan.

Get Pre-Approved Before Shopping

One of the most effective strategies is to get pre-approved for a loan before you even visit a dealership or find a specific car. This means you apply for a loan with a lender (like a credit union or online lender) and they give you an idea of how much you can borrow, at what interest rate, and for what term.

Having pre-approval gives you a clear budget. It also shows the seller that you are a serious buyer with financing already secured. This can give you more negotiating power when it comes to the car’s price.

You can focus on finding the right car, knowing your financing is already sorted.

Understand The Car’s History Thoroughly

Before you even think about a loan, you need to know everything about the car’s history. Use services like CarFax or AutoCheck to get a vehicle history report. This report will detail any accidents, title issues, mileage discrepancies, and previous owners.

Beyond the report, if possible, have a trusted, independent mechanic inspect the car. They can identify potential issues that might not show up on a report, especially if the car has been repaired after an accident. This thorough check is vital for both your safety and for satisfying lender requirements.

Be Prepared For Higher Interest Rates

It’s important to be realistic. Loans for branded title cars are considered higher risk, so you will likely face higher interest rates compared to loans for clean title vehicles. Understand that this is a common trade-off.

Your goal should be to find the lowest possible rate within the options available to you.

Shop around and compare loan offers from multiple lenders. Even a small difference in interest rate can save you a lot of money over the loan term. Always read the loan agreement carefully to understand the annual percentage rate (APR), fees, and repayment schedule.

Negotiate The Best Price For The Car

Since branded title cars are worth less than comparable clean title vehicles, you should aim to negotiate a lower purchase price. Use the vehicle history report and the mechanic’s inspection report as leverage in your negotiation. A car with a branded title should be priced accordingly.

Don’t be afraid to walk away if the price isn’t right. There are many cars on the market, and you may find a better deal elsewhere. Your goal is to get a fair price for a vehicle that meets your needs, even with its title history.

Build A Strong Financial Profile

Even if you are looking for a branded title loan, having a strong financial profile can significantly help. This includes having a good credit score, stable employment, and a reasonable debt-to-income ratio. If your credit isn’t perfect, focus on improving it before you apply.

Pay down existing debts, make all payments on time, and avoid opening new credit accounts just before applying. Showing lenders that you are financially responsible in other areas can make them more confident in lending to you for a branded title car.

Example Scenarios And Outcomes

Let’s look at a couple of real-life examples to see how these loans can work out. These scenarios will help illustrate the process and potential outcomes when seeking Banks That Give Loans for Branded Title Cars Near You. Understanding these examples can make the process feel more concrete and less intimidating.

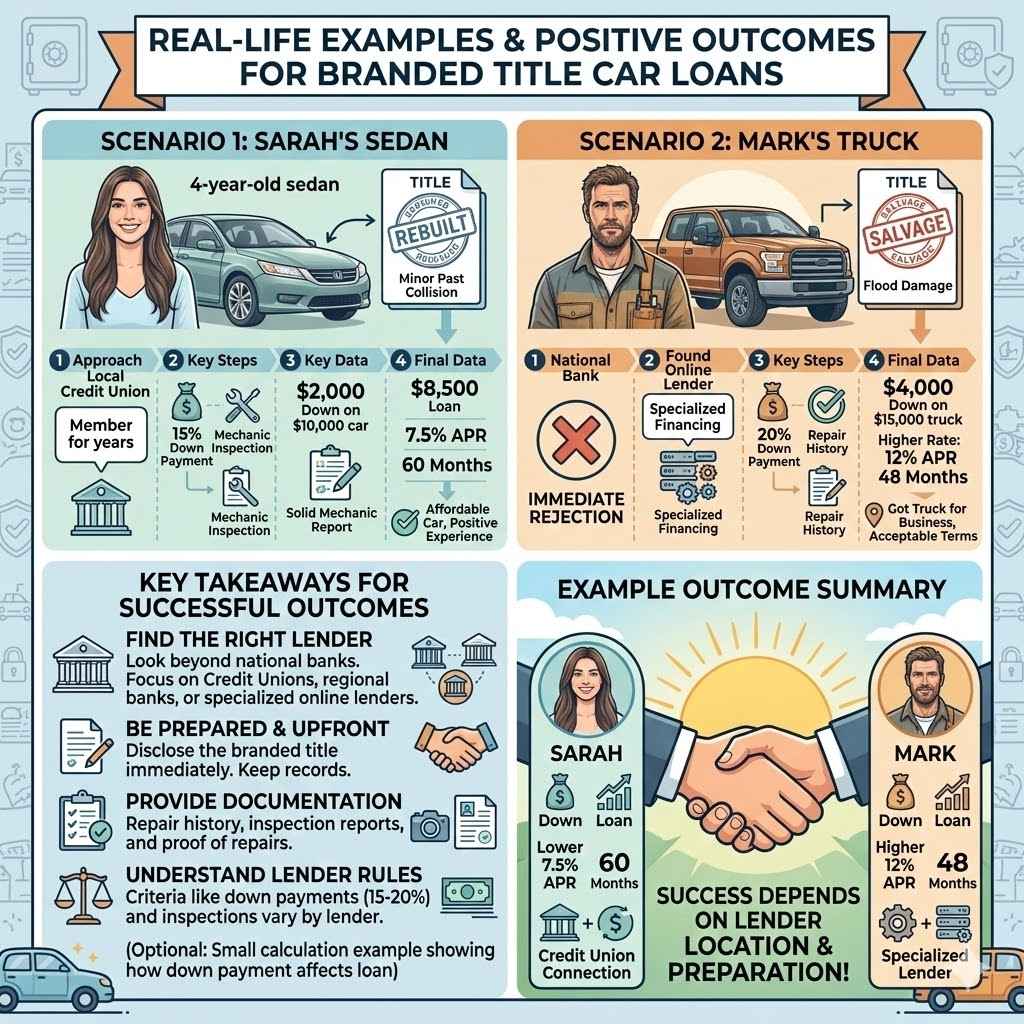

Scenario 1 Sarah’s Sedan

Sarah found a car she loved, a four-year-old sedan, but it had a “rebuilt” title due to a past minor collision. She approached her local credit union first, where she had been a member for years. They agreed to a loan, but required a 15% down payment and an inspection by a mechanic they trusted.

Sarah paid $2,000 down on a $10,000 car. The mechanic’s report confirmed the repairs were solid. The credit union approved her loan for $8,500 at 7.5% APR for 60 months.

Sarah ended up with a car she liked and could afford, thanks to her credit union’s willingness to work with her.

Scenario 2 Mark’s Truck

Mark needed a truck for his work and found one with a “salvage” title after a flood. He had a decent credit score but had some past late payments. He applied to a large national bank but was immediately rejected.

He then found an online lender that specialized in used car financing. This lender required a 20% down payment and a detailed history of repairs. Mark put down $4,000 on a $15,000 truck.

The lender approved him, but at a higher interest rate of 12% APR for 48 months. While the rate was higher, Mark got the truck he needed for his business.

Example Outcome For A Branded Title Loan

In both Sarah’s and Mark’s cases, the outcome was positive because they found lenders willing to consider their unique situations. Sarah benefited from a personal relationship with her credit union, leading to a lower interest rate. Mark, facing stricter lending criteria, found a specialized online lender that still met his needs, albeit at a higher cost.

The key takeaway is that success often depends on where you look and how well you prepare. Being upfront about the branded title, providing documentation, and understanding the lender’s requirements are crucial steps. These examples show that with the right approach, obtaining financing for a branded title vehicle is achievable.

Frequently Asked Questions

Question: Can I get a loan for any branded title car

Answer: It depends on the lender and the specific circumstances. Some lenders are more flexible than others. Lenders will evaluate the severity of the damage that led to the brand, the quality of repairs, and your financial situation.

Question: What is the difference between a salvage title and a rebuilt title

Answer: A salvage title means the vehicle has been declared a total loss by an insurance company due to severe damage. A rebuilt title means the vehicle was previously salvaged, but has since been repaired and inspected to be roadworthy again.

Question: Will my interest rate be higher for a branded title car loan

Answer: Yes, generally speaking, you can expect higher interest rates for branded title car loans because they are considered a higher risk by lenders.

Question: How much of a down payment do I need for a branded title car

Answer: Down payment requirements vary, but lenders often ask for a larger down payment on branded title cars, typically ranging from 10% to 25% or even more, to reduce their risk.

Question: Where can I find banks that give loans for branded title cars near me

Answer: Start by looking at local credit unions, community banks, and specialized online auto lenders. These institutions are often more willing to consider branded title vehicles than large national banks.

Conclusion

Finding the right bank for a branded title car loan is possible. Focus your search on credit unions and specialized lenders. Prepare by getting a pre-approval and understanding the car’s history.

Always compare offers and be ready for potential higher rates and down payments. You can get the car you need with the right preparation.